- Home

- »

- Next Generation Technologies

- »

-

Operator Training Simulator Market Size Report, 2026-2033GVR Report cover

![Operator Training Simulator Market (2026 - 2033)Report]()

Operator Training Simulator Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Hardware, Software, And Services), By Operator (Console Operator And Field Operator), By End Use, By Region, And Segment Forecasts

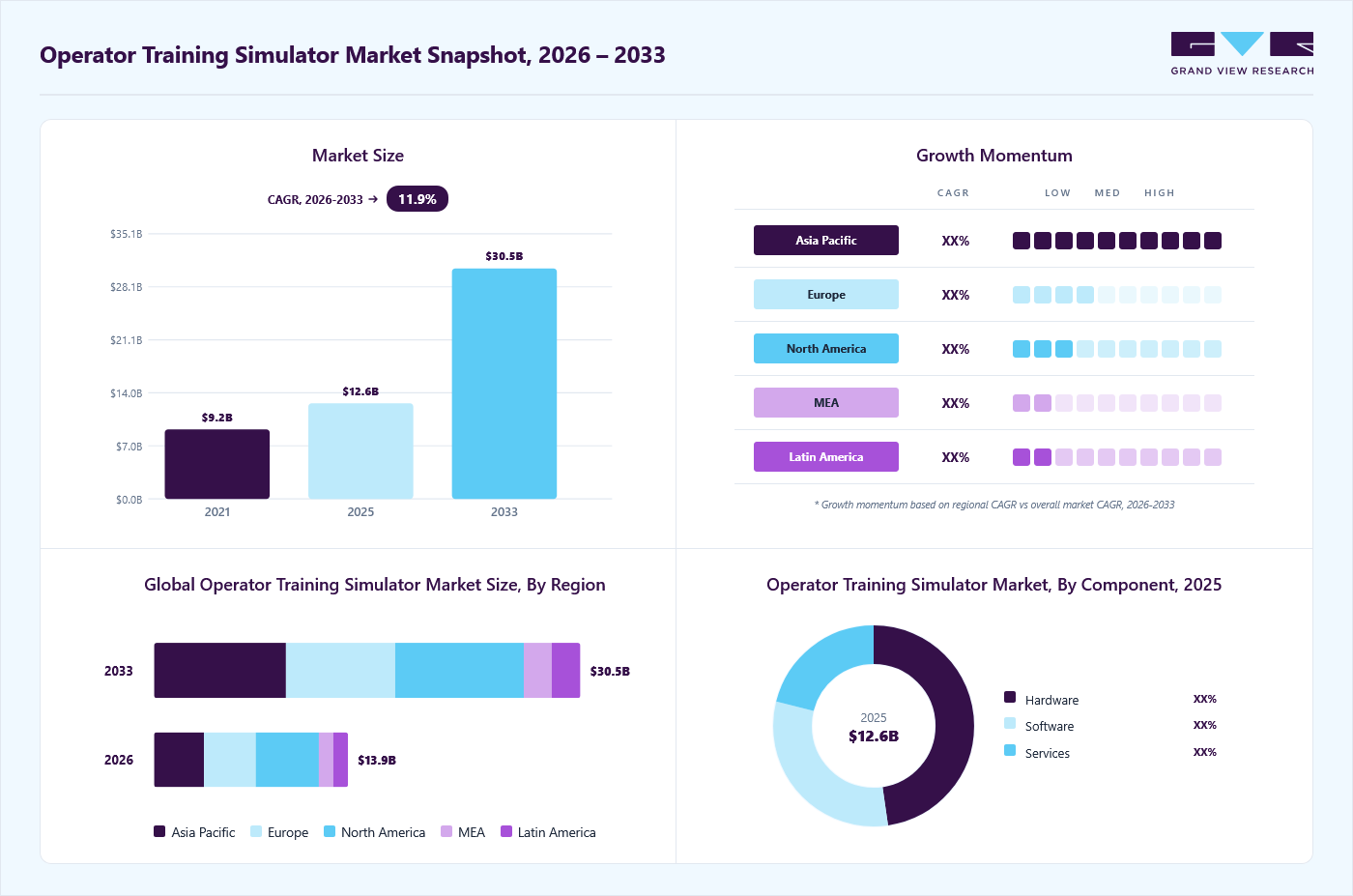

Market Size, 2025

$12.6BMarket Estimate, 2026

$13.9BMarket Forecast, 2033

$30.5BCAGR, 2026–2033

11.9%Operator Training Simulator Market Summary

The global operator training simulator market size was valued at USD 12.6 billion in 2025 and is projected to grow from USD 13.9 billion in 2026 to USD 30.5 billion by 2033, at a CAGR of 11.9% from 2026 to 2033. The market in North America dominated with a revenue share of 32.9% in 2025. A rising demand for skilled operators across organizations globally, growing concerns and stringent regulations regarding safety measures, and technological advancements in simulation are driving market growth.

Key Market Trends & Insights

- By component: Hardware segment held the largest market share of 47.7% in 2025.

- By operator: Console operator segment held the largest market share in 2025.

- By end use: Oil & gas segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (32.9% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 12.6 Billion

- Estimated market size in 2026: USD 13.9 Billion

- Projected market size by 2033: USD 30.5 Billion

- CAGR (2026-2033): 11.9%

An operator training simulator (OTS) is a computer-based simulation system that mimics the working environment using a dynamic simulation model. The system offers an economical solution for workforce training for various real-life situations and challenges. The integration of virtual and augmented reality, coupled with the adoption of sophisticated simulation software, has helped enhance the realism and effectiveness of training experiences. Technological innovations across industries have compelled organizations to adopt OTS solutions, which are expected to drive steady industry growth.Rising industrialization worldwide has led to the establishment of various heavy industries in developing and emerging economies, an essential driver of this market. Industries such as aviation, oil and gas exploration, petroleum refining, energy, and healthcare are subject to stringent safety protocols from regulatory authorities and local governments. Simulators provide a computer-generated, virtual reality-based controlled environment for operators to practice emergency procedures and comply with regulatory mandates. Furthermore, these simulators offer a cost-effective alternative to real-world training by minimizing equipment damage, reducing downtime, and improving operational efficiency, justifying their adoption among enterprises.

")

The application of operator training simulators is broadening beyond traditional sectors to encompass industries such as automotive, mining, construction, and medical & healthcare, thereby substantially advancing the market. These training simulators enable operators to encounter and manage hazardous situations in a safe and controlled setting, thereby minimizing the risk of accidents and improving safety culture. In addition, increasing investments in defense modernization and digital training infrastructure are further strengthening the adoption of advanced simulation technologies across military training programs worldwide. For instance, in January 2025, Rheinmetall and Bohemia Interactive Simulations (BISim) formed a strategic partnership to advance operator training simulator solutions using VBS4 and Blue IG technologies. The collaboration will enhance realistic gunnery and combat training systems for military applications, beginning with the German Army’s Heavy Weapons Carrier project, improving training effectiveness and flexibility. This partnership is expected to accelerate innovation and increase the adoption of advanced operator training simulators in the global defense training market.

Overall, the operator training simulator market is witnessing strong growth driven by safety regulations, industrial expansion, and digital transformation of training systems. Continuous technological advancements and cross-industry adoption are expected to further enhance market penetration and long-term growth potential.

Component Insights

Hardware components accounted for the leading market share of 47.7% in 2025. It serves as the fundamental building block for operator training simulators. Components such as processors, graphics cards, input/output devices, and specialized peripherals are essential for creating immersive and realistic training environments. In addition, continuous innovations in hardware technology, including increased processing power, enhanced graphics capabilities, and miniaturization, have directly contributed to this segment's dominance. These advancements enable the development of more sophisticated and complex simulation scenarios, significantly improving operator skills.

The services segment is expected to register the fastest CAGR from 2026 to 2033. As OTS systems become more sophisticated at accurately replicating real-world conditions, the demand for expert services to install, configure, maintain, and upgrade these systems has risen proportionally. Notably, integration & deployment services account for a substantial share of this segment. Moreover, organizations increasingly seek to maximize the value derived from their OTS investments. Service providers offer performance optimization, training, and support services to enhance simulator utilization and effectiveness, thereby accelerating segment growth.

Operator Insights

The console operator segment held the largest market revenue share in 2025. Console operators are required to manage intricate systems and processes that demand high technical proficiency and decision-making ability. Simulator-based training provides a controlled environment to effectively develop these critical skills, mitigating the risks and high costs associated with on-the-job learning. It primarily applies to the energy, aerospace, and manufacturing industries, which are subject to stringent safety and operational standards.

The field operator segment is expected to grow at the fastest CAGR over the forecast period. Industries with a significant field operator presence, such as oil & gas, manufacturing, and mining, have increasingly prioritized the implementation of safety protocols to improve working conditions. Operator training simulators provide a controlled environment for simulating hazardous situations, reducing on-the-job accidents, and ensuring a safe work environment. Furthermore, the complexity of modern machinery and processes demands highly skilled field operators. Simulators provide an affordable and efficient way to bridge the skills gap by offering hands-on experience without the risks of real-world operations.

End Use Insights

The oil & gas sector accounted for the largest market share in 2025. The industry's inherently complex and high-risk operational environments compel management to arrange rigorous training sessions for its personnel to ensure worker safety, efficiency, and environmental protection. Operator training simulators provide a controlled environment to replicate real-world challenges, mitigating potential risks and financial losses. Moreover, stringent regulatory frameworks governing safety and environmental standards in the oil and gas industry require comprehensive operator training programs. Simulators offer a structured approach to meet these compliance requirements, accounting for this sector's dominance.

The medical & healthcare sector is expected to register the fastest CAGR during the forecast period. The healthcare industry places an unparalleled emphasis on patient safety. Operator training simulators provide a controlled environment to equip medical professionals with the skills and knowledge needed to handle complex procedures and emergencies, thereby mitigating risks to patient health. Additionally, advancements in medical technology have led to the emergence of increasingly complex procedures and equipment. Simulators provide a platform for healthcare providers to master them without compromising patient well-being. As innovations in the healthcare sector continue to advance with sophisticated technologies, the demand for OTS systems is expected to increase in proportion.

Regional Insights

The North America operator training simulator industry led the market with a revenue share of 32.9% in 2025. The region possesses a diverse and mature industrial landscape, with critical sectors such as defense, aerospace, energy, manufacturing, and transportation driving advancements. These industries require highly skilled operators, boosting the demand for advanced training solutions. For instance, the airline industry utilizes flight simulators to train its pilots to operate various aircraft types. This option is affordable and environmentally friendly, as it uses no actual aircraft-grade fuel and thus causes no air pollution. Such factors account for a significant demand for OTS systems in the regional market.

U.S. Operator Training Simulator Market Trends

The operator training simulator industry in the U.S. held the largest share of the regional market in 2025. The country is a major supplier of defense equipment, such as the latest generation fighter jets and helicopters. Actual fighter pilot training on these aircraft may compromise the safety of operators and incur huge costs related to operational damages. OTS solutions offer a better alternative to industry stakeholders owing to the use of virtual reality simulators, which mimic the actual functional environments. These factors have led to heightened demand for such simulators among defense equipment manufacturers in the country.

Asia Pacific Operator Training Simulator Market Trends

The operator training simulator industry in the Asia Pacific is expected to grow at the fastest CAGR from 2026 to 2033. The region's expanding industrial landscape, characterized by growth in manufacturing, aerospace, energy, and transportation sectors, has highlighted the need for a skilled workforce proficient in operating complex machinery. Operator training simulators offer a cost-effective solution to bridge this skill gap. Furthermore, significant infrastructure investments across regional economies have increased demand for skilled operators in sectors such as power generation, transportation, and construction. Simulator-based training ensures operational efficiency and safety in these rapidly evolving industries.

The China operator training simulator industry held a significant share in 2025, driven by the country’s rapid industrial modernization, strong emphasis on workplace safety, and accelerating adoption of automation technologies across high-risk sectors such as oil & gas, power generation, chemicals, manufacturing, and aviation. Under national initiatives such as “Made in China 2025,” China is actively promoting digital transformation and intelligent manufacturing, which has significantly increased the deployment of simulation-based training systems to improve operator competency and reduce operational risks.

The operator training simulator industry in Japan held a significant share in 2025, supported by the country’s strong industrial automation base and its emphasis on operational safety, efficiency, and workforce skill enhancement across sectors such as energy, chemicals, power generation, and advanced manufacturing. A key driving factor is Japan’s demographic challenge, particularly an aging workforce and rising retirements among experienced plant operators, which is accelerating the need for structured knowledge transfer and immersive, risk-free training environments.

The India operator training simulator industry is expanding rapidly as India's defense, aviation, and energy sectors have experienced a high growth rate for the past three decades. The urgent and constant need for highly skilled personnel to operate sophisticated machines such as fighter jets, commercial aircraft, and power generation control systems has led to substantial investments in OTS solutions to mitigate risks associated with real-world training. In recent years, the government has prioritized skill development among youth and technological advancement in industries with several policy initiatives. This support for operator training and the adoption of simulation technologies has catalyzed market growth in the economy.

Europe Operator Training Simulator Market Trends

The operator training simulator industry in Europe accounted for a notable market share in 2025. The region is known for its industrial innovation across several sectors. The European Union closely monitors regulatory mandates across sectors such as healthcare, aviation, oil and gas exploration, and automobiles. Additionally, advancements in computer-generated graphics and design, such as Virtual Reality (VR), Extended Reality (XR), and Augmented Reality (AR), have caused a surge in the adoption of OTS solutions for comprehensive training programs. These factors are expected to drive steady regional demand growth over the forecast period.

The UK operator training simulator industry is expected to grow rapidly in the coming years. This is owing to the country’s established industrial environment, which obliges stakeholders to employ cutting-edge solutions for enhanced operational efficiency and superior workplace safety. Moreover, the rapid adoption of automation technology in the manufacturing sector has induced a strong demand for skilled workers to remotely operate these machines. These factors have collectively led to promising growth prospects for the OTS market in the UK.

The operator training simulator industry in Germany held a significant market share in 2025, driven by the country’s strong industrial base and its leadership in Industry 4.0 adoption across manufacturing, energy, automotive, and process industries. As German industries increasingly prioritize operational safety, productivity optimization, and regulatory compliance, particularly in high-risk sectors such as chemicals, power generation, and oil & gas, the demand for high-fidelity simulation-based training solutions is rising significantly.

Key Operator Training Simulator Company Insights

Some of the key companies operating in the market include ABB, ANDRITZ, Applied Research Associates, Inc., Aspen Technology Inc, AVEVA Group Limited, CORYS, DNV GL, among others.

-

In December 2025, Rheinmetall and VRAI entered a partnership to advance simulation data and AI-driven operator training solutions using VRAI’s HEAT platform. The collaboration focuses on improving armored crew performance through data analytics and the development of AI-enabled training systems, initially applied to XR driving simulators and expanding across defense training applications. This partnership will strengthen the integration of AI and data analytics in operator training simulators, accelerating the shift toward intelligent, performance-driven training ecosystems in the global defense market.

-

In January 2025, Somero Enterprises and ForgeFX Simulations launched the S-22EZ Laser Screed virtual training simulator to enhance construction operator training. The immersive VR-based solution enables risk-free learning of concrete leveling operations, improving precision, safety, and efficiency while reducing training costs and accelerating skill development through realistic machine simulation and performance tracking. This development is expected to expand the adoption of VR-based operator training simulators in the construction sector, driving market growth through scalable, cost-effective, and standardized skill development solutions.

-

In June 2024, Campus Veolia announced that its simulator had migrated to INDISS Plus, a dynamic simulation platform developed by CORYS. Other upgrades include developing a hazardous waste furnace model and finalizing Cloud deployment, aimed at improving training for waste incineration plant employees. The migration to INDISS Plus has made the instructor viewer console more intuitive and user-friendly, while also adding the option to design evaluation scenarios.

Key Operator Training Simulator Companies:

The following key companies have been profiled for this study on the operator training simulator market.

- ABB

- ANDRITZ

- Applied Research Associates, Inc.

- Aspen Technology Inc

- AVEVA Group Limited

- CORYS

- DNV GL

- Emerson Electric Co.

- ESI Group

- FLSmidth

- Honeywell International Inc.

- Schneider Electric

- Siemens

- SimGenics, LLC

- Yokogawa Electric Corporation

Operator Training Simulator Market Report Scope

Report Attribute

Details

Market size in 2025

USD 12.6 billion

Estimated market size in 2026

USD 13.9 billion

Projected market size by 2033

USD 30.5 billion

Growth rate

CAGR of 11.9% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, operator, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Thailand; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

ABB; ANDRITZ; Applied Research Associates, Inc.; Aspen Technology Inc; AVEVA Group Limited; CORYS; DNV GL; Emerson Electric Co.; ESI Group; FLSmidth; Honeywell International Inc.; Schneider Electric; Siemens; SimGenics, LLC; Yokogawa Electric Corporation

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Operator Training Simulator Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global operator training simulator market report based on component, operator, end use, and region.

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Hardware

-

Software

-

Control Simulation

-

Process Simulation

-

Immersive Simulation

-

-

Services

-

Integration & Deployment

-

Support & Maintenance

-

Training & Consulting

-

-

-

Operator Outlook (Revenue, USD Billion, 2021 - 2033)

-

Console Operator

-

Field Operator

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Automotive

-

Aerospace & Defense

-

Energy & Power

-

Oil & Gas

-

Medical & Healthcare

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

The hardware segment led with a 47.7% revenue share in 2025, while services is the fastest-growing component.

The console operator segment held the largest revenue share in 2025, while field operator is the fastest-growing segment.

Oil & gas segment held the largest revenue share in 2025, while medical & healthcare is the fastest-growing segment.

Key players include ABB; ANDRITZ; Applied Research Associates, Inc.; Aspen Technology Inc; AVEVA Group Limited; CORYS; DNV GL; Emerson Electric Co.; ESI Group; FLSmidth; Honeywell International Inc.; Schneider Electric; Siemens; SimGenics, LLC; Yokogawa Electric Corporation.

Key factors that are driving the market growth include rising demand for competent process operators, coupled with corporate initiatives for workplace safety for employees often in hazardous sectors and occupations.

The global operator training simulator market size was valued at USD 12.6 billion in 2025 and is estimated at USD 13.9 billion for 2026.

The global operator training simulator market is expected to grow at a CAGR of 11.9% from 2026 to 2033, reaching USD 30.5 billion by 2033.

North America dominated the operator training simulator market with a share of 32.9% in 2025. This is attributable to the rise in the adoption of automation, innovations, and technological advancements in the industrial domain in the region.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.