- Home

- »

- Next Generation Technologies

- »

-

Smart Cities Market Size, Share & Trends Report, 2026-2033GVR Report cover

![Smart Cities Market (2026 - 2033)Report]()

Smart Cities Market (2026 - 2033)

Size, Share & Trends Analysis Report By Application (Smart Governance, Smart Building, Smart Healthcare), By Smart Governance, By Smart Utilities, By Smart Transportation, By Smart Healthcare, By Region, And Segment Forecasts

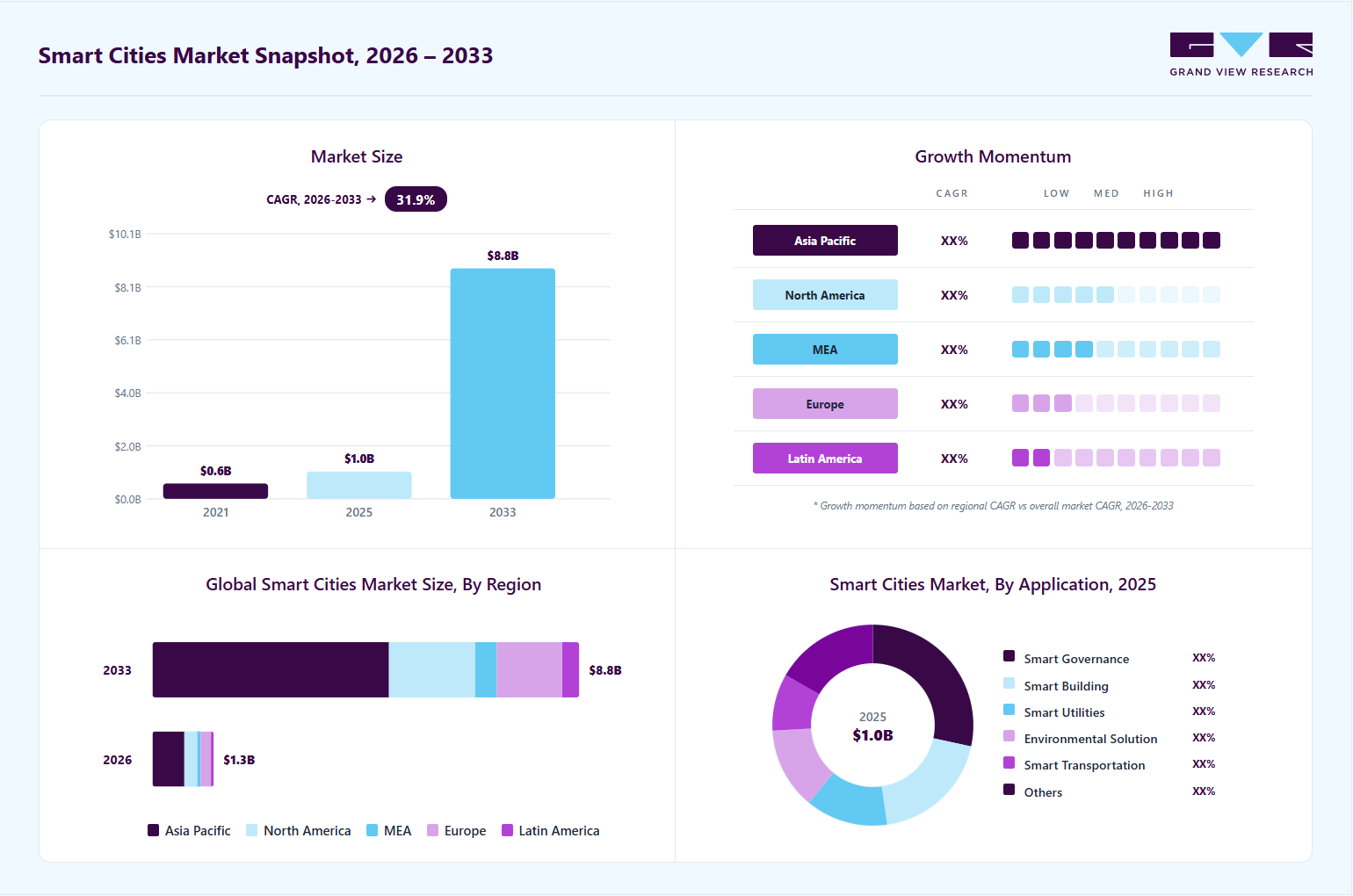

Market Size, 2025

$1.0TMarket Estimate, 2026

$1.3TMarket Forecast, 2033

$8.8TCAGR, 2026–2033

31.9%Smart Cities Market Summary

The global smart cities market size was valued at USD 1.0 trillion in 2025 and is projected to grow from USD 1.3 trillion in 2026 to USD 8.8 trillion by 2033, growing at a CAGR of 31.9% from 2026 to 2033. Asia Pacific dominated the market with a revenue share of 51.3% in 2025. The market growth is primarily driven by rapid urbanization, which is pressuring governments and municipalities to adopt sustainable and efficient city planning solutions.

Key Market Trends & Insights

- By application: Smart utility segment accounted for a significant revenue share in 2025.

- By smart governance: smart lighting segment led the market with the largest revenue share of 31.5% in 2025.

- By smart utilities: Energy management segment led the market with a share of 27.2% in 2025.

- By smart transportation: Intelligent transportation system segment accounted for the largest market share of 29.4% in 2025.

- By smart healthcare: Medical devices segment accounted for a dominant market share of 56.6% in 2025

Regional Highlights

- Largest regional market: Asia Pacific (51.3% revenue share, 2025)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 1.0 Trillion

- Estimated market size in 2026: USD 1.3 Trillion

- Projected market size by 2033: USD 8.8 Trillion

- CAGR (2026-2033): 31.9%

The widespread integration of IoT and connected devices across infrastructure systems is enabling real-time data collection and management. Rising investments in smart infrastructure, including smart grids, intelligent transportation, and e-governance platforms, are significantly accelerating market growth. Advancements in communication technologies such as 5G and edge computing are further enabling seamless connectivity and supporting the deployment of advanced urban applications, which is expected to drive the smart cities industry expansion.")

The increasing focus on sustainability and environmental management is reshaping the smart cities landscape as governments and urban planners prioritize green infrastructure and eco-friendly solutions. Smart cities are integrating energy-efficient systems, renewable energy sources, and green building technologies to reduce carbon emissions and improve environmental performance. Initiatives such as smart grids, electric public transport, and waste-to-energy programs are being widely adopted to meet sustainability goals.

In addition, the surge in demand for intelligent transportation systems is significantly contributing to the expansion of the market. Urban areas are increasingly adopting smart mobility solutions such as adaptive traffic signals, real-time transit updates, autonomous vehicles, and integrated multimodal transport platforms. Technologies aim to reduce traffic congestion, lower emissions, and enhance commuter experiences. Rising concerns around urban traffic inefficiencies and pollution, smart transport initiatives are becoming central to city planning strategies, thereby accelerating the deployment of smart cities industry infrastructure.

Furthermore, public safety and security are emerging as critical drivers for smart cities development, with increasing investments in surveillance, emergency response systems, and cybersecurity infrastructure. Advanced video analytics, AI-powered threat detection, and integrated communication platforms are being deployed to ensure real-time monitoring and faster incident response. Technologies help governments maintain urban safety and resilience against both physical and cyber threats, thereby boosting the smart cities industry growth.

Moreover, the growing smart buildings and urban infrastructure is also playing a key role in market growth. Smart cities are investing in intelligent buildings equipped with automated lighting, climate control, energy management systems, and integrated security. Buildings optimize resource usage and reduce operational costs while enhancing comfort and safety for occupants. The integration of digital twins and BIM (Building Information Modeling) is transforming how infrastructure is planned, managed, and maintained. This trend is driving innovation in construction and urban planning, fueling the broader adoption of smart cities technologies.

Market Dynamics

The smart cities market is expanding rapidly with governments worldwide investing in digital transformation initiatives powered by IoT, AI, big data analytics, and 5G connectivity to improve operational efficiency, enhance citizen services, and support sustainable urban development. The growing emphasis on sustainability, safety, and improved quality of life is further accelerating the adoption of smart city solutions, making it a key priority in long-term urban planning strategies across both developed and emerging economies.

Rapid urbanization is emerging as a key growth driver for the smart cities market, as a growing share of the global population continues to shift toward urban centers. This accelerating urban migration is placing substantial pressure on existing infrastructure systems, including transportation networks, energy grids, water supply chains, and waste management facilities. In many cities, the pace of infrastructure development has not kept up with population growth, resulting in congestion, resource inefficiencies, and declining service quality. These challenges are further amplified by rising economic activity and increased demand for real-time urban services.

To address these structural constraints, governments and municipal authorities are increasingly adopting smart city solutions that leverage IoT, artificial intelligence, cloud computing, and advanced data analytics. These technologies enable continuous monitoring of urban systems and support data-driven decision-making to efficiently allocate resources and deliver services. Applications such as intelligent traffic management, smart energy distribution, predictive infrastructure maintenance, and automated public services are improving operational efficiency and urban sustainability. As a result, smart city initiatives are becoming a critical enabler for managing modern urban complexity and improving overall quality of life.

The high cost of deploying smart city infrastructure remains a major restraint on market growth. Establishing connected systems involving sensors, communication networks, data platforms, and control centers requires substantial capital investment, which can be challenging for developing and budget-constrained regions. In addition to cost, the integration of multiple technologies across existing urban infrastructure presents significant complexity. Coordinating among various stakeholders, ensuring interoperability with legacy systems, and managing large-scale deployments often lead to delays and implementation challenges, slowing adoption in many cities.

The rapid deployment of 5G networks, IoT ecosystems, and AI-powered analytics is creating significant growth opportunities for the smart cities market. These technologies enable high-speed connectivity, real-time data processing, and intelligent automation across urban systems, supporting applications such as smart mobility, energy optimization, and enhanced public safety.

The growing government emphasis on building sustainable, digitally connected cities is further driving investments in next-generation infrastructure. Solutions that improve energy efficiency, reduce carbon emissions, and strengthen urban resilience are witnessing strong adoption, creating substantial opportunities for technology providers and infrastructure developers worldwide. Additionally, the integration of these technologies is enabling unified digital platforms that connect multiple urban functions, improving interoperability across transportation, utilities, and emergency services while enhancing response efficiency and overall operational performance.

Market Concentration & Characteristics

The smart cities market is moderately fragmented, with many technology providers, system integrators, infrastructure vendors, telecommunications companies, and software developers participating across different solution categories such as smart transportation, utilities, governance, buildings, and public safety. The market is characterized by a high degree of innovation, driven by continuous advancements in IoT, artificial intelligence, digital twins, edge computing, 5G connectivity, and cloud-based urban management platforms. The level of M&A activity is medium to high, as technology providers, infrastructure companies, and software vendors increasingly pursue acquisitions and strategic partnerships to expand smart city capabilities, strengthen platform integration, and gain access to new geographic markets. The impact of regulations is high, given the sector’s dependence on government policies, public procurement frameworks, data privacy laws, cybersecurity standards, environmental mandates, and urban development regulations, all of which directly influence project deployment and funding.

Additionally, the threat of product substitutes is low to medium, as traditional urban infrastructure systems can serve similar functions but often lack the efficiency, automation, interoperability, and sustainability benefits offered by smart city solutions. Meanwhile, end-user concentration is high, with revenue largely concentrated among municipal governments, public utilities, transportation authorities, and large public-sector agencies that control infrastructure investments and digital transformation initiatives.

Analyst Perspective

The smart cities market is being driven by accelerating urbanization, increasing demand for efficient public services, growing sustainability initiatives, and sustained investments in digital infrastructure. As cities face mounting pressure to improve mobility, energy efficiency, public safety, and governance, smart city technologies are becoming a critical component of long-term urban development strategies. The key competitive advantage belongs to platforms that integrate multiple city functions into a unified operating ecosystem, enabling real-time decision-making, operational efficiency, resource optimization, and enhanced citizen experiences across interconnected urban environments.

Application Insights

Based on application, the smart utility segment accounted for a significant revenue share in 2025 and is expected to grow at a significant CAGR over the forecast period. The smart utility segment forms an integral part of the city infrastructure and includes multiple domains such as water treatment, consolidated data management, energy distribution, and civil distribution infrastructure management, among others. The advent of smart grids is also a significant factor driving the adoption of smart utilities. Integration of advanced data analytics and cloud technologies is also expected to drive market growth. The rapidly increasing demand for energy, companies and governments are formulating and implementing strategies for improving renewable sources contribution to overall energy production, thereby driving segmental growth.

The smart transportation solution segment is expected to witness a significant CAGR of 36.8% from 2026 to 2033. Industry players are increasingly investing in advanced transportation technologies such as connected vehicles, intelligent traffic management systems, and autonomous mobility solutions to enhance urban mobility and reduce congestion. This strategic focus on smart infrastructure and mobility innovation is fueling the growth of the smart transportation segment.

Smart Transportation Insights

Based on smart transportation, the intelligent transportation system segment accounted for the largest market share of 29.4% in 2025, owing to the increasing number of vehicles on the road and the need to reduce traffic congestion are key factors in deploying advanced traffic management systems. These systems reduce delays and air pollution, ensure efficient traffic management by reducing travel duration, and enable authorities and public safety agencies to rapidly and efficiently respond to accidents and emergencies. Furthermore, the governments of several countries are adopting intelligent transportation systems to improve road safety and operational performance of the transport system and reduce the impact of transportation on the environment, thereby driving segmental growth.

The parking management segment is expected to witness the highest CAGR from 2026 to 2033. The segment growth can be attributed to the demand for efficient parking space management, environmental protection cost reduction, solutions to improve the convenience of end users, and improved safety and security in parking lots. The rising number of vehicles in cities makes it challenging for traffic departments to manage congestion problems. As a result, the smart city projects adopted by governments worldwide are now concentrating on effectively utilizing available parking spaces to reduce pollution and traffic jams. These factors will further boost the demand for parking management systems.

Smart Governance Insights

Based on smart governance, the smart infrastructure segment dominated the market and accounted for the largest market share of 27.6% in 2025. Shifting various governments focus on digitizing their business operations is anticipated to fuel the demand for smart infrastructure solutions in multiple sectors such as BFSI, healthcare, retail, manufacturing, and F&B. Most governments are investing in smart infrastructure solutions for economic digitalization. The government will also create the regulatory framework for BFSI infrastructure to support, monitor & control evolving payment systems and crypto ecosystems, thereby driving segmental growth.

The smart lighting segment is expected to witness a significant CAGR from 2026 to 2033. Increasing the energy efficiency of the city and reducing costs of energy and maintenance, smart lighting can also provide a backbone for a wide range of smart city applications, including traffic management, public safety, environmental monitoring, smart parking, and extended Wi-Fi and cellular communications, among others. Smart lighting has gained much traction in recent years due to the evolution of human-centric lighting with light-emitting diodes and organic light-emitting diodes.

Smart Healthcare Insights

Based on smart healthcare, the medical devices segment accounted for a dominant market share of 56.6% in 2025, owing to the growing integration of medical devices within urban health infrastructure. Devices facilitate real-time health monitoring, early diagnosis, and timely intervention, significantly reducing the burden on hospitals and improving patient outcomes. Governments and urban planners are prioritizing the incorporation of smart healthcare solutions as part of their broader smart city initiatives to enhance quality of life, reduce healthcare delivery costs, and manage the increasing demand for healthcare services in densely populated areas. This strong governmental push, coupled with advancements in connected medical technologies, is driving the dominance of the medical devices segment.

The systems & software segment is expected to witness the highest CAGR from 2026 to 2033. The segment growth can be attributed to the increasing demand for integration of electronic health records (EHRs), remote diagnostics, and AI-based decision-support systems. These solutions enhance the operational efficiency of healthcare providers and improve patient outcomes through timely interventions and accurate diagnostics. Urban populations grow and healthcare infrastructure becomes more digitized, the reliance on intelligent systems to streamline workflows and manage patients is also expected to accelerate the adoption of advanced software-driven healthcare solutions.

Smart Utilities Insights

Based on smart utilities, energy management segment led the market with a share of 27.2% in 2025, owing to the growing energy demand sparked the adoption of virtual power plants, which operate on AI, machine learning, and IoT to provide security and efficiency. Key market players are focusing on establishing a strong R&D infrastructure to drive the development and overview of advanced energy management systems and design analytics solutions to integrate emerging technologies such as blockchain, thus contributing to the dominance of the energy management segment in the smart cities industry.

The waste management segment is expected to witness the highest CAGR from 2026 to 2033. Several governments are approaching system integrators, distributors, and OEMs for smart trash bin installation across various cities. Local governments, technology solutions providers, distributors, and system integrators are the major stakeholders in implementing city-level waste management projects. Different mobile apps are also being developed to monitor the fill levels of bins and add to the users' convenience. OEMs and system integrators are particularly focusing on venues that are more crowded and can often result in generating higher volumes of waste to deploy smart garbage bins and other waste management equipment, supporting the smart cities industry growth.

Regional Insights

North America accounted for the market share of 21.5 % in 2025, primarily driven by the region’s strong emphasis on urban innovation and the early adoption of smart city technologies. Key areas such as intelligent transportation systems, energy-efficient utilities, public safety technologies, and digital governance platforms are experiencing rapid growth. The widespread adoption of AI, IoT, 5G, and cloud computing enables cities to deliver smarter services, optimize resource use, and improve quality of life, reinforcing regions dominance in the smart cities industry.

U.S. Smart Cities Market Trends

The smart cities market in the U.S. held the largest share in the North America region in 2025, driven by the country’s strong focus on innovation, digital infrastructure, and sustainable urban development. The presence of leading technology firms and a thriving startup ecosystem further accelerates the adoption of advanced solutions in transportation, energy, and urban planning. The emphasis on climate resilience and carbon-neutral goals is pushing cities to adopt green technologies and integrated infrastructure, thereby fueling the growth of the smart cities market.

Europe Smart Cities Market Trends

Europe smart cities are expected to grow at a CAGR of 30.1% from 2025 to 2030. The region’s growth is fueled by strong policy support from the European Union, including initiatives like the European Green Deal and Horizon Europe, which are driving large-scale investments in urban innovation and sustainability. The region also benefits from a high level of public awareness and civic participation, encouraging the adoption of e-governance platforms and citizen-focused smart services. Collaboration between public institutions, research centers, and private enterprises is fostering innovation ecosystems that are accelerating the development and implementation of smart cities industry.

The UK Smart Cities market is expected to grow at a significant rate in the coming years, driven by the increasing adoption of digital governance and citizen-centric services. Local councils are leveraging data analytics and mobile platforms to deliver real-time public services and boost civic engagement. The widespread rollout of 5G networks is enhancing connectivity, enabling smarter transportation and infrastructure systems. Investment in cybersecurity is also rising, as cities prioritize data protection in connected environments. Additionally, the rise of smart housing and urban regeneration projects is reshaping urban living and driving long-term market expansion.

The Germany smart cities market is fueled by the country’s strong commitment to digital transformation, with cities increasingly adopting smart technologies to enhance urban life. Germany’s government-led initiatives are fostering collaborations between public and private sectors to develop innovative solutions for urban sustainability. Integrating smart mobility systems, such as electric vehicle charging stations and autonomous transportation, is driving market growth.

Asia Pacific Smart Cities Market Trends

Asia Pacific dominated the smart cities market with the largest revenue share of 51.3% in 2025, driven by rapid urbanization and a growing need for sustainable urban solutions. The increasing demand for energy-efficient buildings and green infrastructure is propelling the region towards more environmentally conscious city designs. The rise of smart healthcare solutions, driven by digital health platforms and AI-based diagnostics, is improving access to healthcare services in densely populated areas. Government policies focused on smart mobility solutions, such as electric vehicles and autonomous transportation systems, further contribute to the growth of smart cities across the APAC region.

The Japan smart cities market is gaining traction, fueled the country's aging population, which is creating a growing demand for healthcare and elderly care solutions integrated into urban infrastructure. Japan is increasingly adopting AI and robotics to automate tasks in healthcare, transportation, and public safety, making urban environments more efficient and livable. The development of 5G networks enables faster and more reliable communication systems, crucial for smart city technologies. Japan's emphasis on disaster preparedness pushes innovations in resilient infrastructure, thereby driving the smart cities industry growth.

The China smart cities market is rapidly expanding, fueled by the country’s ambitious urbanization policies and large-scale infrastructure investments. Government-led initiatives such as the New Infrastructure Plan are accelerating the deployment of smart transportation, energy, and surveillance systems. Public-private partnerships are increasingly playing a role in scaling smart city solutions across tier-1 and tier-2 cities. This strategic alignment between policy, technology, and investment is propelling China’s position in the global smart cities landscape.

Key Smart Cities Company Insights

Some of the key players operating in the market include Cisco Systems, Inc. and Honeywell International Inc. among others

-

Cisco Systems, Inc. is a global leader in networking and IT infrastructure, providing innovative solutions that form the backbone of Smart Cities. The company enables cities to become more connected and efficient through its smart network architecture, IoT platforms, and cybersecurity solutions. Cisco's Smart+Connected Communities initiative focuses on transforming urban infrastructure by offering intelligent solutions for transportation, energy management, public safety, and digital governance. By leveraging cutting-edge technologies such as edge computing, AI, and 5G, Cisco helps cities gather and analyze real-time data to make informed decisions, improving citizen services and operational efficiency.

-

Honeywell International Inc. is a conglomerate known for its strong presence in industrial automation, smart building technologies, and environmental solutions, all crucial components of smart cities. Honeywell provides integrated systems that enhance building performance, energy efficiency, public safety, and urban mobility. Its offerings include smart thermostats, security systems, and building management tools, all designed to improve comfort, sustainability, and cost-effectiveness in urban environments. With a deep focus on digital transformation and operational intelligence, Honeywell plays a pivotal role in shaping the future of smart cities industry.

UrbanFootprint, Inc. and Quantela, Inc. are some of the emerging market participants in the smart cities market.

-

UrbanFootprint, Inc. is a data intelligence and urban planning company that empowers governments, utilities, and enterprises to build more sustainable and resilient cities. The company provides an advanced location intelligence platform that combines environmental, demographic, and infrastructure data to support smarter urban decision-making. UrbanFootprint’s solutions help cities optimize transportation, land use, energy, and disaster response strategies, using data-driven insights to improve public services and resource allocation. With a strong focus on sustainability and climate resilience, UrbanFootprint enables smart cities to plan future growth more effectively and equitably.

-

Quantela, Inc. is a digital infrastructure and smart cities automation company that delivers AI-powered solutions for urban management and public service efficiency. Its flagship platform, Atlantis, provides centralized, data-driven control for city operations such as traffic, waste management, public safety, and street lighting. Quantela partners with municipalities and governments globally to create intelligent urban ecosystems that are more efficient, responsive, and sustainable. By offering outcome-based solutions and leveraging predictive analytics, the company supports cities in optimizing resources, reducing operational costs, and enhancing citizen experiences in real time.

Key Smart Cities Companies

The following key companies have been profiled for this study on the smart cities market.

-

Cisco Systems, Inc.

-

Microsoft

-

International Business Machines Corporation (IBM)

-

Huawei Technologies Co., Ltd.

-

Honeywell International Inc.

-

Schneider Electric

-

Siemens

-

Hitachi, Ltd.

-

General Electric

-

NEC Corporation

-

UrbanFootprint, Inc.

-

Quantela, In

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Cisco Systems, Inc.; NEC Corporation; Huawei Technologies Co., Ltd.; Honeywell International Inc.

- Mature players focus on government contracts, integrated infrastructure projects, and large-scale smart city deployments.

- They invest heavily in AI, IoT, cloud, and digital twin technologies to expand smart city capabilities.

- Strong financial strength, global presence, and technical expertise support large-scale project execution.

- Broad solution portfolios and established government relationships improve market positioning and adoption rates.

- Complex organizational structures can slow innovation and customized solution deployment.

- High implementation costs and reliance on government funding may limit expansion in cost-sensitive regions.

Emerging Players: UrbanFootprint, Inc.; Quantela, Inc.

- Emerging players focus on niche applications such as urban analytics and AI-based city management solutions.

- They use agile models and partnerships to scale solutions across developing urban markets.

- These companies provide flexible and customized solutions with faster deployment capabilities.

- Strong expertise in AI analytics and cloud platforms improves operational efficiency for cities.

- Limited financial strength and lower brand recognition restrict large-scale project opportunities.

- Dependence on partnerships and external funding can create scalability challenges.

Recent Developments

-

In March 2025, Huawei and the Barcelona City Council announced a strategic collaboration at MWC Barcelona 2025 to support the development of smart city initiatives in Barcelona. The agreement focuses on key areas such as the City Command Center, Smart Buildings, Connectivity, Green Energy, and ICT Talent Development. The partnership, supported by Barcelona Activa’s IT Academy, aims to strengthen the city’s digital infrastructure and accelerate its smart cities industry.

-

In February 2025, IBM announced a collaboration with C40 Cities through its Sustainability Accelerator program to drive innovation in the Smart Cities sector. The initiative focuses on developing AI-driven solutions to enhance urban resiliency and tackle challenges faced by cities worldwide. This partnership aligns with the United Nations Sustainable Development Goal 11 and reflects IBM’s growing commitment to leveraging advanced technologies for smart cities.

-

In February 2025, Quantela Inc. announced a strategic partnership with Connected Kerb Inc. The partnership aims to optimize urban infrastructure for micromobility, Digital Out-of-Home (DOOH) advertising, IoT applications, and electric vehicle (EV) charging, helping cities across the U.S. create future-ready urban environments. This joint effort supports the development of smart cities.

Smart Cities Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 1.0 trillion

Market size value in 2026

USD 1.3 trillion

Revenue forecast in 2033

USD 8.8 trillion

Growth rate

CAGR of 31.9% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Application, smart governance, smart utilities, smart transportation, smart healthcare, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Germany; UK; Germany, France; Italy; Spain; Russia; Nordic Region; China; Japan; India; Australia; ASEAN, Brazil; Saudi Arabia; South Africa; UAE

Key companies profiled

Cisco Systems, Inc.; Microsoft; International Business Machines Corporation (IBM); Huawei Technologies Co., Ltd.; Honeywell International Inc.; Schneider Electric; Siemens; Hitachi, Ltd.; General Electric; NEC Corporation; UrbanFootprint, Inc.;

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Smart Cities Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest technological trends in each of the sub-segments from 2018 to 2030. For this study, Grand View Research has segmented the smart cities market report based on application, smart governance, smart utilities, smart transportation, smart healthcare, and region:

-

Application Outlook (Revenue, USD Trillion, 2021 - 2033)

-

Smart Governance

-

City Surveillance

-

C.C.S.

-

E-governance

-

Smart Lighting

-

Smart Infrastructure

-

-

Smart Building

-

Environmental Solution

-

Smart Utilities

-

Energy Management

-

Water Management

-

Waste Management

-

Meter Data Management

-

Distribution Management System

-

Substation Automation

-

Other Smart Utilities Solutions

-

-

Smart Transportation

-

Intelligent Transportation System

-

Parking Management

-

Smart Ticketing & Travel Assistance

-

Traffic Management

-

Passenger Information

-

Connected Logistics

-

Other Smart Transportation Solutions

-

-

Smart Healthcare

-

Medical Devices

-

Systems & Software

-

-

Smart Public Safety

-

Smart Security

-

Smart Education

-

-

Governance Outlook (Revenue, USD Trillion, 2021 - 2033)

-

City Surveillance

-

C.C.S.

-

E-governance

-

Smart Lighting

-

Smart Infrastructure

-

-

Utilities Outlook (Revenue, USD Trillion, 2021 - 2033)

-

Energy Management

-

Water Management

-

Waste Management

-

Meter Data Management

-

Distribution Management System

-

Substation Automation

-

Other Smart Utilities Solutions

-

-

Transportation Outlook (Revenue, USD Trillion, 2021 - 2033)

-

Intelligent Transportation System

-

Parking Management

-

Smart Ticketing & Travel Assistance

-

Traffic Management

-

Passenger Information

-

Connected Logistics

-

Other Smart Transportation Solutions

-

-

Smart Healthcare Outlook (Revenue, USD Trillion, 2021 - 2033)

-

Medical Devices

-

Systems & Software

-

-

Regional Outlook (Revenue, USD Trillion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Russia

-

Nordic Region

-

Eastern Europe

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

ASEAN

-

-

Latin America

-

Brazil

-

Mexico

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Type

Revenue capture definition

Smart Governance

Revenue is generated through government contracts for digital administration platforms such as e-governance portals, citizen service apps, digital identity systems, and AI-enabled decision-support systems. Monetization comes from project implementation fees, cloud hosting, and recurring maintenance or SaaS subscriptions funded by public sector digital transformation budgets.

Smart Building

Revenue is captured via B2B contracts for building management systems (BMS), IoT sensors, automation tools, and energy optimization software. Providers earn through hardware installation, software licensing, and recurring subscriptions for monitoring, predictive maintenance, and energy efficiency services, primarily driven by real estate developers and facility managers.

Environmental Solution

Revenue is generated from environmental monitoring and sustainability platforms tracking air quality, emissions, noise, and climate indicators. Monetization includes sensor deployment contracts, analytics subscriptions, and ESG reporting tools funded through government climate programs, green bonds, and sustainability initiatives.

Smart Utilities

Revenue comes from the digitization of utilities such as smart grids, water, gas, and waste systems. Vendors earn through large infrastructure contracts, IoT device deployment (smart meters and sensors), and recurring software revenues for monitoring, forecasting, and automated billing in partnership with utility providers.

Smart Transportation

Revenue is generated from intelligent transport systems including traffic management, smart ticketing, fleet tracking, and mobility-as-a-service platforms. Monetization includes system integration fees, SaaS analytics subscriptions, per-city deployment contracts, and revenue-sharing models with transport authorities.

Smart Healthcare

Revenue is captured through connected healthcare systems such as telemedicine platforms, remote patient monitoring, emergency response integration, and urban hospital IoT networks. Monetization includes platform subscriptions, government healthcare digitization contracts, and partnerships with hospitals and insurers.

Smart Public Safety

Revenue is derived from city emergency response systems, disaster management platforms, surveillance analytics, and incident detection tools. Providers earn via command-and-control system deployments, AI-based predictive safety solutions, and recurring monitoring and integration service contracts.

Smart Security

Revenue is generated from cybersecurity and physical security solutions protecting smart city infrastructure, including identity management, network security, and critical infrastructure protection. Monetization includes enterprise security subscriptions, managed security services, and government compliance-driven contracts.

Smart Education

Revenue comes from digital education infrastructure such as smart classrooms, AI-based learning platforms, and connected campuses. Monetization includes government education digitization programs, LMS licensing, device provisioning contracts, and recurring SaaS subscriptions for learning analytics and content delivery.

Estimation Model

Layer Name

Key Questions

Description

Urban Infrastructure Layer

Which cities are relevant for smart city deployments?

Identify global cities and urban areas investing in digital infrastructure, mobility, sustainability, governance, and public services to define the total addressable market.

Technology Readiness Layer

Which cities can realistically deploy smart city solutions?

Filter the addressable city base across regions using digital readiness factors like broadband, IoT, cloud, 5G, smart utilities, data infrastructure, and e-governance to identify capable cities and define the reachable smart cities market.

Solution Adoption Layer

Which cities adopt smart solutions?

Apply adoption rates across smart city solutions such as transport, energy, water, buildings, public safety, waste management, and e-governance to identify active deployments.

Monetisation Layer

How much revenue is generated?

Estimate annual per-city spending across IoT, software, sensors, connectivity, integration, consulting, and managed services, then multiply by active deployments to derive total market revenue.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Smart Transportation, Utilities & Urban Mobility Trends

Conducted a focused analysis of smart transportation systems, traffic management platforms, mobility-as-a-service (MaaS), smart grids, water and waste management systems, and IoT-enabled utility infrastructure, covering adoption trends, technology integration, and digital transformation across urban services.

Helps stakeholders identify high-growth urban infrastructure segments, evaluate efficiency and sustainability gains, and assess monetization opportunities in data-driven mobility and utility ecosystems.

Smart Governance, Public Services & Citizen Experience Adoption Trends

Evaluated digital governance platforms including e-governance portals, digital identity systems, citizen engagement apps, AI-driven public service delivery, and integrated urban management dashboards, along with adoption maturity across regions and city tiers.

Provides insights into government digitization priorities, citizen engagement trends, and scalable platform opportunities for improving transparency, efficiency, and service delivery outcomes.

Smart City Infrastructure & Integrated Urban Intelligence Assessment

Assessed demand for integrated smart city platforms combining IoT networks, cloud-based urban data systems, AI analytics, surveillance and public safety infrastructure, and cross-domain city operating systems, along with interoperability, cybersecurity, and data governance challenges.

Supports investment and expansion strategies by identifying high-readiness cities, evaluating digital infrastructure maturity, and highlighting opportunities for unified urban intelligence platforms enabling long-term scalable growth.

Frequently Asked Questions About This Report

The global smart cities market was valued at USD 1.0 trillion in 2025 and is expected to reach USD 1.3 trillion in 2026.

The global smart cities market is expected to grow at a compound annual growth rate of 31.9% from 2026 to 2033, reaching USD 8.8 trillion by 2033.

Some key players operating in the smart cities market include Cisco Systems, Inc.; Microsoft; International Business Machines Corporation (IBM); Huawei Technologies Co., Ltd.; Honeywell International Inc.; Schneider Electric; Siemens; Hitachi, Ltd.; General Electric; NEC Corporation; UrbanFootprint, Inc.

Asia Pacific dominated the global market with a revenue share of over 51% in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The growing urbanization, need for efficient management and utilization of resources, public safety concerns, and increasing demand for a healthy environment with efficient energy consumption are anticipated to be the key driving factors for the growth of the smart cities market.

The smart utility segment held with the largest revenue share in 2025, while smart transportation is the fastest-growing segment.

The smart infrastructure segment led with a 27.6% revenue share in 2025, while smart lighting is the fastest-growing model.

The energy management segment dominated with a revenue share of 27.2% in 2025, while water management segment is the significant-growing area.

The intelligent transportation system segment held the largest revenue share of 29.4% in 2025, while other smart ticketing & travel assistance segment is the significant-growing model.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.