- Home

- »

- Advanced Interior Materials

- »

-

Metal Casting Market Size And Share Report, 2026-2033GVR Report cover

![Metal Casting Market (2026 - 2023)Report]()

Metal Casting Market (2026 - 2023)

Size, Share & Trend Analysis Report, By Material (Iron, Steel, Aluminum), By Application (Automotive, Industrial, Building & Construction), By Region (North America, Europe, Asia Pacific, Latin America, MEA), And Segment Forecasts

Market Size, 2025

$290.2BMarket Estimate, 2026

$303.7BMarket Forecast, 2033

$408.3BCAGR, 2026–2033

4.3%Metal Casting Market Summary

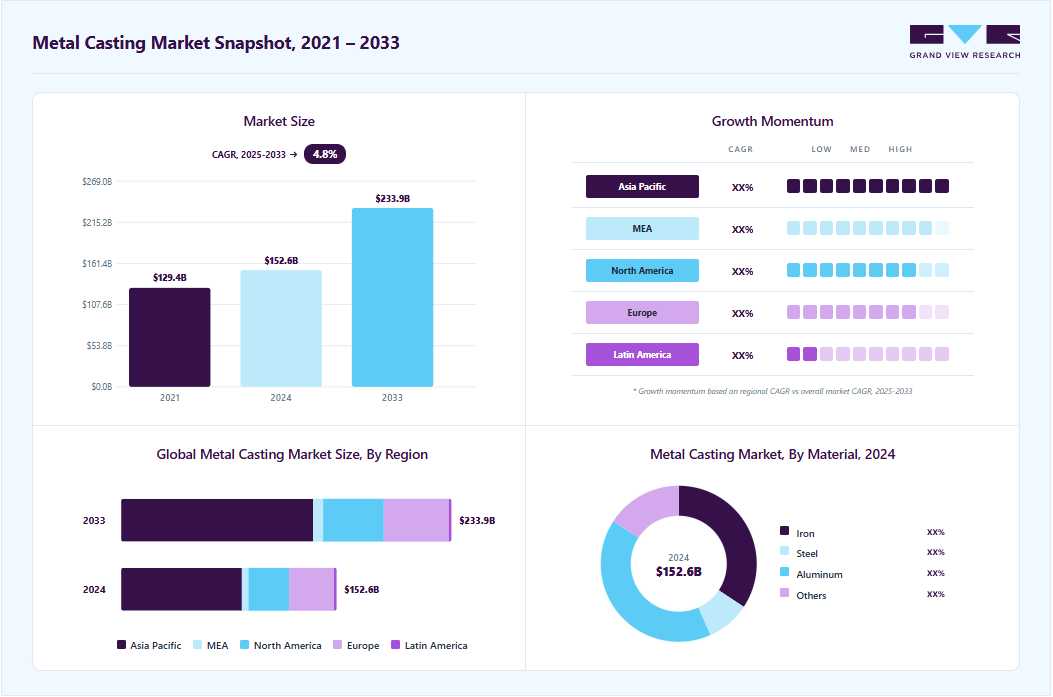

The global metal casting market size was valued at USD 290.2 billion in 2025 and is projected to grow from USD 303.7 billion in 2026 to USD 408.3 billion by 2033, at a CAGR of 4.3% from 2026 to 2033. Asia Pacific dominated the metal casting market with the largest revenue share of 56.2% in 2025. Metal castings are essential for producing complex and high-strength components at relatively lower costs.

Key Market Trends & Insights

- By material: Iron segment held the largest market share of 40.0% in 2025.

- By application: Automotive segment held the largest market share of 41.0% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (56.2% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 290.2 Billion

- Estimated market size in 2026: USD 303.7 Billion

- Projected market size by 2033: USD 408.3 Billion

- CAGR (2026-2033): 4.3%

With growing vehicle production, particularly in electric and hybrid vehicles, the demand for lightweight, durable cast metal components such as engine blocks, chassis, and transmission housings has surged. Automakers are also shifting toward aluminum and magnesium castings to reduce vehicle weight, improve fuel efficiency, and meet emission regulations. Infrastructure and industrial development across emerging economies are other major drivers for the metal casting industry. In India, for instance, the government allocated over USD 130 billion in 2024 for infrastructure projects under the PM Gati Shakti plan, spurring demand for castings used in construction equipment, water distribution, and transportation systems. Similarly, in 2025, Saudi Arabia and the UAE ramped up investment in mega-projects like NEOM and Etihad Rail, requiring massive volumes of ductile iron and steel castings. Such large-scale infrastructure activities fuel demand for ferrous and non-ferrous cast products across construction, utilities, and public transportation networks.The renewable energy sector is contributing significantly to the expansion of the casting industry. In 2024 alone, global wind power capacity additions reached 116 GW, led by China, the U.S., and Germany. Wind turbine components such as rotor hubs, nacelle frames, and bearing housings are commonly produced using precision casting techniques due to their complex geometry and durability requirements. The scaling up of offshore wind farms in Europe and coastal Asia in 2025 further amplified the demand for corrosion-resistant metal castings, particularly stainless steel and specialized iron alloys.

")

Technological advancements in casting processes have strengthened the market's capability to meet high-precision industrial demands. As of 2025, more than 35 percent of mid-to-large foundries globally have adopted 3D printing for pattern making and rapid prototyping, reducing development time by over 40 percent. Countries such as Germany, Japan, and South Korea have seen widespread integration of automated molding lines and solidification simulation software, enabling consistent production of high-performance components for aerospace, marine, and defense applications. These innovations improve quality and address labor shortages by streamlining operations.

Sustainability and environmental compliance are increasingly shaping market strategies. In 2024, over 65 percent of European metal casting facilities reported using recycled materials as their primary feedstock, aligning with EU Green Deal policies. During the same year, the U.S. also witnessed a 12 percent increase in ferrous scrap recycling for casting applications. As environmental awareness grows and regulatory frameworks tighten, the demand for cast products made through eco-friendly practices is rising. These developments position metal casting as a key enabler of circular manufacturing systems while maintaining economic viability.

Market Dynamics

The metal casting market is growing as industries such as automotive, construction, machinery, and aerospace continue to require durable and cost-effective metal components. Rising infrastructure development and manufacturing activities are increasing the demand for cast parts across a wide range of applications. Advancements in casting technologies are helping manufacturers improve product quality and production efficiency. However, fluctuations in raw material prices and increasing environmental regulations continue to pose challenges for market participants.

The metal casting market is being driven by the automotive industry's growing focus on lightweight vehicle manufacturing and production efficiency. Automakers are increasingly using large aluminum cast components to reduce vehicle weight, improve fuel economy, and simplify assembly processes. Compared with traditional fabrication methods that require multiple welded parts, metal casting enables the production of complex components as a single piece, reducing material usage, manufacturing time, and overall production costs. As vehicle manufacturers continue to redesign platforms for electric and next-generation vehicles, demand for advanced casting technologies is rising significantly.

A recent example of this trend is the expansion of gigacasting technology across the automotive industry. At the IAA Mobility 2025 event, Volkswagen announced the adoption of gigacasting for several upcoming entry-level electric vehicles, highlighting the industry's growing shift toward large structural castings. Hyundai commenced production using its first 9,000-ton Giga Press at its Ulsan facility, supporting its hypercasting strategy for future EV manufacturing. These developments demonstrate how leading automakers are investing in advanced metal casting technologies to improve manufacturing efficiency and reduce vehicle complexity, creating strong growth opportunities for the metal casting market.

The metal casting industry is highly energy-intensive, as foundries rely on melting furnaces, heat-treatment equipment, and automated production systems that consume large amounts of electricity and fuel. Fluctuations in energy prices can significantly increase production costs and put pressure on profit margins, particularly for small and mid-sized foundries. Setting up and modernizing casting facilities requires substantial capital investment in furnaces, molding equipment, automation systems, and environmental compliance technologies. For instance, the Foundry Association of Ukraine in 2025, which reported that electricity prices for foundries had increased by 10-15%. The association noted that electricity accounts for approximately 15-20% of total production costs in foundry operations, making rising power prices a major concern for competitiveness. The increasing cost burden has encouraged foundries worldwide to invest in energy-efficiency initiatives, but high operating and capital costs continue to remain a key restraint for the metal casting market.

The adoption of advanced manufacturing technologies is creating significant opportunities for the metal casting market. Technologies such as 3D sand printing, automated molding systems, and casting simulation software enable foundries to produce complex components with greater precision while reducing production time and material waste. These solutions also help manufacturers respond more quickly to customer requirements and improve overall operational efficiency. As industries such as aerospace, energy, and industrial equipment increasingly require customized and high-performance components, demand for digitally enabled casting processes is expected to grow. An example of this trend was reported by the American Foundry Society in 2025, which highlighted the growing use of 3D sand printing in foundries. For instance, Grede adopted 3D-printed cores to reduce energy consumption, assembly time, and tooling costs while improving casting accuracy. Such advancements demonstrate how digital manufacturing technologies are helping foundries improve efficiency and expand their production capabilities.

Analyst Perspective

The metal casting market is entering a period of transformation as manufacturers focus on producing lighter, stronger, and more complex components for industries such as automotive, industrial machinery, and construction. Demand is being supported by the growing adoption of electric vehicles, ongoing infrastructure development, and increasing investment in advanced manufacturing technologies. The foundries are embracing automation, 3D sand printing, and digital simulation tools to improve efficiency, reduce waste, and enhance product quality. While challenges such as high energy costs, raw material price fluctuations, and environmental regulations continue to impact profitability, they are also encouraging the industry to adopt more sustainable and efficient production methods. In the long term, companies that can balance cost efficiency, technological innovation, and sustainability will be best positioned to strengthen their market presence and capture future growth opportunities.

Material Insights

Based on material, the iron segment led the market with the largest revenue share of 40.0% in 2025. Manufacturers are actively adopting aluminum casting due to its lightweight properties, contributing to fuel efficiency and reduced emissions. As electric vehicle production scales up globally, the need for lightweight structural components such as engine blocks, battery housings, and body panels, is rising, encouraging foundries to expand their aluminum casting capabilities. In addition, improved recyclability and corrosion resistance make aluminum a preferred choice in durable applications with minimal maintenance.

The steel segment in the market is witnessing strong growth due to rising investments in infrastructure, energy, and heavy machinery industries. Steel castings offer high strength, toughness, and wear resistance, making them suitable for structural and load-bearing applications. Growing construction activity across Asia-Pacific, the Middle East, and Africa drives demand for steel components such as girders, beams, and structural connectors. In the energy sector, expanding thermal and renewable power generation capacity is supporting the use of steel castings in turbines, valves, and pressure vessels.

Application Insights

Based on application, the automotive segment led the market with the largest revenue share of 41.0% in 2025, global electric vehicle sales surpassed 17 million units, accounting for over 14 million battery-electric vehicles and plug-in hybrids, marking a robust year-over-year increase of around 26%. This surge elevates EVs to over 14% share of new light-duty vehicles worldwide, with some regions reaching as high as 22% and rising EV sales fuel demand for lightweight, high-precision metal castings used in battery enclosures, motor housings, and chassis components. Advanced casting processes such as high-pressure die casting allow manufacturers to meet electric vehicles' stringent weight and performance standards, deploying optimized alloys and complex geometries.

Industrial is anticipated to register the fastest CAGR over the forecast period. Steel and iron castings remain vital in producing robust components such as gears, pumps, valves, compressor housings, and machinery bases. As global industrial activity grows, driven by infrastructure development, manufacturing modernization, and the expansion of power, oil & gas, and mining industries, foundries are scaling up capacities and adopting efficient production methods like investment casting and automated sand casting. These trends support cost-effective mass production of durable, high-tolerance components required in heavy-duty applications.

Regional Insights

The metal casting industry in North America is growing steadily due to strong demand from the automotive, aerospace, and defense industries. These sectors require high-precision components with complex geometries, which has increased the use of advanced casting techniques such as investment casting and pressure die casting. Automakers focus on lightweight materials like aluminum and magnesium to improve fuel efficiency, supporting non-ferrous metal castings. Rising investments in electric vehicles and hybrid technology have also opened new avenues for casting applications in battery housings, motor parts, and chassis components.

U.S. Metal Casting Market Trends

The metal casting industry in the U.S. is advancing due to growing demand from key sectors such as automotive and aerospace. For example, Ford and General Motors have expanded their use of aluminum castings in EV platforms to reduce vehicle weight and enhance battery efficiency. Tesla’s Gigafactories also utilize giga-casting techniques to produce large vehicle components in a single mold, streamlining production and cutting assembly time. In the aerospace sector, companies like Pratt & Whitney and GE Aerospace rely heavily on investment casting for turbine blades and other engine parts that must withstand extreme temperatures and stress.

Asia Pacific Metal Casting Market Trends

Asia Pacific dominated the metal casting market with the largest revenue share of 56.2% in 2025. As countries such as China, India, and Vietnam continue to invest in infrastructure development and urbanization, the demand for cast metal products such as pipes, valves, engine components, and structural parts has grown significantly. Rapid industrialization and government support for manufacturing under initiatives like "Make in India" and China's "New Infrastructure" strategy have increased the region's foundry activity and capacity expansion.

China Metal Casting Market Trends

The metal casting market in China held the largest share in the Asia Pacific region in 2025.

Europe Metal Casting Market Trends

The metal casting industry in Europe is expanding due to rising demand from automotive, aerospace, and industrial equipment manufacturers. Automakers across Germany, France, and Italy are increasingly adopting lightweight metal castings made from aluminum and magnesium to meet fuel efficiency standards and reduce vehicle emissions. This trend has accelerated with the shift toward electric vehicles, where cast components are used in battery housings, motor parts, and structural frames. Aerospace manufacturers such as Airbus rely on high-precision investment casting for engine components and airframe structures, supporting the growth of specialized foundries across the region.

Latin America Metal Casting Market Trends

The metal casting industry in Latin America is expanding due to increasing industrial activity and infrastructure development across Brazil, Argentina, and Mexico. Construction of roads, bridges, railways, and urban infrastructure has boosted the demand for cast iron and steel components used in structural frameworks, drainage systems, and heavy machinery. Brazil dominates the regional casting landscape with a strong base of iron foundries, driven by its large construction and manufacturing sectors. On the other hand, Argentina is seeing growing investment in automotive manufacturing, which supports engine blocks, chassis parts, and transmission housings made through casting.

Middle East & Africa Metal Casting Market Trends

The metal casting industry in the Middle East and Africa is evolving with significant developments across sectors such as oil and gas, construction, automotive, and power generation. In the Gulf countries, especially Saudi Arabia and the UAE, large-scale infrastructure and energy projects are increasing the demand for cast components used in pipelines, pumps, valves, and heat exchangers. These countries are investing in foundry upgrades to produce corrosion-resistant and high-strength castings suited for high-temperature and high-pressure applications in oil and gas. In addition, ongoing refinery expansions and petrochemical plant developments require reliable casting inputs for complex machinery.

Key Metal Casting Company Insights

Some of the key players operating in the market include Alcast Technologies Ltd., Calmet Inc. and others

-

Alcast Technologies Ltd. is a Canada-based company headquartered in Hamilton, Ontario, known for its expertise in high-quality aluminum and zinc die casting. Established in 1994, the company serves various industries including automotive, aerospace, lighting, and electronics. Alcast is equipped with advanced vertical and horizontal die casting machines, which allow for the production of precision components with complex geometries. Alcast specializes in high-pressure aluminum and zinc components in metal castings, often using alloys such as A380, A383, and ZA-12.

-

Calmet Inc. is an international manufacturing and supply company that provides metal castings and precision machined parts to clients across North America and Europe. With manufacturing facilities based in India and China, Calmet offers ferrous and non-ferrous castings, catering to automotive, hydraulics, agriculture, power transmission, and heavy equipment industries. Calmet’s casting offerings include grey iron, ductile iron, malleable iron, steel, aluminum, brass, and bronze. The company provides services such as heat treatment, CNC machining, galvanizing, electroplating, and painting to enhance the performance and durability of its cast components.

Key Metal Casting Companies:

The following are the leading companies in the metal casting market. These companies collectively hold the largest market share and dictate industry trends.

- Alcast Technologies Ltd.

- Ahresty Corporation

- Calmet Inc

- Dynacast Ltd

- Endurance Technologies Limited

- GF Casting Solutions (Georg Fischer AG)

- MES, Inc. (Metrics Holdings)

- Proterial, Ltd

- Rheinmetall AG

- Ryobi Limited

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Ahresty Corporation; Dynacast; GF Casting Solutions; Proterial, Ltd.; Rheinmetall AG; Ryobi Limited)

- Invest heavily in automation, robotics, and smart foundry technologies to improve productivity.

- Focus on long-term supply agreements with major automotive OEMs and industrial customers.

- Expand production capacity through new facilities and technology upgrades.

- Strong brand reputation and established customer relationships.

- Large-scale production capabilities resulting in lower per-unit costs.

- Access to advanced technologies and proprietary manufacturing processes.

- High operating and maintenance costs due to large manufacturing facilities.

- Significant exposure to fluctuations in automotive production cycles.

- Longer decision-making processes due to complex organizational structures.

Emerging Players (Alcast Technologies Ltd.; CALMET; Endurance Technologies Limited; MES, Inc.)

- Focus on niche casting applications and customized component manufacturing.

- Compete through cost-efficient production and flexible manufacturing processes.

- Expand presence in regional and developing markets.

- Greater flexibility in adapting to customer requirements.

- Faster decision-making and quicker implementation of operational changes.

- Lower overhead and administrative costs.

- Limited global presence and brand recognition.

- Smaller production capacities compared to industry leaders.

- Lower bargaining power with raw material suppliers.

Recent Development

-

In November 2024, CFS Foundry announced the launch of advanced metal casting and CNC machining services, elevating its capabilities to produce high-quality, precision-engineered metal components for various industries. The company specializes in diverse casting techniques, including die casting, investment casting, and stainless steel casting, leveraging state-of-the-art facilities and strict quality assurance protocols. Focusing on innovation and customer satisfaction, CFS Foundry integrates CNC machining into its processes, ensuring components meet precise specifications and are delivered as ready-to-use solutions.

Metal Casting Market Report Scope

Report Attribute

Details

Market size in 2025

USD 290.2 billion

Estimated Market size in 2026

USD 403.7 billion

Projected Market size by 2033

USD 408.3 billion

Growth rate

CAGR of 4.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD Million, Volume in Kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, volume forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; France; Italy; Spain; China; India; Japan; South Korea; Brazil

Key companies profiled

Alcast Technologies Ltd; Ahresty Corporation; CALMET; Dynacast; Endurance Technologies Limited; GF Casting Solutions; MES, Inc.; Proterial, Ltd.; Rheinmetall AG; Ryobi Limited

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Metal Casting Market Report Segmentation

This report forecasts revenue and volume growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global metal casting market report based on material, application, and region.

-

Material Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Iron

-

Steel

-

Aluminum

-

Others

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Automotive

-

Industrial

-

Building & Construction

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

Spain

-

Italy

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Research Methodology

Segment Definition

Segment - Material

Revenue capture definition

Iron

Revenue is generated from the production and sale of cast components manufactured using various iron grades, including gray iron, ductile iron, white iron, malleable iron, and compacted graphite iron, for applications across automotive, industrial, and construction sectors.

Steel

Market revenue is derived from the manufacturing and consumption of steel castings made from carbon steel, alloy steel, stainless steel, and other specialty steel grades used in demanding industrial, energy, transportation, and infrastructure applications.

Aluminum

Revenue is captured through the production and utilization of aluminum castings made from various aluminum alloys for lightweight, corrosion-resistant, and high-performance components, particularly in automotive, aerospace, industrial, and consumer applications.

Others

This segment generates revenue from cast components manufactured using metals and alloys other than iron, steel, and aluminum, including magnesium, zinc, copper, bronze, and brass alloys used across specialized industrial and engineering applications.

Segment - Application

Revenue capture definition

Automotive

Revenue is generated through the demand for metal cast components used in passenger vehicles, commercial vehicles, electric vehicles, railways, aerospace, marine vessels, and other transportation equipment, including engine, transmission, chassis, and structural parts.

Industrial

Market value is derived from the use of metal castings in industrial machinery and equipment across sectors such as mining, oil & gas, chemicals, agriculture, power generation, food processing, healthcare, and manufacturing.

Building & Construction

Revenue is captured from the consumption of metal castings in residential, commercial, and infrastructure projects, including pipes, fittings, valves, structural components, and construction equipment parts.

Others

This segment generates revenue from metal casting applications in industries such as electrical & electronics, telecommunications, consumer appliances, defense, and other niche end-use sectors requiring precision-engineered cast components.

Estimation Model

Layer Name

Key Question

Description

End-Use Industry Analysis

Where does demand originate?

This stage evaluates manufacturing activity and infrastructure development across key end-use sectors such as automotive, industrial, building & construction, and others. Industry production trends, capital investments, and equipment demand are analyzed to identify the primary sources of demand for metal cast components. The analysis helps determine the overall addressable market for metal castings.

Cast Component Assessment

Which components require metal castings?

This stage identifies the components that are commonly manufactured through casting processes across different industries. Demand is assessed for products such as engine blocks, transmission housings, pumps, valves, pipes, fittings, and structural components. Component production volumes are then mapped to their respective end-use applications to estimate casting demand.

Material Consumption Analysis

How much casting material is consumed?

The estimated demand for cast components is translated into material consumption across iron, steel, aluminum, and other alloy castings. Material selection is evaluated based on application requirements, performance characteristics, and industry preferences. This step quantifies the total casting volume consumed by material type and application segment.

Revenue Estimation

How much market revenue is generated?

The calculated casting volumes are converted into market revenue using average selling prices across different materials and applications. Pricing analysis considers factors such as alloy type, casting complexity, production process, and regional market dynamics. The aggregated revenue estimates are used to determine the overall market size and forecast growth.

Delivered Customizations

Client Request

Customization Delivered

Value Adds

Raw Material Pricing Analysis

Conducted a detailed assessment of key raw materials used in metal casting, including iron, steel, aluminum, magnesium, zinc, and copper alloys, covering price trends, supply-demand dynamics, trade flows, and sourcing risks across major regions.

Helps stakeholders understand cost drivers, evaluate procurement risks, and develop sourcing strategies to improve profitability and supply chain resilience.

Growth Opportunity Assessment

Conducted a comprehensive assessment of emerging growth opportunities across electric vehicles, renewable energy infrastructure, industrial automation, aerospace, and advanced manufacturing applications. The analysis included demand outlook, technology adoption trends, investment activity, and market attractiveness across key regions.

Helps stakeholders identify high-growth application areas, prioritize investment opportunities, and develop long-term expansion strategies in rapidly evolving end-use sectors.

Global Trade Flow & Import-Export Analysis

Evaluated international trade patterns for metal castings and casting materials, including import-export volumes, key trading countries, tariff structures, supply chain dependencies, and regional manufacturing competitiveness.

Enables stakeholders to understand trade dynamics, assess supply chain risks, identify export opportunities, and make informed sourcing and market-entry decisions across global markets.

Frequently Asked Questions About This Report

The metal casting market is primarily driven by rising demand from the automotive, industrial, and construction sectors, along with increasing infrastructure and manufacturing activities worldwide. The growing adoption of lightweight materials and advanced casting technologies is further supporting market growth.

The metal casting market size was estimated at USD 290.2 billion in 2025 and is expected to reach USD 303.7 billion in 2026.

The metal casting market is expected to grow at a compound annual growth rate of 4.3% from 2026 to 2033 to reach USD 408.3 billion by 2033.

Based on material, iron accounted for largest revenue share of 40.0% in 2025.

The key players operating in the metal casting market are Alcast Technologies Ltd; Ahresty Corporation; CALMET; Dynacast; Endurance Technologies Limited; GF Casting Solutions; MES, Inc.; Proterial, Ltd.; Rheinmetall AG; Ryobi Limited, and others.

Asia Pacific dominated the market with revenue share of 56.2% in 2025.

China dominated the Asian market with revenue share of 53.7% in 2025.

Asia Pacific is anticipated to register the fastest CAGR of 4.8% over the forecast period.

Based on application, automotive accounted for largest revenue share of 41.0% in 2025.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.