- Home

- »

- Next Generation Technologies

- »

-

Smart Building Market Size And Share Report, 2026-2033GVR Report cover

![Smart Building Market Size, Share & Trends Report]()

Smart Building Market (2026 - 2033) Size, Share & Trends Analysis Report By Component (Solution, Service), By Solution (Safety & Security Management, Energy Management, Network Management), By Service, By End Use (Residential, Commercial), By Region, And Segment Forecasts

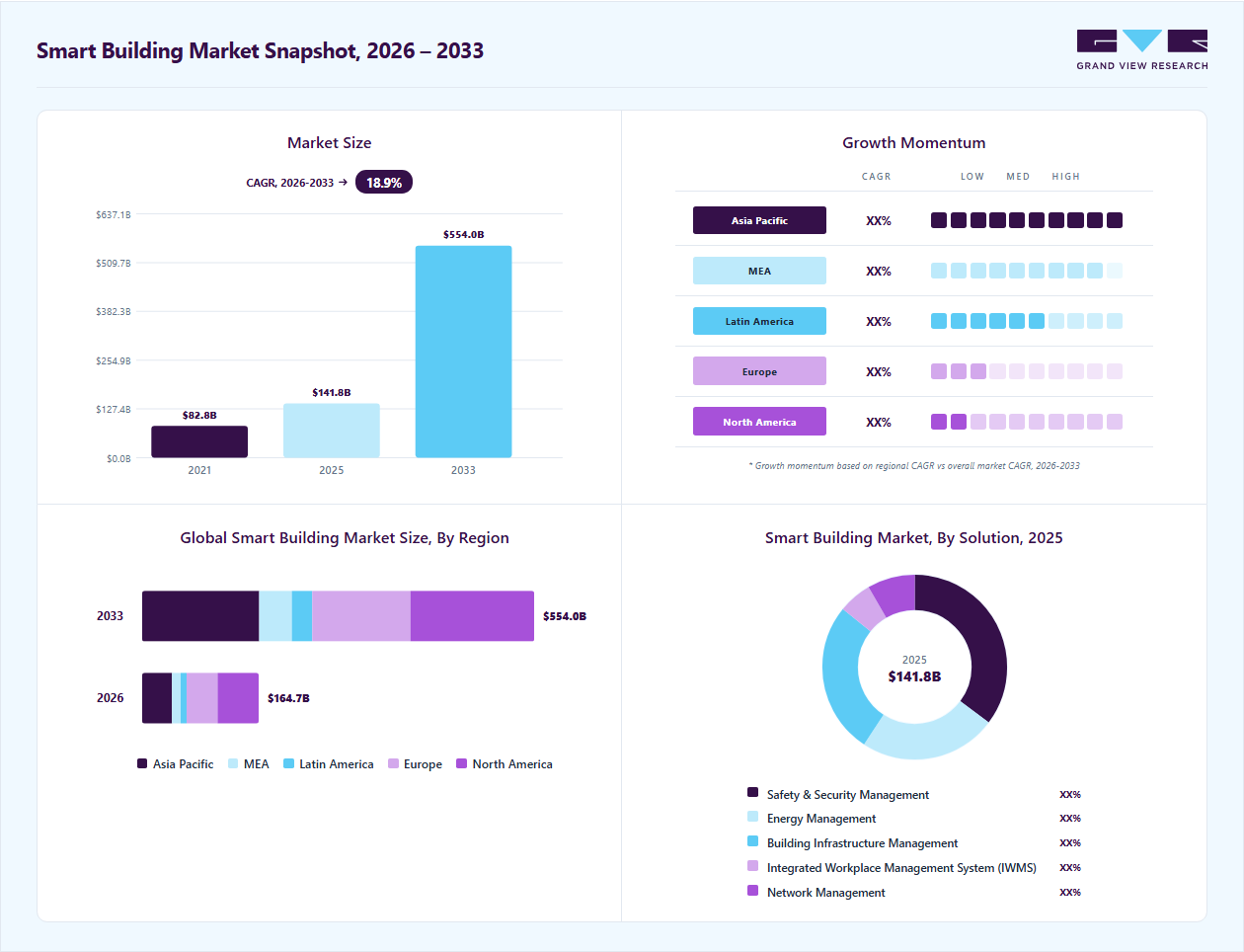

Market Size, 2025

$141.8BMarket Estimate, 2026

$164.7BMarket Forecast, 2033

$554.0BCAGR, 2026–2033

18.9%Smart Building Market Summary

The global smart building market size was estimated at USD 141.8 billion in 2025 and is projected to grow from USD 164.7 billion in 2026 to USD 554.0 billion by 2033, at a CAGR of 18.9% from 2026 to 2033. The smart building market in North America accounted for the largest revenue share of over 35% in 2025. The market growth is driven by the increasing adoption of IoT-enabled building management systems, rising demand for energy efficiency, and heightened awareness of sustainability.

Key Market Trends & Insights

- By component: Solution segment accounted for the largest revenue share of over 77% in 2025.

- By solution: Safety & security management segment is expected to grow at the highest CAGR of over 35% in 2025.

- By end use: Commercial segment accounted for the highest market share over 53% in 2025.

Regional Highlights

- Largest regional market: North America (35% revenue share, 2025)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 141.8 Billion

- Estimated market size in 2026: USD 164.7 Billion

- Projected market size by 2033: USD 554.0 Billion

- CAGR (2026-2033): 18.9%

Technological advancements in automation, data analytics, and AI-driven energy management solutions enable predictive maintenance, real-time monitoring, and optimized climate control, further accelerating the growth of the smart building industry.The increasing adoption of advanced automation, IoT, and AI technologies to enhance energy efficiency, occupant comfort, and operational performance is significantly driving the market growth. Smart buildings integrate interconnected systems such as lighting, HVAC, security, and facility management into a centralized platform, enabling real-time monitoring and data-driven decision-making. Urbanization, sustainability mandates, and the growing demand for energy conservation are encouraging both private and public sectors to invest in these solutions. Furthermore, government initiatives and green building certifications are boosting the adoption rate worldwide, thereby boosting the smart building industry expansion.

")

In addition, technological advancements are reshaping the smart building market, with AI-driven analytics, edge computing, and digital twin technologies becx`oming central to operational efficiency. Building management systems (BMS) are evolving from basic monitoring tools into predictive and adaptive platforms, enabling cost optimization and improved energy efficiency. Integration of renewable energy systems and smart grids is further strengthening sustainability outcomes in line with global carbon reduction goals.

Furthermore, rising environmental concerns and net-zero commitments are prompting governments to implement stricter policies focused on energy efficiency, green retrofits, and low-carbon technologies. These initiatives aim to reduce emissions, lower operational costs, and support green job creation. Increased emphasis on renewable energy adoption and efficient infrastructure is accelerating decarbonization across sectors.

Moreover, the competitive landscape is becoming increasingly dynamic with the entry of startups alongside established players, intensifying innovation and rivalry. Companies are focusing on interoperability, cybersecurity, and scalable platforms to meet evolving customer needs. Strategic collaborations among technology providers, developers, and energy firms are enabling integrated smart building ecosystems. This is expected to drive the smart building market.

Market Dynamics

Growing emphasis on energy conservation and carbon reduction is significantly driving the adoption of smart building technologies worldwide. Governments and regulatory bodies are implementing stricter energy-efficiency standards and green building regulations, encouraging facility owners to modernize their infrastructure with intelligent automation systems.

The smart home automated building market is also gaining momentum due to the rising integration of IoT, artificial intelligence (AI), and cloud-based analytics in modern buildings. Smart building systems allow centralized control of lighting, ventilation, security, and power consumption through connected devices and mobile applications. AI-driven analytics further help identify usage patterns and optimize energy consumption based on occupancy and environmental conditions.

The increasing adoption of smart homes, intelligent commercial buildings, and automated industrial facilities is accelerating demand for advanced automation solutions that support sustainability and operational efficiency objectives. In addition, rising electricity costs and growing corporate ESG commitments are encouraging organizations to deploy intelligent energy management systems. Businesses are increasingly prioritizing smart infrastructure solutions to reduce operational expenses, improve occupant comfort, and achieve long-term sustainability goals.

The high upfront cost associated with smart building infrastructure remains a major challenge for market growth. Deployment of advanced automation systems, sensors, connected devices, and integrated building management platforms often requires substantial capital investment. Expenses related to software licensing, network infrastructure, and system customization further increase the overall implementation cost for building owners.

In addition, integration complexities with legacy infrastructure and ongoing maintenance expenses can limit adoption, particularly among small and medium-sized property owners. Budget constraints in developing economies also continue to restrict large-scale implementation. Many older buildings require extensive retrofitting and hardware upgrades before smart technologies can be effectively integrated into existing systems.

The shortage of skilled professionals required for system integration, cybersecurity management, and advanced building analytics further increases operational challenges. Many organizations also face difficulties in justifying return on investment during the early stages of deployment. As a result, some businesses remain hesitant to fully transition toward advanced smart building automation despite the long-term efficiency benefits.

The increasing integration of artificial intelligence and IoT technologies is creating strong growth opportunities in the smart building market. Advanced AI-powered analytics enable predictive maintenance, intelligent energy management, occupancy optimization, and real-time operational control.

The growing adoption of cloud-based building management platforms and connected infrastructure is further supporting demand for intelligent automation solutions. Expansion of smart cities and digitally connected commercial spaces is expected to generate significant long-term market opportunities.

Furthermore, advancements in edge computing, wireless connectivity, and digital twin technologies are enabling more efficient and autonomous building operations. The increasing demand for data-driven facility management and smart workplace environments is expected to accelerate innovation and global market expansion.

Market Concentration & Characteristics

The global smart building market is highly concentrated, with a mix of building automation leaders, IoT platform providers, energy management firms, and large technology companies driving competitive dynamics. A small group of established players dominates large-scale commercial and infrastructure projects through integrated hardware-software ecosystems, advanced building management systems, and strong relationships with real estate developers and facility operators. Market growth is being strongly supported by increasing demand for energy-efficient infrastructure, rapid urbanization, rising adoption of IoT-enabled systems, and the integration of AI-driven building automation and predictive maintenance solutions.

Furthermore, the market is defined by rapid technological convergence across IoT, artificial intelligence, cloud computing, and edge analytics, enabling real-time monitoring and optimization of building operations, including HVAC, lighting, security, and energy consumption. M&A activity remains moderately high as large industrial automation and technology firms acquire niche smart building solution providers to strengthen their ecosystem capabilities. Regulatory influence is significant, driven by energy-efficiency mandates, sustainability goals, green building certifications, and an increasing emphasis on carbon-reduction and occupant-safety standards.

Component Insights

The solution segment accounted for the largest market share of over 77% in 2025, driven by strong adoption of AI-enabled access control, biometric authentication, video surveillance, emergency communication systems, and cybersecurity solutions. Increasing integration of IoT and AI is enabling predictive building management and real-time operational intelligence. Demand is further supported by convergence of safety, security, and facility management systems into unified platforms. Rising deployment of mobile-based access credentials and cloud-connected building systems is improving operational flexibility and user convenience. Stringent building safety codes and sustainability regulations are further reinforcing adoption.

The service segment is expected to register the fastest CAGR of over 20% from 2026 to 2033, fueled by rising demand for predictive maintenance, commissioning, energy audits, remote monitoring, and managed building services. Increasing complexity of smart infrastructure is accelerating reliance on specialized consulting, implementation, and support services. Occupant expectations for enhanced experiences, such as intelligent lighting, personalized climate control, and indoor air quality monitoring, are further driving demand.

Solution Insights

The safety & security management segment accounted for the largest market share in 2025, driven by increasing demand for AI-based access control, biometric systems, surveillance solutions, emergency communication, and cybersecurity frameworks. Growing regulatory emphasis on building safety standards is accelerating deployment of integrated security systems. Furthermore, the rising use of mobile credentials and unified security platforms is improving access efficiency and incident response, thereby driving the segmental growth.

The energy management segment is expected to register the fastest CAGR from 2026 to 2033, supported by AI-enabled HVAC optimization, smart lighting systems, demand-response solutions, and intelligent energy metering. Rising global focus on net-zero emissions and decarbonization targets is a key growth driver. Increasing regulatory pressure on energy efficiency is accelerating adoption of smart energy systems. Integration of IoT and AI for predictive analytics and real-time energy optimization is further enhancing efficiency.

Service Insights

The implementation segment accounted for the largest market share in 2025, driven by the installation and deployment of advanced building technology systems, including actuators, sensors, and microchips, to collect and manage data for optimizing building operations. This infrastructure enables owners, operators, and facility managers to enhance asset reliability, ensure occupant comfort and safety, improve energy efficiency, and minimize operational costs. These factors drive the growth of the implementation segment in the market.

The support and maintenance segment is expected to register the fastest CAGR from 2026 to 2033. The growth can be attributed to the involvement of providing ongoing services after solution deployment to ensure optimal performance, system upgrades, and operational efficiency. Vendors conduct routine evaluations to implement technological enhancements and process improvements, enabling intelligent automation for cost-effective building operations in the smart building industry.

End Use Insights

The commercial segment accounted for the largest market share in 2025, driven by widespread adoption across offices, retail spaces, hospitality, and commercial complexes. Rising energy costs and strict regulatory frameworks are compelling organizations to adopt smart building technologies for efficiency and sustainability. Integration of automation systems is improving occupant comfort, operational performance, and energy optimization. Growing emphasis on ESG compliance and cost reduction is further accelerating deployment.

The residential segment is expected to register significant growth at a CAGR from 2026 to 2033, fueled by the increasing adoption of smart HVAC systems, security solutions, lighting automation, and smart meters. Rising consumer awareness of energy efficiency and home automation is a key growth driver. Growth in disposable income and expansion of smart home ecosystems are further accelerating adoption. The integration of IoT-enabled devices and smart grid connectivity is enhancing convenience, safety, and energy efficiency, thereby driving segmental growth.

Regional Insights

North America dominated the market with a share of over 35% in 2025, driven by increasing public and private investments, coupled with the rapid adoption of digitalization across commercial, industrial, and residential sectors. The expanding integration of Internet of Things (IoT) technologies and advancements in digital infrastructure are enhancing building automation, energy efficiency, and security systems across the North America region.

U.S. Smart Building Market Trends

The U.S. smart building market dominated the market with a share of over 74% in 2025, driven by substantial government investments in digital infrastructure aimed at accelerating the country’s transition toward a digital economy. The U.S. government is actively focusing on digitizing commercial buildings to enhance citizen experiences and ensure service transparency. Various industries are converting their conventional offices into smart buildings to leverage advanced technologies for energy efficiency and operational excellence.

Europe Smart Building Market Trends

The Europe smart building market is expected to grow at a CAGR of over 17% from 2026 to 2033, owing to the rising adoption of Industry 4.0 technologies and the growing integration of big data analytics, IoT, artificial intelligence (AI), and machine learning (ML) in building operations, smart building solutions are gaining strong traction. Governments across countries are increasingly prioritizing digitalization initiatives to improve occupant safety, enhance operational efficiency, enable predictive maintenance, and support long-term sustainability goals in the smart building industry.

The Germany smart building market is expected to grow significantly in the coming years, owing to the rising need to reduce energy consumption amid increasing energy costs, prompting building owners and operators to adopt innovative solutions for efficiency and cost savings. Smart buildings in Germany leverage advanced energy management systems to optimize heating, ventilation, air conditioning, lighting, and other electrical operations.

The UK smart building market is rapidly expanding, driven by substantial growth as building owners and operators increasingly adopt connected technologies to improve energy efficiency, reduce operational costs, and meet stringent national sustainability targets. Government initiatives promoting digital infrastructure and decarbonization are catalyzing market adoption. The integration of cloud computing, analytics, and real-time data systems is enabling UK buildings to operate more sustainably, improve occupant experience.

Asia Pacific Smart Building Market Trends

The Asia Pacific market is expected to grow at the fastest CAGR of 21% from 2026 to 2033, owing to the rapid urbanization, increasing internet penetration, and a rising preference for remote building management services powered by IoT technology. Governments are making substantial investments in smart building infrastructure, fostering large-scale adoption across commercial and residential sectors. The shift in consumer focus toward upgrading existing properties into smart-enabled facilities is further accelerating regional demand.

The China smart building market is driven by the increasing digitalization of building systems, widespread rollout of 5G-powered IoT networks, and strong government backing for green and intelligent infrastructure initiatives. Tech giants such as Huawei and ZTE are advancing cloud-integrated building management platforms that enhance energy optimization, predictive maintenance, and occupant comfort.

The Japan smart building market is rapidly expanding, driven by the country’s emphasis on disaster-resilient infrastructure and strict building codes, fuel demand for advanced smart building solutions. The expanding deployment of 5G networks supports real-time data communication and remote monitoring capabilities.

Key Smart Building Company Insights

Some of the key players operating in the market include ABB Ltd. and Johnson Controls, among others.

-

ABB Ltd. operates in four business segments: motion, robotics & discrete automation, electrification, and process automation. The company offers its products to 24 industries, including marine, automotive, smart cities, data centers, power generation, and ports. It has invested in various technology companies through its ABB Technology Ventures (ATV), such as AFC Energy, CMR Surgical, Element Analytics, Graphmatech, IMSystems, Natron Energy, Numocity, Spear Power Systems, Vicarious, Vion Technologies, and Stellapps. The company has established its service and dealer network in over 100 countries.

-

Johnson Controls designs and develops control and automation systems. Its product portfolio includes fire suppression, HVAC equipment, security, industrial refrigeration, smart home, fire detection, digital solutions, building automation & controls, distributed energy storage, and oil & gas products. The company serves data centers, academic institutions, sports & entertainment, residential, healthcare, industrial manufacturing, marine & navy, federal & state government, transportation, and urban markets.

Cisco Systems, Inc. and Emerson Electric Co. are some of the emerging market participants in the smart building market.

-

Cisco Systems, Inc. specializes in developing and distributing hardware and software solutions. The company serves industries such as mining, oil & gas, smart buildings, retail, education, financial services, government, transportation, utilities, healthcare, insurance, and entertainment. It offers various technological solutions, including cloud, data center, network infrastructure, mobility, IoT, security, AI, and analytics & automation.

-

Emerson Electric Co. designs, develops, and distributes automation and commercial & residential technological solutions. The company’s product portfolio includes fluid controls & pneumatics, automation & control modules, measurement instruments, control & safety systems, assembly & cleaning equipment, electrical components and lighting, HVAC, tools & vacuum systems, valves, actuators, regulators, and other service kits.

Key Smart Building Companies:

The following key companies have been profiled for this study on the smart building market.

-

ABB Ltd.

-

BOSCH

-

Cisco Systems Inc.

-

Emerson Electric Co.

-

Hitachi, Ltd.

-

Honeywell International Inc.

-

Intel Corporation

-

Johnson Controls

-

KMC Controls

-

LG Electronics Inc.

-

Legrand

-

Schneider Electric Corporation

-

Siemens AG

-

Sierra Wireless (Semtech)

-

Telit

Recent Developments

-

In May 2026, Siemens AG introduced an AI-enabled managed service under its smart infrastructure portfolio designed to advance autonomous building operations. The solution combines predictive failure detection, fault diagnostics, and prescriptive analytics to continuously optimize asset performance across building systems.

-

In February 2026, Honeywell International Inc. and Tata Consultancy Services (TCS) announced a strategic partnership aimed at accelerating the transition from traditional building automation to fully autonomous building operations. The collaboration integrates Honeywell’s building automation and industrial control systems with TCS’s digital, cloud, and AI capabilities to enable real-time intelligence across commercial and industrial facilities.

-

In December 2025, Cisco Systems Inc. announced its Advisor Select partnership with Environments to enhance network integration and automation in smart buildings, targeting offices, education, healthcare, retail spaces, industrial facilities, and data centers through IoT ecosystems of cameras, sensors, thermostats, lighting controls, speakers, security devices, and shades.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: ABB Ltd., BOSCH, Honeywell International, Inc.

- Focus on integrated end-to-end smart building ecosystems combining automation, energy management, HVAC, security, and analytics platforms.

- Expand through long-term enterprise contracts, strategic partnerships, and acquisitions to strengthen digital infrastructure capabilities.

- Strong global distribution networks, established customer relationships, and extensive installed infrastructure base.

- High R&D investments enabling advanced AI-driven automation, interoperability, and scalable smart building solutions.

- Legacy systems and complex organizational structures can slow innovation and product deployment cycles.

- Higher implementation and maintenance costs may limit adoption among small and mid-sized customers.

Emerging Players: KMC Controls, Sierra Wireless, Telit

- Focus on niche innovations such as cloud-native building management, IoT connectivity, edge analytics, and low-cost smart monitoring solutions.

- Compete through flexible deployment models, rapid customization, and partnerships with technology integrators and regional developers.

- Faster innovation cycles and greater agility in adopting emerging technologies such as AI, edge computing, and wireless IoT systems.

- Ability to offer cost-effective and modular solutions tailored for specific building applications and mid-market customers.

- Limited brand recognition and smaller service networks compared to established market leaders.

- Dependence on third-party infrastructure providers and constrained financial resources may affect large-scale expansion capabilities.

Smart Building Market Report Scope

Report Attribute

Details

Market size in 2025

USD 141.8 billion

Estimated Market size in 2026

USD 164.7 billion

Projected Market size by 2033

USD 554.0 billion

Growth rate

CAGR of 18.9% from 2026 to 2033

Base year of estimation

2025

Actual data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Component, solution, service, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East; Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; Japan; India; South Korea; Australia; Brazil; Argentina; UAE; Saudi Arabia; South Africa

Key companies profiled

ABB Ltd.; BOSCH; Cisco Systems Inc.; Emerson Electric Co.; Hitachi, Ltd.; Honeywell International Inc.; Intel Corporation; Johnson Controls; KMC Controls; LG Electronics Inc.; Legrand; Schneider Electric Corporation; Siemens AG; Sierra Wireless (Semtech); Telit

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Global Smart Building Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global smart building market report based on component, solution, service, end use, and region.

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Solution

-

Service

-

-

Solution Outlook (Revenue, USD Billion, 2021 - 2033)

-

Safety & Security Management

-

Access Control System

-

Video Surveillance System

-

Fire and Life Safety System

-

-

Energy Management

-

HVAC Control System

-

Lighting Management System

-

Others

-

-

Building Infrastructure Management

-

Parking Management System

-

Water Management System

-

Others

-

-

Network Management

-

Wired Technology

-

Wireless Technology

-

-

Integrated Workplace Management System (IWMS)

-

Real Estate Management

-

Capital Project Management

-

Facility Management

-

Operations and Services Management

-

Environment and Energy Management

-

-

-

Service Outlook (Revenue, USD Billion, 2021 - 2033)

-

Consulting

-

Implementation

-

Support & Maintenance

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Residential

-

Commercial

-

Healthcare

-

Retail

-

Academic

-

Others

-

-

Industrial

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customization

We have successfully delivered the following deep-dive customizations

Client Objective

Custom Research Modules Delivered

Strategic Value / Business Impact

Product Positioning & Competitive Intelligence

Benchmarking of smart building solutions and core automation capabilities

Analysis of pricing models, value delivery, and market positioning

Study of brand reputation and customer adoption trends

Evaluation of competitor strategies in smart infrastructure and automation

Improved differentiation through automation and energy optimization features Enabled pricing strategies aligned with smart infrastructure demand

Identified gaps in interoperability, security, and real-time analytics

Strengthened positioning in the evolving smart building ecosystem

Technology & Innovation Assessment

Emerging technology trend analysis

Innovation pipeline and patent review

Technology adoption readiness assessment

Ecosystem and partnership mapping

Identified future growth areas Supported innovation roadmap planning

Evaluated commercialization potential

Strengthened strategic partnership decisions

Frequently Asked Questions About This Report

Key players operating in the smart building market include ABB Ltd.; BOSCH; Cisco Systems Inc.; Emerson Electric Co.; Hitachi, Ltd.; Honeywell International Inc.; INTEL Corporation; Johnson Controls; KMC Controls; LG Electronics Inc.; Legrand; Schneider Electric SE; Siemens; Sierra Wireless; and Telit.

North America dominated with a 35% revenue share in 2025.

Key factors include growing adoption of Business Information Modeling (BIM), Artificial Intelligence (AI), Internet-of-Things (IoT), Virtual Reality (VR), cloud computing and data analytics is driving the growth of the smart building market. Further, the growing popularity of home automation, and rising preference towards working from home is further propelling the smart building market growth.

The global smart building market size was estimated at USD 141.8 billion in 2025 and is expected to reach USD 164.7 billion in 2026.

The global smart building market is expected to grow at a compound annual growth rate of 18.9% from 2026 to 2033 to reach USD 554.0 billion by 2033.

The solution segment accounted for the largest revenue share of over 77% in 2025, while service is the fastest-growing segment.

The safety & security management segment held the highest market share in 2025, while energy management is the fastest-growing segment.

The commercial segment held the highest market share in 2025, while residential is the fastest-growing segment.

The implementation segment held the highest market share in 2025, while support and maintenance is the fastest-growing segment.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.