- Home

- »

- Advanced Interior Materials

- »

-

Nitrogen Oxide Control Systems Market Size Report, 2033GVR Report cover

![Nitrogen Oxide Control Systems Market Size, Share & Trends Report]()

Nitrogen Oxide Control Systems Market (2026 - 2033) Size, Share & Trends Analysis Report By Technology (Selective Catalytic Reduction, Selective Non-Catalytic Reduction, Low NOx Burners), By End Use (Power Generation, Chemical), By Region, And Segment Forecasts

Market Size, 2025

$7.5BMarket Estimate, 2026

$7.7BMarket Forecast, 2033

$11.7BCAGR, 2026–2033

6.1%Nitrogen Oxide Control Systems Market Summary

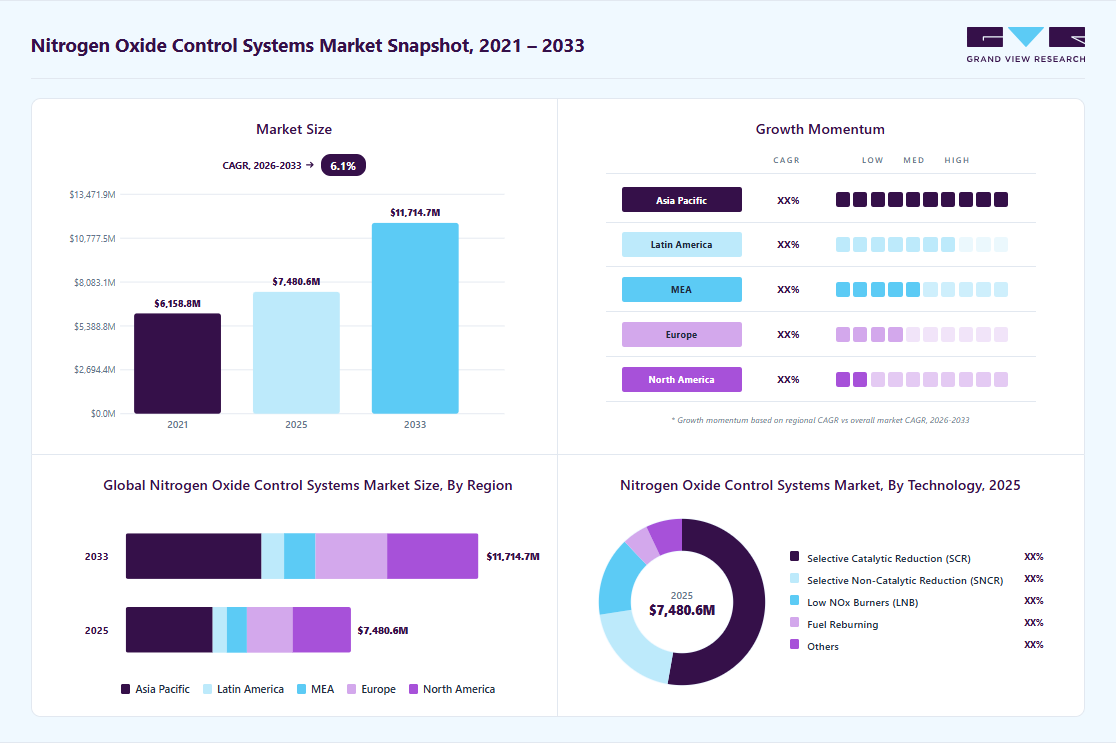

The global nitrogen oxide control systems market size was valued at USD 7.5 billion in 2025 and is projected to grow from USD 7.7 billion in 2026 to USD 11.7 billion by 2033, at a CAGR of 6.1% from 2026 to 2033. Asia Pacific held the dominating position in the global nitrogen oxide control systems market with 35.7% share in 2025. The market is growing due to increasing environmental concerns and stricter emission regulations across industrial sectors.

Key Market Trends & Insights

- By technology: Selective Non-Catalytic Reduction (SNCR) segment is projected to grow at 5.7% CAGR during the forecast period.

- By end use: Power generation segment dominated the market in 2025, holding 33.1% market share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (35.7% revenue share, 2025)

- By country: The China nitrogen oxide control systems industry is a major contributor to the global market.

Market Size & Forecast

- Market size in 2025: USD 7.5 Billion

- Estimated market size in 2026: USD 7.7 Billion

- Projected market size by 2033: USD 11.7 Billion

- CAGR (2026-2033): 6.1%

Governments are implementing limits on nitrogen oxide emissions from power plants, manufacturing facilities, and transportation sources to reduce air pollution and improve public health. Industries are adopting technologies such as selective catalytic reduction (SCR) and selective non-catalytic reduction (SNCR) systems to meet compliance requirements.")

Growth in power generation, cement production, and chemical manufacturing is also supporting the demand for NOx control solutions. Increasing industrialization in emerging economies, particularly in Asia Pacific, is further driving demand for emission control solutions. Additionally, retrofitting of existing plants with advanced NOx control technologies is gaining traction as industries seek cost-effective ways to meet tightening environmental norms.

Market Concentration & Characteristics

The nitrogen oxide control systems industry is moderately fragmented, with the presence of several global engineering firms along with regional equipment manufacturers and service providers. Companies offer a range of technologies such as selective catalytic reduction (SCR) and selective non-catalytic reduction (SNCR) systems. Differences in project requirements, plant sizes, and regional emission standards encourage participation from multiple vendors, resulting in varied product offerings and competitive market conditions across industries.

Advancements focus on improving catalyst performance, optimizing reagent use, and integrating digital monitoring systems. Manufacturers are also developing compact and energy-efficient designs suitable for retrofitting existing facilities, supporting better compliance and improved environmental performance across industrial operations.

Merger and acquisition activities in the industry are increasing as companies seek to expand technical capabilities and strengthen market presence. Larger engineering firms are acquiring specialized emission control technology providers to enhance their product portfolios. These strategic activities support access to new geographic markets, improve project delivery capacity, and enable companies to provide integrated air pollution control solutions across various industrial sectors.

Regulations play a major role in shaping the industry by setting strict emission limits for industries such as power generation, cement, and manufacturing. Environmental authorities require facilities to install approved emission control technologies to meet air quality standards. Continuous tightening of emission norms encourages plant operators to upgrade existing systems and adopt advanced nitrogen oxide control solutions, supporting steady market demand.

Drivers, Opportunities & Restraints

Enforcement of stringent air emission regulations across industrial sectors is fueling the market. Governments are introducing strict limits on nitrogen oxide emissions from power plants, cement kilns, and manufacturing facilities. To comply with these standards, industries are installing advanced control technologies such as selective catalytic reduction and selective non-catalytic reduction systems, increasing overall demand for effective emission control solutions.

Modernization and retrofitting of aging industrial facilities are creating significant opportunities in the market. Many existing power plants and manufacturing units require upgrades to meet updated emission standards. This creates demand for advanced and compact nitrogen oxide control technologies that can be integrated into existing systems. Growth in developing regions with expanding industrial bases also presents opportunities for new installations and system upgrades.

A major challenge in the industry is the high installation and operational costs associated with advanced emission control technologies. Systems such as selective catalytic reduction require significant capital investment and ongoing maintenance, including catalyst replacement and reagent supply. Smaller facilities may face budget constraints, limiting adoption. Additionally, the complexity of integrating these systems into existing infrastructure can increase project timelines and operational difficulties.

Technology Insights

The Selective Catalytic Reduction (SCR) segment held the dominant share in the market and accounted for a share of 52.8% in 2025, due to its high efficiency in reducing nitrogen oxide emissions. Industries such as power generation, cement, and chemicals are increasingly adopting SCR systems to meet strict emission standards. Continuous upgrades of large industrial facilities and power plants are further supporting demand for SCR technology.

The growth of the Selective Non-Catalytic Reduction (SNCR) segment is primarily driven by its lower installation cost and simpler design compared to catalytic systems. It is commonly used in medium-scale industrial plants such as waste incineration and cement production. Increasing demand for cost-effective emission control solutions and compliance with regulatory requirements is supporting the adoption of SNCR technology across various industries.

End Use Insights

The power generation segment dominated the market in 2025 due to strict emission limits on coal- and gas-fired power plants. Utilities are upgrading existing plants with advanced control technologies to comply with environmental standards. Increasing electricity demand and the continued operation of thermal power facilities are supporting the adoption of nitrogen oxide reduction systems.

The chemical segment is expected to grow at 7.5% CAGR during the forecast period as chemical manufacturing processes generate nitrogen oxide emissions. Companies are adopting emission control technologies to meet environmental regulations and improve operational safety. Expansion of chemical production facilities and modernization of existing plants are contributing to the increasing demand for nitrogen oxide control systems within this sector.

Regional Insights

North America nitrogen oxide control systems market is experiencing steady growth due to strict emission regulations and the presence of established industrial and power generation sectors. Aging power plants are undergoing upgrades to meet updated environmental standards. Investments in cleaner technologies and modernization of industrial facilities are supporting the installation of advanced nitrogen oxide reduction systems across various applications.

U.S. Nitrogen Oxide Control Systems Market Trends

The nitrogen oxide control systems market in the U.S. is expanding due to the enforcement of federal and state emission standards. Power generation, cement, and manufacturing industries are investing in emission control technologies to comply with environmental policies. Retrofitting older facilities and increasing demand for cleaner energy production methods are contributing to the steady adoption of nitrogen oxide control technologies.

Mexico nitrogen oxide control systems market is growing significantly due to expanding industrial activities and increased focus on environmental protection. Government initiatives to improve air quality are encouraging industries to adopt emission control technologies. Growth in power generation and cement production sectors is also contributing to rising demand for nitrogen oxide reduction systems across industrial facilities.

Europe Nitrogen Oxide Control Systems Market Trends

The nitrogen oxide control systems market in Europe is driven by strict environmental regulations and a strong focus on reducing air pollution. Industries are upgrading existing plants to meet emission limits set by regional authorities. Continuous investments in sustainable industrial operations and advanced pollution control technologies are supporting the widespread adoption of nitrogen oxide control systems across multiple industrial sectors.

Germany nitrogen oxide control systems market is witnessing stable growth, supported by its strong industrial base and strict emission control policies. The country’s focus on reducing industrial pollution is encouraging companies to install advanced nitrogen oxide reduction technologies. Ongoing modernization of power plants and manufacturing facilities is contributing to consistent demand for emission control systems across various industries.

The nitrogen oxide control systems market in the UK is driven by stringent environmental standards and increased attention to air quality improvement. Industrial facilities and power plants are adopting advanced emission control technologies to comply with regulatory requirements. Investments in sustainable industrial practices and modernization of existing infrastructure are supporting continued adoption of nitrogen oxide control solutions.

Asia Pacific Nitrogen Oxide Control Systems Market Trends

The nitrogen oxide control systems market in Asia Pacific is driven by rapid industrialization, expanding power generation capacity, and increasingly stringent environmental regulations. Countries such as China, India, Japan, and South Korea are witnessing significant demand for NOx reduction technologies across sectors, including power generation, cement, chemicals, and refining, where emissions from high-temperature combustion processes are substantial.

China nitrogen oxide control systems market is experiencing strong growth due to strict pollution control measures and the expansion of industrial production. Government initiatives to reduce air pollution are encouraging industries to install advanced emission control systems. Continuous investments in power generation and heavy industries are supporting the demand for nitrogen oxide reduction technologies across large-scale industrial operations.

The nitrogen oxide control systems market in India is driven by the rising industrialization and increasing electricity demand. Government regulations aimed at improving air quality are encouraging power plants and manufacturing industries to adopt emission control technologies. Expansion of thermal power plants and growing industrial activities are supporting the steady installation of nitrogen oxide control systems across key sectors.

Middle East & Africa Nitrogen Oxide Control Systems Market Trends

The nitrogen oxide control systems market in the Middle East & Africa (MEA) is witnessing gradual growth, supported by expanding industrial activities and increasing focus on environmental sustainability. Key demand is driven by sectors such as power generation, oil & gas, cement, and petrochemicals, where combustion processes contribute significantly to NOx emissions. Countries in the Gulf Cooperation Council (GCC), including Saudi Arabia and the UAE, are increasingly implementing emission control regulations and investing in cleaner and more efficient industrial technologies.

Saudi Arabia nitrogen oxide control systems market is experiencing steady growth due to the expansion of oil refining, petrochemical, and power generation industries. Government initiatives aimed at environmental sustainability are encouraging industries to adopt emission reduction technologies. Investments in new industrial projects and the modernization of existing facilities are supporting the demand for nitrogen oxide control systems across key industrial sectors.

Latin America Nitrogen Oxide Control Systems Market Trends

The nitrogen oxide control system market in Latin America is expected to grow at 6.4% CAGR during the forecast period due to increasing industrial development and rising environmental awareness. Governments are introducing stricter emission regulations to control air pollution. Growth in cement production, power generation, and manufacturing sectors is contributing to the adoption of nitrogen oxide control technologies across industrial facilities.

Brazil nitrogen oxide control system market is growing due to the expansion of the industrial and energy sectors. Increasing focus on environmental compliance and air quality improvement is encouraging industries to install emission control systems. Investments in power generation and cement manufacturing facilities are supporting the adoption of nitrogen oxide reduction technologies across various industrial applications.

Key Nitrogen Oxide Control Systems Companies Insights

Some of the key players operating in the nitrogen oxide control system market include Honeywell International, Mitsubishi Heavy Industries, Ltd., BASF SE, Kanadevia Corporation Holding A/S, and Haldor Topsoe A/S

-

Honeywell International Inc. is a U.S.-based technology and manufacturing company that provides industrial automation and environmental control solutions. The company offers emission control technologies, including systems used for nitrogen oxide reduction in industrial and energy applications. Its solutions support regulatory compliance, operational efficiency, and improved environmental performance across multiple industries.

-

Mitsubishi Heavy Industries, Ltd. is a Japan-based engineering company providing air pollution control and emission reduction systems. The company supplies nitrogen oxide control technologies, including selective catalytic reduction systems, for power plants and industrial facilities. Its solutions support improved air quality, regulatory compliance, and efficient operation across energy, manufacturing, and heavy industrial sectors.

Key Nitrogen Oxide Control Systems Companies:

The following key companies have been profiled for this study on the nitrogen oxide control systems market

- Honeywell International

- Mitsubishi Heavy Industries, Ltd.

- BASF SE

- Babcock & Wilcox Enterprises, Inc.

- Kanadevia Corporation

- Yara International ASA

- GE Vernova

- CECO Environmental

- Fuel Tech, Inc.

- Ducon Environmental Systems, Inc.

- ANDRITZ AG

- Haldor Topsoe A/S

- Tri-Mer Corporation

- Umicore

- Valmet

Recent Developments

-

In February 2026, Honeywell entered into an amended agreement to acquire Johnson Matthey’s Catalyst Technologies business to strengthen its capabilities in emission control and sustainable technologies. The acquisition is intended to expand Honeywell’s portfolio in catalyst solutions used for industrial and environmental applications, supporting compliance with emission regulations and enhancing its presence in advanced pollution control technologies.

-

In December 2025, GEA Group showcased its advanced NOx Separator at Marintec China 2025, designed to support cleaner marine operations by reducing nitrogen oxide emissions through integration with exhaust gas recirculation systems. The solution also improves wash water treatment efficiency, ensuring reliable performance under demanding conditions while helping vessels meet strict IMO Tier III standards.

Nitrogen Oxide Control Systems Market Report Scope

Report Attribute

Details

Market size in 2025

USD 7.5 billion

Market size value in 2026

USD 7.7 billion

Revenue forecast in 2033

USD 11.7 billion

Growth rate

CAGR of 6.1% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Technology, end use, region.

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; China; Japan; India; Australia; South Korea; Brazil; Argentina; UAE; Saudi Arabia; South Africa

Key companies profiled

Honeywell International; Mitsubishi Heavy Industries, Ltd.; BASF SE; Babcock & Wilcox Enterprises, Inc.; Kanadevia Corporation; Yara International ASA; GE Vernova; CECO Environmental; Fuel Tech, Inc.; Ducon Environmental Systems, Inc.; Haldor Topsoe A/S; Tri-Mer Corporation; Umicore.; Valmet; ANDRITZ AG

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Nitrogen Oxide Control Systems Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global nitrogen oxide control systems market report based on technology, end use and region.

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Selective Catalytic Reduction (SCR)

-

Selective Non-Catalytic Reduction (SNCR)

-

Low NOx Burners (LNB)

-

Fuel Reburning

-

Others

-

-

End Use (Revenue, USD Million, 2021 - 2033)

-

Power Generation

-

Chemical

-

Cement

-

Refinery & Petrochemical

-

Pulp & Paper

-

Textile

-

Metals

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

Italy

-

UK

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The global nitrogen oxide control systems market size was valued at USD 7.5 billion in 2025 and is expected to reach USD 7.7 billion in 2026.

The global nitrogen oxide control systems market, in terms of revenue, is expected to grow at a compound annual growth rate of 6.1% from 2026 to 2033 to reach USD 11.7 billion by 2033.

Key factors driving the nitrogen oxide control systems market include stringent environmental regulations, increasing industrialization, expansion of thermal power generation, rising environmental awareness, and growing investments in cleaner emission control technologies.

Asia Pacific dominated with a 35.7% revenue share in 2025.

Selective catalytic reduction segment hold the dominant share in the market and accounted for a share of 52.8% in 2025, due to its high efficiency in reducing nitrogen oxide emissions. Industries such as power generation, cement, and chemicals are increasingly adopting SCR systems to meet strict emission standards.

The power generation segment held the largest share (over 33.0%) in 2025.

Some of the key players operating in the nitrogen oxide control systems market are Honeywell International, Mitsubishi Heavy Industries, Ltd., BASF SE, Babcock & Wilcox Enterprises, Inc., Kanadevia Corporation., Yara International ASA, GE Vernova, CECO Environmental, Fuel Tech, Inc., Ducon Environmental Systems, Inc., ANDRITZ AG, and Haldor Topsoe A/S.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.