- Home

- »

- Advanced Interior Materials

- »

-

Graphene Market Size, Share, Growth, Industry Report 2033GVR Report cover

![Graphene Market Size, Share & Trends Report]()

Graphene Market (2026 - 2033) Size, Share & Trends Analysis Report By Product (Graphene Oxide, Monolayer Graphene, Reduced Graphene Oxide, Graphene Nanoplatelets), By Application (Paints & Coatings, Electronic Components), By End Use, By Region, And Segment Forecasts

Market Size, 2025

$341.4MMarket Estimate, 2026

$456.8MMarket Forecast, 2033

$4,569.9MCAGR, 2026–2033

39.0%Graphene Market Summary

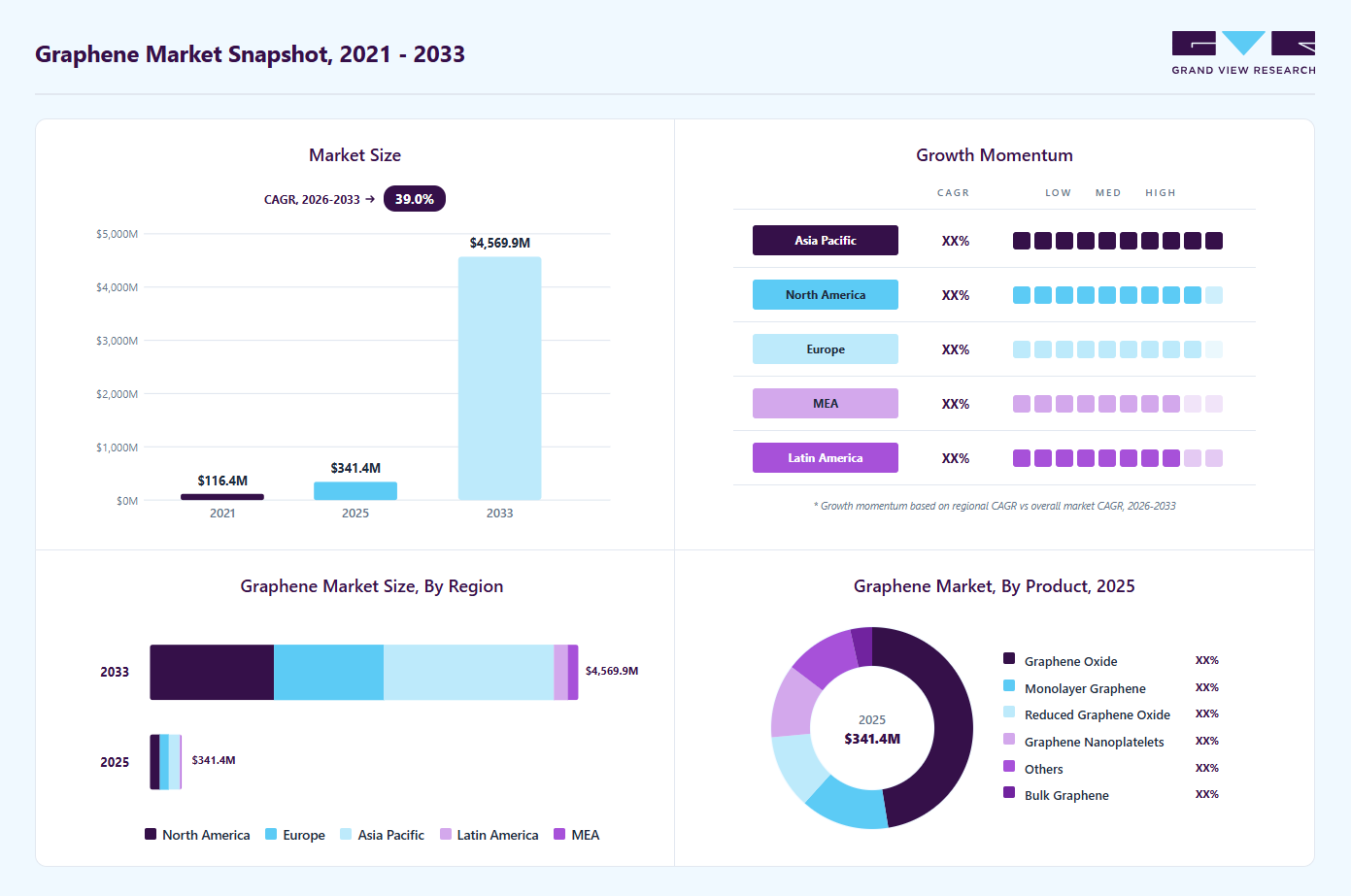

The global graphene market size was valued at USD 341.4 million in 2025 and is projected to grow from USD 456.8 million in 2026 to USD 4,569.9 million by 2033, at a CAGR of 39.0% from 2026 to 2033. The Asia Pacific graphene market held the largest share of 33.4% of the global market in 2025. Increasing demand for lightweight, high-strength, and highly conductive materials in industries such as electronics, energy storage, and automotive is driving the adoption of graphene.

Key Market Trends & Insights

- By product: Graphene oxide segment is projected to register a CAGR of 39.7% during 2026-2033.

- By application: Composites segment is anticipated to grow at a CAGR of 39.5% from 2026 to 2033.

- By end use: Automotive segment accounting for over36.0% of the total market share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (33.4% revenue share, 2025)

- By country: The graphene industry in the U.S. is expected to grow at healthy CAGR over the forecast period.

Market Size & Forecast

- Market size in 2025: USD 341.4 Million

- Estimated market size in 2026: USD 456.8 Million

- Projected market size by 2033: USD 4,569.9 Million

- CAGR (2026-2033): 39.0%

Rapid advancements in nanotechnology and expanding applications in batteries, supercapacitors, coatings, and composite materials are further accelerating the growth of the graphene industry. The growth of the graphene industry is primarily driven by the increasing demand for high-performance materials across advanced manufacturing sectors such as electronics, energy storage, automotive, and aerospace. Graphene’s exceptional electrical conductivity, mechanical strength, and thermal stability make it a highly desirable material for next-generation products. As industries seek lighter, stronger, and more efficient materials, the adoption of graphene-based solutions continues to expand. This demand is particularly evident in the graphene sheet market, where high-purity graphene sheets are widely utilized in flexible electronics, sensors, and conductive films due to their superior electron mobility and thin structure.Graphene’s ability to enable ultra-fast electron transport and miniaturized device architectures is attracting strong interest from semiconductor manufacturers and research institutions. This has accelerated innovation in the graphene chip market, where graphene is being explored as a potential alternative or complement to silicon in high-speed computing, photonics, and next-generation integrated circuits. In addition, the emergence of 3D graphene market solutions, such as graphene foams and porous structures, has expanded opportunities in energy storage, particularly in batteries and supercapacitors, where enhanced surface area and conductivity significantly improve performance.

")

Sustainability and bio-based material innovation are also fueling industry expansion. Researchers and manufacturers are increasingly exploring cost-effective and environmentally friendly production routes, including biomass-derived graphene. This trend is evident in the growing lignin based graphene industry, where lignin sourced from biomass and paper industry by-products is used as a precursor for graphene production. Such developments not only reduce production costs but also align with global sustainability goals, making graphene more commercially viable for large-scale industrial applications across energy, packaging, and electronics sectors.

Furthermore, the integration of graphene into multifunctional materials is significantly boosting demand across several downstream industries. The graphene composites market is witnessing strong growth as manufacturers incorporate graphene into polymers, metals, and ceramics to enhance strength, conductivity, and durability. At the same time, the graphene coating market is expanding due to rising demand for anti-corrosion, conductive, and protective coatings in automotive, marine, construction, and electronics applications. Together, these developments highlight how graphene’s versatility and performance advantages are positioning it as a transformative material across multiple emerging technology markets.

Market Dynamics

Research activities focused on improving the performance, energy density, and sustainability of lithium-ion batteries are increasing globally. Scientists and battery manufacturers are actively exploring advanced materials to address limitations of conventional lithium-ion batteries, including high costs, limited driving range in electric vehicles, and dependency on lithium and cobalt supply chains. Growing emphasis on sustainable energy storage technologies is accelerating investments in next-generation battery research across automotive, electronics, and renewable energy industries.

Graphene is emerging as a promising material in advanced battery research due to its exceptional thermal conductivity, electrical conductivity, and chemical stability. Researchers are increasingly incorporating graphene into lithium-ion battery electrodes to enhance conductivity, improve energy density, increase charge retention, and extend battery life cycles. Although all-graphene batteries remain in the experimental stage, ongoing R&D activities related to graphene-enhanced electrodes and energy storage systems are expected to create significant growth opportunities for the graphene industry over the coming years.

Graphene is still in its nascent stage; the majority of graphene applications are in laboratory or trial phases of development and have not been commercialized to their full potential for most application areas. The lack of viable cost-effective mass-production technology is the major bottleneck restraining the widespread adoption of graphene. Applications such as electrochemical sensing, solar cells, supercapacitors, LCD smart windows, OLED displays, data storage, and high-speed electronics require defect-free and grain boundary-free graphene in large quantities. In addition, equipment required for the production of high-quality, single-layer graphene is expensive, however, it creates quality issues during large-scale production. Several companies and research institutes are working to mitigate this challenge to enhance the quality of materials produced and develop superior graphene nanoplatelets and graphene oxide films.

Market Concentration & Characteristics

The graphene industry is characterized by rapid technological innovation, strong research intensity, and a growing transition from laboratory-scale development to commercial-scale production. Since graphene is considered a next-generation nanomaterial with exceptional electrical, thermal, and mechanical properties, the industry is heavily driven by R&D activities conducted by universities, research institutes, and private companies.

Cost reduction and scalable manufacturing remain defining characteristics of the graphene industry. While graphene offers exceptional performance advantages, large-scale commercialization has historically been constrained by high production costs and inconsistent material quality. As a result, manufacturers are increasingly focusing on the development of cost-efficient production technologies and alternative raw material sources to improve scalability and commercial viability.

A notable example is the lignin based graphene industry, where lignin, a renewable byproduct of the pulp and paper industry, is utilized as a precursor for graphene production. This approach supports more sustainable and economical manufacturing processes while enhancing supply chain efficiency. Such advancements are enabling wider adoption of graphene materials beyond niche high-technology applications and facilitating their integration into broader industrial and commercial markets.

Product Insights

The graphene oxide segment dominated the market in 2025, accounting for 47.4% of revenue share, primarily due to its cost-effective production, high scalability, and ease of chemical functionalization compared to other graphene forms. Its excellent dispersibility in water and polymers makes it widely used in coatings, composites, membranes, and energy storage applications, enabling broader commercial adoption across multiple industrial sectors.

Monolayer graphene represents a high-value product segment characterized by a single atomic layer of carbon arranged in a hexagonal lattice, offering exceptional electrical conductivity, transparency, and mechanical strength. It is widely utilized in advanced applications such as high-frequency electronics, photonics, flexible displays, and next-generation semiconductor devices. Growing research and commercialization efforts in nanoelectronics and sensing technologies are expected to drive demand for monolayer graphene in specialized high-performance markets.

Application Insights

The electronic components segment accounted for 29.4% of the market in 2025, driven by the material’s exceptional electrical conductivity, high electron mobility, and thermal management capabilities. Graphene is increasingly used in applications such as transistors, sensors, conductive inks, flexible circuits, and advanced semiconductor devices, supporting the development of next-generation electronics. The growing demand for miniaturized, high-performance, and energy-efficient electronic components continues to accelerate graphene adoption in this segment.

The composites segment represents a significant application area in the market due to graphene’s ability to enhance mechanical strength, electrical conductivity, and thermal stability when incorporated into polymer, metal, and ceramic matrices. Graphene-based composites are increasingly used in industries such as automotive, aerospace, construction, and sports equipment to develop lightweight yet high-performance materials. Growing demand for advanced lightweight materials and durable structural components continues to drive adoption of graphene composites across industrial manufacturing sectors.

End Use Insights

The automotive segment dominated the market in 2025, accounting for over 36.0% of the total market share, driven by increasing adoption of graphene in lightweight composites, conductive coatings, batteries, and thermal management systems. Automakers are integrating graphene-based materials to improve vehicle efficiency, durability, and energy storage performance, particularly in electric vehicles. The growing focus on lightweighting, battery efficiency, and advanced materials continues to support strong graphene demand in the automotive sector.

The medical segment represents an emerging end use area in the market due to graphene’s high surface area, biocompatibility, and antimicrobial properties. It is increasingly explored in applications such as biosensors, drug delivery systems, tissue engineering, and medical coatings. Growing research in nanomedicine and advanced biomedical devices is expected to support the adoption of graphene in healthcare and life sciences applications.

Regional Insights

Asia Pacific graphene industry dominated the global market in 2025, accounting for over 33.4% of market share and is expected to grow at the fastest CAGR of 42.1% during the forecast period, driven by strong investments in advanced materials, electronics manufacturing, and energy storage technologies. Countries such as China, Japan, and South Korea are leading in graphene research, commercialization, and large-scale production. The presence of major electronics manufacturers and growing demand for graphene in automotive batteries, coatings, and semiconductor applications further supports regional market growth.

North America Graphene Market Trends

North America graphene industry represents a key market for graphene, driven by strong investments in nanotechnology research, advanced material innovation, and the presence of leading technology companies. The region benefits from extensive R&D activities supported by institutions and government initiatives, including programs from organizations such as the National Science Foundation. Growing demand for graphene in electronics, aerospace, energy storage, and advanced composites, particularly in the United States and Canada, continues to support market expansion across North America.

U.S. Graphene Market Trends

The graphene industry in the U.S. is driven by the demand for graphene in the United States and it is expected to increase due to rising investments in advanced materials and nanotechnology research. The country has a strong ecosystem of technology companies, universities, and startups actively working on graphene-based innovations. Growing applications in energy storage, electronics, and aerospace are also supporting its adoption. In addition, the rapid development of electric vehicles and next-generation batteries is increasing the need for high-performance conductive materials. Government funding for defense and semiconductor technologies further encourages graphene research and commercialization. As a result, expanding industrial and research activities are expected to drive higher graphene demand in the U.S. market.

Europe Graphene Market Trends

Europe graphene industry represents a significant market for graphene, supported by strong government funding, advanced research infrastructure, and growing industrial adoption of nanomaterials. Initiatives such as the Graphene Flagship have accelerated graphene research, commercialization, and collaboration between universities and industry players. Increasing applications in automotive, aerospace, energy storage, and advanced coatings across countries such as Germany, the UK, and France are further supporting market growth in the region.

Key Graphene Company Insights

The graphene industry is characterized by a moderately fragmented and innovation-driven competitive environment, with the presence of specialized nanomaterial manufacturers, research-driven startups, and large advanced materials companies. Competition is primarily based on product quality, scalability of production, cost efficiency, and application-specific material development, particularly for graphene oxide, graphene sheets, and graphene composites.

Many companies focus on strategic collaborations with research institutions, technology licensing, and partnerships with electronics, automotive, and energy storage manufacturers to accelerate commercialization and expand their application portfolios. In addition, continuous investments in R&D, pilot-scale manufacturing facilities, and sustainable production methods are key competitive strategies adopted by market participants.

-

In March 2026, Graphene Manufacturing Group (GMG) approved an additional USD 0.92 million USD, the remaining capital for its Gen 2.0 Graphene Production Plant in Brisbane, Australia, with a total cost of USD 1.52 million USD, targeting 10 tons per annum capacity by mid-2026.

-

In November 2025, OCSiAl launched development of the world’s largest graphene nanotube manufacturing hub in Differdange, Luxembourg, with a USD 300 million deep-tech investment following a land lease with the state and funding from local investors. The scalable, energy-efficient facility, set for gradual production ramp-up between 2028-2030, boost nanotube output for automotive plastics/rubbers, electronics, and batteries, and position Europe as an advanced materials leader.

Key Graphene Companies:

The following key companies have been profiled for this study on the graphene market.

- Applied Graphene Materials

- 2D Carbon Graphene Material Co., Ltd.

- Thomas Swan & Co. Ltd.

- Graphene Laboratories, Inc.

- Graphensic AB

- GRAPHENE SQUARE INC

- AMO GmbH

- Talga Group

- ACS Material

- BGT Materials Limited, Ltd.

- CVD Equipment Corporation

- Directa Plus S.p.A.

- Grafoid Inc

- Graphenea

- NanoXplore Inc.

- HAYDALE GRAPHENE INDUSTRIES PLC

- Zentek Ltd.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: NanoXplore Inc; CVD Equipment Corporation; Talga Group; Directa Plus S.p.A

- Focus on products that serve high growth markets, such as high-power electronics.

- Extend its market-leading position, through capacity expansion.

- Continuous investment in new product development.

- Able to employ large economies of scale to reduce the per-unit cost of the product.

- Strong distribution network.

- Superior market goodwill leads to an ease in gaining new contacts.

- Expansion to external markets through investments to expand presence in different markets.

Emerging Players: Graphene Laboratories Inc.; Graphensic AB; Graphene Square Inc; ACS Material

- A low-cost strategy for businesses to gain an advantage in the market.

- A company form strategic affiance with other companies having the technological expertise to outcompete strong competitors.

- A company may adopt a cooperative strategy (strategic alliance) by forming a partnership with key suppliers of materials and components.

- Acquisition strategy is followed to acquire skills so that the company can weaken the competitors.

- High market experience in niche product segments.

- Deployment of robust distribution networks to cater to the local market in the area of operation.

Graphene Market Report Scope

Report Attribute

Details

Market size in 2025

USD 341.4 million

Estimated market size in 2026

USD 456.8 million

Projected market size by 2033

USD 4,569.9 million

Growth rate

CAGR of 39.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million, Volume in Tons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, volume forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, end use,region

Regional Scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Key companies profiled

Applied Graphene Materials; 2D Carbon Graphene Material Co., Ltd.; Thomas Swan & Co. Ltd.; Graphene Laboratories, Inc.; Graphensic AB; GRAPHENE SQUARE INC; AMO GmbH; Talga Group; ACS Material; BGT Materials Limited, Ltd.; CVD Equipment Corporation; Directa Plus S.p.A.; Grafoid Inc; Graphenea; NanoXplore Inc.; HAYDALE GRAPHENE INDUSTRIES PLC; Zentek Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail of customized purchase options to meet your exact research needs. Explore purchase options

Global Graphene Market Report Segmentation

This report forecasts revenue growth at the regional and country levels and provides an analysis on the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global graphene market report based on product, application, end use and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Graphene Oxide

-

Monolayer Graphene

-

Reduced Graphene Oxide

-

Graphene Nanoplatelets

-

Bulk Graphene

-

Others

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Electronic Components

-

Batteries

-

Paints & Coatings

-

Composites

-

Solar Panels

-

Others

-

-

End Use Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Automotive

-

Aerospace

-

Medical

-

Concrete Industry

-

Defense

-

Tires

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Opportunity Assessment

Assessment of growth opportunities across energy storage, electronics, coatings, composites, automotive, aerospace, and semiconductor applications, along with analysis of emerging trends such as graphene-enhanced batteries, conductive materials, lightweight composites, and flexible electronics.

Enables identification of high-growth application areas and emerging commercialization opportunities, supporting strategic investment and product development decisions.

Pricing Analysis

Comparative pricing analysis across graphene product types including graphene nanoplatelets, graphene oxide, reduced graphene oxide, and monolayer graphene, with pricing assessment by application and end-use industries across major regions.

Supports procurement strategy, supplier benchmarking, and cost optimization by identifying pricing variations across graphene grades, production methods, and application industries.

Market Disruptions

Analysis of key market disruptions including raw material supply challenges, scalability limitations in graphene production, evolving commercialization trends, technological advancements, regulatory developments, and shifts in demand across energy, electronics, and advanced material industries.

Helps companies assess market uncertainties, evaluate supply chain risks, and develop resilient business and commercialization strategies in a rapidly evolving market environment.

Frequently Asked Questions About This Report

The key factors that are driving the graphene market includes increasing application of the product in various end use industries such as automotive, construction, electronics, energy storage and coatings.

Asia Pacific dominated with a 33.4% revenue share in 2025.

The electronic components segment led with a 29.4% revenue share in 2025.

Automotive segment held the largest share (over 36.0%) in 2025.

The graphene oxide dominated the market with the revenue share of 47.4% in 2025 owing to the rising penetration of the product in wide range of applications coupled with the possibility of large quantity production.

The global graphene market size was valued at USD 341.4 million in 2025 and is estimated at USD 456.8 million for 2026.

The global graphene market is expected to grow at a CAGR of 39.0% from 2026 to 2033, reaching USD 4,569.9 million by 2033.

Key players include Applied Graphene Materials; 2D Carbon Graphene Material Co., Ltd.; Thomas Swan & Co. Ltd.; Graphene Laboratories, Inc.; Graphensic AB; GRAPHENE SQUARE INC; AMO GmbH; Talga Group; ACS Material; BGT Materials Limited, Ltd.; CVD Equipment Corporation; Directa Plus S.p.A.; Grafoid Inc; Graphenea; NanoXplore Inc.; HAYDALE GRAPHENE INDUSTRIES PLC; Zentek Ltd.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.