- Home

- »

- Next Generation Technologies

- »

-

Fly-By-Wire Systems Market Size & Share Report 2026-2033GVR Report cover

![Fly-By-Wire Systems Market (2026 - 2033)Report]()

Fly-By-Wire Systems Market (2026 - 2033)

Size, Share & Trends Analysis Report By Technology (Digital, Analog), By Component (Flight Control Computers, Actuators, Cockpit controls, Sensors), By Application (Commercial Aviation, Military Aviation, Business Aviation), By Region, & Segment Forecasts

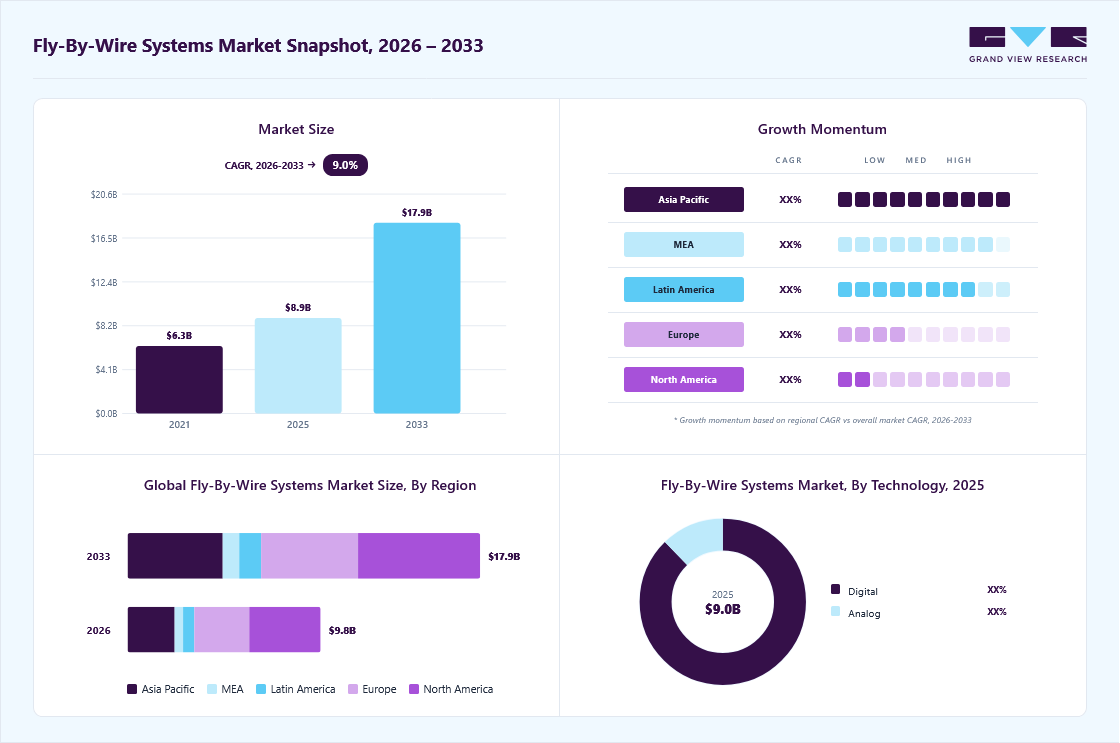

Market Size, 2025

$8.9BMarket Estimate, 2026

$9.8BMarket Forecast, 2033

$17.9BCAGR, 2026–2033

9.0%Fly-By-Wire Systems Market Summary

The global fly-by-wire systems market size was valued at USD 8.9 billion in 2025 and is projected to grow from USD 9.8 billion in 2026 to USD 17.9 billion by 2033, at a CAGR of 9.0% from 2026 to 2033. The market in North America dominated with a revenue share of 37.0% in 2025. The rising demand for fuel‑efficient and lightweight aircraft, the growing adoption of digital flight‑control technologies such as automation and machine‑learning‑enabled control precision, and the increasing production of commercial and military aircraft that require enhanced maneuverability, safety, and reliability are the key factors driving the fly-by-wire systems industry expansion.

Key Market Trends & Insights

- By technology: Digital segment held the largest market share of 87.0% in 2025.

- By component: Flight control computers segment held the largest market share in 2025.

- By application: Commercial aviation segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (37.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 8.9 Billion

- Estimated market size in 2026: USD 9.8 Billion

- Projected market size by 2033: USD 17.9 Billion

- CAGR (2026-2033): 9.0%

The market growth can be attributed to the aviation industry’s growing push for fuel‑efficient and lightweight aircraft. Fly-By-Wire (FBW) systems replace heavy mechanical and hydraulic linkages with electronic interfaces, reducing aircraft weight and improving operational efficiency. Airlines and manufacturers are investing in such systems to lower fuel consumption and meet stringent environmental regulations. This shift is reinforced by the ongoing transition toward More Electric Aircraft (MEA) architectures, where electronic flight control is a core technology.Additionally, the growing integration of sophisticated digital flight control computers, sensors, actuators, and automation features is accelerating FBW adoption. Modern aircraft increasingly require advanced stability augmentation, flight envelope protection, predictive control, and autopilot enhancement capabilities enabled by next‑generation FBW systems. Additionally, emerging technologies such as machine learning and adaptive control are improving real‑time data processing and control precision, supporting safer and more autonomous flight operations.

")

Furthermore, global aircraft production growth driven by rising air travel, fleet expansion, and defense modernization programs is fueling demand for FBW integration across commercial, military, and unmanned aviation platforms. Modern fleets require enhanced maneuverability, weight reduction, and automated control features, all of which rely heavily on FBW systems. As military aircraft emphasize precision, survivability, and electronic control reliability, defense procurement remains a major driver of the fly-by-wire systems industry.

Moreover, the shift toward autonomous, digitally optimized, and MEA platforms, where FBW serves as the foundational control architecture, is a key market trend. Aircraft manufacturers are increasingly adopting electronic interfaces to support semi‑autonomous and, in the future, fully autonomous flight systems. The move toward more electric aircraft, replacing hydraulic systems with electronic ones, further strengthens demand for fly-by-wire systems. This trend is supported by global regulatory bodies and government initiatives that are investing in modern aircraft design, which is expected to further drive the expansion of the fly-by-wire systems industry.

Technology Insights

The digital segment dominated the market, accounting for over 87% in 2025, driven by the aviation industry’s shift toward advanced avionics, automation, and enhanced flight safety. Digital FBW systems excel by delivering precise electronic control signals, slashing pilot workload through intuitive interfaces and automation aids, and offering layered redundancy that outperforms outdated mechanical or analog systems, which suffer from higher failure rates and greater maintenance demands.

The analog segment is expected to grow at a CAGR of 2.5% from 2026 to 2033, owing to its cost‑effectiveness, simpler architectures, and suitability for legacy aircraft platforms, training aircraft, and regions or operators with limited budgets for full digital upgrades. Demand is supported by continued manufacturing and retrofit activity in the commercial and military segments, where analog systems remain adequate for mission requirements, especially in environments that prioritize reliability over advanced automation. The rise in global aircraft production, expansion in regional aviation markets, and ongoing modernization programs is creating sustained demand for analog FBW, as these systems support improved maneuverability, reduced mechanical linkage weight, and better fuel efficiency compared to traditional hydromechanical controls.

Component Insights

The flight control computers segment dominated the market in 2025. Segmental growth is driven by rising demand for advanced automation, fleet modernization in commercial and military aviation, and the integration of AI for predictive maintenance and real-time decision-making. Key drivers include enhanced processing power from quad-core processors, embedded cybersecurity against network threats, and software-defined avionics enabling flexible upgrades with robust certification. Growth accelerates with electrification trends imposing thermal and supply chain demands, alongside surging UAV applications and regulatory pushes for safety redundancy.

The sensors segment is projected to grow at the fastest rate from 2026 to 2033. The segment is gaining traction, driven by the need for precise sensor fusion, lightweight materials reducing aircraft weight, and advancements in collision avoidance for autonomous operations. Trends feature AI-driven data processing for maneuverability in next-gen fighters, multi-sensor integration for UAVs, and rising defense budgets funding hypersonic compatibility. Commercial growth stems from fuel efficiency mandates and Asia-Pacific fleet expansions, while military retrofits emphasize agility amid geopolitical shifts.

Application Insights

The commercial aviation dominated the market in 2025, driven by surging air passenger traffic, fleet modernization programs, and demand for fuel-efficient aircraft like those from Boeing and Airbus. The growing integration of AI for enhanced automation, reduced pilot workload through advanced flight envelope protection, and lightweight materials for better sustainability and emissions compliance are the key factors accelerating the market growth. Rising orders for next-gen jets in regions such as Asia-Pacific further accelerate adoption amid stringent safety regulations.

The military aviation segment is expected to register a significant CAGR from 2026 to 2033, fueled by the modernization of fleets, the need for superior maneuverability in combat, and rising defense budgets globally. Trends emphasize cybersecurity enhancements, AI-driven sensor fusion for precision strikes, and compatibility with unmanned systems amid geopolitical tensions. Retrofitting legacy platforms and developing agile fighters, such as next-gen programs, bolster this segment's momentum.

Regional Insights

North America accounted for the largest market share of over 37% in 2025. The regional market growth is driven by rapid technological advancements in digital flight‑control systems, strong aerospace manufacturing capabilities, and significant demand for advanced aircraft across commercial and defense sectors. The region leads in adopting next‑generation FBW technologies, supported by major industry players and ongoing modernization initiatives that prioritize fuel efficiency, automation, and enhanced safety.

U.S. Fly-By-Wire Systems Market Trends

The U.S. fly-by-wire systems market accounted for the largest share of over 84% in 2025, fueled by high aircraft production volumes, extensive defense procurement, and strong R&D investments. The market growth in the U.S. is further strengthened by FAA‑backed modernization initiatives focused on efficiency, automation, and reduced pilot workload.

Europe Fly-By-Wire Systems Market Trends

The Europe fly-by-wire systems market is expected to grow at a CAGR of over 8% from 2026 to 2033, driven by increasing demand for safer, more efficient aircraft, a mature aerospace industry, and strong emphasis on next‑generation flight control systems. Regional manufacturers prioritize reduced weight, improved fuel efficiency, and enhanced automation, with ongoing R&D investments and strict aviation safety regulations accelerating the adoption of FBW systems across commercial and military fleets.

The UK fly-by-wire systems market is rapidly growing, driven by advanced aerospace capabilities and rising investments in flight‑control innovation, driven by commercial aviation needs and defense modernization programs. Emphasis on digital flight‑control upgrades, enhanced automation, and precision maneuverability supports broader adoption of FBW technologies across aircraft programs.

The Germany fly-by-wire systems market is expected to grow at a significant rate in the coming years, supported by its strong engineering ecosystem, extensive aircraft manufacturing activities, and increasing integration of advanced avionics in both commercial and defense sectors. Continued modernization, focus on automation, and adoption of digital flight‑control systems drive demand for FBW technologies across the country’s aerospace programs.

Asia Pacific Fly-By-Wire Systems Market Trends

The fly-by-wire systems market in the Asia Pacific is expected to grow at the fastest rate of over 10% from 2026 to 2033. The region is seeing rapid growth driven by rising aerospace manufacturing capabilities, fleet expansion, and growing demand for technologically advanced aircraft. Countries across the region are rapidly adopting digital flight‑control systems, driven by increased air‑travel growth, airline modernization efforts, and rising defense investments.

The China fly-by-wire systems market is expanding rapidly due to strong growth in domestic aircraft production, increased investments in advanced avionics, and rising adoption of automation‑driven flight‑control technologies. The country’s expanding commercial aviation sector and strategic push toward indigenous aircraft development continue to boost FBW system demand.

The Japan fly-by-wire systems market is growing in popularity, driven by its focus on high‑precision aerospace engineering, modernization of both civil and defense aircraft fleets, and increasing integration of digital flight‑control and safety‑enhancing technologies. The country’s participation in advanced aircraft programs and its commitment to next‑generation avionics fuel continued adoption of FBW technologies.

Key Fly-By-Wire Systems Company Insights

Some of the key players in the fly-by-wire systems market include Thales Group and Honeywell International, Inc.

-

Thales Group offers FlytRise eFCC flight control computers, SEC/ELAC/FAC systems for Airbus A320 family, Bombardier CRJ/Global, and Gulfstream G700/800, plus full FBW integration for eVTOLs. As the world's largest FBW supplier with 40+ years equipping 12,000+ aircraft, Thales pioneered digital FBW on A310/A320 and leads commercial aviation through envelope protection, weight savings, and certification tools, recently expanding via Safran partnerships and eVTOL wins such as SkyDrive and JetZero.

-

Honeywell International Inc. offers Primus Autopilot 2000 flight computers, FBW systems for Boeing 777/787, and urban air mobility/eVTOL controls. A mature market leader, Honeywell dominates flight computers across commercial/military platforms, reducing pilot workload via sensor fusion and automation while driving fuel efficiency; their innovations hold a strong share in wide-body and next-gen electric aircraft programs.

Collins Aerospace and Liebherr-International AG are some of the emerging market participants in the market.

-

Collins Aerospace (RTX) offers fly-by-wire actuators, pilot controls, and IFCE systems for Boeing 777X plus hybrid-electric propulsion integration. As an emerging challenger, Collins leverages RTX defense expertise for commercial narrow/wide-body upgrades and eVTOL growth, securing key Boeing contracts to challenge incumbents in sustainable high-agility platforms.

-

Liebherr-International AG offers electric/hydraulic FBW actuators and damage-tolerant actuation systems for Airbus, Boeing, and regional jets. Emerging as a precision specialist, Liebherr focuses on weight reduction for green aviation, targeting next-gen programs with modular designs that enhance reliability and envelope protection in sustainable aircraft fleets.

Key Fly-By-Wire Systems Companies:

The following key companies have been profiled for this study on the fly-by-wire systems market.

- Thales Group

- Honeywell International Inc.

- Safran Group

- BAE Systems plc

- Moog Inc.

- Raytheon Technologies Corporation

- Collins Aerospace

- Liebherr-International AG

- Parker Hannifin Corp.

- Lockheed Martin Corporation

Recent Developments

-

In November 2025, Thales Group announced the first successful flight of SkyDrive's eVTOL secured by its next-generation FlytRise flight control system. FlytRise is Thales' next-generation fly-by-wire (FBW) flight control system, specifically designed for eVTOLs, with electronic signaling for control surfaces and thrust.

-

In October 2025, Sikorsky, a Lockheed Martin company, unveiled the S-70UAS U-Hawk, a fully autonomous Black Hawk UAS featuring third-generation fly-by-wire controls integrated with MATRIX autonomy Digital.

-

In December 2024, BAE Systems plc was selected to provide actuator control units (ACUs) and active control sticks for JetZero's blended wing body aircraft demonstrator.

Fly-By-Wire Systems Market Report Scope

Report Attribute

Details

Market size in 2025

USD 8.9 billion

Estimated market size in 2026

USD 9.8 billion

Projected market size by 2033

USD 17.9 billion

Growth rate

CAGR of 9.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD Billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Technology, component, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; India; Japan; South Korea; Australia; Brazil; Saudi Arabia; UAE, South Africa

Key companies profiled

Thales Group; Honeywell International Inc.; Safran Group; BAE Systems plc; Moog Inc.; Raytheon Technologies Corporation; Collins Aerospace; Liebherr-International AG; Parker Hannifin Corp.; Lockheed Martin Corporation

Customization scope

Free report customization (equivalent to up to 8 analyst working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Fly-By-Wire Systems Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For the purpose of this study, Grand View Research has segmented the global fly-by-wire systems market report on the basis of technology, component, application, and region:

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Digital

-

Analog

-

-

Component Outlook (Revenue, USD Million, 2021 - 2033)

-

Flight control computers

-

Actuators

-

Cockpit controls

-

Sensors

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Commercial Aviation

-

Military Aviation

-

Business Aviation

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

North America dominated with a 37.0% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The flight control computers segment held the largest revenue share in 2025, while the sensors segment is the fastest-growing.

The commercial aviation segment held the largest revenue share in 2025, while the military aviation segment is the fastest-growing.

The global fly-by-wire systems market size was valued at USD 8.9 billion in 2025 and is projected to reach USD 9.8 billion in 2026.

The global fly-by-wire systems market is expected to grow at a compound annual growth rate (CAGR) of 9.0% from 2026 to 2033 to reach USD 17.9 billion by 2033.

By technology, digital accounted for the largest revenue share of over 87% in 2025, driven by the aviation industry’s shift toward advanced avionics, automation, and enhanced flight safety, as digital FBW systems provide precise control, reduced pilot workload, and superior redundancy compared to legacy architectures.

Some of the key players operating in the market include Thales Group, Honeywell International Inc., Safran Group, BAE Systems plc, Moog Inc., Raytheon Technologies Corporation, Collins Aerospace, Liebherr-International AG, Parker Hannifin Corp., and Lockheed Martin Corporation.

The rising demand for fuel‑efficient and lightweight aircraft, the growing adoption of digital flight‑control technologies such as automation and machine‑learning‑enabled control precision, and the increasing production of commercial and military aircraft that require enhanced maneuverability, safety, and reliability are the key factors driving the fly-by-wire systems market growth.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.