- Home

- »

- Advanced Interior Materials

- »

-

Machine Tools Market Size, Share, Trends Report, 2026-2033GVR Report cover

![Machine Tools Market (2026 - 2033)Report]()

Machine Tools Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (Metal Cutting, Metal Forming), By Technology (Computer Numerical Control (CNC), Conventional), By End Use, By Region, And Segment Forecasts

Market Size, 2025

$117.2BMarket Estimate, 2026

$123.7BMarket Forecast, 2033

$183.5BCAGR, 2026–2033

5.8%Machine Tools Market Summary

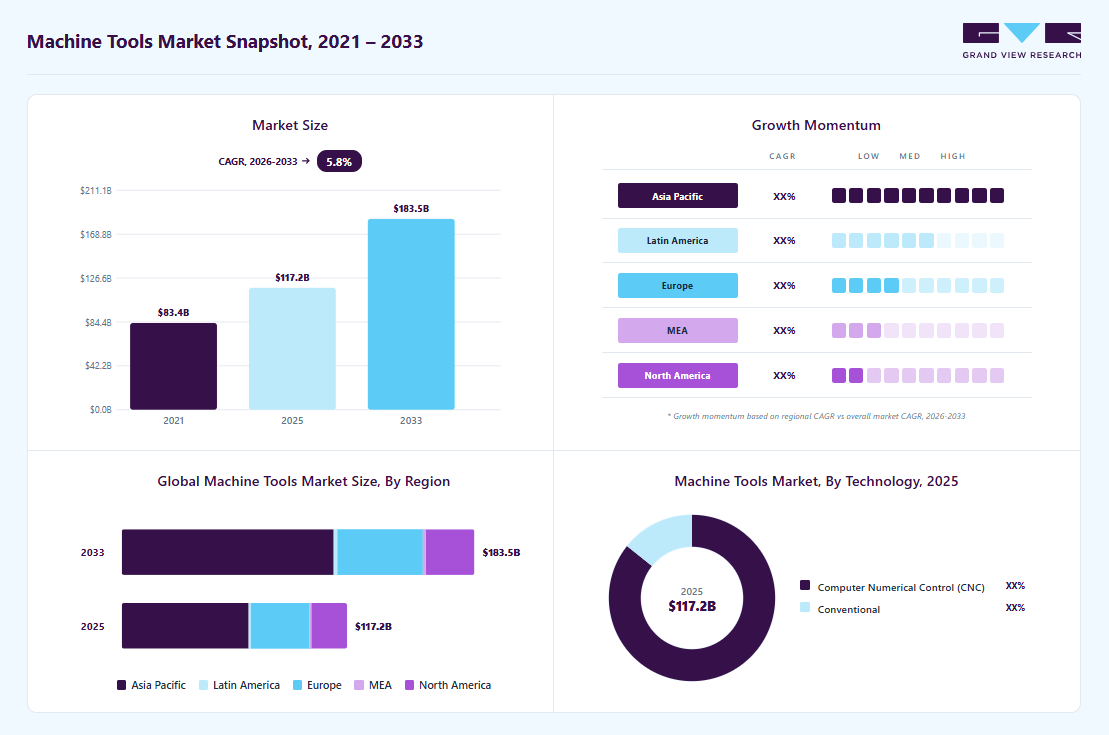

The global machine tools market size was valued at USD 117.2 billion in 2025 and is projected to grow from USD 123.7 billion in 2026 to USD 183.5 billion by 2033, at a CAGR of 5.8% from 2026 to 2033. The Asia Pacific held the largest share of 56.2% of the global market in 2025. The machine tools market is primarily driven by the growing demand for high-precision components across industries such as automotive, aerospace, and electrical manufacturing.

Key Market Trends & Insights

- By end-use: Electrical industry end-use segment is expected to register a CAGR of 7.3% from 2026 to 2033.

- By technology: Computer numerical control segment accounted for 85.7% share in 2025

- By type: Metal cutting segment dominated the market with a 76.8% share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (56.2% revenue share, 2025)

- By country: The China led the Asia Pacific market in 2025.

Market Size & Forecast

- Market size in 2025: USD 117.2 Billion

- Estimated market size in 2026: USD 123.7 Billion

- Projected market size by 2033: USD 183.5 Billion

- CAGR (2026-2033): 5.8%

Rapid industrialization and the expansion of manufacturing activities, especially in emerging economies, are increasing the need for advanced machining solutions.")

Another key driver is the growing focus on efficiency, cost optimization, and shorter production times in manufacturing processes. Industries are continuously upgrading from conventional machines to technologically advanced systems to minimize human error and enhance output quality. Government initiatives supporting domestic manufacturing, along with the growth of sectors such as defense, infrastructure, and heavy engineering, are also contributing to market expansion.

Market Dynamics

The machine tools market is driven by the steady expansion of manufacturing industries and the rising demand for high-precision components across sectors such as automotive, aerospace, and electronics. Increasing adoption of automation and CNC-based systems is enhancing productivity, accuracy, and operational efficiency, making them essential in modern production environments. In addition, the shift toward electric vehicles, lightweight materials, and complex part designs is further accelerating the need for advanced machining and forming technologies.

Although the CNC machines offer a lot of advantages over traditional machines, the high costs associated with the CNC machines are expected to hinder the market growth. The costs associated with purchasing and installing products are high, which results in small manufacturing companies being unable to buy the product. To operate the CNC machines, proper training and skills are required by the operator to perform the desired tasks. In the case of traditional machines, the operators required training regarding the technicalities of the machines, while in the case of CNC machines, the operators need to be aware of the codes used in the machining of jobs/workpieces, thereby, increasing the expenses for training and hiring trained professionals.

Market Concentration & Characteristics

The machine tools market is fragmented, with a mix of established global manufacturers and numerous regional and local players competing across different product segments and price points. While a few large companies hold significant technological expertise and market presence, particularly in advanced CNC systems, a substantial portion of the market is served by small- and mid-sized manufacturers that cater to cost-sensitive and customized requirements. The presence of diverse end-use industries, varying levels of automation adoption, and strong regional manufacturing bases further contribute to this fragmented structure.

The machine tools market is highly innovative, driven by the need for precision, efficiency, and automation in manufacturing. Advancements in CNC systems, multi-axis machining, additive manufacturing integration, and digital technologies such as IoT and AI are transforming traditional machining processes. Manufacturers are increasingly focusing on smart machines with real-time monitoring, predictive maintenance, and improved energy efficiency.

Regulations play a moderate but important role in shaping the market, particularly in areas such as worker safety, environmental standards, and energy efficiency. Governments across regions are enforcing stricter norms on emissions, waste management, and workplace safety, pushing manufacturers to adopt cleaner, more efficient machine tools. Compliance with international quality standards and certifications is also essential, especially for companies operating in global supply chains.

End-user concentration in the machine tools market is relatively diversified, with demand spread across multiple industries, including automotive, aerospace, general engineering, and electrical manufacturing. However, the automotive sector remains a dominant consumer due to its large-scale production requirements and continuous need for precision components. At the same time, growing sectors like aerospace and electronics are increasing their share, driven by high-precision and complex machining needs.

Drivers, Opportunities & Restraints

The machine tools market is driven by the steady expansion of manufacturing industries and the rising demand for high-precision components across sectors such as automotive, aerospace, and electronics. Increasing adoption of automation and CNC-based systems is enhancing productivity, accuracy, and operational efficiency, making them essential in modern production environments. In addition, the shift toward electric vehicles, lightweight materials, and complex part designs is further accelerating the need for advanced machining and forming technologies.

Significant opportunities are emerging from the rapid growth of smart manufacturing and Industry 4.0 practices. Integration of technologies such as IoT, artificial intelligence, and data analytics enables real-time monitoring, predictive maintenance, and improved process optimization. Emerging economies are also showing strong growth potential due to expanding industrial bases, government initiatives supporting domestic manufacturing, and increased investments in infrastructure and defense.

However, the market faces certain restraints, including high initial investment costs and maintenance expenses associated with advanced machine tools, which can limit adoption among small and medium-sized enterprises. Economic uncertainties and fluctuations in key end-use industries, particularly automotive and heavy engineering, can also impact demand.

Type Insights

The metal cutting segment dominated the machine tools market, supported by its widespread application across industries such as automotive, mechanical engineering, metal working, and aerospace. These machines are essential for producing finished components with precise geometry by cutting both ferrous and non-ferrous metals. They enable manufacturers to achieve superior surface finish, high dimensional accuracy, and complex shapes, which are critical for modern industrial requirements. The growing demand for advanced, automated metal-cutting solutions, particularly CNC-based systems, is further driving the segment's expansion as industries continue to prioritize precision and efficiency.

The metal forming segment is witnessing steady growth at a CAGR of 5.4%, driven by its extensive use across industries including aerospace, automotive, construction, energy, and electronics. These machines are employed in processes such as bending, pressing, shaping, and shearing, enabling efficient mass production with minimal material waste. The increasing adoption of press brake machinery is a key driver of segment growth, as it is widely used for sheet metal bending across sectors such as agriculture, shipbuilding, automotive, and petroleum equipment manufacturing.

Technology Insights

Computer Numerical Control (CNC) technology dominated the machine tools market and accounted for 85.7% share in 2025, driven by its ability to deliver high precision, automation, and consistent production quality. CNC machines enable manufacturers to produce complex components with minimal human intervention, reducing errors and improving operational efficiency. The increasing adoption of smart manufacturing practices, along with the integration of digital technologies such as IoT and real-time monitoring, has further strengthened the demand for CNC systems.

The conventional segment is also experiencing steady growth at 4.8% CAGR, primarily due to its cost-effectiveness and suitability for small-scale operations and low-volume production. These machines are widely used in workshops, repair facilities, and small manufacturing units where flexibility and lower initial investment are key considerations. Conventional machine tools are preferred for simple machining tasks and in regions where the adoption of advanced automation is still limited.

End Use Insights

The automotive sector dominated the machine tools market in 2025 with 41.9% share, supported by its large-scale production requirements and continuous demand for precision-engineered components. Machine tools are extensively used in manufacturing engine parts, transmission systems, chassis components, and other critical automotive parts that require high accuracy and consistency. The sector’s strong reliance on mass production, coupled with increasing adoption of automation and CNC technologies, has significantly driven demand.

The electrical industry is expected to be the fastest-growing CAGR of 7.3% during forecast period, driven by the rising demand for electronic devices, power equipment, and electrical infrastructure. Machine tools play a crucial role in producing precise components such as connectors, enclosures, and micro-parts used in electrical and electronic applications. Rapid advancements in consumer electronics, renewable energy systems, and power distribution networks are accelerating the need for high-precision and miniaturized components.

Regional Insights

North America represents a mature yet steadily growing market, supported by the presence of advanced manufacturing industries and early adoption of automation technologies. Demand is largely driven by aerospace, automotive, and defense sectors that require high-precision machining. The region is also witnessing increased investments in smart manufacturing, reshoring of production activities, and integration of digital technologies, which are enhancing productivity and sustaining market growth.

U.S. Machine Tools Market Trends

The U.S. led the North American machine tools market, supported by its strong base in aerospace, automotive, and defense manufacturing, along with widespread adoption of advanced automation technologies. The country continues to prioritize strengthening domestic production and upgrading industrial capabilities. In March 2026, GE Aerospace announced plans to invest an additional USD 1 billion in its U.S. manufacturing facilities and supplier base to accelerate engine deliveries, increase production of components that extend maintenance intervals, and enhance defense manufacturing to meet rising military demand. This reflects the increasing focus on advanced, high-precision manufacturing, which is driving demand for modern machine tools.

The Canada machine tools market is experiencing steady growth in the machine tools market, driven by ongoing development in industrial and manufacturing sectors. The country’s aerospace and automotive industries, along with increasing adoption of automated solutions in metalworking, are supporting demand. Government initiatives promoting innovation and advanced manufacturing are encouraging companies to modernize their operations. In addition, the strong presence of small and medium-sized enterprises and the rising need for flexible, customized production solutions are contributing to consistent market expansion.

Europe Machine Tools Market Trends

Europe holds a significant share in the machine tools market, supported by strong engineering capabilities and a focus on high-quality manufacturing. The region benefits from well-established automotive and industrial machinery sectors, along with stringent quality standards that drive the adoption of advanced machine tools. Increasing emphasis on sustainability, energy-efficient equipment, and Industry 4.0 initiatives is further supporting market expansion across key economies such as Germany, Italy, and France.

The Germany machine tools market dominated the market in Europe in 2025, supported by its strong automotive and industrial manufacturing base, along with advanced engineering capabilities. According to a GTAI report, Germany produced nearly 4.1 million passenger cars and around 351,000 commercial vehicles in 2024, highlighting its position as a leading automotive manufacturing hub. Additionally, the presence of a significant number of global automotive suppliers in the country continues to drive demand for high-precision machine tools. This strong industrial ecosystem, combined with continuous technological advancements, reinforces Germany’s leadership in the regional market.

The Italy machine tools market is emerging as a growing market within Europe, driven by its well-established industrial machinery and metalworking sectors. The country has a strong presence of small and medium-sized manufacturers specializing in precision engineering and customized production. Increasing adoption of advanced machining technologies, along with rising exports of industrial equipment, is supporting market growth. Furthermore, Italy’s focus on innovation, design efficiency, and flexible manufacturing solutions is contributing to the expanding demand for machine tools across various industries.

Asia Pacific Machine Tools Market Trends

Asia Pacific dominated the machine tools market with revenue share of 56.2% in 2025 and is also the fastest-growing region at CAGR of 6.7%, driven by strong manufacturing bases in countries such as China, Japan, South Korea, and India. Rapid industrialization, expanding automotive and electronics sectors, and increasing adoption of advanced manufacturing technologies are fueling demand. Government initiatives supporting domestic production and infrastructure development further strengthen the region’s leadership, along with the presence of both large-scale manufacturers and a wide network of small and mid-sized enterprises.

The China machine tools market dominated the machine tools market in Asia Pacific in 2025, supported by strong government initiatives promoting investments in manufacturing and industrial expansion. The country benefits from rapid urbanization, population growth, and rising disposable incomes, which have significantly boosted sectors such as automotive and construction. Large-scale infrastructure development, evolving business models, and the expansion of the middle-class population continue to strengthen industrial output.

The India machine tools market is expected to be the fastest-growing market in the region, driven by rapid urbanization and increasing infrastructure development activities. Continued economic progress is supporting the expansion of the construction sector, which in turn is fueling demand for machine tools. The industry is benefiting from substantial investments in energy and infrastructure projects under initiatives such as the National Skill Development Mission (NSDM), Atal Mission for Rejuvenation and Urban Transformation (AMRUT), 100 Smart Cities Mission, Make in India, and Power for All (PFA). These programs are encouraging industrial growth, enhancing manufacturing capabilities, and positively impacting the adoption of advanced machine tools across the country.

Latin America Machine Tools Market Trends

Latin America is experiencing gradual growth in the machine tools market, supported by the development of industrial sectors and increasing investments in manufacturing activities. Countries such as Brazil and Mexico are key contributors, driven by automotive production and metalworking industries. While the market is still developing, improving economic conditions and growing demand for localized manufacturing are encouraging the adoption of modern machining technologies.

The Brazil machine tools market dominated the machine tools market in Latin America, supported by its position as the largest industrial and manufacturing hub in the region. The country’s strong presence in automotive production, metalworking, and heavy machinery industries continues to drive demand for machine tools. Increasing investments in infrastructure and industrial development, along with efforts to strengthen domestic manufacturing capabilities, are further supporting market growth.

Middle East & Africa Machine Tools Market Trends

The Middle East & Africa region is witnessing emerging growth, driven by diversification efforts away from oil-dependent economies and increasing investments in industrial and infrastructure projects. Demand for machine tools is rising in sectors such as construction, energy, and metal fabrication. Although the market is relatively smaller compared to other regions, ongoing industrialization initiatives and government-led development programs are expected to create new opportunities over the forecast period.

The South Africa machine tools market led the machine tools market in the Middle East & Africa region, supported by its relatively advanced industrial base and well-established metalworking sector. The country’s automotive assembly, mining equipment manufacturing, and general engineering industries are key contributors to machine tool demand. Ongoing investments in infrastructure development and industrial projects are further strengthening market growth.

Key Machine Tools Company Insights

Some of the key players operating in the market include DMG MORI. CO., LTD., Okuma Corporation, and Makino Inc.

-

DMG MORI Co., Ltd. focuses on providing integrated manufacturing solutions that go beyond standalone machine tools by combining equipment, software, and engineering services. The company specializes in advanced machining technologies, particularly multi-axis and 5-axis systems, while also incorporating automation and digital capabilities to support smart manufacturing environments. Its globally connected production and service network allows it to deliver localized support and respond efficiently to customer needs across industries.

-

Okuma Corporation is a machine tool manufacturer known for developing both its equipment and control systems internally, allowing close integration between machines and software. The company offers a broad portfolio including CNC lathes, machining centers, multitasking machines, and grinding solutions, supported by its own CNC controls and automation technologies. This integrated approach helps improve accuracy, machine stability, and overall productivity. Okuma also incorporates advanced features such as thermal control, collision prevention, and connected technologies to support efficient and reliable operations in modern manufacturing environments.

Key Machine Tools Companies:

The following key companies have been profiled for this study on the machine tools market.

- Amada Machine Tools Co., Ltd.

- CHIRON GROUP SE

- DMG MORI. CO., LTD.

- DN Solutions

- UNITED MACHINING SOLUTIONS

- HYUNDAI WIA CORP

- JTEKT Corporation

- Komatsu Ltd

- Makino Inc.

- Okuma Corporation

- Hurco Companies, Inc.

- Dalian Machine Tool Group (DMTG) Corporation

- Amera Seiki

- Haas Automation, Inc

- Datron AG

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: DMG MORI CO. LTD; Amada Machine Tools Co., Ltd; Georg Fischer Ltd;

HYUNDAI WIA CORP; Datron AG; Haas Automation, Inc.- Focus on expanding global footprint through acquisitions, partnerships, and strengthening dealer networks

- Continuous investment in advanced CNC technologies, automation, and smart manufacturing solutions

- Vast geographic presence ensuring easy product availability and accessibility

- Established brand reputation

- Market experience

- Wide product portfolio

- Exposure to fluctuations in industrial production, automotive demand, and capital expenditure cycles

- Higher equipment costs compared to regional and low-cost manufacturers

- Complex global operations and supply chain dependencies

Emerging Players: CHIRON Group SE; Okuma Corporation; Makino; DN Solutions; Amera Seiki; Dalian Machine Tool Group (DMTG) Corporation

- Focus on cost-competitive and application-specific machine tool solutions

- Expansion through regional partnerships and strengthening local manufacturing capabilities

- Increasing investments in automation, precision machining, and digital manufacturing technologies

- Competitive pricing and lower ownership costs

- Strong presence in regional and developing manufacturing markets

- Faster decision-making and flexible customization capabilities

- Growing adoption in automotive, electronics, and general

- Limited global brand recognition and aftermarket support compared to multinational leaders

- Narrower product portfolio and lower technological diversification

- Lower investment capacity in advanced automation and Industry 4.0 solutions

Recent Developments

-

In January 2026, DN Solutions has acquired Germany-based HELLER to strengthen its global footprint and expand its machine tool portfolio. The combination brings together DN Solutions’ scale with HELLER’s precision engineering capabilities. The merged entity is expected to boost production capacity and improve operational efficiency. This move supports the company’s strategy to enhance competitiveness and address evolving manufacturing needs.

-

In July 2025, UNITED GRINDING Group acquired GF Machining Solutions and formed UNITED MACHINING SOLUTIONS, expanding its presence in the global machine tools market. The new entity brings together multiple brands and a wide international footprint. With strong combined revenues, the group enhances its capabilities in precision machining and advanced manufacturing. The move reflects a growing trend of consolidation to strengthen technology and market reach.

-

In November 2025, CHIRON Group has expanded its micromachining capabilities with advanced solutions designed for producing small, complex components with high precision. Its Micro5 and Micro5 XL machines offer high-speed performance within a compact setup, supporting demanding applications. These systems are tailored for industries requiring tight tolerances and consistent accuracy. The development highlights the company’s focus on precision and efficient manufacturing solutions.

Machine Tools Market Report Scope

Report Attribute

Details

Market size in 2025

USD 117.2 billion

Estimated market size in 2026

USD 123.7 billion

Projected market size by 2033

USD 183.5 billion

Growth rate

CAGR of 5.8% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company market position analysis, competitive landscape, growth factors, and trends

Segments covered

Type, technology, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America, Middle East & Africa

Country Scope

U.S.; Canada; Mexico; Spain; France; Germany; Italy; Switzerland; China; India; Japan; Taiwan; South Korea; Brazil; Argentina; Saudi Arabia; South Africa

Key companies profiled

Amada Machine Tools Co., Ltd.; CHIRON GROUP SE; DMG MORI Co., Ltd.; DN Solutions; UNITED MACHINING SOLUTIONS; HYUNDAI WIA CORP; JTEKT Corporation; Komatsu Ltd.; Makino Inc.; Okuma Corporation; Hurco Companies, Inc.; Dalian Machine Tool Group (DMTG) Corporation; Amera Seiki; Haas Automation, Inc.; Datron AG.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Machine Tools Market Report Segmentation

This report forecasts revenue growth at global, regional & country levels, and provides an analysis on the latest trends and opportunities in each of the sub-segments from 2021 to 2033. For the purpose of this study, Grand View Research has segmented the machine tools market on the basis of type, technology, end use, and region:

-

Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Metal Cutting

-

Machining Centers

-

Turning Machines

-

Grinding Machines

-

Milling Machines

-

Eroding machines

-

Others

-

-

Metal Forming

-

Bending Machines

-

Presses

-

Punching Machines

-

Others

-

-

-

Technology Outlook (Revenue, USD Billion, 2021 - 2033)

-

Computer Numerical Control (CNC)

-

Conventional

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Mechanical Engineering

-

Metal Working

-

Aerospace

-

Electrical industry

-

Automotive

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Spain

-

Germany

-

Italy

-

France

-

Switzerland

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Taiwan

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation

Detailed assessment of the global machine tools market across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, including country-level analysis for China, Japan, Germany, the U.S., Italy, India, South Korea, and other manufacturing hubs. The customization also incorporates a dedicated deep dive into the CNC Machining Centers and Turning Centers market across key regional clusters.

Identify high-growth manufacturing hubs and country-level investment opportunities. Support regional expansion, localization, and distributor network strategies. Enable prioritization of markets based on industrial output, automation adoption, and advanced manufacturing investments.

Trade Assessment

Evaluation of global trade flows for machine tools and CNC equipment, including import-export analysis, manufacturing hubs, tariff structures, localization trends, supply chain dependencies, and geopolitical impacts on precision manufacturing equipment trade.

Identify export-oriented growth opportunities and sourcing advantages. Support supply chain diversification and localization strategies. Enable risk assessment related to tariffs, export controls, and geopolitical exposure.

Company Market Share & Positioning Benchmarking

Detailed benchmarking of key machine tool manufacturers based on estimated market share, regional dominance, product specialization, automation capabilities, pricing positioning, and technology leadership.

Understand market concentration and competitive positioning across global and regional markets. Support competitive differentiation and strategic decision-making.

Frequently Asked Questions About This Report

The automotive segment led with a 41.9% revenue share in 2025, while the electrical industry segment is the fastest-growing.

The computer numerical control (CNC) technology led with a 85.7% revenue share in 2025.

The metal cutting segment accounted for the largest revenue share of 76.8% in 2025.

The global machine tools market size was valued at USD 117.2 billion in 2025 and is estimated at USD 123.7 billion for 2026.

The global machine tools market is expected to grow at a CAGR of 5.8% from 2026 to 2033, reaching USD 183.5 billion by 2033.

Asia Pacific dominated with a 56.2% revenue share in 2025 and is also the fastest-growing region at CAGR of 6.7%, driven by strong manufacturing bases in countries such as China, Japan, South Korea, and India. Rapid industrialization, expanding automotive and electronics sectors, and increasing adoption of advanced manufacturing technologies are fueling demand.

Key players include Amada Machine Tools Co., Ltd.; CHIRON GROUP SE; DMG MORI Co., Ltd.; DN Solutions; UNITED MACHINING SOLUTIONS; HYUNDAI WIA CORP; JTEKT Corporation; Komatsu Ltd.; Makino Inc.; Okuma Corporation; Hurco Companies, Inc.; Dalian Machine Tool Group (DMTG) Corporation; Amera Seiki; Haas Automation, Inc.; Datron AG.

The key factors for the market growth include steady expansion of manufacturing industries and the rising demand for high-precision components across sectors such as automotive, aerospace, and electronics.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.