- Home

- »

- Medical Devices

- »

-

Heart-lung Machine Market Size & Share Report, 2026-2033GVR Report cover

![Heart-lung Machine Market Size, Share & Trends Report]()

Heart-lung Machine Market (2026 - 2033) Size, Share & Trends Analysis Report By Product (Capital Equipment, Consumables), By Application (Coronary Artery Bypass Grafting, Heart Valve Surgeries), By End Use, By Region, And Segment Forecasts

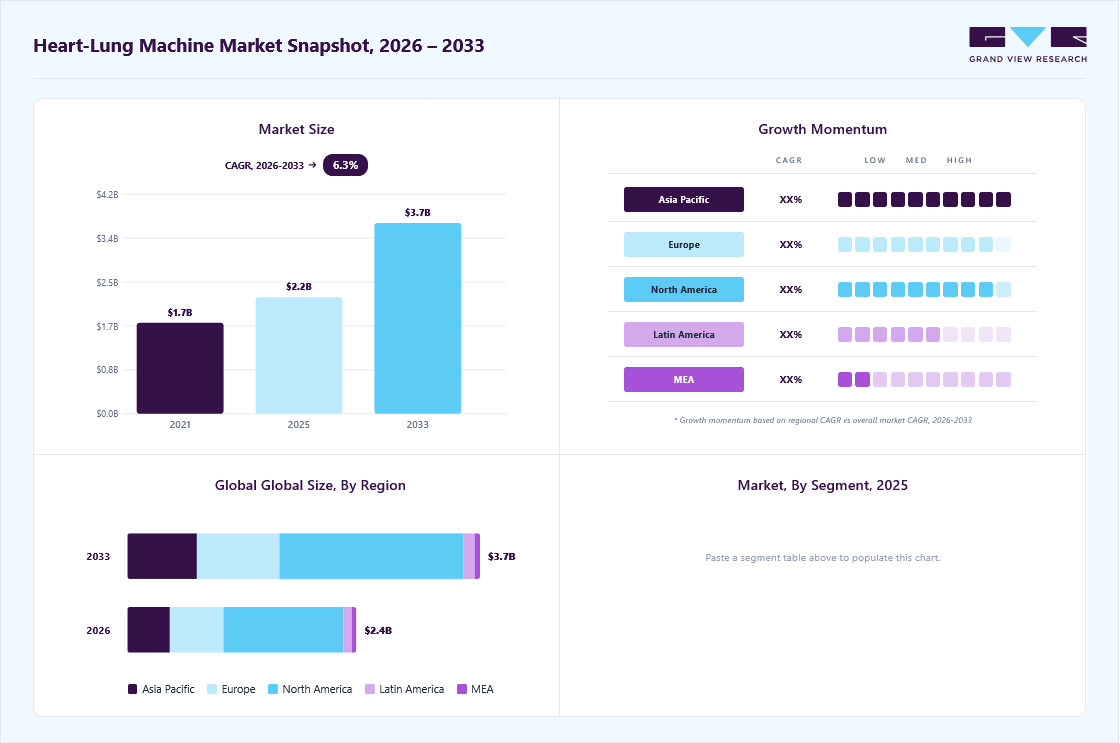

Market Size, 2025

$2.2BMarket Estimate, 2026

$2.4BMarket Forecast, 2030

$3.7BCAGR, 2026–2030

6.4%Heart-lung Machine Market Summary

The global heart-lung machine market size was valued at USD 2.2 billion in 2025 and is projected to grow from USD 2.4 billion in 2026 to USD 3.7 billion by 2033, at a CAGR of 6.4% from 2026 to 2033. North America dominated the global market in 2025, accounting for the largest revenue share of 52.1%. The increasing burden of cardiovascular diseases, the rising number of open-heart surgeries, the adoption of technologically advanced perfusion systems, and the expansion of healthcare facilities in both emerging and developed regions are key aspects driving the market's growth.

Key Market Trends & Insights

- By product: Consumables segment dominated the heart-lung machine market in 2025 and accounted for the largest revenue share of 68.24%.

- By application: Coronary Artery Bypass Grafting (CABG) segment dominated the industry in 2025 and accounted for the largest revenue share of 31.56%.

- By end-use: Public healthcare institutions segment dominated the market for heart-lung machines in 2025 with a revenue share of 55.38%.

Regional Highlights

- Largest regional market: North America (52.06% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- The heart-lung machine industry in the U.S. held the largest share, 88.04% in 2025.

Market Size & Forecast

- Market size in 2025: USD 2.2 Billion

- Estimated market size in 2026: USD 2.4 Billion

- Projected market size by 2033: USD 3.7 Billion

- CAGR (2026-2033): 6.4%

In October 2025, Cleveland Clinic highlighted advances in ex vivo lung perfusion (EVLP), a perfusion-based system functionally aligned with heart-lung machine technologies, to assess and preserve donor lungs before transplantation.")

The growth of heart and lung transplant programs is driving rising demand for advanced perfusion and extracorporeal support technologies, including heart-lung machines and associated consumables. In February 2025, the American Journal of Transplantation reported that U.S. adult heart transplants reached 4,092 in 2023, a 101.1% increase since 2012, with waitlist mortality falling to 8.5 deaths per 100 patient-years. Pediatric heart transplants also rose 36.3%, although the transplant rate declined 14.9%, and 5-year post-transplant survival rates were 80.3% for adults and 84.4% for children.In 2023, adult heart transplant rates varied by patient status, with Status 1 to 6 ranging from the highest urgency (Status 1) to the least urgent (Status 6), based on clinical condition and transplant need.

Collaboration between device manufacturers and hospitals is the prominent driver of growth in the heart-lung machine market, as it reduces the time from prototype to clinical use. Major manufacturers and specialist perfusion companies, such as LivaNova PLC and Getinge AB, conduct targeted clinical trials and regulatory programs in collaboration with cardiac centers to validate new cardiopulmonary bypass and ECMO platforms in real-world settings. Achieving regulatory milestones and generating early clinical data directly support broader procurement and hospital adoption. In December 2025, NHS Wales Shared Services Partnership entered into a service agreement with LivaNova UK Limited for the maintenance of heart-lung machines and autotransfusion systems supporting the Cardiothoracic Directorate at Cardiff & Vale University Health Board, covering the period from September 2025 to August 2026.

Table 1: Technological partnerships and collaborations

Company Name

Year

Month

Description

Save a Child’s Heart & American Jewish Committee

2025

August

Donated a LivaNova S-5 heart-lung machine to Zambia’s National Heart Hospital, doubling pediatric cardiac-surgery capacity and supporting local staff training.

Integration Health

2025

August

Integration Health launched as a strategic platform unifying ECMO, perfusion, and Normothermic Regional Perfusion (NRP) services across hospitals and organ procurement organizations in the U.S. The structure consolidates recognized brands such as Innovative ECMO Concepts and Innovative Perfusion Concepts under one umbrella.

Moreover, the industry is undergoing significant change. These systems are essential for open-heart and complex thoracic procedures, while advances in surgical techniques, automation, and patient management are redefining their use. Hospitals and surgical centers are adopting new platforms that enhance clinical outcomes, reduce perfusion times, and minimize blood loss, supporting the shift toward precision-driven and minimally invasive cardiac care. In October 2025, Stanford Medicine expanded its minimally invasive coronary artery bypass grafting (CABG) program, which includes robotic-assisted and MIDCAB procedures, offering patients a faster recovery and reduced pain.

In addition, growing awareness and adoption of advanced cardiopulmonary bypass (CPB) techniques are driving the heart-lung machine market. Hospitals and cardiac centers are increasingly recognizing the benefits of modern CPB, which enables precise control of circulation and oxygenation during complex surgeries. This is prompting procurement of heart-lung machines with improved pumps, oxygenators, and integrated monitoring systems. The trend is particularly pronounced in tertiary and high-volume cardiac centers, which aim to enhance surgical efficiency and patient safety. In July-August 2025, a cross-sectional study in Iran reported high levels of awareness, attitude, and self-care behaviors among 138 post-CABG patients, highlighting that education and targeted nursing interventions significantly improve self-management and recovery outcomes.

Market Concentration & Characteristics

The heart-lung machine industry shows a high degree of innovation, driven by incremental advancements aimed at improving patient safety, surgical efficiency, and personalized perfusion. Key developments include smarter perfusion platforms, improved biocompatible materials, enhanced imaging and robotic compatibility, and data-driven monitoring. For instance, in August 2025, LivaNova PLC initiated the commercial launch of its Essenz Perfusion System in China following NMPA approval, expanding access in its second-largest heart-lung machine market after the U.S. The next-generation perfusion platform strengthens LivaNova’s cardiopulmonary footprint in China, with Essenz having supported over 100,000 patients globally since its 2023 debut.

The level of M&A activity is moderate but strategically focused, with leading players pursuing targeted acquisitions to expand portfolios and access high-growth adjacencies. Transactions are primarily aimed at strengthening acute heart and lung support capabilities, transplant-related technologies, and geographic presence, particularly in the U.S. For instance, in August 2024, Getinge AB acquired Paragonix Technologies for approximately USD 477 million, thereby entering the organ preservation and transportation segment and reinforcing Getinge’s position in advanced cardiopulmonary and transplant technologies.

The impact of regulations on the market for heart-lung machines is significant, as these systems are classified as high-risk, life-support medical devices and are subject to stringent approval, quality, and post-market surveillance requirements. Regulatory frameworks mandate robust clinical validation, biocompatibility testing, and compliance with international standards, which increases development timelines and costs but ensures high safety and performance benchmarks. While strict regulations can slow new product launches, they also limit low-quality competition and favor established manufacturers with strong regulatory expertise, thereby shaping market entry, innovation pace, and global expansion strategies.

The threat of product substitutes for heart-lung machines is low, as they are essential life-support systems required for open-heart and complex cardiac surgeries. While alternatives such as minimally invasive cardiac techniques, catheter-based interventions, and extracorporeal life support systems can reduce reliance on traditional cardiopulmonary bypass in selected cases, they cannot fully replace heart-lung machines in procedures requiring complete circulatory and respiratory support.

Companies operating in the market are expanding into regions with the rising incidences of cardiovascular disease, focusing on countries with increasing cardiac surgery demand. This expansion is supported by partnerships with local hospitals, distributors, and healthcare institutions, helping manufacturers extend their reach and strengthen regional presence.

Product Insights

By product, the consumables segment dominated the heart-lung machine market in 2025 and accounted for the largest revenue share of 68.24%. Rising CVD cases and the launch of technologically advanced products drive the growth of the market. For instance, in May 2024, Hemovent GmbH’s MOBYBOX portable pneumatic ECMO completed initial European use, showing mobility for hospital transfers. Weighing 2.5 kg and operating without external power, it supports heart and lung function for conditions such as cardiac arrest and severe respiratory failure, enabling ECMO use beyond ICUs in ambulances, ships, and aircraft.

“Our completely new approach to pump drive, to handle blood flow as well as the safety, simplicity, and compactness of the entire ECMO system, will allow MOBYBOX to serve both traditional in-hospital settings and mobile medical scenarios, playing a crucial role in scenarios like intra-hospital and outdoor transport, as well as outdoor rescue. We are very proud of our achievements thus far and are actively expanding its market access in more countries, with the aim of extending the benefits of this technology to more patients.”

-CEO & CMO of Hemovent

The capital equipment segment is anticipated to witness the significant CAGR over the forecast period. The growing number of complex cardiac and cardiothoracic surgeries requiring extracorporeal circulation and ongoing technological and clinical advancements that enhance patient outcomes and optimize intraoperative management, increasing hospital investment in advanced heart-lung systems are the key aspect that drives the growth of the market. For instance, in September 2024, a University of Bristol led randomized clinical trial published in the Journal of the American Heart Association reported that maintaining low frequency ventilation during use of an existing heart lung machine in adult heart valve surgery was feasible and safe, with preserved postoperative lung function and improved exercise capacity.

Application Insights

The Coronary Artery Bypass Grafting (CABG) segment dominated the industry in 2025 and accounted for the largest revenue share of 31.56%. There has been an increasing demand for cardiopulmonary bypass in complex and high-risk cases and a growing volume of elderly and multi-comorbidity patients undergoing CABG. According to the AME Publishing Company article published in August 2025, an extensive single-center study published in 2025 showed that in patients with left main coronary disease, off-pump CABG performed by experienced surgeons achieved 5-year outcomes comparable to on-pump CABG, suggesting that, in high-volume centers, select cases may safely be managed without full extracorporeal support while maintaining low conversion rates to CPB and minimizing operative complications. However, as per the JAMA Network article published in February 2022, long-term evidence from multicenter trials such as the ROOBY trial indicates that over 10 years, traditional on-pump CABG with heart-lung machine support did not increase survival or reduce repeated revascularization relative to off-pump, strengthening that CPB-supported surgery remains a standard approach where a complete and durable revascularization strategy is required.

The heart valve surgeries segment is anticipated to witness the fastest CAGR over the forecast period. Rising prevalence of age-related valvular heart disease and the clinical necessity for precise, controlled surgical environments are key drivers supporting heart-lung machine use in valve procedures. According to a SAGE Publications article published in July 2025, heart valve surgeries such as aortic and mitral repair or replacement are performed under cardiopulmonary bypass (CPB), where heart-lung machines temporarily assume cardiac and pulmonary functions to enable motionless, bloodless access, with ongoing refinement of goal-directed perfusion and advanced monitoring strategies helping reduce complications and improve postoperative recovery.

End Use Insights

The public healthcare institutions segment dominated the market for heart-lung machines in 2025 with a revenue share of 55.38%. High surgical volumes in government-funded hospitals, combined with continued public investment in advanced cardiac infrastructure, are key drivers of heart-lung machine demand. For instance, according to an article published in December 2025 by the National Health Service, public healthcare institutions perform around 28,000 cardiac surgeries annually, with cardiopulmonary bypass remaining the standard of care for valve replacement and complex coronary procedures, supported by ongoing upgrades to cardiac operating theatres and perfusion equipment.

The private healthcare institutions segment is anticipated to register the fastest growth rate over the forecast period. Rising demand for advanced cardiac care and the adoption of innovative surgical technologies in private hospitals are key drivers supporting the use of heart-lung machines. For instance, in December 2025, private cardiac centres in the U.S., including the robotic cardiac surgery program at New York‑Presbyterian/Columbia, demonstrated how heart-lung machines continue to support complex procedures alongside robotic and minimally invasive techniques, with the program having completed over 300 robotic heart surgeries, including intricate mitral valve repairs.

Moreover, in November 2025, the Baptist Health Miami Cardiac & Vascular Institute, a specialized team, achieved its 100th robotic cardiac surgery milestone since the program’s launch, reflecting growing procedural volume and patient access within a private hospital setting. These milestones demonstrate how private U.S. institutions are leveraging emerging techniques while still relying on comprehensive heart-lung machine support for open and hybrid cardiac surgical workflows.

Regional Insights

The North America heart-lung machine industry dominated the global market in 2025, accounting for the largest revenue share of 52.1%, due to rising CVD incidence, government initiatives, and technological advancements. According to the National Heart, Lung, and Blood Institute in June 2025, in the Fiscal Year (FY) 2025 appropriations process, the U.S. Congress authorized approximately USD 3.98 billion in funding for the National Heart, Lung, and Blood Institute (NHLBI) as part of the Departments of Labor, Health and Human Services, and Education appropriations bill. This level of funding indicates sustained federal support for research on heart, lung, blood, and sleep disorders, including cardiovascular disease, which continues to be a leading cause of mortality. The allocation is aligned with the NHLBI’s objectives to advance prevention, diagnosis, treatment, and innovation, with congressional appropriations emphasizing cardiovascular research aimed at reducing disease burden and improving outcomes in heart disease and congenital heart conditions.

U.S. Heart-Lung Machine Market Trends

The heart-lung machine industry in the U.S. held the largest share, 88.04% in 2025. The increasing incidence of cardiovascular disease is driving the growth of the market. According to the TCTMD article published in January 2025, there are an estimated 128 million adults living with conditions such as coronary heart disease, heart failure, stroke, and hypertension. This high prevalence reflects a large and growing pool of patients at risk of developing advanced cardiac complications. Cardiovascular disease also continues to be a leading cause of mortality, with an age-adjusted death rate of about 224.3 deaths per 100,000 people. The mortality burden is notably higher among men compared with women, highlighting differences in disease severity and progression.

The Canada heart-lung machine industry is anticipated to register the fastest growth rate during the forecast period. The increasing incidence of CVD and rising government initiatives significantly drive the market's growth. For instance, in September 2024, the Canadian Institutes of Health Research (CIHR), the Government of Canada, Heart & Stroke, and Brain Canada announced a USD 10 million investment to establish two national research networks. One focuses on improving heart health during and after pregnancy, while the other addresses stroke in women, with each network receiving USD 5 million over five years.

Europe Heart-Lung Machine Market Trends

The heart-lung machine industry in Europe is anticipated to register a significant growth rate during the forecast period. The high mortality rate from cardiovascular diseases boosts demand for heart-lung machines in Europe. According to the WHO article published in May 2024, cardiovascular diseases (CVDs) are the leading cause of disability and premature death in the European region, responsible for over 42.5% of all deaths annually. This staggering statistic translates to approximately 10,000 deaths every day. The scale of CVD prevalence continues to drive demand for advanced cardiac care, including open-heart procedures and other complex surgeries that rely on heart-lung machines to maintain circulation and oxygenation during intervention.

The UK heart-lung machine industry is anticipated to register a significant growth rate during the forecast period. Advanced cardiopulmonary bypass technology continues to be integrated into cardiac surgical care in the UK, reflecting ongoing clinical demand and modernization of cardiac support systems. For instance, in May 2025, London’s Air Ambulance introduced a groundbreaking pre-hospital extracorporeal membrane oxygenation (ECMO) service, the first of its kind in the UK, designed to deliver advanced life support to critically ill patients with cardiac arrest before they reach the hospital. The initiative, led by a specialized ECAT unit, deploys portable ECMO systems that provide on-scene heart and lung support when resuscitation fails, acting as a bridge to specialist care and marking a key advancement in UK emergency cardiovascular treatment, aligned with heart-lung machine technology.

The heart-lung machine industry in Germany is anticipated to grow considerably during the forecast period. The increasing number of CHD cases drives the growth of the market. In Germany, advancements in cardiopulmonary support technologies continue to evolve, driven by innovation in surgical devices and growing clinical demand. For instance, in January 2025, surgeons at the RHÖN-KLINIKUM Campus Bad Neustadt in Germany completed the hospital’s 100,000th open-heart operation using a heart-lung machine, marking a significant clinical milestone for the center’s cardiac surgery program. The procedure involved a patient undergoing complex heart valve surgery with the cardiopulmonary bypass system temporarily assuming the functions of the heart and lungs, enabling safe performance of the operation. Hospital leaders highlighted this achievement as evidence of both institutional expertise and the essential role of modern heart-lung machine technology in enabling life-saving cardiac procedures.

The France heart-lung machine industry is anticipated to grow significantly during the forecast period. In France, extracorporeal support technologies that build on the principles of heart‑lung machines are increasingly part of advanced cardiac care and innovation pathways. For instance, in December 2024, the ongoing application of extracorporeal membrane oxygenation (ECMO) by emergency medical teams such as SAMU in Lyon and Paris, where specialized crews now use portable ECMO systems to provide extracorporeal cardiopulmonary resuscitation (ECPR) to patients who experience refractory cardiac arrest outside the hospital. This approach circulates and oxygenates blood externally, serving as a life-saving bridge when standard resuscitation fails. The expanding use of mobile ECMO in France highlights the integration of advanced heart-lung bypass technologies into emergency cardiac and respiratory care beyond operating rooms.

Asia Pacific Heart-lung Machine Market Trends

The heart-lung machine industry in the Asia Pacific is anticipated to be the fastest-growing region, driven by the increasing adoption of advanced heart-lung support technologies, such as ECMO, in tertiary hospitals and critical care units to improve survival rates in patients with severe cardiopulmonary failure. According to the Oxford University Press article published in March 2025, clinicians at Shenzhen Guangming District People’s Hospital in China reported the successful use of veno‑arterial ECMO (VA‑ECMO) to support a 49‑year‑old man with acute myocardial infarction complicated by cardiogenic shock when conventional resuscitation and PCI were insufficient; the patient was stabilized on ECMO and recovered without long‑term sequelae, showing how ECMO can serve as a life‑saving bridge to recovery in high‑acuity cardiac emergencies.

The China heart-lung machine industry is expected to experience significant growth during the forecast period. The increasing incidence of CVD drives the market's growth. According to an article published by Beijing Renhe Information Technology Co., Ltd. in August 2025, Cardiovascular disease (CVD) poses a significant health challenge in China, affecting approximately 330 million people nationwide. This substantial prevalence highlights the increasing demand for advanced interventions, such as the heart-lung machine, to manage complex coronary conditions.

The heart-lung machine industry in Japan is expected to experience significant growth during the forecast period. The rising demand for complex cardiac surgeries and the increasing need for advanced critical care support are key drivers for heart-lung machine adoption in Japan. For instance, in March 2025, the Tokyo Medical and Dental University Hospital announced the procurement of a heart-lung machine, scheduled for delivery, demonstrating ongoing investment in essential surgical support infrastructure. Heart-lung machines are used to temporarily take over heart and lung function during complex procedures such as open-heart surgery and serve as the foundation for ECMO systems used in emergency and intensive care settings.

Latin America Heart-lung Machine Market Trends

The heart-lung machine industry in Latin America is growing during the forecast period, driven by the rising prevalence of cardiovascular disease and a steady increase in open-heart and minimally invasive cardiac procedures. Moreover, public and private healthcare spending continues to increase across the region, improving access to modern surgical equipment and replacing aging systems. In August 2025, Brazil’s healthcare market accounted for 9.7% of the country's GDP, with 63% of hospitals operating in the private sector. By mid-July 2024, BNDES had approved credit for the pharmaceutical and pharmaceutical chemical industries, marking a record increase of 16.4% in market size. Stronger distribution networks, local training programs, and partnerships between global manufacturers and regional cardiac institutes are reducing adoption barriers and improving clinical confidence. The shift toward digital monitoring, enhanced safety features, and integrated OR ecosystems is also influencing purchasing decisions, making advanced heart-lung machines the preferred choice for future-ready cardiac programs.

The Brazil heart-lung machine industry is expected to grow notably over the forecast period. Brazil’s demand for heart-lung machines is increasing as the country expands its cardiovascular care capacity and enhances access to advanced cardiac surgery within both public (SUS) and private hospital systems. The growing incidence of coronary artery disease, more referrals to tertiary cardiac centers, and growing use of minimally invasive and hybrid procedures are pushing hospitals to modernize perfusion equipment. In September 2025, Mayo Clinic Proceedings reported on iCardio, a Brazilian real-world data platform that analyzes over 375,809 cardiovascular procedures, including heart surgeries and interventional cardiology, across 558 healthcare centers. Large teaching hospitals and federally funded institutes are also scaling up programs for ECMO and pediatric cardiac surgery, creating sustained demand for systems with broader clinical capability rather than basic bypass functionality.

Middle East and Africa Heart-lung Machine Market Trends

The heart-lung machine industry inthe Middle East and Africa is growing significantly over the forecast period, driven by the increasing adoption of advanced heart-lung support technologies, such as extracorporeal membrane oxygenation (ECMO), in critical care settings. These systems temporarily take over cardiac and respiratory functions by externally circulating and oxygenating blood, enabling clinicians to manage severe, life-threatening cardiopulmonary failure more effectively. According to the Cureus article published in December 2025, in the UAE, a compelling recent case was documented when clinicians at Dubai Hospital employed veno-arterial ECMO (VA-ECMO) to successfully resuscitate a 40-year-old patient who experienced intraoperative cardiac arrest during surgery; after multiple defibrillations and conventional resuscitative efforts failed, VA-ECMO was initiated, stabilizing the patient’s circulation and enabling recovery of heart function marking one of the first reported uses of ECMO as emergent circulatory support in Dubai’s surgical critical care setting.

The Saudi Arabia heart-lung machine industry is growing considerably over the forecast period. The increasing prevalence of cardiovascular disease (CVD) in Saudi Arabia is driving demand for advanced cardiac surgical technologies, including heart-lung machines. According to a BMC Cardiovascular Diseases article published in March 2024, 1.6% of individuals aged 15 years and older in the country are affected by CVD, encompassing a range of heart conditions and related disorders. While this percentage may appear modest, it represents a significant number of patients requiring specialized cardiac care. The data underscores the importance of timely interventions, including surgical procedures such as bypass surgeries and valve repairs, which rely on heart-lung machines to maintain circulation and oxygenation during open-heart operations.

Key Heart-lung Machine Company Insights

Key participants in the market are focusing on devising innovative business growth strategies in the form of product portfolio expansions, partnerships & collaborations, mergers & acquisitions, and business footprint expansions.

Key Heart-lung Machine Companies:

The following are the leading companies in the heart-lung machine market. These companies collectively hold the largest market share and dictate industry trends.

- Medtronic

- Terumo Corporation

- LivaNova PLC

- Getinge AB

- Braille Biomedical

- Nipro Corporation do Brasil (NIPRO)

- Surge Cardiovascular

- EUROSETS

- Technowood America Corporation

- Fresenius Medical Care

- MERA (Senko Medical Instrument Mfg. Co., Ltd.)

Recent Developments

-

In April 2025, Eurosets announced the launch of Xtreme Rescue, a lightweight and highly portable extracorporeal cardiopulmonary support device, unveiled at the EuroELSO congress to enable rapid ECMO support in emergency and hard-to-reach settings.

-

In September 2024, Medtronic launched VitalFlow, a configurable, single-platform ECMO system that bridges bedside care and intra-hospital transport with a strong focus on simplicity and performance. The launch expands Medtronic’s cardiac surgery portfolio by integrating MC3 technology to deliver portable, user-friendly, and reliable ECMO support.

-

In December 2023, BTC Health, through its wholly owned subsidiary BTC Cardio, entered into an exclusive sales and distribution agreement with Eurosets for its cardiopulmonary bypass and extracorporeal life support product portfolio across Australia and New Zealand.

Heart-Lung Machine Market Report Scope

Report Attribute

Details

Market size in 2025

USD 2.2 billion

Estimated market size in 2026

USD 2.4 billion

Projected market size by 2033

USD 3.7 billion

Growth rate

CAGR of 6.4% from 2026 to 2033

Actual data

2021 - 2024

Forecast data

2026 - 20303

Quantitative units

Revenue in USD million/billion, Unit Volume, in ‘000 Units, and CAGR from 2026 to 2033

Report coverage

Revenue & Volume forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East and Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; Spain; Italy; France; Norway; Denmark; Sweden; Japan; China; India; Australia; Thailand; South Korea; Brazil; Chile; Colombia; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

Medtronic; Terumo Corporation; LivaNova PLC; Getinge AB; Braille Biomedical; Nipro Corporation do Brasil (NIPRO); Surge Cardiovascular; EUROSETS; Technowood America Corporation; Fresenius Medical Care; MERA (Senko Medical Instrument Mfg. Co., Ltd.)

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Heart-Lung Machine Market Report Segmentation

This report forecasts revenue and volume growth at global, regional, and country levels and analyzes industry trends in each sub-segments from 2021 to 2033. For this study, Grand View Research, Inc. has segmented the global heart-lung machine market report based on product, application, end use, and region:

-

Product Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Capital Equipment

-

Pumps

-

Heater-Cooler Units / Heat Exchange Systems

-

Monitoring Systems

-

Others

-

-

Consumables

-

Cannulas

-

By Product

-

Arterial Cannulas

-

Venous Cannulas

-

Cardioplegia Cannulas

-

Vent Cannulas

-

ECMO Cannulas

-

-

By Age Group

-

Adult

-

Pediatric

-

-

-

Oxygenators

-

By Product

-

Membrane Oxygenators

-

ECMO Oxygenators

-

Pediatric/Neonatal Oxygenators

-

Other Oxygenators

-

-

By Age Group

-

Adult

-

Pediatric

-

-

-

Blood Reservoirs & Filtration Systems

-

Tubing Sets & Circuits

-

Accessories & Consumables

-

-

-

Application Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Coronary Artery Bypass Grafting (CABG)

-

Heart Valve Surgeries

-

Heart Transplant

-

Lung Transplant

-

Others

-

-

End Use Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Public Healthcare Institutions

-

Private Healthcare Institutions

-

-

Regional Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

Spain

-

Italy

-

France

-

Denmark

-

Norway

-

Sweden

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

Thailand

-

South Korea

-

-

Latin America

-

Brazil

-

Chile

-

Colombia

-

Argentina

-

-

Middle East and Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

Some key players operating in the heart-lung machine market include Medtronic, Terumo Europe NV, LivaNova, Inc., Getinge, Braile Biomédica, NIPRO, Tianjin Welcome Medical Equipment Co., Ltd., ELITE LIFECARE, Hemovent GmbH, MERA (Senko Medical Instrument Mfg. Co., Ltd.), Technowood International Pte. Ltd.

Key factors include increasing demand for cardiac surgeries and continuous technological advancements in the cardiopulmonary bypass machine.

Asia Pacific is the fastest-growing region over the forecast period

The consumables segment led with a 68.24% revenue share in 2025.

The coronary artery bypass grafting segment led with a 54.5% revenue share in 2025, while heart valve surgeries is the fastest-growing segment.

The public healthcare institutions segment led with a 55.38% revenue share in 2025, while private healthcare institutions is the fastest-growing segment.

The global heart-lung machine market size was estimated at USD 2.2 billion in 2025 and is expected to reach USD 2.4 billion in 2026.

The global heart-lung machine market is expected to grow at a compound annual growth rate of 6.4% from 2026 to 2033 to reach USD 3.7 billion by 2033.

North America dominated with a 52.06% revenue share in 2025.

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.