- Home

- »

- Pharmaceuticals

- »

-

Generic Pharmaceuticals Market Size Report, 2026-2033GVR Report cover

![Generic Pharmaceuticals Market (2026 - 2033)Report]()

Generic Pharmaceuticals Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (Simple Generics, Specialty Generics), By Application, By Product, By Route Of Administration, By Distribution Channel, By Region, And Segment Forecasts

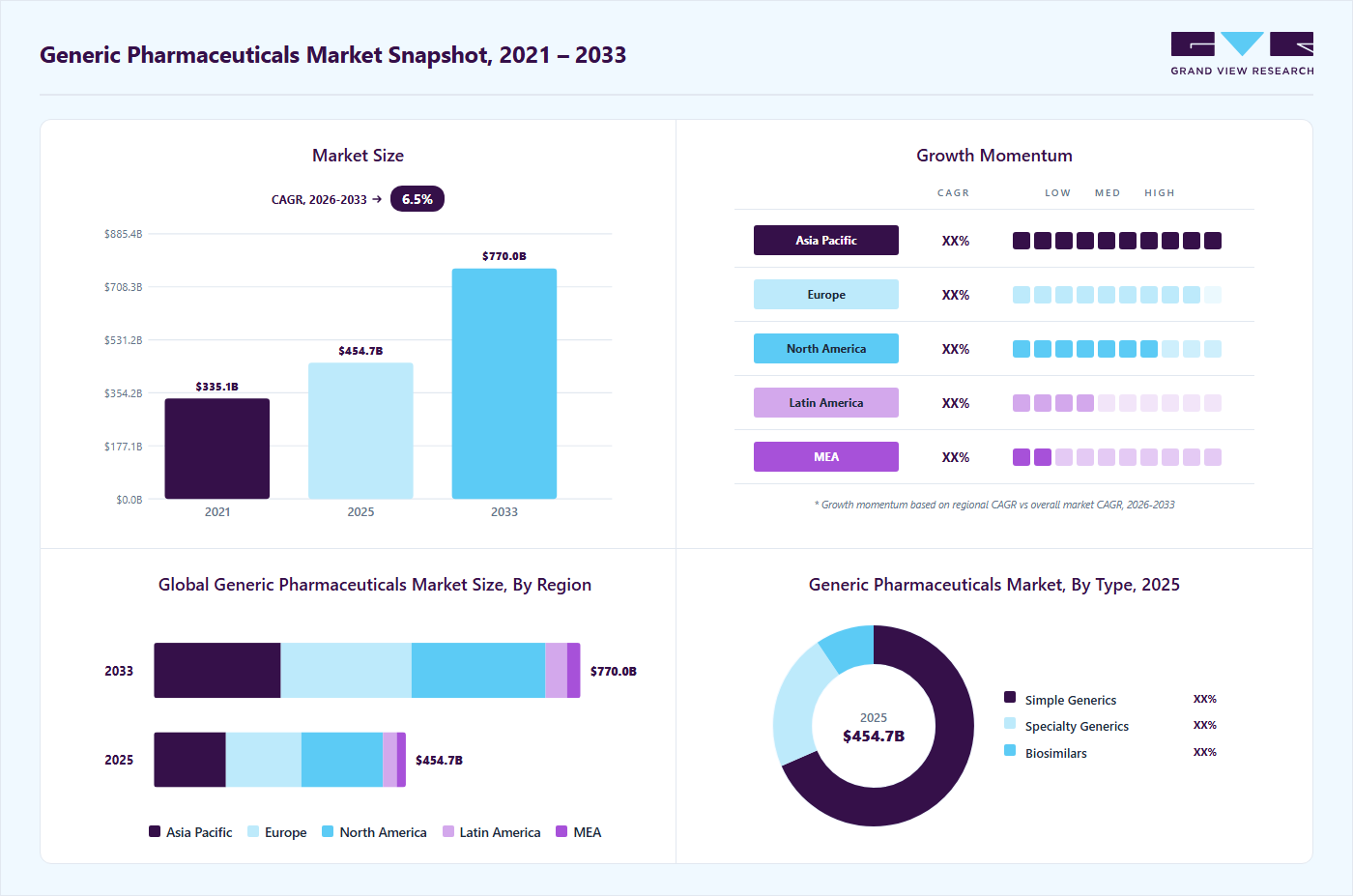

Market Size, 2025

$454.7BMarket Estimate, 2026

$495.7BMarket Forecast, 2033

$770.0BCAGR, 2026–2033

6.5%Generic Pharmaceuticals Market Summary

The global generic pharmaceuticals market size was valued at USD 454.7 billion in 2025 and is projected to grow from USD 495.7 billion in 2026 to USD 770.0 billion by 2033, at a CAGR of 6.5% from 2026 to 2033. The market in North America dominated with a revenue share of 32.4% in 2025. The growth can be attributed to the constant increase in the number of ANDA approvals and generic drug product launches.

Key Market Trends & Insights

- By product: Small molecule segment held the largest market share of 87.4% in 2025.

- By route of administration: Oral segment held the largest market share of 73.6% in 2025.

- By type: Simple generics segment held the largest market share of 68.3% in 2025.

- By distribution channel: Retail pharmacies segment held the largest market share of 51.9% in 2025.

- By application: Cardiovascular diseases segment held the largest market share of 25.3% in 2025.

Regional Highlights

- Largest regional market: North America (32.4% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 454.7 Billion

- Estimated market size in 2026: USD 495.7 Billion

- Projected market size by 2033: USD 770.0 Billion

- CAGR (2026-2033): 6.5%

The generic pharmaceuticals industry is a critical pillar of modern healthcare, enabling access to therapeutically equivalent alternatives to originator drugs following patent expiry. Generics are approved through abbreviated regulatory pathways (such as ANDA in the U.S.), which prioritize bioequivalence, safety, and quality while enabling faster market entry and supporting healthcare cost containment. In 2025, competitive dynamics remained driven by patent expirations and associated legal challenges. For example, litigation surrounding the generic version of Novartis’ heart failure drug Entresto led to a temporary pause on U.S. generic entry, underscoring how intellectual property disputes can materially influence launch timing despite patent expiry expectations.")

Manufacturers remained focused on portfolio expansion and regulatory execution. Alembic Pharmaceuticals secured multiple U.S. FDA approvals in 2025 across cardiovascular, oncology, ophthalmic, and dermatology products, highlighting ongoing diversification beyond commoditized oral solids and increasing emphasis on complex and specialty generics. Regulatory scrutiny remained a defining operational factor. Glenmark Pharmaceuticals received U.S. FDA warning letters regarding manufacturing practices in 2025, underscoring the importance of compliance discipline and quality assurance for sustained access to regulated markets.

Looking ahead, upcoming patent cliffs in high-value therapies continued to shape strategic positioning. The anticipated patent expiry of semaglutide was widely viewed as a significant future opportunity for generic manufacturers, particularly in India and other emerging markets, reflecting growing interest in metabolic and chronic disease segments. Overall, in 2025, the generic pharmaceuticals industry remained highly competitive and regulation-driven, balancing patent-linked entry opportunities, compliance requirements, pricing pressure, and supply reliability as manufacturers adapt to evolving therapeutic and policy environments.

Market Dynamics

The biggest driver of the generic pharmaceutical market is the expiration of branded drug patents, often referred to as the “patent cliff.” When patent protection ends, other pharmaceutical companies can manufacture and sell generic versions of the same medicines at much lower prices while maintaining the same quality, safety, and effectiveness. This increases the availability of affordable treatments, reduces healthcare costs, and creates major growth opportunities for generic drug manufacturers. For instance, in February 2026, Reuters reported that several Indian pharmaceutical companies, including Dr. Reddy’s Laboratories, Sun Pharmaceutical Industries, Zydus Lifesciences, and Natco Pharma, had prepared to launch generic versions of semaglutide in India following the expiry of Novo Nordisk’s patent in March 2026. Reuters further stated that Natco Pharma planned to introduce a generic semaglutide at a starting price of approximately USD15 per month, significantly lower than the branded products Ozempic and Wegovy, thereby expanding patient access and accelerating growth in the generic pharmaceutical market.

Stringent regulatory approval processes and compliance requirements are a major restraint on the generic pharmaceuticals market, as manufacturers must meet strict standards for bioequivalence, product quality, safety, and manufacturing practices set by regulatory authorities such as the U.S. FDA and the European Medicines Agency (EMA). These regulations increase operational costs, prolong product approval timelines, and create challenges for companies seeking to commercialize generic medicines across multiple international markets. For instance, in September 2024, the European Medicines Agency (EMA) recommended the suspension of more than 400 generic medicines tested by India-based Synapse Labs due to concerns regarding unreliable bioequivalence study data. The EMA stated that approximately 400 marketing authorizations linked to multiple pharmaceutical companies across the European Union were impacted, demonstrating how regulatory non-compliance can disrupt product availability and hinder growth in the global generic pharmaceuticals market.

The increasing demand for biosimilars is creating significant growth opportunities in the generic pharmaceuticals market, particularly as patents for several biologic drugs continue to expire globally. Biosimilars provide cost-effective alternatives to biologic medicines used the treat cancer, autoimmune disorders, diabetes, and other chronic diseases. Their adoption is rising due to rising healthcare costs, increasing patient demand for affordable therapies, and supportive regulatory approvals across major markets. In addition, pharmaceutical companies are expanding their biosimilar pipelines and manufacturing capabilities to strengthen their presence in this rapidly growing segment. For instance, in July 2024, Biocon Biologics announced the launch of YESAFILI, a biosimilar to aflibercept, in Canada after receiving regulatory approval from Health Canada. The company stated that the biosimilar was introduced for the treatment of multiple retinal disorders, including neovascular age-related macular degeneration and diabetic macular edema, expanding patient access to affordable biologic therapies and supporting growth opportunities in the global generic pharmaceuticals market.

Market Concentration & Characteristics

Innovation in the generic pharmaceuticals industry is primarily incremental rather than discovery-driven. The core focus lies in demonstrating bioequivalence, improving manufacturing efficiency, and optimizing formulations to meet regulatory standards. While traditional oral solid generics exhibit limited innovation, higher complexity is emerging in areas such as modified-release formulations, complex injectables, ophthalmic, and drug-device combinations. Process innovation, cost optimization, and regulatory strategy are more critical competitive levers than novel molecule development. As a result, innovation is largely execution-focused, emphasizing reliability, scalability, and compliance rather than breakthrough scientific advancement.

Barriers to entry in the generic pharmaceuticals industry are moderate and largely regulatory and operational. New entrants must demonstrate strict compliance with quality, safety, and bioequivalence requirements, which demands significant investment in manufacturing infrastructure and regulatory expertise. While intellectual property barriers are lower once patents expire, economic barriers persist due to intense price competition, tendering systems, and rapid price erosion. Established players benefit from scale, regulatory track record, and supply reliability, making sustained participation challenging for smaller or undercapitalized entrants.

Regulation has a high and direct impact on the generic pharmaceuticals industry, shaping product approvals, manufacturing operations, and market access. Regulatory agencies govern abbreviated approval pathways, manufacturing inspections, labeling, and post-marketing surveillance. Compliance failures can result in warning letters, import alerts, or supply disruptions, materially affecting business continuity. In addition, pricing controls, reimbursement policies, and tendering frameworks influence commercial outcomes in many markets. As a result, regulatory alignment and compliance discipline are strategic imperatives, with regulatory risk management playing a central role in long-term competitiveness.

The generic pharmaceutical industry is characterized by high product substitutability. Multiple manufacturers often supply therapeutically equivalent versions of the same molecule, enabling pharmacists, hospitals, and payers to switch products based on price and availability. Therapeutic interchangeability and reference pricing further intensify substitution dynamics. This high level of substitutability limits brand differentiation and reinforces price-based competition, particularly for mature molecules. Consequently, sustaining margins depend on operational efficiency, supply reliability, and portfolio breadth rather than product-level differentiation.

Geographical expansion is a key strategic lever for generic pharmaceutical manufacturers, particularly as mature markets experience pricing pressure and heightened competition. Companies increasingly pursue multi-regional regulatory approvals to diversify revenue streams and mitigate country-specific risks. Emerging markets offer growth potential driven by expanding healthcare access and rising demand for affordable medicines, while regulated markets provide scale and volume opportunities. However, expansion is constrained by localized regulatory requirements, pricing frameworks, and supply chain complexities, which require tailored market-entry strategies and strong regulatory capabilities.

Type Insights

The simple generics segment led the market with the largest revenue share of 68.32% in 2025, due to its broad therapeutic relevance, high prescription volumes, and mature manufacturing and regulatory pathways. Simple generics, largely oral solid dosage forms, are widely used in the long-term treatment of cardiovascular, metabolic, anti-infective, and central nervous system disorders, resulting in consistent demand and repeat prescribing. These products benefit from well-established bioequivalence requirements and standardized manufacturing processes, allowing faster approvals, lower development risk, and scalable commercialization across multiple markets.

In 2025, regulatory approvals continued to favor simple generics as manufacturers prioritized volume-driven portfolios. Companies such as Alembic Pharmaceuticals and Aurobindo Pharma received multiple US FDA approvals for oral solid formulations, reinforcing the dominance of simple molecules within generic pipelines. In addition, payer and pharmacy-level substitution policies consistently favor simple generics due to their interchangeability, reliable supply, and predictable pricing. FDA analyses have shown that increased competition among simple oral generics accelerates adoption and displacement of branded drugs, further supporting their revenue leadership relative to complex generics, which face higher development and manufacturing barriers.

The biosimilar segment is projected to grow at the fastest CAGR of 9.6% over the forecast period, driven by expanding biologics patent expirations, increasing payer acceptance, and greater regulatory clarity across major markets. As biologic therapies account for a growing share of treatment in oncology, immunology, and metabolic disorders, healthcare systems are increasingly promoting biosimilars to improve affordability and access. Unlike simple generics, biosimilars benefit from reference biologic-linked demand, higher baseline pricing, and longer treatment durations, which support stronger value growth.

This trajectory is reinforced by real-world developments as of 2025. Companies such as Sandoz and Celltrion continued to expand biosimilar approvals and launches across Europe and the United States, particularly in oncology and autoimmune indications. In parallel, policy actions by regulators and payers increasingly favor biosimilar substitution, with updated interchangeability guidelines and formulary incentives accelerating uptake. In addition, upcoming patent expiries of high-revenue biologics, including GLP-1 and monoclonal antibody therapies, are driving sustained pipeline investment, positioning biosimilars as the fastest-growing segment within the broader generics landscape.

Application Insights

The cardiovascular disease segment led the market with the largest revenue share of 25.34% in 2025, driven by high clinical demand and patent expiries on key products. The first generic versions of rivaroxaban (Xarelto) were approved by the U.S. FDA in early 2025, providing more affordable anticoagulant options for patients at risk of major cardiovascular events such as stroke and thrombosis, illustrating the strategic importance of cardiovascular generics in portfolio expansion.

Legal and patent developments also underscored cardiovascular market dynamics. In July 2025, a U.S. federal judge denied a bid by Novartis to block the launch of a generic version of its blockbuster heart failure drug Entresto, clearing the way for entry by competitors, a milestone event reflecting how patent expiries and litigation outcomes directly influence generic competition in high-value cardiovascular therapeutics. In addition, regulatory authorities continued to prioritize cardiovascular health through approvals and broader therapeutic policy, reinforcing the segment’s relevance within overall drug development and generic access strategies.

The cancer segment is projected to grow at the fastest CAGR of 11.3% over the forecast period, supported by increasing reliance on drug-based oncology treatments, sustained therapy durations, and expanding generic and biosimilar penetration across high-incidence cancers. Oncology care increasingly involves chronic or multi-line treatment regimens, including oral chemotherapies, injectables, and supportive drugs, which structurally favors volume and value expansion for generics once exclusivity lapses.

In the United States, the FDA approved multiple generic oncology injectables to address long-standing supply gaps, including generic versions of pemetrexed and fludarabine, underscoring the continued regulatory prioritization of cancer medicines. Separately, Europe saw expanded adoption of oncology biosimilars following procurement-led uptake of biosimilar trastuzumab and rituximab across national health systems, accelerating displacement of originator brands. In Asia, Chinese regulators advanced approvals for domestic generic oncology drugs targeting lung and colorectal cancers, reflecting growing regional manufacturing and self-sufficiency initiatives. In parallel, global oncology incidence continued to rise, with public health agencies reporting steady increases in diagnosed cancer cases, particularly in aging populations. Combined with payer-driven substitution policies and expanding treatment access in emerging markets, these factors position oncology as the fastest-growing therapeutic segment within the generic pharmaceuticals industry over the forecast period.

Product Insights

The small molecule segment led the market with the largest revenue share of 87.42% in 2025, due to its broad therapeutic applicability, mature regulatory pathways, and sustained reliance across chronic and acute disease management. Small molecules continue to underpin treatment protocols in cardiovascular, oncology, metabolic, anti-infective, and central nervous system indications, benefiting from oral bioavailability, scalable chemical synthesis, and well-established bioequivalence standards. These structural advantages support rapid commercialization, wide geographic reach, and high levels of pharmacy-level substitution, reinforcing the segment’s revenue leadership.

The U.S. Food and Drug Administration continued to grant first generic and advance approvals for small molecule drugs ahead of broad market entry, enabling manufacturers to prepare for immediate commercialization upon exclusivity expiry. For example, the FDA’s 2025 First Generic Drug Approvals included small-molecule oncology and chronic disease therapies, allowing approved applicants to secure early market positioning before broader competitive entry. Such advance approvals reduce launch risk, accelerate time-to-revenue, and further entrench small molecules as the preferred focus for generic portfolios.

The large molecule segment is projected to grow at the fastest CAGR of 12.4% over the forecast period, driven by accelerating biosimilar adoption, expanding biologics patent expirations, and increasing payer focus on cost containment for high-value specialty therapies. Large molecule drugs, including monoclonal antibodies and recombinant proteins, are increasingly central to treatment in oncology, immunology, endocrinology, and inflammatory diseases. As biologics are among the most expensive therapies in clinical use, healthcare systems are actively encouraging biosimilar uptake to improve affordability while maintaining therapeutic outcomes.

Regulatory agencies continued to strengthen and clarify biosimilar approval and interchangeability frameworks, reducing uncertainty for manufacturers and payers. In parallel, companies such as Samsung Bioepis and Biocon Biologics advanced regulatory approvals and commercial rollouts of large molecule biosimilars across the United States and Europe, particularly in oncology and autoimmune indications. These launches demonstrate increasing technical capability, regulatory confidence, and market readiness for complex biologic alternatives.

Route of Administration Insights

The oral segment led the market with the largest revenue share of 73.62% in 2025, due to its clinical convenience, strong patient adherence, and entrenched role in chronic disease management. Oral dosage forms remain the preferred option for long-term treatment of cardiovascular, metabolic, gastrointestinal, and central nervous system conditions, as they enable outpatient therapy without specialized administration. From a manufacturing and regulatory perspective, oral solids benefit from standardized bioequivalence requirements, predictable scale-up, and broad pharmacy-level substitutability, which together support rapid adoption and repeat prescribing.

The U.S. FDA continued to issue the first generic approvals for oral small-molecule drugs, reinforcing its regulatory prioritization of tablets and capsules for broad patient access. In parallel, companies such as Teva Pharmaceutical Industries advanced oral generic launches across neurology and metabolic disorders, reflecting sustained portfolio emphasis on high-volume oral therapies. At a global level, the World Health Organization’s Essential Medicines List remains heavily weighted toward oral formulations, reinforcing their role as first-line therapies in both developed and emerging healthcare systems.

The inhalable segment is projected to grow at the fastest CAGR of 11.3% over the forecast period, driven by the rising prevalence of chronic respiratory diseases, expanding access to complex generic inhalers, and greater regulatory clarity for drug-device combinations. Inhaled therapies are central to long-term management of asthma and chronic obstructive pulmonary disease, where sustained use, guideline-driven treatment escalation, and adherence programs support durable demand. As healthcare systems emphasize disease control and avoidance of acute exacerbations, payers increasingly favor cost-effective inhaled alternatives once exclusivity lapses.

The U.S. FDA continued to advance approvals of generic inhalation products that meet device equivalence and performance standards, lowering entry barriers for well-capitalized manufacturers. Companies such as Cipla expanded their global inhalation portfolios with approvals and launches across regulated markets, while Teva Pharmaceutical Industries advanced complex generic inhalers leveraging in-house device capabilities. In Europe, procurement frameworks increasingly include inhalable generics in formularies, accelerating their uptake in public health systems.

Distribution Channel Insights

The retail pharmacies segment led the market with the largest revenue share of 51.88% in 2025, driven by its direct access to outpatient populations, high refill rates for chronic therapies, and its strong role in generic dispensing and substitution. Retail pharmacies remain the primary distribution channel for long-term treatments in cardiovascular, metabolic, respiratory, and CNS disorders, where continuity of therapy and convenience strongly influence patient behavior. Their ability to manage prescriptions, reimbursement, and patient counseling at scale positions them as the preferred channel for generic medicines.

In the UK, NHS England continued to rely heavily on community pharmacies for dispensing generic medicines, supported by national policies that promote generic prescribing and pharmacist-led substitution. In India, Apollo Pharmacy expanded its retail footprint and chronic care programs, strengthening access to affordable generics across urban and semi-urban regions. Similarly, Boots maintained a strong focus on generic dispensing through its nationwide pharmacy network, reinforcing retail-led distribution in regulated European markets.

The online pharmacies segment is projected to grow at the fastest CAGR of 10.7% over the forecast period, driven by accelerating digital adoption, expanding e-prescription penetration, and increasing consumer preference for convenient, cost-effective access to generic medicines. Online platforms are particularly well-suited for chronic disease management, where repeat prescriptions, home delivery, and subscription-based refills enhance adherence and reduce friction for patients. Price transparency and easy comparison further favor generics in digital channels, reinforcing volume growth.

This outlook is supported by distinct real-world developments around 2025. In the United States, Amazon Pharmacy continued to expand its generic-focused offering and same-day or next-day delivery coverage, positioning online fulfillment as a viable alternative to traditional retail for maintenance therapies. In India, Tata 1mg strengthened its online pharmacy and chronic care ecosystem, leveraging e-prescriptions and integrated diagnostics to drive repeat generic purchases. Similarly, PharmEasy expanded last-mile delivery and digital prescription services, reinforcing online adoption for everyday medicines.

Regional Insights

North America dominated the global generic pharmaceuticals market with the largest revenue share of 32.40% in 2025, characterized by strong substitution practices, payer-driven cost containment, and mature regulatory systems. Generic uptake is supported by well-established pharmacy-level substitution rights and reimbursement frameworks that favor lower-cost alternatives. Manufacturers operating in the region prioritize regulatory compliance, supply reliability, and litigation preparedness, as patent challenges and exclusivity disputes frequently shape entry timing. While pricing pressure is intense, the region continues to reward scale, portfolio breadth, and execution discipline, particularly in chronic disease therapies and complex generics where technical and regulatory capabilities create differentiation.

U.S. Generic Pharmaceuticals Market Trends

The generic pharmaceuticals market in the U.S. accounted for the largest market revenue share in North America in 2025. The United States is the most structured and compliance-intensive market for generics, governed by abbreviated approval pathways and rigorous post-approval oversight. Generic penetration is reinforced by pharmacist substitution authority, payer formularies, and mail-order distribution. Litigation related to patents and exclusivity is a defining feature, often influencing launch sequencing and competitive intensity. Manufacturers focus on operational resilience, regulatory inspection readiness, and cost efficiency to sustain margins under pricing pressure. The market increasingly favors complex generics, biosimilars, and differentiated delivery formats, while maintaining strong baseline demand for oral small-molecule generics.

Europe Generic Pharmaceuticals Market Trends

The generic pharmaceuticals market in Europe is characterized by heterogeneous regulatory and reimbursement frameworks, with generics promoted through national healthcare policies and tendering systems. Governments actively encourage generic prescribing to control healthcare expenditure, leading to high substitution rates. However, price controls and centralized procurement can limit pricing flexibility and increase competition intensity. Manufacturers operating across Europe must navigate country-specific market access rules, reference pricing systems, and tender cycles. Supply continuity and cost leadership are critical success factors, particularly as authorities balance affordability objectives with concerns about medicine shortages and manufacturing sustainability.

The UK generic pharmaceuticals market maintains a highly generics-friendly environment driven by centralized procurement and strong policy support for generic prescribing. Community pharmacies play a central role in dispensing, supported by automatic substitution practices and national reimbursement frameworks. Pricing pressure is significant, but predictable demand and streamlined access pathways support volume stability. Supply resilience has become a growing priority, with increased scrutiny on sourcing and continuity following recent disruption events. The UK market rewards operational efficiency, reliable supply chains, and the ability to respond quickly to tender and reimbursement changes.

The German generic pharmaceuticals market operates in a highly structured environment, shaped by statutory health insurance funds and tender-based procurement. Generic substitution is well established, particularly for chronic therapies. While margins are constrained, the market offers stable volumes and predictable demand. Compliance with manufacturing and pharmacovigilance standards is critical, as regulators and payers closely monitor quality and supply performance. The environment increasingly favors supplier consolidation and operational excellence.

The France generic pharmaceuticals market is anticipated to grow at a significant CAGR during the forecast period. In France, generics are actively promoted through prescribing incentives, substitution policies, and reimbursement differentiation. While physician and patient acceptance have historically been more cautious than in some European peers, uptake has strengthened due to policy alignment and cost pressures. Pricing regulation remains strict, requiring manufacturers to optimize cost structures. The market emphasizes therapeutic equivalence, supply reliability, and alignment with national health priorities. Manufacturers benefit from predictable demand patterns but must manage regulatory complexity and pricing negotiations to maintain sustainable participation.

Asia-Pacific Generic Pharmaceuticals Market Trends

The generic pharmaceuticals market in the Asia Pacific is expected to register the fastest CAGR of 7.0% over the forecast period, driven by expanding healthcare access, rising chronic disease prevalence, and government efforts to improve the affordability of medicines. Local manufacturing strength and export orientation play a central role, particularly in regional supply chains. Regulatory maturity varies widely, requiring tailored market entry strategies. While competition is intense, the region offers long-term growth opportunities through volume expansion, domestic substitution initiatives, and increasing alignment with international quality standards.

The Japan generic pharmaceutical market has steadily increased its emphasis on generic adoption as part of national efforts to control healthcare costs. Government policies actively encourage generic prescribing and dispensing, particularly in outpatient settings. Although physician and patient preferences historically favored branded drugs, acceptance of generics has improved. The market prioritizes quality assurance, stable supply, and trust in manufacturers. Regulatory requirements are stringent, favoring experienced suppliers with strong compliance records. Japan offers stable demand but requires careful navigation of pricing revisions and regulatory expectations.

The generic pharmaceuticals market in China is shaped by centralized procurement programs and aggressive price negotiations aimed at reducing healthcare costs. Volume-based procurement has accelerated substitution toward approved generics, intensifying competition while expanding access. Domestic manufacturers benefit from policy support, while foreign players must adapt to local pricing and regulatory dynamics. Quality, consistency, and manufacturing scale are increasingly important as authorities emphasize equivalence standards. The market favors high-volume suppliers capable of meeting procurement requirements and maintaining cost competitiveness.

Latin America Generic Pharmaceuticals Market Trends

The generic pharmaceuticals market in Latin America presents a mixed environment, influenced by public procurement, economic volatility, and expanding healthcare coverage. Governments actively promote generics to improve affordability, particularly through public health systems. Regulatory frameworks differ across countries, requiring localized strategies. Currency volatility and pricing controls can affect profitability, even as demand for essential medicines remains strong. Manufacturers with regional presence, flexible pricing strategies, and strong distributor partnerships are better positioned to navigate regulatory and economic complexity.

The Brazil generic pharmaceuticals market is one of the most established generics markets in Latin America, supported by strong regulatory oversight and public acceptance of generics. Government procurement and reimbursement programs drive demand, particularly in chronic disease therapies. Local manufacturing plays a significant role, encouraged by policy frameworks. While competition is high, predictable demand and structured regulation provide stability. Compliance, pricing discipline, and relationships with public healthcare institutions are key determinants of success.

Middle East & Africa Generic Pharmaceuticals Market Trends

The generic pharmaceuticals market in the Middle East & Africa is characterized by uneven market maturity, with generics adoption driven by affordability needs and expanding healthcare infrastructure. Governments increasingly prioritize local manufacturing and generic substitutions to reduce dependence on imports. Regulatory harmonization is improving, though variability across markets persists. Demand growth is supported by population expansion and rising chronic disease burden. Manufacturers face challenges related to pricing controls, tender dependence, and supply logistics, but benefit from long-term expansion initiatives to gain market access.

The Saudi Arabia generic pharmaceuticals market held a significant share in the Middle East & Africa in 2025, driven by healthcare modernization and cost containment objectives under national reform programs. Government procurement and centralized purchasing strongly influence market dynamics. Regulatory standards are tightening, emphasizing quality and equivalence. Local production is encouraged through policy incentives, creating opportunities for partnerships and domestic manufacturing. The market favors suppliers that combine regulatory compliance, competitive pricing, and reliable supply to meet public healthcare demand.

Key Generic Pharmaceuticals Company Insights

The generic pharmaceuticals industry is highly fragmented, with no single company holding meaningful global dominance. Leading players such as Sandoz, Teva, Sun Pharma, Viatris, and major Indian manufacturers, including Aurobindo, Cipla, Dr. Reddy’s, and Lupin, each command low single-digit global shares, reflecting intense competition and broad supplier participation. Market leadership is driven less by scale alone and more by regulatory execution, portfolio breadth, channel focus, and supply reliability. While consolidation and targeted acquisitions are increasing in specific regions and segments, overall competition remains strong, reinforcing price pressure and favoring manufacturers with operational efficiency and diversified geographic exposure.

Key Generic Pharmaceuticals Companies:

The following key companies have been profiled for this study on the generic pharmaceutical market.

- Teva Pharmaceutical Industries

- Sandoz

- Sun Pharmaceutical Industries

- Viatris

- Dr. Reddy’s Laboratories

- Cipla

- Aurobindo Pharma

- Lupin

- Glenmark Pharmaceuticals

- Torrent Pharmaceuticals

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Player: Teva Pharmaceutical Industries

- Mature players focus on expanding generic drug portfolios, strengthening global manufacturing capabilities, securing regulatory approvals, and increasing penetration in regulated markets such as the U.S. and Europe.

- They also invest in biosimilars, complex generics, and strategic acquisitions to maintain long-term market leadership and pricing competitiveness.

- Mature players maintain a competitive advantage through strong global distribution networks, large-scale manufacturing infrastructure, diversified product portfolios, financial strength, and extensive regulatory expertise.

- Their established relationships with healthcare providers, pharmacies, and government procurement agencies support consistent market dominance.

- Mature players face challenges including pricing pressure in highly competitive markets, increasing regulatory scrutiny, high compliance costs, patent litigation risks, and supply chain disruptions.

- Large organizational structures may also reduce operational flexibility and slow response to rapidly changing market dynamics.

Emerging Player: Torrent Pharmaceuticals

- Emerging players prioritize portfolio diversification, expansion into specialty generics and biosimilars, and strategic partnerships to strengthen international presence.

- They emphasize cost-efficient manufacturing, rapid product launches after patent expirations, and investments in R&D to improve competitiveness in regulated and emerging markets.

- Emerging players gain a competitive advantage through operational agility, lower production costs, faster adaptation to market opportunities, and increasing focus on niche therapeutic areas.

- Their ability to rapidly develop affordable generic alternatives and expand into underserved markets supports growth and market penetration.

- Emerging players often face limited global distribution capabilities, lower brand recognition, funding constraints, and dependence on a smaller product portfolio.

- They may also experience challenges related to scaling manufacturing operations, attaining international regulatory approvals, and competing against established multinational pharmaceutical companies.

Recent Developments

-

In December 2025, Teva Pharmaceuticals and Sandoz secured multiple first generic drug approvals in late 2025, including estradiol vaginal insert (Teva) and sitagliptin/metformin (Sandoz), expanding their U.S. generic portfolios.

-

In August 2025, the U.S. FDA approved Teva’s generic liraglutide (Saxenda) for weight loss, the first approved generic GLP-1 for this indication, representing a significant advance in complex generics.

-

In July 2025, Glenmark Pharmaceuticals received another U.S. FDA warning letter following inspection findings at a manufacturing site, highlighting ongoing quality compliance challenges.

-

In May 2025, Alembic received final U.S. FDA approvals for Rivaroxaban tablets (generic Xarelto), Amlodipine/Atorvastatin combo, and Doxorubicin liposome injectable (generic Doxil), broadening its oncology and cardiovascular generics.

-

In February 2025, Sandoz agreed to pay $275 million to settle price-fixing allegations related to certain generic drug pricing in the U.S., concluding litigation but maintaining denial of wrongdoing.

Generic Pharmaceuticals Market Report Scope

Report Attribute

Details

Market size in 2025

USD 454.7 billion

Estimated market size in 2026

USD 495.7 billion

Projected market size by 2033

USD 770.0 billion

Growth rate

CAGR 6.5% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, trends

Segments covered

Type, application, product, route of administration, distribution channel, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; China; Japan; India; Australia; South Korea; Thailand; Brazil; Argentina; Saudi Arabia; South Africa; UAE; Kuwait

Key company profiled

Teva Pharmaceutical Industries; Sandoz; Sun Pharmaceutical Industries; Viatris, Dr. Reddy’s Laboratories; Cipla, Aurobindo Pharma; Lupin; Glenmark Pharmaceuticals; Torrent Pharmaceuticals

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Generic Pharmaceuticals Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends across sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global generic pharmaceuticals market report based on type, application, product, route of administration, distribution channel, and region:

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Simple Generics

-

Specialty Generics

-

Biosimilars

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Central Nervous System Disorders

-

Respiratory Diseases

-

Hormones and Related Diseases

-

Gastrointestinal Diseases

-

Cardiovascular Diseases

-

Infectious Diseases

-

Cancer

-

Diabetes

-

Others

-

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Small Molecule

-

Large Molecule

-

-

Route of Administration Outlook (Revenue, USD Million, 2021 - 2033)

-

Oral

-

Injectable

-

Inhalable

-

Others

-

-

Distribution Channel Outlook (Revenue, USD Million, 2021 - 2033)

-

Online Pharmacies

-

Retail Pharmacies

-

Hospital Pharmacies

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

U.S. Generic Drug Pricing & Market Entry Assessment

Conducted a comprehensive assessment of the U.S. generic pharmaceuticals market, focusing on patent expiry opportunities, pricing erosion trends, ANDA approval timelines, distributor landscape, and competitive benchmarking across cardiovascular, diabetes, and oncology generic drugs. The study also analyzed the influence of pharmacy benefit managers (PBMs), hospital procurement patterns, and regulatory compliance requirements for market entry.

Helped the client identify high-potential generic drug opportunities, optimize launch timing strategies, evaluate pricing competitiveness, and strengthen positioning against established generic pharmaceutical manufacturers in the U.S. market.

Biosimilars Pipeline Benchmarking & Partnership Analysis

Delivered an in-depth benchmarking study on global biosimilar developers focusing on monoclonal antibodies, insulin biosimilars, and autoimmune disease therapies. The assessment covered pipeline analysis, manufacturing capabilities, licensing and partnership agreements, regulatory approvals, intellectual property positioning, and commercialization strategies across the U.S., Europe, and Asia-Pacific markets.

Enabled the client to identify strategic partnership and acquisition opportunities, assess competitive white spaces in biosimilars, prioritize high-growth therapeutic segments, and support long-term investment decisions in advanced generic biologics.

Emerging Markets Generic Manufacturing Feasibility Study

Conducted a country-level feasibility assessment for generic pharmaceutical manufacturing expansion across India, Brazil, Indonesia, and South Africa. The study evaluated API sourcing, labor cost advantages, regulatory pathways, export potential, local demand forecasts, tax incentives, and supply chain infrastructure for oral solids and injectable generics.

Supported the client in identifying cost-efficient manufacturing locations, reducing supply chain risks, strengthening export capabilities, and improving long-term operational scalability across emerging pharmaceutical markets.

Frequently Asked Questions About This Report

Key factors include the rising prevalence of chronic diseases, rising number of generic approvals, and an increasing need to reduce overall healthcare expenditure.

Asia Pacific is the fastest-growing region over the forecast period.

The cardiovascular disease segment led with a 25.34% revenue share in 2025, while cancer is the fastest-growing segment.

The simple generics segment accounted for the largest share of 68.32% in 2025, while biosimilar is the fastest-growing segment.

The retail pharmacies segment held the highest market share of 51.88% in 2025, while online pharmacies is the fastest-growing segment.

The small molecule segment held the highest market share of 87.42% in 2025, while large molecule is the fastest-growing segment.

The global generic pharmaceuticals market is expected to grow at a compound annual growth rate of 6.5% from 2026 to 2033, reaching USD 770.0 billion in 2033.

The global generic pharmaceuticals market size was estimated at USD 454.7 billion in 2025 and is expected to reach USD 495.7 billion in 2026.

North America dominated with a 32.4% revenue share in 2025.

Some key players operating in the generic pharmaceuticals market include Sandoz, Teva, Sun Pharma, Viatris, and major Indian manufacturers, including Aurobindo, Cipla, Dr. Reddy’s, and Lupin.

About the Author(s)

Pharmaceuticals Research Team

Healthcare · PharmaceuticalsThis report was authored by the pharmaceuticals research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the pharmaceuticals segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.