- Home

- »

- Next Generation Technologies

- »

-

Generative Design Market Size And Share Report, 2026-2033GVR Report cover

![Generative Design Market (2026 - 2033)Report]()

Generative Design Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Software, Service), By Deployment Mode (Cloud-Based, On-Premises), By Application, By End Use (Automotive, Aerospace & Defense, Industrial Manufacturing), By Region, And Segment Forecasts,

Market Size, 2025

$377.8MMarket Estimate, 2026

$451.8MMarket Forecast, 2033

$1,586.0MCAGR, 2026–2033

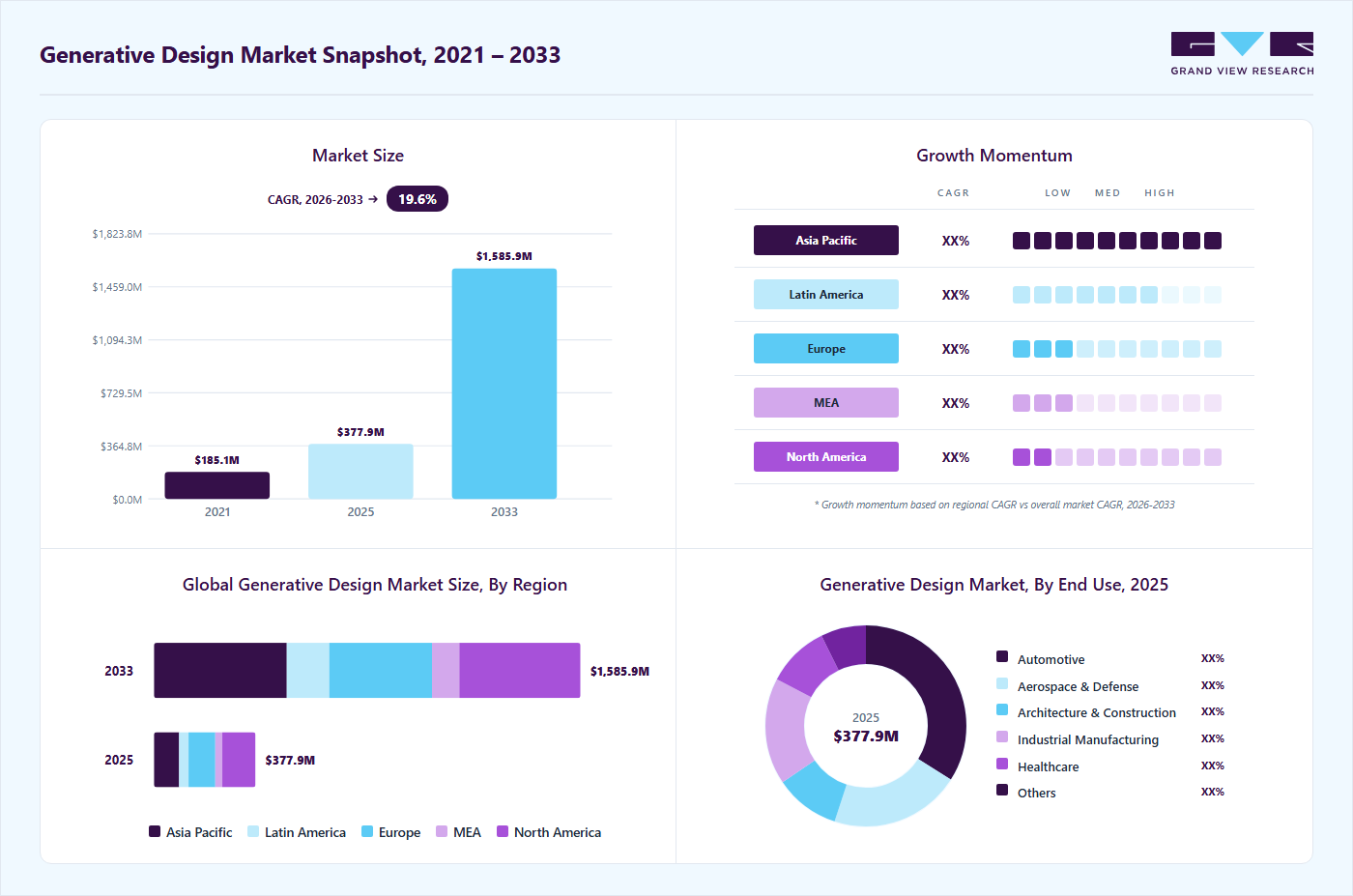

19.6%Generative Design Market Summary

The global generative design market size was valued at USD 377.8 million in 2025 and is projected to grow from USD 451.8 million in 2026 to USD 1,586.0 million by 2033, at a CAGR of 19.6% from 2026 to 2033. The North America market held the largest share of 32.7% of the global market in 2025. The industry is growing as the generative design is replacing traditional coding support tools by delivering contextual, real-time recommendations directly within development environments.

Key Market Trends & Insights

- By component: The software segment led the market and accounted for 78.7% of the global revenue in 2025.

- By deployment mode: The cloud-based segment accounted for the largest revenue share in 2025.

- By application: The topology optimization segment held the highest market share of the global revenue in 2025.

- By end use: The automotive segment accounted for the largest revenue share in 2025.

Regional Highlights

- Largest regional market: North America (32.7% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S.held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 377.8 Million

- Estimated market size in 2026: USD 451.8 Million

- Projected market size by 2033: USD 1,586.0 Million

- CAGR (2026-2033): 19.6%

The generative design industry is driven by the growing integration of artificial intelligence into engineering and manufacturing workflows as AI enhances productivity, supports complex decision-making, and improves efficiency across product development processes. These capabilities enable organizations to generate optimized designs with reduced material usage and improved performance, strengthening the role of generative design tools market in industrial applications. The increasing focus on efficiency and precision in manufacturing and designing continues to accelerate the adoption of generative design software. As industries aim to improve operational outcomes, generative design becomes a key component in digital engineering strategies.Another major driver is the advancement of generative AI and its application in research, innovation, and the generative design software market. Generative technologies enable automated design exploration, reduce development timelines, and support innovation across sectors. These technologies allow engineers to evaluate multiple design alternatives simultaneously, improving accuracy and reducing manual intervention. The ability to integrate simulation, testing, and optimization into a unified workflow enhances design quality and accelerates product development cycles with the help of generative design software. This trend supports the expansion of generative AI in design market across industries requiring high-performance and customized solutions.

")

In addition, increasing digital transformation initiatives and government support for AI adoption are contributing to market growth. AI-driven technologies improve research and development efficiency and contribute to economic growth through innovation. Expanding investments in digital infrastructure and engineering capabilities across emerging economies are further supporting the adoption of generative AI in design market. Industries are incorporating generative design to address evolving requirements for customization, sustainability, and cost efficiency. The combination of policy support, technological advancement, and industrial demand continues to shape the growth curve of the generative design industry.

Component Insights

The software segment led the market and accounted for 78.7% of the global revenue in 2025. Advanced algorithms integrated within design platforms support the creation of multiple design iterations based on predefined constraints, improving efficiency and accuracy. Such software tools enhance decision-making and reduce design cycle time. For instance, in June 2024, TestFit announced the launch of Generative Design, a computational AI tool that automates site plan generation for real estate development, such as floor area ratio, parking ratio, and yield on cost, to deliver optimized designs for multi-family, industrial, and other building typologies.

The service segment is predicted to foresee significant growth in the forecast period, due to the rising need for specialized expertise in implementing generative design solutions. Organizations require consulting, integration, and support services to effectively incorporate these tools into existing engineering workflows. Training and customization services are also gaining importance as companies focus on optimizing design processes and improving operational efficiency. In addition, companies seek customization services to focus on generative design solutions according to specific industry requirements and performance criteria.

Deployment Mode Insights

The cloud-based segment accounted for the largest revenue share in 2025, due to its ability to provide scalable computational resources required for complex generative design processes. Organizations are increasingly adopting cloud solutions to enable real-time collaboration across distributed teams, improving design efficiency and coordination. Integration with AI-driven tools and simulation environments further enhances the effectiveness of cloud-based generative design software workflows. Additionally, reduced upfront infrastructure costs and flexible subscription models contribute to wider adoption of generative design tools across both large enterprises and Topology Optimization.

The on-premises segment is predicted to foresee significant growth in the forecast period. On-premises deployment remains relevant in organizations that prioritize data security, intellectual property protection, and strict regulatory compliance. Industries such as aerospace, defense, and healthcare continue to rely on internal infrastructure to maintain control over sensitive design data. Existing legacy systems and established IT environments also support the continued use of on-premises solutions in certain enterprises. These deployments offer greater customization and integration with proprietary engineering workflows.

Application Insights

The topology optimization segment held the highest market share of the global revenue in 2025, driven by the increasing demand for lightweight and high-performance components across industries such as automotive and aerospace. This approach enables engineers to remove excess material while maintaining structural integrity, resulting in improved efficiency and reduced production costs. Integration with simulation tools enhances accuracy in evaluating stress, load distribution, and material performance, supporting the growth of the generative design applications.

The design automation segment is predicted to foresee significant growth in the forecast period, driven by the increasing need to reduce manual intervention and accelerate engineering workflows. Organizations are adopting automated design processes to generate multiple design iterations quickly, improving efficiency and reducing development time. The integration of artificial intelligence enables systems to analyze constraints and optimize designs with minimal human input. Growing complexity in product requirements across industries further supports the use of automated design tools for accurate and consistent outcomes.

End Use Insights

The automotive segment accounted for the largest revenue share in 2025. The automotive sector is a major adopter of generative design due to the increasing focus on lightweight components and improved fuel efficiency. Manufacturers are using generative design to optimize structures, reduce material consumption, and enhance vehicle performance. For instance, in September 2025, Qualcomm Technologies and HARMAN announced a collaboration to advance generative‑AI‑enabled cockpit solutions for the automotive sector, integrating Qualcomm’s high‑performance automotive compute platforms with HARMAN’s Ready product portfolio and central‑compute architectures.

The healthcare segment is projected to grow significantly over the forecast period, driven by the need for customized and patient-specific solutions. The technology enables the development of optimized medical devices, implants, and prosthetics focused on individual anatomical requirements. For instance, in March 2024, NVIDIA Healthcare, to advance drug discovery, MedTech, and digital health, launched generative AI microservices. Tools such as BioNeMo for biomolecular AI and MONAI for medical imaging help with accurate protein structure prediction, molecular generation, and 3D medical visualization.

Regional Insights

North America dominated the market, accounting for 32.7% of revenue share in 2025. North America’s generative design market is driven by the strong presence of advanced engineering and software ecosystems across industries. Organizations in the region are actively integrating generative design within digital product development to improve design accuracy and reduce time-to-market. High investment in research and development supports continuous innovation in design tools and computational capabilities. The region also benefits from early adoption of cloud-based engineering platforms that enhance collaboration and scalability.

U.S. Generative Design Market Trends

The generative design market in the U.S. is driven by continuous advancements in artificial intelligence and high-performance computing technologies. Companies are incorporating generative design into product innovation strategies to enhance performance and reduce development complexity. The presence of leading technology providers supports the rapid integration of advanced design capabilities into engineering processes. Strong focus on innovation across sectors encourages the adoption of next-generation design methodologies. This supports the expansion of generative design applications across diverse industries.

Europe Generative Design Market Trends

The generative design market in Europe is supported by its well-established industrial base and emphasis on sustainable manufacturing practices. Companies are increasingly adopting design optimization tools to reduce material usage and meet stringent environmental standards. The region’s focus on precision engineering and advanced production techniques encourages the use of generative design in complex applications. Strong collaboration between industry and research institutions further supports technological advancement. This environment promotes the integration of generative design into modern engineering workflows.

Asia Pacific Generative Design Market Trends

The generative design market in Asia Pacific is expected to witness the highest CAGR over the forecasted period, due to expanding industrialization and increasing digital transformation initiatives. The region is witnessing rising adoption of advanced design tools across manufacturing and infrastructure development projects. Growing availability of skilled engineering talent supports the implementation of AI-driven design solutions. Increasing demand for cost-efficient production methods encourages the use of optimized design approaches.

Key Generative Design Company Insights

Some key companies in the generative design industry are NVIDIA Corporation, Bentley Systems, Incorporated, Autodesk, Inc., and Hexagon AB.

-

NVIDIA focuses on accelerated computing and artificial intelligence technologies that support complex problem-solving across industries. The company develops advanced computing platforms, including GPUs and AI frameworks, that enable high-performance data processing and simulation. Its initiatives in AI extend across sectors such as healthcare, sustainability, and scientific research, where intelligent systems are applied to real-world challenges. NVIDIA also contributes to the development of digital twins and simulation environments that enhance design and engineering workflows.

-

Autodesk provides software solutions that support design, engineering, and manufacturing processes across a wide range of industries. Its platforms enable professionals to create, simulate, and optimize designs using advanced digital tools and integrated workflows. The company incorporates artificial intelligence to enhance productivity by automating repetitive tasks and improving decision-making throughout project lifecycles. Its solutions are applied across architecture, construction, manufacturing, and media sectors, enabling efficient project execution and collaboration. Autodesk also supports sustainable design practices through tools that analyze environmental impact and resource utilization.

Key Generative Design Companies:

The following key companies have been profiled for this study on the generative design market.

- Altair

- Arc Impact, Inc. (Desktop Metal)

- Autodesk, Inc.

- Bentley systems, incorporated

- Carbon, Inc. (ParaMatters)

- Dassault Systèmes

- Hexagon AB

- nTopology Inc.

- NVIDIA Corporation

- Siemens

Recent Developments:

-

In March 2026, Fujitsu launched Fujitsu Application Transform powered by Fujitsu Kozuchi, a generative AI service offered as SaaS in Japan. The service analyzes legacy source code, such as COBOL, and generates design documents, reducing production time by 97% compared to manual methods.

-

In January 2026, Siemens collaborated with NVIDIA to integrate AI across product design and engineering to manufacturing, operations, and supply chains. The initiative combines NVIDIA’s AI infrastructure, simulation libraries, models, and frameworks with Siemens’ industrial software, hardware, and digital‑twin capabilities to deliver AI‑accelerated solutions for product development, adaptive manufacturing sites, and AI‑driven electronic design automation.

-

In September 2023, Bentley Systems announced generative AI capabilities within OpenBuildings Designer CONNECT Edition, enabling civil site designers to produce concept designs rapidly from simple inputs like project briefs or sketches. The system generates compliant layouts for site elements, including roads, parcels, grading, drainage, parking, and utilities, while optimizing for constraints such as zoning regulations and environmental factors.

Generative Design Market Report Scope

Report Attribute

Details

Market size in 2025

USD 377.8 Million

Estimated market size in 2026

USD 451.8 million

Projected market size by 2033

USD 1,586.0 million

Growth rate

CAGR of 19.6% from 2026 to 2033

Base year for estimation

2025

Actual data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Component, deployment mode, end use, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

Altair; Arc Impact, Inc. (Desktop Metal); Autodesk, Inc.; Bentley systems, incorporated; Carbon, Inc. (ParaMatters); Dassault Systèmes; Hexagon AB ; nTopology Inc.; NVIDIA Corporation; Siemens

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Generative Design Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global generative design market report based on component, deployment mode, application, end use, and region.

-

Component Outlook (Revenue, USD Million, 2021 - 2033)

-

Software

-

Service

-

-

Deployment Mode Outlook (Revenue, USD Million, 2021 - 2033)

-

Cloud-Based

-

On-Premises

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Automotive

-

Aerospace & Defense

-

Architecture & Construction

-

Industrial Manufacturing

-

Healthcare

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Product Design & Development

-

Topology Optimization

-

Simulation & Testing

-

Design Automation

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

The software segment led with a 78.7% revenue share in 2025, while service is growing significantly.

The cloud-based segment held the highest market share in 2025. while on-premises is growing significantly.

The topology optimization segment held the highest market share in 2025, while design automation is growing significantly.

The automotive segment accounted for the largest share in 2025, while healthcare is growing significantly.

The global generative design market size was estimated at USD 377.8 million in 2025 and is expected to reach USD 451.8 million in 2026.

The global generative design market is expected to grow at a compound annual growth rate of 19.6% from 2026 to 2033 to reach USD 1,586.0 million by 2033.

North America dominated the generative design market with a share of 32.7% in 2025.

Some key players operating in the generative design market include Altair; Arc Impact, Inc. (Desktop Metal); Autodesk, Inc.; Bentley systems, incorporated; Carbon, Inc. (ParaMatters); Dassault Systèmes; Hexagon AB ; nTopology Inc.; NVIDIA Corporation; Siemens

Key factors include increasingly replacing traditional coding support tools by delivering contextual, real-time recommendations directly within development environments.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.