- Home

- »

- Drilling & Extraction Equipments

- »

-

Mining Chemicals Market Size, Growth Report, 2026-2033GVR Report cover

![Mining Chemicals Market (2026 - 2033)Report]()

Mining Chemicals Market (2026 - 2033)

Size, Share & Trends Analysis Report By Ore Type (Powder Gold, Iron, Copper, Phosphate), By Application (Mineral Processing, Explosives & Drilling, Water Treatment), By Region, And Segment Forecasts

Market Size, 2025

$12.9BMarket Estimate, 2026

$13.8BMarket Forecast, 2033

$23.2BCAGR, 2026–2033

7.7%Mining Chemicals Market Summary

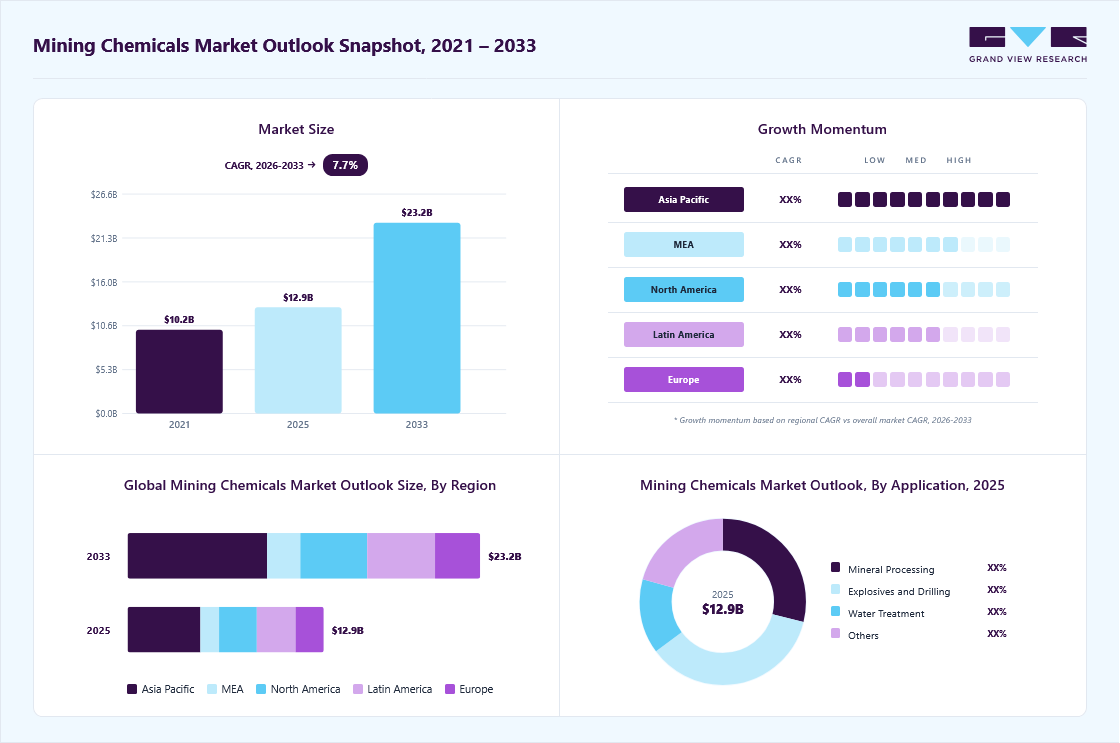

The global mining chemicals market size was valued at USD 12.9 billion in 2025 and is projected to grow from USD 13.8 billion in 2026 to USD 23.2 billion by 2033, at a CAGR of 7.7% from 2026 to 2033. Asia Pacific dominated the global market, accounting for the largest revenue share of 37.1% in 2025. The global shift toward electric vehicles, renewable energy, and advanced electronics is driving higher demand for critical metals such as lithium, copper, and cobalt.

Key Market Trends & Insights

- By ore type: Iron dominated the market, accounting for a revenue share of 19.0%.

- By application: Explosives and drilling dominated the global mining chemicals market, accounting for a 35.9% revenue share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (37.1% revenue share, 2025)

- By country: The China mining chemicals industry is a major contributor to the global market.

Market Size & Forecast

- Market size in 2025: USD 12.9 Billion

- Estimated market size in 2026: USD 13.8 Billion

- Projected market size by 2033: USD 23.2 Billion

- CAGR (2026-2033): 7.7%

To efficiently extract these minerals, mining operations are increasingly relying on flotation reagents, leaching agents, and solvent extractants. This surge in mining activity directly boosts the consumption of mining chemicals, making it a key market driver. Mining companies are under pressure to improve operational efficiency while adhering to strict environmental regulations. This is encouraging the adoption of high-performance, eco-friendly, and water-efficient chemical solutions that enhance ore recovery and minimize waste. The focus on sustainable mineral processing is driving innovation and demand within the market.

")

Growing exploration in untapped mineral-rich regions and increasing investments in sustainable mining technologies present an opportunity for mining chemical suppliers to expand their presence, introduce innovative solutions, and capture long-term contracts with emerging mining operations.

Market Concentration & Characteristics

The mining chemicals industry is moderately consolidated, with global leaders and regional players shaping the competitive landscape. Within the market, the mining flotation chemicals market and mining dust suppression chemicals market represent key segments, driven by demand for efficient mineral recovery and environmentally compliant operations. Leading companies leverage extensive product portfolios, technical expertise, and robust supply chains, while smaller or regional players focus on niche solutions and specialized applications to capture market share.

The market exhibits strong demand for advanced chemical solutions that optimize ore processing, enhance dust control, and improve overall operational efficiency. Major players capitalize on research and development, strategic partnerships, and global distribution networks to deliver tailored solutions, while emerging suppliers target niche applications within flotation and dust suppression chemicals, reflecting a sector characterized by technical complexity, steady growth, and high entry barriers.

Ore Type Insights

Iron segment holds a dominant position with a revenue market share of 19.0% in 2025, due to sustained demand for steel across construction, automotive, and infrastructure sectors. High-volume extraction and processing of iron ore require extensive use of flotation reagents, grinding aids, and processing chemicals to improve yield and operational efficiency. Growing urbanization and industrial activity globally continue to drive steady consumption of mining chemicals in this segment.

The phosphate segment is witnessing market growth with a CAGR revenue of 7.8% during the forecast period, driven by rising demand for fertilizers and agricultural productivity. Within this, the mining flotation chemicals market and mining dust suppression chemicals market play a key role, as efficient phosphate extraction and beneficiation rely on specialized flotation chemicals and separation reagents. Expansion of agricultural activities, particularly in emerging economies, is further accelerating the consumption of mining chemicals in this segment.

Application Insights

Explosives and drilling hold a dominant position in the global market with a revenue share of 35.9% in 2025, due to its critical role in mineral extraction and mine development. High demand for efficient drilling and blasting operations across large-scale mining projects drives consistent consumption of specialized chemicals, supporting operational productivity and process reliability.

Water treatment is witnessing significant growth in the global market with a revenue CAGR of 7.9% during the forecast period, as mining companies prioritize sustainable operations and regulatory compliance. Increasing focus on treating process water, reducing environmental impact, and recycling water within mining operations is driving demand for advanced chemical solutions in this application.

Regional Insights

Asia Pacific held the largest revenue share of 37.1% in 2025, supported by large-scale mining operations and strong demand for coal, iron ore, copper, and rare earth elements. Rapid industrialization, urban infrastructure development, and the region’s central role in battery and renewable energy supply chains are driving mineral extraction activities.

China Mining Chemicals Market Trends

The mining chemicals market in China is driven by its dominant position in mineral production and processing, particularly in coal, rare earth elements, and base metals. Strong domestic demand, extensive refining capacity for battery materials, and continued investments in mining assets are supporting high consumption of mineral processing chemicals. The government's focus on resource security and industrial output further strengthens market growth.

Europe Mining Chemicals Market Trends

The mining chemicals market in Europe is influenced by its strong regulatory framework and focuses on reducing dependence on imported raw materials. The region is witnessing increased investments in sustainable mining, recycling, and secondary resource recovery, which is driving demand for advanced and environmentally compliant mining chemicals. Innovation in bio-based reagents and low-toxicity formulations is also gaining traction.

Germany mining chemicals market demand for mining chemicals is influenced by its focus on raw material security and advanced manufacturing needs. Investments in battery material processing, recycling technologies, and sustainable resource utilization are driving the use of high-performance specialty chemicals.

North America Mining Chemicals Market Trends

The mining chemicals market in North America is driven by increasing efforts to strengthen domestic supply chains for critical minerals such as lithium, cobalt, and nickel. Government-backed incentives, rising investments in clean energy and electric vehicle infrastructure, and renewed mining exploration are supporting demand for high-performance and sustainable chemical solutions.

The U.S. mining chemicals market is supported by increasing emphasis on securing domestic sources of critical minerals essential for clean energy, electronics, and defense sectors. Rising investments in mining exploration, coupled with federal support for infrastructure and energy transition, are driving demand for advanced mining chemicals. The shift toward sustainable and efficient extraction technologies is also contributing to market expansion.

Latin America Mining Chemicals Market Trends

The mining chemicals market in Latin America is driven by its vast reserves of copper, lithium, iron ore, and precious metals. The region plays a critical role in global copper and lithium supply chains, with ongoing investments in large-scale mining projects and capacity expansions. Growing exploration activities and supportive regulatory frameworks in key countries are sustaining long-term demand for flotation reagents and extraction chemicals.

Middle East & Africa Mining Chemicals Market Trends

The mining chemicals market in the Middle East & Africa region is experiencing notable growth due to expanding mining activities, particularly across resource-rich African nations. Increasing foreign investments, infrastructure development, and exploration of untapped reserves such as gold, copper, and diamonds are fueling demand for mineral processing chemicals. The gradual formalization and modernization of mining operations are further supporting market expansion.

Key Mining Chemicals Company Insights

Key mining chemicals companies are focusing on developing high-performance and sustainable reagents to improve mineral recovery and meet environmental standards. Strategic partnerships, innovation, and expansion into emerging mining regions are helping players strengthen market presence and secure long-term contracts.

-

BASF SE operates in the market with a diversified portfolio of mineral processing solutions, including flotation reagents, solvent extractants, and performance chemicals. The company emphasizes innovation and sustainable product development to improve ore recovery rates, optimize processing efficiency, and align with environmental regulations. Its global manufacturing footprint and integrated value chain support consistent supply to mining operations across key regions.

-

Ashland participates in the market through its range of specialty additives and performance solutions designed for mineral processing applications. The company focuses on customized formulations that enhance separation efficiency, reduce water usage, and improve overall process performance. Its emphasis on specialty chemistry and application-driven innovation supports its presence in targeted and high-value mining segments.

Key Mining Chemicals Companies:

The following key companies have been profiled for this study on the mining chemicals market

- BASF SE

- Ashland

- Dow

- Cytec Solvay Group (Solvay)

- Arkema

- Clariant

- Kemira

- Shell Chemicals

- Quaker Chemical Corporation

- Akzo Nobel N.V.

- Solenis

- The Sherwin-Williams Company

- AECI Ltd.

Recent Developments

-

In June 2025, BASF SE announced a strategic collaboration with FUCHS to strengthen its mining chemicals business in Australia. The partnership combines BASF’s advanced flotation and mineral processing chemistries with FUCHS’ strong regional distribution and technical service capabilities. This collaboration is aimed at delivering tailored chemical solutions, improving process efficiency, and enhancing customer engagement in the Australian mining sector.

-

In October 2023, BASF SE introduced a new range of eco-friendly flotation reagents designed to improve metal recovery while reducing environmental impact in copper and gold mining operations. The development reflects the industry’s shift toward sustainable and low-toxicity mining chemical solutions aligned with stricter environmental standards.

Mining Chemicals Market Report Scope

Report Attribute

Details

Market size in 2025

USD 12.9 billion

Estimated Market size in 2026

USD 13.8 billion

Projected Market size by 2033

USD 23.2 billion

Growth rate

CAGR of 7.7% from 2026 to 2033

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Volume in kilotons, revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, volume forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Ore type, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Spain; Russia; Italy; China; India; Japan; South Korea; Brazil: Argentina; Peru; Chile; Colombia; Saudi Arabia; Africa; South Africa; Ghana; Morocco; DRC; Zambia; Zimbabwe; Tanzania; Mali; Ivory Coast; Sudan

Key companies profiled

BASF SE; Ashland; Dow; Cytec Solvay Group (Solvay); Arkema; Clariant; Kemira; Shell Chemicals; Quaker Chemical Corporation; Akzo Nobel N.V.; Solenis; The Sherwin-Williams Company; AECI Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Mining Chemicals Market Report Segmentation

This report forecasts volume & revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global mining chemicals market report based on ore type, application, and region:

-

Ore Type Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Powder Gold

-

Collectors

-

Coatings

-

Flocculants

-

Grinding Aids

-

Solvent Extractants

-

Dust Suppressants

-

Defoamers

-

Antiscalants

-

Biocides

-

Lubricants

-

Frothers

-

Others

-

-

Iron

-

Collectors

-

Coatings

-

Flocculants

-

Grinding Aids

-

Solvent Extractants

-

Dust Suppressants

-

Defoamers

-

Antiscalants

-

Biocides

-

Lubricants

-

Frothers

-

Others

-

-

Copper

-

Collectors

-

Coatings

-

Flocculants

-

Grinding Aids

-

Solvent Extractants

-

Dust Suppressants

-

Defoamers

-

Antiscalants

-

Biocides

-

Lubricants

-

Frothers

-

Others

-

-

Phosphate

-

Collectors

-

Coatings

-

Flocculants

-

Grinding Aids

-

Solvent Extractants

-

Dust Suppressants

-

Defoamers

-

Antiscalants

-

Biocides

-

Lubricants

-

Frothers

-

Others

-

-

Others

-

Collectors

-

Coatings

-

Flocculants

-

Grinding Aids

-

Solvent Extractants

-

Dust Suppressants

-

Defoamers

-

Antiscalants

-

Biocides

-

Lubricants

-

Frothers

-

Others

-

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Mineral Processing

-

Explosives and Drilling

-

Water Treatment

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Russia

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

Peru

-

Chile

-

Colombia

-

Argentina

-

-

Middle East and Africa

-

Saudi Arabia

-

South Africa

-

Ghana

-

Morocco

-

DRC

-

Zambia

-

Zimbabwe

-

Tanzania

-

Mali

-

Ivory Coast

-

Sudan

-

-

Frequently Asked Questions About This Report

The iron segment dominated the market and accounted for the largest revenue share of 19.0% in 2025.

The explosives and drilling segment led with a 35.9% revenue share in 2025.

Key players include BASF SE; Ashland; Dow; Cytec Solvay Group (Solvay); Arkema; Clariant; Kemira; Shell Chemicals; Quaker Chemical Corporation; Akzo Nobel N.V.; Solenis; The Sherwin-Williams Company; AECI Ltd.

The global mining chemicals market size was valued at USD 12.9 billion in 2025 and is estimated at USD 13.8 billion for 2026.

The global mining chemicals market is expected to grow at a CAGR of 7.7% from 2026 to 2033, reaching USD 23.2 billion by 2033.

Asia Pacific held the largest revenue share of 37.1% in 2025, supported by large-scale mining operations and strong demand for coal, iron ore, copper, and rare earth elements. Rapid industrialization, urban infrastructure development, and the region’s central role in battery and renewable energy supply chains are driving mineral extraction activities.

The global shift toward electric vehicles, renewable energy, and advanced electronics is driving higher demand for critical metals such as lithium, copper, and cobalt. To efficiently extract these minerals, mining operations are increasingly relying on flotation reagents, leaching agents, and solvent extractants. This surge in mining activity directly boosts the consumption of mining chemicals, making it a key growth driver for the market.

About the Author(s)

Drilling & Extraction Equipments Research Team

Bulk Chemicals · Drilling & Extraction EquipmentsThis report was authored by the drilling & extraction equipments research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the drilling & extraction equipments segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.