- Home

- »

- Advanced Interior Materials

- »

-

Heat Pump Compressor Market Size & Share Report, 2033GVR Report cover

![Heat Pump Compressor Market Size, Share & Trends Report]()

Heat Pump Compressor Market (2026 - 2033) Size, Share & Trends Analysis Report By Technology (Fixed-Speed Compressors, Variable-Speed / Inverter Compressors) By Capacity, By End Use, By Compressor, By Product, By Region And Segment Forecasts

Market Size, 2025

$32.1BMarket Estimate, 2026

$35.2BMarket Forecast, 2033

$71.1BCAGR, 2026–2033

10.6%Heat Pump Compressor Market Summary

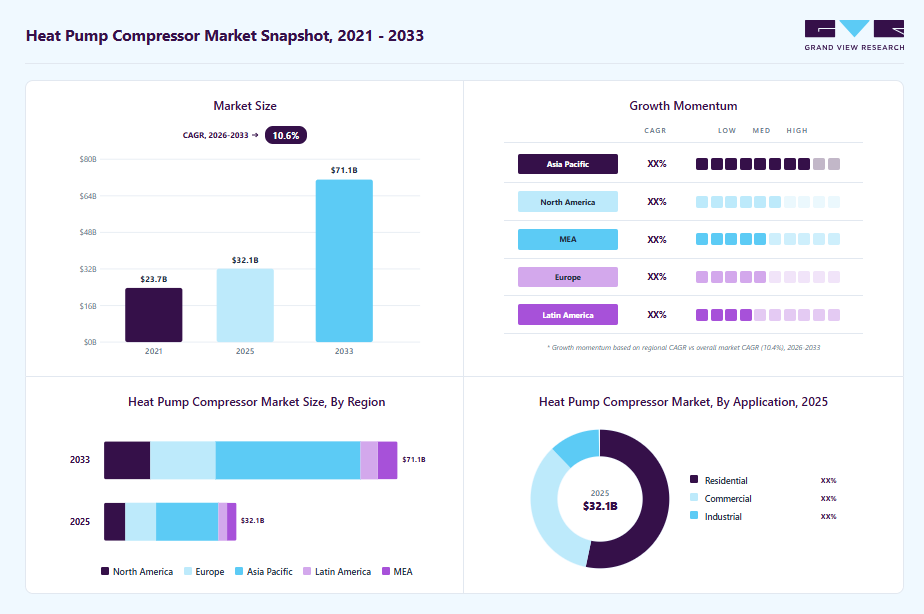

The global heat pump compressor market size was valued at USD 32.1 billion in 2025 and is projected to grow from USD 35.2 billion in 2026 to USD 71.1 billion by 2033, at a CAGR of 10.6% from 2026 to 2033. Asia Pacific dominated the heat pump compressor market with the largest revenue share of 47.0% in 2025. Policy support and climate targets are accelerating market growth.

Key Market Trends & Insights

- By technology: Fixed-speed compressors segment led the market in 2025, accounting for 61.3% of the global revenue.

- By end use: residential segment is expected to be the fastest-growing segment with a CAGR of 11.0% over the forecast period.

- By Compressor: compressors held the majority market share in 2025, holding 44.3% of the global heat pump compressor market.

- By Product: Air-source heat pump compressors accounted for the dominant product segment in 2025, with approximately 84.9% of total market revenue.

- By Capacity: Below 20 kW represented the largest portion of the market in 2025, accounting for approximately 41.8% of total revenue.

Regional Highlights

- Largest regional market: Asia Pacific (47.0% revenue share, 2025)

- The heat pump compressor industry in China is a major market, supported by large-scale construction activity and the growing adoption of energy-efficient heating and cooling technologies.

Market Size & Forecast

- Market size in 2025: USD 32.1 Billion

- Estimated market size in 2026: USD 35.2 Billion

- Projected market size by 2033: USD 71.1 Billion

- CAGR (2026-2033): 10.6%

Several countries have introduced incentives, subsidies, and regulatory frameworks encouraging the deployment of heat pump systems in both new buildings and retrofit applications. As these initiatives continue to expand, manufacturers are increasing production of heat pump components, including compressors designed for high efficiency and compatibility with low-global-warming-potential refrigerants.")

Continuous innovation in compressor technologies is supporting the growth of the heat pump compressor market. Manufacturers are introducing advanced compressor designs such as scroll, rotary, and inverter-driven compressors that offer improved efficiency, reduced noise levels, and enhanced durability. These innovations enable heat pump systems to operate efficiently across a wider range of temperature conditions, including colder climates where heat pump performance has traditionally been limited.

Market Concentration & Characteristics

The heat pump compressor industry is concentrated, with a mix of large multinational HVAC component manufacturers and specialized compressor suppliers. Major companies such as Danfoss, Copeland, BITZER, Mitsubishi Electric, and Daikin account for a significant share of the market due to their extensive product portfolios, established manufacturing capabilities, and global distribution networks. At the same time, several regional manufacturers, particularly in Asia, supply compressors for residential heat pumps and air-conditioning systems. The competitive landscape is characterized by continuous investment in product development, strategic partnerships, and expansion of manufacturing capacity to address the growing demand for heat pump systems.

Technological advancements are playing a significant role in shaping the market, with market players emphasizing improving compressor efficiency and compatibility with environmentally friendly refrigerants. Variable-speed and inverter-driven compressors are expected to grow in demand as they enhance system performance and reduce energy consumption in heat pump applications. Moreover, regulatory policies aimed at reducing greenhouse gas emissions and promoting energy-efficient heating technologies are promoting the installation of heat pumps across residential, commercial, and industrial sectors. These regulations are also driving the development of compressors designed to operate with low-global-warming-potential refrigerants such as CO₂, propane, and other natural refrigerants.

The availability of alternative heating technologies represents a potential substitute threat for heat pump systems in certain markets. Conventional heating solutions such as gas boilers, electric resistance heaters, and district heating systems continue to be used in many regions due to their established infrastructure and lower upfront costs. However, increasing emphasis on energy efficiency and decarbonization is gradually shifting demand toward heat pump technologies. In terms of end-use distribution, the residential sector accounts for a major share of the heat pump compressor market due to the widespread adoption of heat pumps for space heating and cooling in homes. The commercial sector also contributes significantly, while industrial applications are emerging as a growing segment as industries adopt heat pump systems for waste heat recovery and process heating.

Drivers, Opportunities & Restraints

The growth of the construction industry and increasing demand for energy-efficient HVAC systems are supporting the adoption of heat pumps across residential and commercial buildings. As new buildings incorporate advanced heating and cooling solutions to improve energy performance, heat pump installations are increasing, thereby driving demand for compressors used in these systems. In addition, global decarbonization efforts are encouraging the transition from fossil-fuel-based heating systems to electric heat pumps, further supporting the demand for heat pump compressors.

The growth of emerging economies presents significant opportunities for the heat pump compressor market. Rapid urbanization, expanding construction activity, and increasing demand for modern heating and cooling systems are driving the adoption of advanced HVAC technologies in countries across Asia, Latin America, and parts of the Middle East. As governments and private developers invest in residential and commercial infrastructure, demand for energy-efficient climate control systems such as heat pumps is expected to increase. This trend is likely to support the growing demand for compressors used in heat pump systems across emerging markets.

Performance limitations of heat pumps in extremely cold climates can act as a restraint for the market. In regions with very low ambient temperatures, conventional air-source heat pumps may experience reduced efficiency, requiring supplemental heating systems to maintain indoor comfort levels. Although technological advancements have improved cold-climate heat pump performance, concerns regarding heating capacity and system reliability in harsh weather conditions may still limit adoption in certain regions, thereby affecting demand for heat pump compressors.

Technology Insights

The fixed-speed compressors segment accounted for the largest share of the market in 2025, representing approximately 61.3% of total revenue. Their continued adoption is supported by their simple design, lower manufacturing costs, and widespread use in conventional residential heat pump systems. Fixed-speed compressors are commonly used in standard heating and cooling applications where constant operating loads are sufficient. Their reliability, ease of maintenance, and cost advantages make them a preferred choice in cost-sensitive markets and entry-level heat pump installations.

The variable-speed (inverter) compressor segment is expected to grow significantly during the forecast period, with a CAGR of approximately 10.1%. Demand for inverter-driven compressors is increasing as heat pump manufacturers focus on improving system efficiency and energy performance. These compressors allow the system to adjust operating speeds according to heating or cooling requirements, resulting in lower energy consumption and improved temperature stability. Growing regulatory emphasis on energy-efficient HVAC technologies and the increasing adoption of advanced heat pump systems are further supporting the expansion of variable-speed compressor technologies.

Capacity Insights

Compressors with capacities below 20 kW represented the largest portion of the market in 2025, accounting for approximately 41.8% of total revenue. Their strong market presence is primarily supported by widespread use in residential heat pump systems and small commercial HVAC installations. These compressors are commonly deployed in air-source heat pumps used for space heating and cooling in homes and small buildings. Growing residential construction activity and increasing adoption of energy-efficient heating technologies are continuing to support demand for lower-capacity heat pump compressors.

The 20–100 kW capacity segment is projected to expand at the fastest pace during the forecast period, registering a CAGR of 11.5%. Compressors in this range are widely used in medium-sized commercial buildings, district heating substations, and larger residential complexes where higher heating and cooling capacities are required. The increasing adoption of heat pumps in commercial facilities such as offices, hotels, and educational institutions is driving demand for compressors in this capacity range. In addition, expanding investments in energy-efficient commercial HVAC systems are further supporting the growth of this segment.

End Use Insights

Residential applications account for the majority of heat pump compressor end users, with a global revenue share of 53.4% of total revenue. Demand from this segment is supported by the increasing adoption of heat pumps for space heating and cooling in residential buildings. Growing residential construction activity and the replacement of conventional heating systems with heat pump solutions are contributing to higher installations of residential heat pump units. In addition, government incentives and building energy efficiency regulations in several countries are encouraging homeowners to adopt heat pump technologies, thereby sustaining demand for compressors used in residential systems.

The commercial segment is expected to grow at a CAGR of 10.6% during the forecast period. Increasing adoption of energy-efficient HVAC systems in commercial facilities such as offices, hotels, hospitals, and educational institutions is supporting demand for heat pump compressors. Heat pump systems provide efficient heating and cooling while helping commercial buildings reduce energy consumption and operational emissions. Rising investments in sustainable building infrastructure and stricter energy efficiency standards for commercial properties are further contributing to the growth of this segment.

Compressor Insights

Scroll compressors captured the largest share of the market in 2025, accounting for approximately 44.3% of total revenue. Their strong adoption is supported by their high efficiency, compact design, and reliable performance in heat pump systems. Scroll compressors are widely used in residential and light commercial heat pumps due to their ability to provide smooth and quiet operation with fewer moving parts compared to other compressors. Their compatibility with inverter technology and ability to operate efficiently across varying load conditions have further strengthened their position in modern heat pump installations.

The screw compressors segment is anticipated to record one of the highest growth rates during the forecast period, with a projected CAGR of 10.6%. These compressors are commonly used in large commercial and industrial heat pump systems that require higher capacities and continuous operation. Their ability to deliver stable performance under high load conditions and support high-temperature heat pump applications makes them suitable for district heating networks and industrial process heating. Increasing investments in industrial heat pumps and large-scale energy recovery systems are further supporting the expansion of the screw compressor segment.

Product Insights

Air-source heat pump compressors accounted for the dominant product segment in 2025, with approximately 84.9% of total market revenue. Their strong market presence is supported by the widespread adoption of air-source heat pump systems in residential and commercial buildings. These systems are widely used due to their lower installation costs, simpler design, and ability to operate efficiently across a wide range of climates. Increasing deployment of air-source heat pumps as part of building electrification initiatives and energy-efficient HVAC upgrades continues to support demand for compressors used in these systems.

Geothermal heat pump compressors are projected to grow at the fastest rate during the forecast period, registering a CAGR of 11.9%. Growth in this segment is driven by the increasing adoption of ground-source heat pump systems, which offer higher energy efficiency and stable performance due to consistent underground temperatures. These systems are gaining traction in commercial buildings, large residential developments, and institutional facilities seeking long-term energy savings and reduced operating emissions. Rising investments in sustainable building infrastructure and renewable heating technologies are further supporting the expansion of geothermal heat pump systems and the compressors used in them.

Regional Insights

The Asia Pacific heat pump compressor industry led the global revenue share accounting for 47.0% of the market revenue in 2025. The region’s market is rapidly expanding, driven by urbanization, rising construction activity, and growing demand for energy-efficient HVAC systems. Countries such as China, Japan, and South Korea are witnessing increasing adoption of heat pump technologies across residential and commercial sectors. In addition, government initiatives promoting the electrification of heating and improvements in building energy efficiency are encouraging the deployment of heat pump systems. The presence of major compressor manufacturers and expanding production capacities across the region further support market growth.

The heat pump compressor industry in China is a major market, supported by large-scale construction activity and the growing adoption of energy-efficient heating and cooling technologies. Government initiatives promoting the electrification of heating and improvements in building energy efficiency are encouraging the deployment of heat pump systems across residential, commercial, and industrial sectors. In addition, the presence of large HVAC manufacturers and compressor suppliers in the country further supports market growth.

The Japan heat pump compressor industry represents a notable market due to the widespread adoption of heat pump technologies across residential and commercial sectors. Strong government support for energy efficiency and the modernization of building infrastructure continues to encourage the installation of advanced HVAC systems. In addition, the presence of major compressor and HVAC manufacturers in the country further supports the development and adoption of heat pump compressor technologies.

North America Heat Pump Compressor Market Trends

The heat pump compressor industry in North America represents a significant market, supported by increasing adoption of heat pumps across a growing construction sector, particularly residential and commercial construction. Government incentives, tax credits, and decarbonization policies aimed at reducing reliance on fossil-fuel-based heating systems are encouraging the installation of heat pumps in the region. The presence of established HVAC manufacturers, along with growing investments in energy-efficient building technologies, is further supporting demand for heat pump compressors.

U.S.Heat Pump Compressor Market Trends

The U.S. heat pump compressor industry is supported by the increasing adoption of heat pumps across residential and commercial buildings as part of broader electrification and energy efficiency initiatives. Government incentives and policy measures encouraging the transition from fossil-fuel-based heating systems to electric heat pumps are driving installations across the country. Growing construction activity and the replacement of aging HVAC systems with energy-efficient alternatives are further supporting the demand for heat pump compressors in the U.S. market.

Europe Heat Pump Compressor Market Trends

The heat pump compressor industry in Europe is a key market due to strong regulatory support for energy efficiency and the transition toward low-carbon heating technologies. Several countries across the region have introduced policies and financial incentives to accelerate the adoption of heat pumps as part of broader climate and energy transition strategies. The increasing phase-out of fossil-fuel-based heating systems, combined with high energy prices and growing environmental awareness, has further supported the deployment of heat pumps. These factors continue to drive demand for advanced compressor technologies used in residential, commercial, and district heating applications.

The UK heat pump compressor industry is driven by national decarbonization targets and policies aimed at reducing emissions from residential heating systems. Government programs promoting the adoption of low-carbon heating technologies, including heat pumps, are encouraging the replacement of conventional gas boilers. Increasing investments in energy-efficient buildings and the expansion of heat pump installations across residential and commercial sectors are supporting the demand for compressors used in heat pump systems.

The heat pump compressor industry in Germany represents a key market in Europe due to strong policy support for energy-efficient heating technologies and building decarbonization. The country has been actively promoting the installation of heat pumps as part of its energy transition strategy aimed at reducing reliance on fossil fuels. Increasing construction of energy-efficient buildings and the modernization of heating infrastructure are contributing to the growing adoption of heat pump systems, thereby supporting the demand for compressors used in these applications.

Latin America Heat Pump Compressor Market Trends

The heat pump compressor industry in Latin America is gradually developing, supported by growing demand for modern heating and cooling technologies in residential and commercial buildings. Increasing urbanization and improvements in building infrastructure are encouraging the adoption of energy-efficient HVAC systems in several countries across the region. Although the use of heat pumps remains limited compared to more mature markets, rising awareness of energy efficiency and gradual investments in sustainable building solutions are supporting the demand for heat pump compressors.

The Brazil heat pump compressor industry represents an emerging market in Latin America, supported by growing construction activity and increasing adoption of modern HVAC technologies in commercial and residential buildings. Rising awareness of energy-efficient climate control systems and gradual improvements in building infrastructure are contributing to the deployment of heat pump systems. As the adoption of energy-efficient heating and cooling technologies expands, demand for compressors used in heat pump applications is expected to grow.

Middle East & Africa Heat Pump Compressor Market Trends

The heat pump compressor industry in the Middle East & Africa represents an emerging market, with demand primarily driven by commercial building development and expanding HVAC infrastructure. Increasing investments in construction, tourism, and commercial real estate are contributing to the adoption of advanced climate control systems across the region. In addition, growing interest in energy-efficient cooling and heating solutions, particularly in large commercial facilities and institutional buildings, is supporting the deployment of heat pump systems and the compressors used in them.

The Saudi Arabia heat pump compressor industry represents a developing market for heat pump compressors in the Middle East, supported by increasing investments in construction and commercial infrastructure. The country’s expanding hospitality, residential, and commercial building sectors are driving demand for advanced HVAC systems to maintain indoor climate control. In addition, growing focus on energy efficiency and sustainable building technologies is encouraging the adoption of modern heat pump systems, thereby supporting demand for compressors used in these systems.

Key Heat Pump Compressor Company Insights

Some of the key players operating in the market include Mitsubishi Electric Corporation and Danfoss, among others.

-

Mitsubishi Electric Corporation is a global manufacturer of electrical and electronic equipment headquartered in Tokyo, Japan, with a strong global presence and manufacturing facilities across Asia, Europe, and North America. The company operates across several business segments, including HVAC systems, industrial automation, power systems, and electronic devices. Mitsubishi Electric is a major supplier of heating, ventilation, and air conditioning technologies, including heat pump systems used in residential and commercial buildings. Moreover, the company develops advanced compressor technologies and inverter-driven systems designed to improve energy efficiency and performance in heat pump and air conditioning applications.

-

Danfoss is a multinational engineering company specializing in energy-efficient technologies for heating, cooling, industrial automation, and power systems. The company operates through several business segments, including Danfoss Climate Solutions, which focuses on refrigeration, air conditioning, and heat pump components. Danfoss develops a wide range of compressors, controls, and system components used in heat pump and HVAC applications.

Key Heat Pump Compressor Companies:

The following key companies have been profiled for this study on the heat pump compressor market.

- GMCC (Midea)

- Mitsubishi Electric Corporation

- Dorin S.p.A.

- Danfoss

- Copeland LP

- BITZER

- FRASCOLD SPA

- Boyard Compressor Co.,LTD

- ebm-papst

- Panasonic Industry

- Sabroe

- FRIOTHERM AG

- Glen Refrigeration

- GEA Group Aktiengesellschaft

- DAIKIN INDUSTRIES, LTD

Recent Developments

-

In July 2024, Danfoss launched a new range of compressors designed for comfort and industrial heat pump applications. The lineup includes the BOCK HGX56 CO₂ T semi-hermetic reciprocating compressor, the PSH scroll compressor, and the VZN inverter scroll compressor. These compressors support natural and low-global-warming-potential (GWP) refrigerants and are intended to improve energy efficiency and reduce emissions in heating systems.

-

In December 2025, Daikin Industries and Copeland announced the expansion of their existing joint venture into the European market to support the growing demand for residential heat pumps. The collaboration will introduce advanced inverter swing rotary compressors, along with power electronics and control technologies specifically designed for European heat pump systems.

Heat Pump Compressor Market Report Scope

Report Attribute

Details

Market size in 2025

USD 32.1 billion

Estimated Market size in 2026

USD 35.2 billion

Projected Market size by 2033

USD 71.1 billion

Growth rate

CAGR of 10.6% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company market position analysis, competitive landscape, growth factors, and trends

Segments covered

Technology, capacity, end use, compressor, product, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country Scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; China; India; Japan; South Korea; Australia; Brazil;

Argentina; South Africa; Saudi Arabia; UAE

Key companies profiled

GMCC (Midea); Mitsubishi Electric Corporation; Dorin S.p.A.; Danfoss; Copeland LP; BITZER; FRASCOLD SPA; Boyard Compressor Co., LTD; ebm-papst; Panasonic Industry; Sabroe; FRIOTHERM AG; Glen Refrigeration; GEA Group Aktiengesellschaft; DAIKIN INDUSTRIES, LTD.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Heat Pump Compressor Market Report Segmentation

This report forecasts revenue growth at global, regional & country levels and provides an analysis on the industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global heat pump compressor market report on the basis of technology, capacity, end use, compressor, product, and region:

-

Technology Outlook (Revenue, USD Billion, 2021 - 2033)

-

Fixed-Speed Compressors

-

Variable-Speed / Inverter Compressors

-

-

Capacity Outlook (Revenue, USD Billion, 2021 - 2033)

-

Below 20 kW

-

20 - 100 kW

-

100 - 200 kW

-

Above 200 kW

-

-

End Use (Revenue, USD Billion, 2021 - 2033)

-

Residential

-

Commercial

-

Industrial

-

-

Compressor (Revenue, USD Billion, 2021 - 2033)

-

Scroll Compressors

-

Rotary Compressors

-

Screw Compressors

-

Centrifugal Compressors

-

-

Product Outlook (Revenue, USD Billion, 2021 - 2033)

-

Air Source

-

Water Source

-

Geothermal

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

-

Frequently Asked Questions About This Report

The global heat pump compressor market size was estimated at USD 32.1 billion in 2025 and is expected to reach USD 35.2 billion in 2026

The global heat pump compressor market, in terms of revenue, is expected to grow at a compound annual growth rate of 10.6% from 2026 to 2033 to reach USD 71.1 billion by 2030

The Asia Pacific heat pump compressor market dominated the global revenue share in 2025 accounting for 47.0% of the share, driven by rapid urbanization, expanding construction activity, increasing adoption of energy-efficient HVAC systems, and supportive government initiatives.

Some of the key players operating in the heat pump compressor market GMCC (Midea), Mitsubishi Electric Corporation, Dorin S.p.A., Danfoss, Copeland LP, BITZER, FRASCOLD SPA, Boyard Compressor Co., LTD, ebm-papst, Panasonic Industry, Sabroe, FRIOTHERM AG, Glen Refrigeration, GEA Group Aktiengesellschaft, and DAIKIN INDUSTRIES, LTD.

The heat pump compressor market is driven by the growing adoption of heat pumps for energy-efficient heating and cooling, increasing building electrification initiatives, rising construction activity, and government policies promoting decarbonization and low-carbon heating technologies.

The fixed-speed compressors segment led with a 61.3% revenue share in 2025, while variable-speed (inverter) compressor is expected to grow significantly during the forecast period, with a CAGR of approximately 10.1%.

Compressors with capacities below 20 kW segment held the largest revenue share in 2025, while the 20–100 kW capacity segment is expected to register the fastest CAGR.

Residential segment held the largest share in 2025, while the commercial segment is expected to grow at a CAGR of 10.6% during the forecast period.

Scroll compressors captured the largest share of the market in 2025, while the screw compressors segment is projected to grow at a CAGR of 10.6%.

Air-source heat pump compressors accounted for the dominant product segment in 2025, while the geothermal heat pump compressors are projected to grow at the fastest rate during the forecast period, registering a CAGR of 11.9%.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.