- Home

- »

- HVAC & Construction

- »

-

Facade Market Size, Share And Trends Report 2026-2033GVR Report cover

![Facade Market (2026 - 2033)Report]()

Facade Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Ventilated Facades, Non-ventilated Facades), By End Use (Commercial, Residential, Industrial), By Region (North America, Europe, Asia Pacific, Latin America, MEA), And Segment Forecasts

Market Size, 2025

$284.4BMarket Estimate, 2026

$296.0BMarket Forecast, 2033

$439.0BCAGR, 2026–2033

5.8%Facade Market Summary

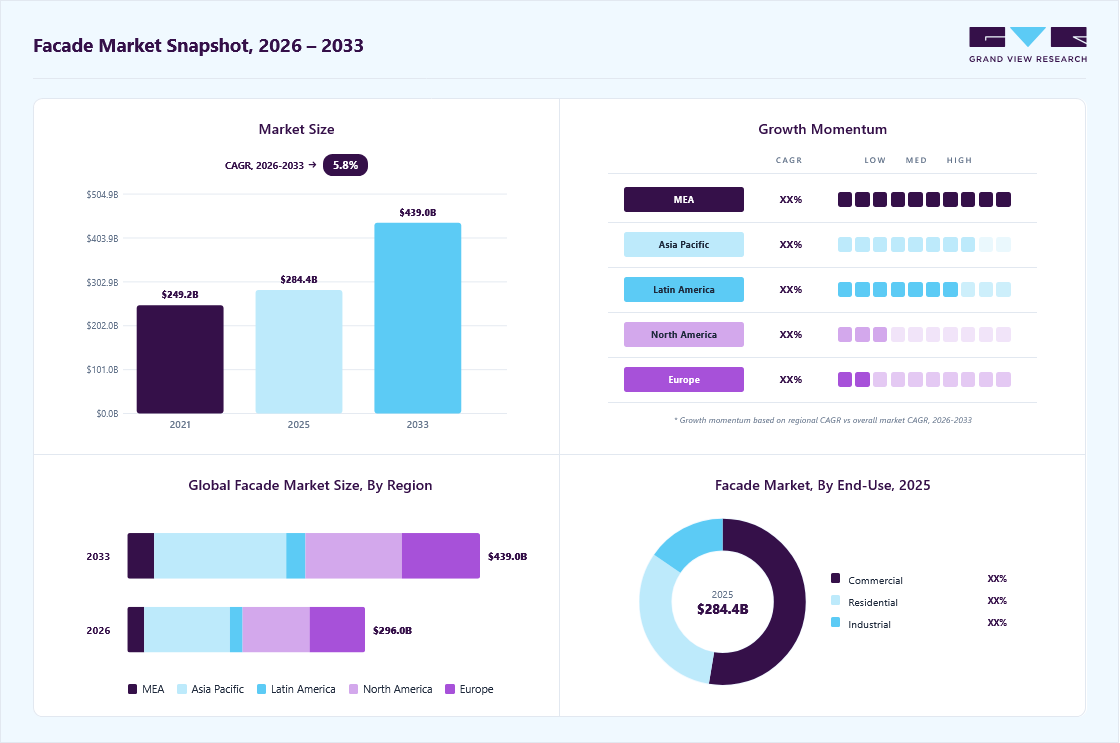

The global facade market size was valued at USD 284.4 billion in 2025 and is projected to grow from USD 296.0 billion in 2026 to USD 439.0 billion by 2033, at a CAGR of 5.8% from 2026 to 2033. The Asia Pacific held the largest share of 35.9% of the global market in 2025. This growth is driven by the expansion in global construction activity, particularly in urban and commercial infrastructure development.

Key Market Trends & Insights

- By product: Ventilated facades led the market with share of 46.0% in 2025.

- By end use: Commercial segment held the largest revenue share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (35.9% revenue share, 2025)

- By country: The China led the Asia Pacific market in 2025.

Market Size & Forecast

- Market size in 2025: USD 284.4 Billion

- Estimated market size in 2026: USD 296.0 Billion

- Projected market size by 2033: USD 439.0 Billion

- CAGR (2026-2033): 5.8%

Rapid urbanization and infrastructure development will drive growth in the façade systems market in the coming years. As populations shift toward cities, especially across the Asia Pacific, governments and private developers are investing heavily in residential housing, commercial complexes, airports, and public infrastructure. This surge in construction activity directly fuels demand for facade systems, which serve as the external envelope of buildings. Facades not only protect structures from environmental elements such as heat, rain, and wind but also enhance energy efficiency and aesthetic appeal. Modern architectural trends increasingly prioritize visually striking and high-performance exteriors, further boosting adoption. Consequently, expanding urban landscapes and large-scale infrastructure projects are significantly accelerating the growth of the global glass facade market.The market is evolving beyond traditional building exteriors toward multifunctional and energy-generating systems. A key emerging segment is the building integrated photovoltaics facade market, where solar panels are seamlessly incorporated into building envelopes. This trend is driven by rising demand for sustainable construction, net-zero buildings, and energy-efficient infrastructure, making facades both protective structures and renewable power sources.

")

Facades significantly influence a building’s energy performance by regulating indoor temperatures, managing solar heat gain, and reducing reliance on heating and cooling systems. As energy costs rise and environmental concerns intensify, governments worldwide are implementing stricter building codes and green certifications. This is accelerating the adoption of high-performance facade solutions such as double-skin facades and smart glazing, which enhance insulation, optimize natural light, and lower overall energy consumption in modern buildings.

The rising demand for green and net-zero buildings is creating strong opportunities in the facade industry. Facades play a crucial role in improving a building’s thermal performance, directly impacting energy consumption and efficiency. As sustainability targets become more stringent, developers are increasingly adopting advanced facade solutions. Technologies such as Building Integrated Photovoltaics (BIPV) and solar facades enable buildings to generate renewable energy while maintaining structural functionality. This integration of energy generation with building envelopes not only reduces carbon footprints but also enhances long-term cost savings and environmental performance.

Product Insights

The ventilated facades segment dominated the facade market, accounting for the largest revenue share of 46.0% in 2025. Growing retrofit and renovation activities are significantly boosting demand for ventilated facades, particularly in Europe and North America, where a large stock of aging buildings requires modernization. These systems provide an efficient solution to enhance thermal insulation and overall energy performance without the need for major structural alterations. By adding an external ventilated layer, buildings can achieve improved temperature regulation, reduced energy consumption, and extended lifespan. Additionally, ventilated facades enhance the visual appeal of older structures, aligning them with modern architectural standards. As governments push for energy-efficient renovations and stricter building regulations, the adoption of ventilated facades in retrofit projects continues to accelerate.

The non-ventilated facades segment is anticipated to grow at the fastest CAGR during the forecast period, driven by their strong demand from residential and mid-rise buildings. These systems are widely used in housing and low- to mid-rise structures, where advanced ventilation solutions are often unnecessary. In regions with stable climates and limited exposure to extreme weather, non-ventilated facades provide adequate protection, insulation, and durability at a lower cost. Their simplicity and cost-effectiveness make them ideal for large-scale housing developments. As a result, their widespread use across residential projects has created a substantial installed base globally, supporting steady growth in this segment.

End Use Insights

The commercial segment dominated the facade industry, accounting for the largest revenue share in 2025, driven by the rapid expansion of commercial infrastructure across emerging economies. Continuous development of office buildings, shopping malls, airports, hospitals, and hotels is increasing the need for advanced building envelopes. Emerging economies such as India, China, Brazil, and countries in the Middle East are experiencing significant growth in commercial construction due to urbanization and economic development. This surge directly boosts demand for facade systems that provide durability, energy efficiency, and modern aesthetics. As commercial projects grow in scale and complexity, the adoption of high-performance facade solutions continues to rise.

The residential segment is expected to grow at a significant CAGR during the forecast period. Rapid population growth and increasing migration to urban areas are creating strong demand for new housing. Governments and private developers are investing heavily in apartments, gated communities, and affordable housing projects. This expansion in residential construction directly increases the need for facade systems, which provide protection, insulation, and aesthetic appeal, thereby supporting steady growth in the segment.

Regional Insights

Asia Pacific Facade Market Trends

Asia Pacific dominated the global market with the largest revenue share of 35.9% in 2025, driven by large-scale smart city developments and mega infrastructure projects across countries like India, China, and Southeast Asia. Governments are investing heavily in integrated urban infrastructure, including transport hubs, business districts, and mixed-use developments, all of which require advanced facade systems, thereby driving significant demand across the region.

The Japan facade market is expected to grow rapidly in the coming years, driven by seismic resilience requirements in building design. Facade systems must be engineered to withstand earthquakes, leading to the adoption of lightweight, flexible, and high-performance materials. This unique structural requirement drives continuous innovation and replacement demand, particularly in urban commercial and residential buildings.

The facade market in China held a substantial share in 2025, propelled by mass-scale urban redevelopment and vertical construction, with a strong focus on high-density urban centers. The government’s push for modern cityscapes and redevelopment of older urban zones is generating sustained demand for facade systems, particularly in high-rise and mixed-use developments.

North America Facade Market Trends

The North America facade industry held a significant global share in 2025. The growth is primarily driven by the large-scale retrofit and recladding of aging building stock, particularly across commercial and institutional infrastructure. A significant portion of buildings constructed decades ago now require upgrades to meet modern performance standards, including insulation, durability, and compliance with updated codes. This has created sustained demand for facade replacement and modernization projects, positioning retrofitting as a core market driver alongside new construction.

U.S. Facade Market Trends

The facade industry in the U.S. is expected to grow significantly at a CAGR of 5.1% from 2026 to 2033. The growth is strongly influenced by stringent building safety and fire regulations, particularly following high-profile building incidents. Authorities have tightened compliance requirements for materials, installation, and performance, prompting widespread replacement of outdated or non-compliant facade systems. This regulatory push is accelerating demand for certified, high-performance facade solutions across both new and existing buildings.

Europe Facade Market Trends

The facade industry in Europe is anticipated to register considerable growth from 2026 to 2033, driven by aggressive decarbonization targets and climate policies under regional sustainability frameworks. Governments are mandating energy-efficient building envelopes as part of broader carbon neutrality goals, pushing developers to adopt advanced facade systems. This regulatory environment is creating consistent demand for high-performance, environmentally compliant facade solutions across both residential and commercial sectors.

The UK facade market is expected to grow rapidly in the coming years. Developers and property owners are prioritizing fire-resistant and compliant facade systems, particularly in high-rise residential buildings. This safety-driven transformation has created a significant and ongoing pipeline of facade upgrade projects.

The facade market in Germany held a substantial share in 2025. Organizations in the German market are supported by strong industrial and engineering-driven construction standards that focus on precision, durability, and high-performance materials. The country’s emphasis on quality construction and advanced building technologies encourages the adoption of sophisticated facade systems, particularly in commercial and institutional buildings, driving steady and innovation-led market growth.

Key Facade Company Insights

Key players operating in the facadeindustry are Permasteelisa Group, Jangho Group, Yuanda China Holdings, Schuco International, AluK Group, JiangHong Group, YKK AP, Enclos Corp., Benson Curtain Wall & Glass, Kingspan Group, Apogee Enterprises, Alumil S.A., Saint-Gobain S.A, and Zahner Company. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In February 2026, Saint-Gobain S.A. launched COOL-LITE SKL 170, a highly selective solar control coating designed for complex facade systems. It is embedded in laminated glass and offers over 70% light transmission while reducing solar heat gain. The product enhances energy efficiency by controlling internal temperatures and lowering cooling loads. It also provides a neutral aesthetic and is suitable for advanced facade types, such as double-skin and closed-cavity facades, supporting both performance and design flexibility.

-

In August 2025, Permasteelisa Group and ALBADDAD Capital announced a strategic joint venture to strengthen facade project delivery in the Middle East. The collaboration focuses on establishing a dedicated curtain wall manufacturing facility in Dubai, combining Permasteelisa’s facade engineering expertise with ALBADDAD’s large-scale manufacturing capabilities. This partnership aims to enhance efficiency, accelerate project timelines, and create a strong regional player in glass and aluminum facade systems.

-

In January 2025, Permasteelisa Group announced the acquisition of key assets from Benson Industries to strengthen its presence in North America. Benson, a leading specialist in custom curtain wall and glass systems, brings strong engineering and project expertise. The deal significantly expands Permasteelisa’s regional footprint, particularly on the U.S. West Coast, while enhancing its technical capabilities and service offerings. The combined entity enables broader global resources and improved delivery for complex facade projects.

Key Facade Companies:

The following key companies have been profiled for this study on the facade market.

- AluK Group

- Alumil S.A.

- Apogee Enterprises

- Benson Curtain Wall & Glass

- Enclos Corp.

- Jangho Group

- JiangHong Group

- Kingspan Group

- Saint-Gobain S.A

- Schuco International

- YKK AP

- Yuanda China Holdings

- Zahner Company

Facade Market Report Scope

Report Attribute

Details

Market size in 2025

USD 284.4 billion

Market size in 2026

USD 296.0 billion

Revenue forecast in 2033

USD 439.0 billion

Growth rate

CAGR of 5.8% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report enterprise size

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Product, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

AluK Group; Alumil S.A.; Apogee Enterprises; Benson Curtain Wall & Glass; Enclos Corp.; Jangho Group; JiangHong Group; Kingspan Group; Saint-Gobain S.A.; Schuco International; YKK AP; Yuanda China Holdings; Zahner Company

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Facade Market Report Segmentation

This report forecasts volume & revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the facade market report based on product, end use, and region:

-

Product Outlook (Revenue, USD Billion, 2021 - 2033)

-

Ventilated Facades

-

Curtain Wall

-

Others

-

-

Non-ventilated Facades

-

Others

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Commercial

-

Residential

-

Industrial

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The global facade market size was valued at USD 284.4 billion in 2025 and is estimated at USD 296.0 billion for 2026.

Asia Pacific dominated with a 35.9% revenue share in 2025.

The commercial segment held the largest revenue share in 2025.

The global facade market is expected to grow at a CAGR of 5.8% from 2026 to 2033, reaching USD 439.0 billion by 2033.

The ventilated facades segment dominated the market and accounted for the revenue share of 46.0% in 2025. Growing retrofit and renovation activities are significantly boosting demand for ventilated facades, particularly in Europe and North America where a large stock of aging buildings requires modernization. These systems provide an efficient solution to enhance thermal insulation and overall energy performance without the need for major structural alterations.

Key players include AluK Group; Alumil S.A.; Apogee Enterprises; Benson Curtain Wall & Glass; Enclos Corp.; Jangho Group; JiangHong Group; Kingspan Group; Saint-Gobain S.A.; Schuco International; YKK AP; Yuanda China Holdings; Zahner Company.

Rapid urbanization and infrastructure development will help in the façade systems market growth in the coming years. As populations shift toward cities, especially across Asia-Pacific, governments and private developers are investing heavily in residential housing, commercial complexes, airports, and public infrastructure. This surge in construction activity directly fuels demand for facade systems, which serve as the external envelope of buildings.

About the Author(s)

HVAC & Construction Research Team

Technology · HVAC & ConstructionThis report was authored by the hvac & construction research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the hvac & construction segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.