- Home

- »

- Clinical Diagnostics

- »

-

Liquid Biopsy Market Size And Share Report, 2026-2033GVR Report cover

![Liquid Biopsy Market (2026 - 2033)Report]()

Liquid Biopsy Market (2026 - 2033)

Size, Share & Trends Analysis Report By Biomarker (Exosomes, Circulating Nucleic Acids, CTC), By Technology, By Sample Type, By Application, By Clinical Application, By End Use, By Product, By Region, And Segment Forecasts

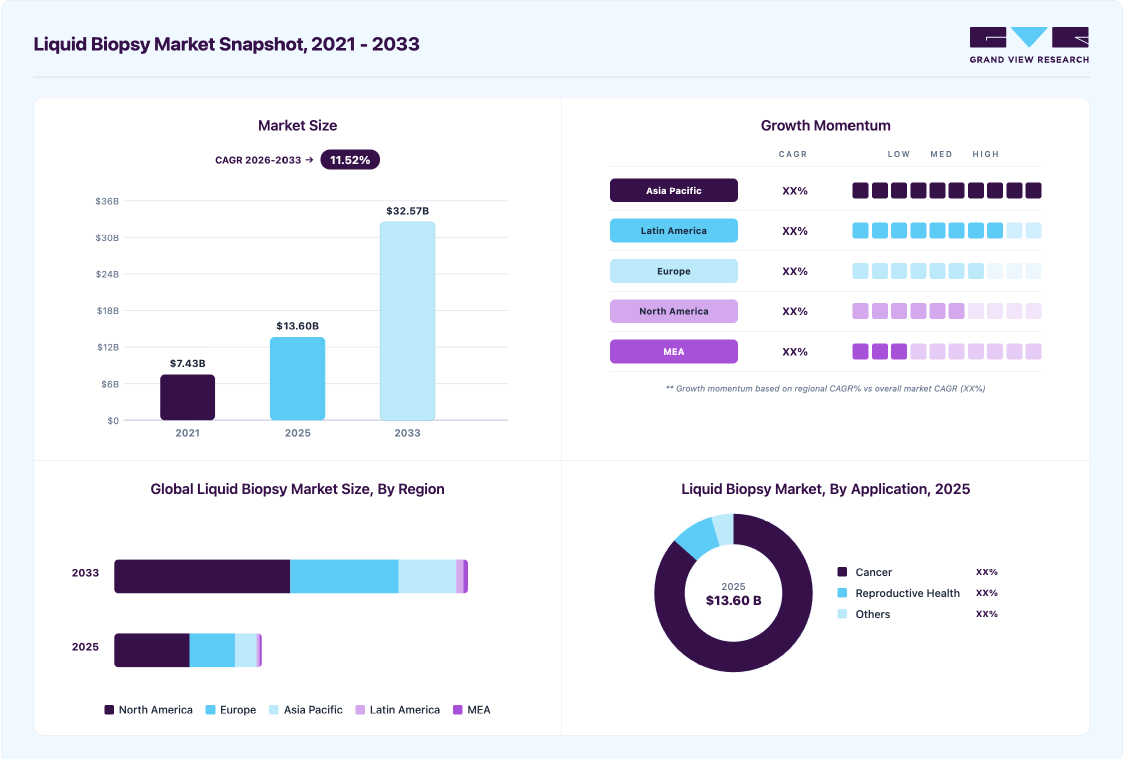

Market Size, 2025

$13.6BMarket Estimate, 2026

$16.2BMarket Forecast, 2033

$32.6BCAGR, 2026–2033

11.5%Liquid Biopsy Market Summary

The global liquid biopsy market size was estimated at USD 13.6 billion in 2025 and is projected to grow from USD 15.2 billion in 2026 to USD 32.6 billion by 2033, growing at a CAGR of 11.5% from 2026 to 2033. North America dominated the Liquid Biopsy Market with the largest revenue share of 51.0% in 2025. The industry is witnessing growth due to factors such as the growing prevalence of cancer, technological advancements in cancer diagnostics, and rising preference for minimally invasive cancer diagnostics.

Key Market Trends & Insights

- By technology: Multi-gene-parallel analysis (NGS) segment held the largest market share of 76.7% in 2025.

- By biomarker: Circulating nucleic acids segment held the largest market share of 35.4% in 2025.

- By application: Cancer application segment held the largest market share of 86.5% in 2025.

- By product: Instruments segment held the largest market share of 47.1% in 2025.

Regional Highlights

- Largest regional market: North America (51.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 13.6 Billion

- Estimated market size in 2026: USD 16.2 Billion

- Projected market size by 2033: USD 32.6 Billion

- CAGR (2026-2033): 11.5%

")

Moreover, ongoing research for the development of liquid biopsy assays and tests, aided by the rising adoption and development of multi-cancer early detection tests, is providing a major opportunity for the growth of the overall market. Liquid biopsy is an advanced testing technology for the detection of genetic alterations related tumor. It has also been utilized to stratify tumors and deliver precise cancer treatment. For instance, in January 2023, Guardant Health received FDA approval for Guardant360 CDx, its liquid biopsy assay as companion diagnostics for ESR1 mutant breast cancer diagnosis. These recent innovations, advancements, and expansions in the industry promoting the use of liquid biopsy are driving the market.

For various applications, such as breast, colorectal, ovarian cancer, non-small-cell lung, and prostate cancer, liquid biopsy is used for diagnostic & screening, making it an important tool. After various studies and speculations, it has been determined that the liquid biopsy technique may provide an improved diagnosis outcome. Data show that screening techniques should be used on high-risk patients who have an ancestral history of cancer. Moreover, over the past several years, studies have shown positive outcomes of liquid biopsy platforms. The government and various regulatory bodies have also shown interest in the area by promoting multiple breakthrough devices for the rapid development of the technology.

Furthermore, Multi Cancer Early Detection (MCED) provides major opportunities for the growth of the liquid biopsy market. The MCED market represents an emerging field of interest for the diagnostics industry, which not only enables early detection of cancer but also facilitates early treatment of these patients by saving time and minimizing the risk of requiring invasive medical procedures. There are several limitations to single cancer tests, including high false-positive rates and reduced sensitivity. In addition, diagnosis is usually conducted with a focus on just one type of cancer; hence, other cancers are left undiagnosed. Hence, these single cancer detection tests are failing to meet the changing needs of the consumers. Thus, opportunities presented by these MCED tests are significant.

Liquid biopsies are progressively being studied as a tool that can determine tumor evolution and guide systemic treatment. According to a study by ASCO, it is insufficient to prove the clinical utility for most of the ctDNAs in advanced-stage cancers and early-stage disease screening. For ctDNA and CTC, there is a requirement to regulate preanalytical variables for cross-platform comparison studies. However, to address these challenges, initiatives are being undertaken in the U.S and Europe. A low concentration of ctDNA and CTCs in biological samples is expected to limit the use of liquid biopsy in early-stage cancer diagnosis. Moreover, increasing ctDNA or CTC volume by drawing a large amount of blood from the patients is not clinically advisable. Such challenges in early-stage diagnosis are expected to restrain growth to a certain extent.

Market Dynamics

The liquid biopsy market is witnessing growth driven by the increasing global burden of cancer, rising adoption of precision oncology, and growing demand for minimally invasive diagnostic solutions. Healthcare providers are increasingly incorporating liquid biopsy technologies into clinical practice for early cancer detection, therapy selection, disease monitoring, and treatment response assessment. Technological advancements in next generation sequencing and circulating tumor DNA analysis are enhancing analytical performance and broadening the clinical utility of liquid biopsy across oncology applications. Furthermore, expanding interest in multi-cancer early detection and minimal residual disease testing is supporting market adoption. A recent industry development reflects this trend. For instance, in April 2025, Guardant Health announced a strategic collaboration with Pfizer to support the development and commercialization of oncology therapies through its Guardant Infinity liquid biopsy platform, reinforcing the growing role of liquid biopsy technologies in precision medicine and clinical research. However, reimbursement limitations, clinical validation requirements, and evolving regulatory frameworks continue to influence adoption across healthcare systems.

The increasing adoption of precision oncology is driving demand for liquid biopsy solutions across the cancer care continuum. Healthcare providers are placing greater emphasis on biomarker guided treatment selection to improve therapeutic outcomes and support personalized treatment approaches. Liquid biopsy technologies enable non-invasive detection of genomic alterations, allowing clinicians to monitor disease progression, evaluate treatment response, and identify actionable mutations throughout the course of therapy. The growing integration of genomic testing into oncology workflows, combined with advancements in next generation sequencing and circulating tumor DNA analysis, is further supporting market expansion. In addition, pharmaceutical companies are increasingly incorporating liquid biopsy platforms into clinical development programs to facilitate patient stratification and companion diagnostic development. This trend is reinforcing the commercial adoption of liquid biopsy technologies across oncology applications. For instance, in January 2026, Guardant Health entered a multi-year collaboration with Merck to develop companion diagnostics for oncology therapies, reflecting the increasing importance of liquid biopsy in precision medicine and targeted drug development.

Stringent clinical validation requirements and reimbursement limitations continue to constrain broader adoption of liquid biopsy technologies. Regulatory authorities and healthcare payers require substantial clinical evidence demonstrating analytical validity, clinical utility, and economic value before supporting widespread commercialization and reimbursement coverage. The generation of such evidence often requires extensive clinical studies, increasing development costs and extending product commercialization timelines. In addition, reimbursement policies remain inconsistent across healthcare systems, creating challenges for diagnostic providers seeking broader market penetration. These factors are particularly relevant for emerging applications such as multi cancer early detection, where long term clinical outcome data are still being established. Limited reimbursement coverage can also affect physician adoption and patient access to advanced liquid biopsy testing. For instance, in September 2025, ClearNote Health received UKCA approval for its Avantect cancer detection tests, highlighting the extensive regulatory review and validation processes required to bring innovative liquid biopsy solutions to the market.

The growing focus on early cancer detection is creating substantial opportunities for the liquid biopsy market. Healthcare systems are increasingly prioritizing screening initiatives aimed at identifying cancer at earlier stages when treatment outcomes are generally more favorable. Liquid biopsy-based screening approaches offer a convenient and minimally invasive alternative to conventional diagnostic procedures, supporting broader patient participation in cancer detection programs. Advancements in biomarker discovery, genomic profiling, and artificial intelligence driven data analysis are further enhancing the performance and clinical applicability of multi-cancer early detection tests. As healthcare providers seek scalable solutions for population level cancer screening, demand for blood based diagnostic technologies is expected to increase. In addition, ongoing investments in product development and commercialization activities are accelerating market growth. For instance, in September 2025, Exact Sciences launched Cancerguard, a multi cancer early detection blood test designed to identify more than 50 cancer types, demonstrating the expanding role of liquid biopsy technologies in cancer screening and early diagnosis.

Market Concentration & Characteristics

The liquid biopsy industry exhibits high innovation, driven by advanced technologies such as ctDNA and exosome analysis. New diagnostic platforms, such as NGS-based tests, are improving cancer detection and monitoring. Companies like Guardant Health and Foundation Medicine are leading in innovation, enhancing test sensitivity and specificity, which is crucial for early cancer intervention and personalized treatment.

Mergers and acquisitions are robust in the liquid biopsy space, aimed at enhancing technological capabilities and market reach. For instance, Illumina’s acquisition of GRAIL in 2021 sought to integrate early cancer detection tools into mainstream diagnostics. Such activities accelerate product commercialization, facilitate regulatory navigation, and allow access to wider patient populations, strengthening competitive positions.

Regulations significantly shape the market, ensuring test accuracy and safety. Agencies such as the FDA and EMA are increasingly involved, particularly in approving companion diagnostics. The FDA’s 2020 guidance on liquid biopsy for minimal residual disease detection marked a pivotal step, fostering trust but also necessitating rigorous clinical validation, which can slow down market entry for newer players.

Companies are diversifying their offerings to cover more cancer types and stages. From non-small cell lung cancer to colorectal and breast cancer, tests are becoming tumor-agnostic. Examples include Guardant360 and Signatera expanding indications across solid tumors. This broadening of applications drives demand, especially in recurrence monitoring and therapy selection, aiding long-term market sustainability.

North America leads in adoption due to strong R&D and reimbursement infrastructure. However, the Asia Pacific is emerging fast, driven by rising cancer incidence and growing healthcare investments. Firms are partnering locally to meet regulatory norms and cost sensitivities. For example, Chinese firms are developing cost-effective assays, widening access, and boosting the market’s global footprint.

Technology Insights

Based on technology, the multi-gene-parallel analysis (NGS) segment led the market with the largest revenue share of 76.7% in 2025 and anticipated to grow at the fastest CAGR over the forecast period.. NGS technology allows the detection of various tumor-causing mutations and the identification of potential emergence of post-treatment resistance mechanisms from pre-existing clones. Rapid developments in NGS technology have led to significant cost reductions in sequencing with high accuracy. Furthermore, key players operating in the market are focusing on developing innovative products to meet the growing demand for diagnosis and maintain their position with an expanded product portfolio, thus driving the market. For instance, in January 2023, Agilent Technologies collaborated with Quest Diagnostics to provide access to Agilent Resolution ctDx FIRST, an NGS liquid biopsy test in the U.S.

The Single Gene Analysis (PCR Microarrays) segment is anticipated to show significant growth during the forecast period. Technological advancements in PCR are expected to propel market growth over the coming years. The recently introduced Droplet Digital PCR (ddPCR) is an advanced technology that allows absolute quantification of nucleic acids with high sensitivity and precision. This PCR technique has been developed as a rapid & precise tool for detecting and monitoring several types of cancers. For instance, Bio-Rad’s ddPCR technology detects cancer subtypes, monitors residual disease, optimizes drug treatment plans, and studies tumor evolution. ddPCR assays have advantages when used in liquid biopsies, enabling measurement of Circulating Tumor Cells (CTCs) and Circulating Nucleic Acids (cfDNA) in blood samples.

Biomarker Insights

Based on biomarkers, the circulating nucleic acids segment led the market with the largest revenue share of 35.4% in 2025. The growth of the segment is attributed to widespread applications of circulating tumor DNA (ctDNA) in liquid biopsy of cancer. Translational cancer researchers are identifying ctDNA from tumors using liquid biopsy. The discovery of ctDNA presents new opportunities for future liquid biopsy applications in cancer diagnosis, serving as a potential biomarker. CtDNA has been suggested as an alternative source in cancer patients for molecular profiling of tumor DNA, as opposed to invasive techniques. A new technique for early detection of cancer and monitoring of disease has been made possible by the identification of aberrant ctDNA from cancer cells.

The exosomes/microvesicles segment is anticipated to grow at the fastest rate over the forecast period with a CAGR of 13.71% over the forecast period. Exosomes show significant advantages in liquid biopsy. Exosomes are present in almost all body fluids, including plasma, cerebrospinal fluid, and urine. They possess high stability and are encapsulated by lipid bilayers. Exosomes act as a common central participant between cells during cancer progression and metastasis. The complex signaling pathway network between exosome-mediated cancer cells and the tumor microenvironment acts as a crucial factor in the cancer progression at all stages.

Application Insights

Based on applications, the cancer application segment led the market with the largest revenue share of 86.5% in 2025, owing to the rising adoption of liquid biopsy in the detection of cancer, aided by the rising prevalence of cancer globally. Liquid biopsy technology is one of the most evolving technologies in diagnostics and has made considerable headway in recent years, showing a significant growth in adoption in clinical applications. This approach is a fast-emerging precision oncology tool that allows for longitudinal monitoring and less invasive molecular diagnostics for therapy purposes. Furthermore, in June 2022, Elypta raised USD 21 million for the development of the MCED test with the LEVANTIS-0087A study in progress for MCED.

The reproductive health segment is anticipated to show the fastest growth over the forecast period with a CAGR of 12.69% owing to the promising R&D in the field of liquid biopsy is being considered for treating and maintaining reproductive health. Furthermore, alliances and partnerships among reproductive health industry actors promote segment expansion.

End Use Insights

Based on end use, the hospitals and laboratories segment led the market with the largest revenue share of 42.7% in 2025. Hospitals are preferred for care due to the availability of various services under one roof. The biggest benefit of hospitals conducting cancer diagnoses is that they can provide results for tests even in emergency situations. Liquid biopsy is helping the doctors by giving them a highly precise cancer diagnosis in a shorter turnaround time, thereby reducing the treatment lag time. Cancer patients in the hospital undergo routine monitoring for analysis of treatment resistance. Chemotherapy has long been a successful and dependable cancer treatment. Chemotherapy may be used to treat cancer or to improve quality of life by symptom management. In addition, chemotherapy can improve the efficacy of other treatments such as surgery or radiation therapy.

The specialty clinics segment is anticipated to grow at the fastest CAGR of 12.16% over the forecast period. An increase in awareness of personalized medicine, technological advancements, and a rise in demand for affordable services are some of the key factors expected to drive the growth of the specialty clinics segment. Another major factor expected to drive market growth is the increase in government initiatives to provide various facilities, such as compensation for diagnostic tests. Moreover, several healthcare institutions are collaborating with laboratories to integrate various clinical tests, including microbiology testing.

Clinical Application Insights

Based on clinical application insight, the therapy selection segment led the market with the largest revenue share of 33.7% in 2025. The market's growth is attributed to the selection of treatment options that can be affected by liquid biopsies to improve patient outcomes. Cancer is the second leading cause of mortality in the U.S. and the most expensive disease to cure. Several advancements in cancer detection and biomarkers have been developed to aid in the study of cancer progression and the creation of successful treatment options. Liquid biopsies can assist in improving cancer therapies by enabling early intervention, enhancing treatment control, and moving decision-making away from reactionary acts and toward more proactive early interventions. Early detection is also facilitating market growth.

The early screening segment is expected to show the fastest growth with a CAGR of 12.34% over the forecast period. The growth of the segment is attributed to the rise in prevalence of multiple cancers and the increase in need to provide efficient methods to detect them at early stages to enable timely, appropriate treatment, is anticipated to drive the market. The need to develop diagnostic options that can detect cancer at an early stage, which can help improve disease management & reduce mortality, is likely to propel the overall market.

Product Insights

Based on product insights, the instruments segment led the market with the largest revenue share of 47.1% in 2025. The dominance of the segment is attributed to the launch of new instruments and the advancement of existing products. For instance, in May 2025, Guardant Health introduced new features for the Guardant 360 liquid test, expanding its cancer subtyping capabilities & biomarker identification to help clinicians identify optimal treatment plans. These applications are enabled through the Guardant Infinity smart liquid biopsy platform and its AI learning engine.

The kits and reagents segment is expected to witness significant growth during the forecast period, owing to the increasing research and development activities by key market players for the development of advanced forms of kits and reagents. The recurring cost associated with kits and reagents further propels the growth of the market segment.

Sample Type Insights

Based on sample type, the blood sample-based segment led the market with the largest revenue share of 72.8% in 2025 and is projected to maintain its dominance over the forecast period. Blood-based liquid biopsy has remarkable advantages over traditional biopsy methods. Blood-based liquid biopsies are noninvasive, painless, and have no risk. In addition, it reduces the time taken and the cost of diagnosis. Exomes, CTCs, and cfDNAs, as well as microvesicles, in a blood sample can be detected, thus increasing the adoption of blood-based liquid biopsy. Circulating biomarkers play a vital role in the understanding of tumorigenesis and metastasis, which can further help determine tumor dynamics at the time of treatment and disease progression. Moreover, the concentration of biomarkers in blood may allow for the quick detection of cancer stage and enable more favorable predictions regarding prognosis in patients.

The others segment is anticipated to grow at the fastest growth rate over the forecast period with a CAGR of 12.43%. The segment includes urine, saliva, and Cerebrospinal Fluid (CSF)-based tests. Urine has also been used extensively for urinalysis and has proven applications in medical diagnosis. While it is not as commonly used in liquid biopsy studies, a few companies focus on developing urine-based liquid biopsy products. Collection of urine samples in large quantities is noninvasive, easier, and inexpensive.

Regional Insights

North America dominated the Liquid Biopsy Market with the largest revenue share of 51.0% in 2025, owing to high cancer prevalence, rapid technological advancements, and growing government initiatives. Moreover, the market is led by the U.S. owing to greater investments and the presence of several biotechnology companies that are developing advanced tests. Various organizations, including the American Society of Clinical Oncology (ASCO), are working to support the deployment of liquid biopsy, which is expected to increase revenue in this market. The market is expected to grow during the forecast period due to intense competition between biotechnology companies and increasing government investments in healthcare institutions to develop more sophisticated tests.

U.S. Liquid Biopsy Market Trends

The Liquid Biopsy Market in the U.S. held the largest share in the North America region in 2025. Rapid technological advancements, recent FDA approvals for liquid biopsy tests, and intense competition between companies are expected to boost market growth over the forecast period. For instance, in November 2023, Illumina, Inc. announced the launch of the next generation of its distributed liquid biopsy, TruSight Oncology 500 ctDNA v2 (TSO 500 ctDNA v2). The research assay enables non-invasive, comprehensive genomic profiling of ctDNA from blood to complement tissue-based testing. Thus, the need for the implementation of liquid biopsy tests is growing to diagnose and eradicate cancer in the target population.

Europe Liquid Biopsy Market Trends

The liquid biopsy industry in Europe is expected to grow exponentially during the forecast period owing to an increase in the number of approvals by regulatory bodies, intense competition between companies to increase market share, government initiatives, and an improving reimbursement scenario. Collaborations among payers, hospitals, and companies are contributing to market growth. Moreover, it is believed that this technique can effectively replace solid tumor tests in most cancer screenings.

The UK liquid biopsy industry has gained ground due to the presence of sophisticated healthcare infrastructure, collaborations between key market players, and the launch of novel products. Government support & initiatives are expected to further propel the country’s cancer diagnostics market in the coming years. Commercial partnerships between the government and key players for the routine use of liquid biopsy in the country are anticipated to drive market growth.

The liquid biopsy industry in Germany is expected to witness growth owing to increasing number of companies striving to enter the market and government-sponsored aid for developing these tests. Moreover, government negotiations with payers to improve reimbursement scenarios, as these tests are expensive, are expected to drive the adoption of liquid biopsy tests. In Germany, Merck and Sysmex Inostics received the first CE approval for liquid biopsy tests for patients with colorectal cancer. Furthermore, intense competition between various biotechnology companies, such as Epigenomics and Roche, is expected to boost market growth. Increasing collaborations between key market players in this region are expected to fuel market growth by increasing research opportunities and developing better test procedures.

Asia Pacific Liquid Biopsy Market Trends

The liquid biopsy industry in the Asia Pacific is expected to grow at the fastest rate over the forecast period with a CAGR of 12.96% due to various factors, such as improving healthcare reforms. Some of the other factors contributing to market growth are increasing population, improving healthcare infrastructure, and entry of new players. The Asia Pacific has a large population and a high prevalence of cancer. Government initiatives, such as free screening for breast cancer, cervical cancer, & lung cancer, and improved collaborations between the government, research institutes, & companies for distribution & supply of these tests for screening cancers, have increased in the past few years.

The Japan liquid biopsy industry is expected to grow rapidly over the forecast period owing to high government spending to reduce cancer prevalence. Many initiatives, such as government grants to various research institutes and companies, can help develop practical solutions to battle cancer. Multiple companies have collaborated with regional private universities to establish and provide liquid biopsy techniques.

The liquid biopsy industry in China is expected to grow significantly over the forecast period. Lung cancer is the leading cause of mortality in China. On the other hand, prostate cancer is the fastest-growing cancer type in the country and the second leading cause of cancer mortality in the Western world. According to the NIH, in 2024, China is expected to report approximately 3,246,625 new cancer cases and 1,699,066 cancer-related deaths, highlighting a significant disease burden in the country. The government has undertaken various initiatives, such as free cervical cancer screening campaigns for women of all ages and collaborations with nonprofit organizations to improve the accessibility of the tests. Multiple companies have entered into alliances and partnership agreements to provide liquid biopsy tests in the country.

Latin America Liquid Biopsy Market Trends

The liquid biopsy industry in Latin America has exhibited significant growth in the past few years owing to increased prevalence of various types of cancer in the region. Several surveys by various government and nonprofit organizations revealed that overall cancer mortality in Latin America is almost twice that of high-income countries. Moreover, according to the data published by the European Society for Medical Oncology, there have been approximately 1.5 million new cancer cases and 700,000 deaths reported in Latin America and the Caribbean region annually.

The Brazil liquid biopsy industry is expected to grow significantly over the forecast period. In LATAM, Brazil has the largest population. Thus, cancer incidence in the country is high, which has led to increased usage of various biopsy techniques. However, it may take time for liquid biopsy to be used widely in the country, owing to the expensive testing procedure and limited availability of skilled professionals. Many professionals in Brazil still consider solid tumor biopsy the gold standard, as it offers a deep analysis of cancer mutation. Moreover, according to data published by the European Society for Medical Oncology, there have been approximately 1.5 million new cancer cases and 700,000 deaths reported in Latin America and the Caribbean annually. These factors are expected to contribute to market growth during the forecast period.

Middle East and Africa Liquid Biopsy Market Trends

The liquid biopsy industry in the Middle East and Africa is one of the regions with tremendous growth opportunities, as the majority of the market is untapped due to the unavailability of organized cancer screening programs in this region, especially in underdeveloped African countries. In recent years, countries such as the UAE, Morocco, & South Africa have implemented organized cancer screening programs. Collaborations of various companies with government institutes to supply these tests are also expected to boost the market. These initiatives are anticipated to lead to the development of newer liquid biopsy tests.

Key Liquid Biopsy Company Insights

The market is driven by a mix of established leaders and emerging innovators, each employing distinct strategies to enhance their market footprint. Major players such as ANGLE plc, Oncimmune Holdings PLC, Guardant Health, and Thermo Fisher Scientific, Inc., among others, have maintained dominance through continuous test innovations, acquisitions, and strategic partnerships aimed at expanding service offerings and reinforcing their global presence. For instance, in August 2025, Exact Sciences Corp. and Freenome, a biotechnology company pioneering an early cancer detection platform, announced they had entered into an agreement granting Exact Sciences exclusive U.S. rights to Freenome’s blood-based colorectal cancer screening tests. This collaboration strengthens Exact Sciences’ leadership in CRC screening by adding a liquid biopsy-based option to complement its Cologuard platform, with the potential to close critical gaps among unscreened populations.

Key Liquid Biopsy Companies:

The following key companies have been profiled for this study on the liquid biopsy market.

-

ANGLE plc

-

Oncimmune Holdings PLC

-

Guardant Health

-

Myriad Genetics, Inc.

-

Biocept, Inc.

-

Lucence Health Inc.

-

Freenome Holdings, Inc.

-

F. Hoffmann-La Roche Ltd.

-

QIAGEN

-

Illumina, Inc.

-

Thermo Fisher Scientific, Inc.

-

Epigenomics AG

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Well-Established Players (F. Hoffmann-La Roche Ltd., Thermo Fisher Scientific, Inc., QIAGEN, Illumina, Inc., Guardant Health, Myriad Genetics, Inc.)

- Expand liquid biopsy portfolios through investments in next generation sequencing, circulating tumor DNA analysis, companion diagnostics, and multi-cancer early detection technologies. Focus on strategic collaborations with pharmaceutical companies, regulatory approvals, product commercialization, and integration of liquid biopsy testing into precision oncology workflows. Strengthen market position through global laboratory networks, clinical evidence generation, and partnerships with healthcare providers and research organizations.

- Broad molecular diagnostics portfolios, strong technological capabilities, established regulatory expertise, extensive commercial infrastructure, and significant investments in research and development. Ability to support large scale clinical adoption through comprehensive testing platforms, bioinformatics capabilities, and global distribution networks. Strong relationships with pharmaceutical companies further support companion diagnostic and precision medicine opportunities.

- High research and development expenditures, complex regulatory requirements, and lengthy clinical validation processes may increase commercialization timelines. Large organizational structures can limit agility in responding to emerging niche applications and evolving customer requirements. Growing competition from specialized liquid biopsy innovators may create pricing and innovation pressures.

Emerging Players (ANGLE plc, Oncimmune Holdings PLC, Biocept, Inc., Lucence Health Inc., Freenome Holdings, Inc., Epigenomics AG)

- Focus on developing specialized liquid biopsy technologies targeting early cancer detection, circulating tumor cell analysis, molecular profiling, and biomarker discovery. Emphasize strategic partnerships, clinical validation programs, technology differentiation, and expansion of proprietary testing platforms. Invest in targeted commercialization initiatives and collaborations with healthcare institutions to increase market penetration and clinical adoption.

- Strong innovation focus, specialized expertise in specific liquid biopsy technologies, and greater flexibility in addressing emerging clinical applications. Ability to develop differentiated solutions for niche diagnostic needs and rapidly adapt to advancements in biomarker research and cancer screening. Focused product development strategies support innovation in early detection and precision oncology segments.

- Limited financial resources, narrower product portfolios, and lower global commercial reach compared with established industry participants. Dependence on successful clinical validation, regulatory approvals, and external partnerships may affect scalability. Challenges in achieving broad market adoption and reimbursement coverage may constrain long term growth potential.

Recent Development

-

In April 2025, Labcorp announced the expansion of announced the expansion of its precision oncology portfolio with two new offerings. The first is Labcorp Plasma Detect, a clinical test designed to help evaluate the risk of disease recurrence in patients with stage III colon cancer. The second is PGDx elio plasma focus Dx, the first and only FDA-authorized kitted liquid biopsy test for pan-solid tumors, which supports the identification of patients who may be eligible for targeted therapies.

-

In April 2025, Guardant Health, a leading precision oncology company, announced a strategic agreement with Bayshore HealthCare, one of Canada’s largest home and community healthcare providers. Through this collaboration, Guardant’s portfolio of precision oncology tests will be made available across Bayshore’s national clinic network, expanding access to advanced blood-based cancer testing and supporting patients throughout the cancer care continuum in Canada.

-

In June 2025, QIAGEN and GENCURIX entered a strategic partnership under the new QIAcuityDx Partnering Program to develop digital PCR IVD assays for oncology. GENCURIX will act as the legal manufacturer responsible for assay development and regulatory approvals, while QIAGEN will market and distribute the products globally through its QIAcuityDx Four platform. This alliance expands the menu of assays available for digital PCR, supports both tissue and liquid biopsy applications, and supports QIAGEN’s strategy to build a broader ecosystem for clinical diagnostics.

-

In February 2025, Lucence and Agilus Diagnostics entered a strategic collaboration to advance cancer testing services across India. Under this agreement, Agilus, the country’s largest diagnostics provider, will integrate Lucence’s cutting-edge LiquidHALLMARK liquid biopsy technology into its expansive laboratory network. LiquidHALLMARK, an ultra-sensitive next-generation sequencing assay, analyzes both circulating tumor DNA (ctDNAand circulating tumor RNA (ctRNA), profiling 80 targeted ctDNA genes and 37 ctRNA fusions for actionable cancer biomarkers. This collaboration aims to expand access to liquid biopsy-based testing for early cancer detection, treatment monitoring, and therapy personalization throughout India, supporting precision oncology accessibility via Agilus’s nationwide reach.

-

In January 2025, Tempus AI, Inc. announced the launch of its FDA-approved next-generation sequencing (NGS)-based in vitro diagnostic test, xT CDx. The test is available to all ordering clinicians across the U.S. xT CDx provides comprehensive genomic insights through one of the largest FDA-approved gene panels currently on the market.

Liquid Biopsy Market Report Scope

Report Attribute

Details

Market size in 2025

USD 13.6 billion

Estimated Market size in 2026

USD 15.2 billion

Projected Market size by 2033

USD 36.2 billion

Growth rate

CAGR of 11.5% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type of Examination, Product, Application, Regional

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Denmark; Sweden; Norway; Japan; China; India; South Korea; Australia; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; and Kuwait

Key companies profiled

Hologic, Inc., Abbott, Becton, Dickinson and Company, F. Hoffmann-La Roche Ltd, Merck KGaA, Thermo Fisher Scientific, Inc., Danaher, Sysmex Corporation, Trivitron Healthcare, and Koninklijke Philips N.V.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Liquid Biopsy Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this report, Grand View Research has segmented the global liquid biopsy market report based on sample type, biomarker, technology, application, end use, clinical application, product, and region:

-

Sample Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Blood Sample

-

Others

-

-

Biomarker Outlook (Revenue, USD Billion, 2021 - 2033)

-

Circulating Tumor Cells (CTCs)

-

Circulating Nucleic Acids

-

Exosomes/Microvesicles

-

Others

-

-

Technology Outlook (Revenue, USD Billion, 2021 - 2033)

-

Multi-gene parallel Analysis (NGS)

-

Single Gene Analysis (PCR Microarrays)

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Cancer

-

Lung Cancer

-

Prostate Cancer

-

Breast Cancer

-

Colorectal Cancer

-

Leukemia

-

Gastrointestinal Cancer

-

Others

-

-

Reproductive Health

-

Others

-

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Hospitals and Laboratories

-

Specialty Clinics

-

Academic and Research Centers

-

Others

-

-

Clinical Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Therapy Selection

-

Treatment Monitoring

-

Early Cancer Screening

-

Recurrence Monitoring

-

Others

-

-

Product Outlook (Revenue, USD Billion, 2021 - 2033)

-

Instruments

-

Consumables Kits and Reagents

-

Software and Services

-

-

Regional Outlook (Revenue, USD Billion, 2021- 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Research Methodology

The liquid biopsy market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each liquid biopsy segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Sample Type

Revenue capture definition

Blood Sample

Revenue is primarily captured from liquid biopsy tests performed using whole blood, plasma, or serum specimens for detection and analysis of circulating tumor DNA, circulating tumor cells, exosomes, and other blood-based biomarkers used in cancer diagnosis, monitoring, and treatment selection.

Others

Revenue flows from liquid biopsy testing utilizing nonblood specimens such as urine, saliva, cerebrospinal fluid, pleural fluid, and other body fluids for biomarker analysis in oncology and related clinical applications where blood sampling is not the primary testing approach.

Segment - Biomarker

Revenue capture definition

Circulating Tumor Cells (CTCs)

Revenue is captured from products, assays, enrichment systems, and analytical platforms designed to isolate, detect, quantify, and characterize circulating tumor cells present in patient body fluids for cancer diagnosis, prognosis, and treatment monitoring applications.

Circulating Nucleic Acids

Revenue flows from liquid biopsy technologies that analyze circulating tumor DNA, cell free DNA, circulating tumor RNA, and other nucleic acid biomarkers for genomic profiling, mutation detection, therapy selection, and disease monitoring.

Exosomes/Microvesicles

Revenue is primarily derived from products and testing solutions focused on the isolation, characterization, and molecular analysis of exosomes and microvesicles released by cells for biomarker discovery and cancer assessment applications.

Others

Revenue accrues from liquid biopsy platforms utilizing biomarkers other than circulating tumor cells, circulating nucleic acids, and exosomes or microvesicles, including proteins, metabolites, tumor educated platelets, and emerging biomarker categories used in clinical and research settings.

Segment - Technology

Revenue capture definition

Multi-gene Parallel Analysis (NGS)

Revenue is captured from next generation sequencing platforms, consumables, bioinformatics solutions, and testing services that simultaneously evaluate multiple genomic alterations from liquid biopsy samples for comprehensive cancer profiling, biomarker identification, and therapy selection.

Single Gene Analysis

(PCR, Microarrays)

Revenue flows from PCR and microarray based liquid biopsy products, reagents, instruments, and associated testing services designed to detect predefined genetic mutations, individual biomarkers, or specific molecular targets for diagnostic and disease monitoring applications.

Segment - Application

Revenue capture definition

Cancer

Revenue is primarily captured from liquid biopsy products, assays, instruments, and testing services used for cancer detection, molecular profiling, treatment selection, disease monitoring, recurrence assessment, and minimal residual disease evaluation across oncology indications.

Lung Cancer

Revenue flows from liquid biopsy solutions specifically utilized for detection of actionable mutations, therapy guidance, treatment monitoring, and disease progression assessment in patients with non small cell and other lung cancer types.

Prostate Cancer

Revenue is derived from liquid biopsy technologies employed for biomarker analysis, treatment stratification, disease surveillance, and monitoring of therapeutic response in prostate cancer management.

Breast Cancer

Revenue is captured from liquid biopsy assays and associated testing services used to identify molecular alterations, monitor treatment effectiveness, detect recurrence, and support personalized treatment decisions in breast cancer patients.

Colorectal Cancer

Revenue accrues from liquid biopsy platforms used for mutation detection, therapy selection, disease monitoring, and recurrence surveillance in colorectal cancer diagnosis and clinical management.

Leukemia

Revenue originates from liquid biopsy based testing solutions that analyze circulating biomarkers for disease detection, treatment monitoring, relapse assessment, and molecular characterization of leukemia and related hematologic malignancies.

Gastrointestinal Cancer

Revenue is generated through liquid biopsy applications supporting molecular profiling, treatment guidance, disease monitoring, and recurrence detection across gastric, esophageal, pancreatic, liver, and other gastrointestinal cancers.

Others (Cancer)

Revenue flows from liquid biopsy applications in oncology indications not classified under lung, prostate, breast, colorectal, leukemia, or gastrointestinal cancers, including ovarian, melanoma, bladder, head and neck, and other cancer types.

Reproductive Health

Revenue is primarily captured from liquid biopsy technologies utilized in reproductive and prenatal applications, including non invasive genetic assessment, fetal health evaluation, and other reproductive health related molecular testing.

Others (Reproductive Health)

Revenue is derived from reproductive health applications beyond core prenatal and genetic assessment uses, encompassing emerging and specialized liquid biopsy based reproductive testing services and related diagnostic applications.

Segment - End Use

Revenue capture definition

Hospitals and Laboratories

Revenue is primarily captured from liquid biopsy tests, instruments, consumables, and associated services utilized within hospitals, clinical laboratories, pathology laboratories, and diagnostic networks for routine patient diagnosis, treatment selection, and disease monitoring.

Specialty Clinics

Revenue flows from liquid biopsy products and testing services adopted by oncology clinics, cancer centers, and other specialized healthcare facilities focused on disease specific diagnosis, therapeutic decision making, and patient management.

Academic and Research Centers

Revenue is derived from liquid biopsy platforms, reagents, analytical tools, and research services purchased by universities, research institutes, and academic medical centers for biomarker discovery, translational research, and clinical study activities.

Others

Revenue accrues from liquid biopsy products and services utilized by end users outside hospitals, laboratories, specialty clinics, and academic institutions, including pharmaceutical companies, contract research organizations, public health agencies, and other healthcare organizations.

Segment - Clinical Application

Revenue capture definition

Therapy Selection

Revenue is primarily captured from liquid biopsy tests, assays, and analytical solutions used to identify actionable biomarkers, genomic alterations, and molecular signatures that support targeted therapy selection and personalized treatment decisions in clinical practice.

Treatment Monitoring

Revenue flows from liquid biopsy technologies utilized to assess therapeutic effectiveness, track molecular response, evaluate treatment resistance, and support ongoing patient management throughout the course of treatment.

Early Cancer Screening

Revenue is derived from liquid biopsy products and testing services designed to detect cancer associated biomarkers in asymptomatic or at risk individuals for early disease identification and population screening applications.

Recurrence Monitoring

Revenue accrues from liquid biopsy solutions used to detect residual disease, identify cancer relapse, and monitor disease recurrence following treatment completion or clinical remission.

Others

Revenue is captured from liquid biopsy applications beyond therapy selection, treatment monitoring, early cancer screening, and recurrence monitoring, including prognosis assessment, disease stratification, companion diagnostic development, and emerging clinical use cases.

Segment - Product

Revenue capture definition

Instruments

Revenue is primarily captured from capital equipment used for liquid biopsy workflows, including sample preparation systems, nucleic acid extraction platforms, sequencing instruments, PCR systems, analyzers, and other hardware supporting biomarker detection and analysis.

Consumables, Kits and Reagents

Revenue flows from recurring purchases of assay kits, reagents, sample collection products, extraction materials, library preparation kits, cartridges, controls, and other consumables required for routine liquid biopsy testing and laboratory operations.

Software and Services

Revenue is derived from bioinformatics software, data analysis platforms, interpretation tools, testing services, laboratory service offerings, and workflow support solutions that facilitate processing, analysis, reporting, and clinical utilization of liquid biopsy results.

Estimation Model

The Liquid Biopsy Market size was estimated using a bottom up approach that involved identifying key market participants, benchmarking their liquid biopsy product portfolios, and evaluating revenues generated from relevant products and services. Market revenues were further validated through analysis of technology specific adoption rates, patient utilization patterns, and end user demand across major application areas. The aggregated revenues were mapped across key technologies and product categories, followed by assessment of market shares of leading companies to derive the overall market size. The findings were validated through secondary research, industry publications, company disclosures, and expert insights to ensure accuracy and consistency.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Liquid Biopsy Competitive Landscape & Precision Oncology Assessment

Assessed the global liquid biopsy market landscape across circulating tumor DNA analysis, circulating tumor cell technologies, exosome-based diagnostics, multi cancer early detection platforms, and companion diagnostics. Analyzed leading market participants, technology adoption trends, regulatory developments, clinical validation activities, and competitive positioning across oncology applications. Evaluated strategic collaborations, product launches, and commercialization initiatives supporting market expansion.

Helped the client identify growth opportunities across precision oncology and cancer screening applications, benchmark competitive capabilities, assess technology leadership, and prioritize investments in liquid biopsy innovation, biomarker development, and clinical commercialization strategies.

Liquid Biopsy Technology & Product Benchmarking Study

Delivered comprehensive benchmarking of liquid biopsy technologies across next generation sequencing, PCR based testing, circulating tumor DNA analysis, circulating tumor cell detection, exosome profiling, and multi cancer early detection solutions. Evaluated product performance, clinical utility, workflow efficiency, scalability, regulatory status, and technology differentiation among key industry participants.

Enabled the client to assess technology competitiveness, identify product development opportunities, benchmark innovation strategies, and support investment decisions related to molecular diagnostics, precision medicine, and noninvasive cancer testing platforms.

Liquid Biopsy Laboratory Infrastructure & Commercialization Feasibility Assessment

Assessed diagnostic laboratory infrastructure, hospital oncology networks, reference laboratories, pharmaceutical partnerships, reimbursement environments, regulatory frameworks, and commercialization pathways supporting liquid biopsy adoption. Evaluated testing capabilities, market access requirements, laboratory integration trends, and clinical implementation considerations across major healthcare markets.

Supported commercialization planning by identifying market entry opportunities, evaluating laboratory partnerships and distribution models, assessing reimbursement and regulatory considerations, mitigating operational risks, and strengthening long term adoption potential across oncology diagnostics and precision medicine markets.

Frequently Asked Questions About This Report

Some key players operating in the liquid biopsy market include QIAGEN; Myriad Genetics, Inc; BIOCEPT, Inc; Guardant Health; F. Hoffmann-La Roche Ltd; Illumina, Inc; ANGLE plc; Oncimmune Holdings PLC; Thermo Fisher Scientific, Inc.; Lucence Health, Inc.; Freenome Holdings, Inc.; Epigenomics AG

Key factors that are driving the market growth include factor such as the growing prevalence of cancer, technological advancements in cancer diagnostics, and rising preference for minimally invasive cancer diagnostics. Moreover, ongoing research for the development of liquid biopsy assays and tests aided with the rising adoption and development of multi-cancer early detection tests is providing a major opportunity for growth of overall market.

The liquid biopsy industry in the Asia Pacific is expected to grow at the fastest rate over the forecast period with a CAGR of 13.0% due to various factors, such as improving healthcare reforms. Some of the other factors contributing to market growth are increasing population, improving healthcare infrastructure, and entry of new players.

The blood sample segment held the largest market share of 72.8% in 2025 and is projected to maintain its dominance over the forecast period. Blood-based liquid biopsy has remarkable advantages over traditional biopsy methods. Blood-based liquid biopsies are noninvasive, painless, and have no risk.

The instruments product segment dominated the market for liquid biopsy in 2025, with a revenue share of 47.1%. The dominance of the segment is attributed to the launch of new instruments and the advancement of existing products.

The global liquid biopsy market size was estimated at USD 13.6 billion in 2025 and is expected to reach USD 16.2 billion in 2026.

The global liquid biopsy market is expected to grow at a compound annual growth rate of 11.5% from 2026 to 2033 to reach USD 32.6 billion by 2033.

North America dominated the liquid biopsy market with a share of 51.0% in 2025. This is attributable to high cancer prevalence, rapid technological advancements, and growing government initiatives. Moreover, the market is led by U.S. owing to greater investments and presence of several biotechnology companies that are developing advanced tests.

The multi-gene-parallel analysis (NGS) segment held the largest market revenue share of 76.7% in 2025 and is anticipated to grow at the fastest rate over the forecast period. NGS technology allows the detection of various tumor-causing mutations and the identification of potential emergence of post-treatment resistance mechanisms from pre-existing clones.

About the Author(s)

Clinical Diagnostics Research Team

Healthcare · Clinical DiagnosticsThis report was authored by the clinical diagnostics research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the clinical diagnostics segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.