- Home

- »

- Pharmaceuticals

- »

-

Pharmaceutical Market Size And Share Report, 2026-2033GVR Report cover

![Pharmaceutical Market (2026 - 2033)Report]()

Pharmaceutical Market (2026 - 2033)

Size, Share & Trends Analysis Report By Molecule Type, By Product (Branded, Generic), By Type (Prescription, OTC), By Disease, By Route Of Administration (Oral, Topical, Parenteral), By Age Group, By Distribution Channel, By Region, And Segment Forecasts

Market Size, 2025

$1,738.0BMarket Estimate, 2026

$1,837.0BMarket Forecast, 2033

$2,776.7BCAGR, 2026–2033

6.1%Pharmaceutical Market Summary

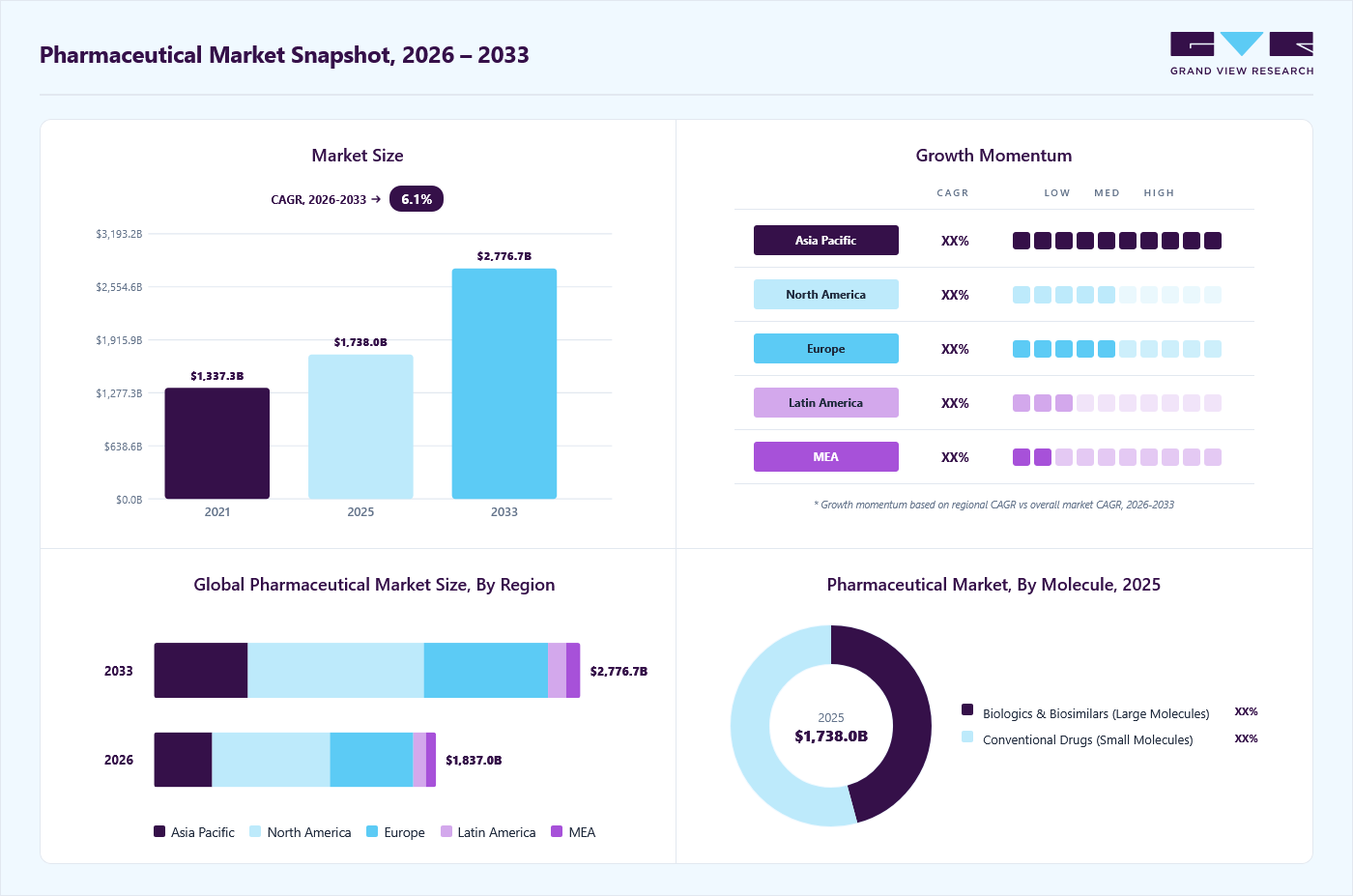

The global pharmaceutical market size was valued at USD 1,738.0 billion in 2025 and is projected to grow from USD 1,837.0 billion in 2026 to USD 2,776.7 billion by 2033, at a CAGR of 6.1% from 2026 to 2033. The market in North America dominated with a revenue share of 41.8% in 2025. The increasing prevalence of chronic and infectious diseases is a primary factor accelerating the market expansion.

Key Market Trends & Insights

- By molecule type: Conventional drugs (small molecules) segment held the largest market share of 54.2% in 2025.

- By product: Branded segment held the largest market share of 66.5% in 2025.

- By type: Prescription segment held the largest market share of 86.5% in 2025.

- By disease: Cancer segment held the largest market share of 18.6% in 2025.

- By route of administration: Oral segment held the largest market share of 57.4% in 2025.

Regional Highlights

- Largest regional market: North America (41.8% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 1,738.0 Billion

- Estimated market size in 2026: USD 1,837.0 Billion

- Projected market size by 2033: USD 2,776.7 Billion

- CAGR (2026-2033): 6.1%

The rising incidence of cancer, cardiovascular disorders, diabetes, and respiratory conditions has created sustained demand for long-term therapeutic management across global populations. The expansion of life expectancy has increased the aging population, which requires ongoing pharmacological intervention for multiple comorbidities. This demographic transition has significantly increased prescription volumes and recurring drug utilization rates. Urbanization, sedentary lifestyles, and changing dietary patterns have further intensified the global disease burden. For instance, in January 2026, the International Diabetes Federation reported that approximately 589 million adults aged 20 to 79 years were living with diabetes in 2024, representing about 11.1 per cent of the global adult population, with over 252 million unaware of their condition and more than 81 per cent residing in low and middle income countries, while projections indicated the total could rise to 853 million by 2050, predominantly driven by type 2 diabetes. Healthcare providers are focusing on early diagnosis and structured treatment protocols to effectively manage disease progression. As a result, consistent demand for branded, specialty, and maintenance therapies continues to support stable revenue generation across mature and emerging markets.Rapid advancements in biotechnology, precision medicine, and novel drug delivery platforms are reshaping treatment paradigms and strengthening the competitive landscape. Pharmaceutical companies are increasing research intensity to develop targeted therapies that offer higher efficacy and improved safety profiles. Expansion of biologics, cell-based therapies, and monoclonal antibodies has diversified product portfolios and enhanced therapeutic specificity. Digital integration within clinical trials has improved patient recruitment, monitoring accuracy, and data analysis efficiency. Artificial intelligence-driven drug discovery tools are accelerating compound identification and reducing development timelines. For instance, in February 2026, the Financial Times reported that a large international study published in The Lancet found adults with obesity had a 70 per cent higher risk of hospitalization or death from serious infectious diseases including influenza, COVID 19, pneumonia, gastroenteritis, urinary tract infections, and lower respiratory tract infections, based on data from 540,000 individuals in the UK and Finland followed for 13 to 14 years, with projections suggesting obesity may have contributed to approximately 0.6 million of the 5.4 million infection related deaths globally in 2023. Collaborative research agreements between manufacturers and academic institutions are enhancing innovation capabilities. These technological advancements are sustaining differentiated product launches and reinforcing long-term market expansion.

")

Rising healthcare expenditure across developed and emerging regions is improving access to treatment and overall drug consumption. Growth in organized retail pharmacy chains and digital distribution platforms has expanded reach to semi-urban and rural populations. Increasing patient awareness of preventive healthcare and routine screening has strengthened the adoption of early-stage treatment. Patent expirations of major branded therapies have stimulated the introduction of cost-efficient generics and biosimilars, broadening patient access. For instance, in January 2026, Medical Buyer reported that India faced escalating health challenges, including 15.6 lakh cancer cases and 8.74 lakh cancer deaths in 2024, over 17 lakh pollution related deaths in 2022, a tuberculosis burden accounting for roughly one quarter of global cases, and a rapidly rising prevalence of obesity, diabetes, and hypertension, with the ICMR INDIAB study estimating 101 million people living with diabetes and 315 million with high blood pressure. Manufacturing modernization and supply chain digitization are improving production scalability and inventory management. Greater emphasis on quality standards and operational efficiency is reducing supply disruptions. These structural improvements collectively enhance market resilience and support the sustained growth of the pharmaceutical industry.

Market Dynamics

The global increase in chronic diseases has become one of the most significant factors driving the growth of the pharmaceutical market. Conditions such as cancer, diabetes, cardiovascular diseases, and chronic respiratory disorders are becoming more common due to aging populations, sedentary lifestyles, unhealthy diets, and rising obesity rates. As life expectancy increases, more individuals require long-term medical treatment and disease management, leading to sustained demand for pharmaceutical products. Chronic diseases often require continuous medication, monitoring, and combination therapies, which further contributes to market expansion. Governments and healthcare organizations are also prioritizing early diagnosis and treatment programs, increasing prescription volumes. This growing patient population creates substantial opportunities for pharmaceutical companies to develop innovative therapies and expand their product portfolios.

In addition to chronic illnesses, the continued emergence and spread of infectious diseases significantly contribute to pharmaceutical market growth. Outbreaks of viral infections, bacterial resistance, and global pandemics have highlighted the importance of vaccines, antiviral medications, and antibiotic development. Pharmaceutical companies are increasingly investing in research to address evolving pathogens and drug-resistant strains, which require new therapeutic approaches. The demand for preventive healthcare solutions, including immunization programs and rapid diagnostic tools, has also increased globally. Governments are allocating higher healthcare budgets to strengthen public health systems and improve access to essential medicines. These factors collectively drive the need for pharmaceutical innovation and production capacity, ensuring sustained market demand across both developed and developing regions.

The rising prevalence of both chronic and infectious diseases is further amplified by demographic and environmental factors. Urbanization, pollution, climate change, and increased global travel contribute to the spread of diseases and health complications. Aging populations, particularly in developed economies, are more susceptible to multiple chronic conditions, requiring complex treatment regimens and specialized drugs. At the same time, developing countries are experiencing epidemiological transitions, where infectious diseases remain prevalent while chronic conditions are rapidly increasing. This dual disease burden creates additional pressure on healthcare systems and increases pharmaceutical consumption. Improved healthcare awareness and screening programs are also leading to earlier diagnosis, further increasing treatment rates and pharmaceutical utilization worldwide.

Technological advancements and improved healthcare infrastructure are enabling better management of chronic and infectious diseases, further supporting pharmaceutical market growth. Innovations in drug development, including biologics, personalized medicine, and targeted therapies, are improving treatment effectiveness and patient outcomes. Digital health technologies and remote monitoring tools are also enhancing disease management and medication adherence. Governments and private organizations are expanding healthcare coverage, increasing access to medicines in emerging markets. Pharmaceutical companies are responding by developing affordable treatment options and expanding distribution networks. As disease prevalence continues to rise globally, the need for effective therapeutic solutions will remain strong, positioning the pharmaceutical market for sustained long-term growth.

The process of developing new pharmaceutical products involves extensive research, multiple phases of clinical trials, and complex regulatory approvals, making it both time-consuming and expensive. On average, bringing a new drug to market can take more than ten years and require billions of dollars in investment. Pharmaceutical companies must allocate substantial financial resources toward laboratory research, preclinical testing, human trials, and post-marketing surveillance. The uncertainty associated with drug discovery further increases financial risk, as many compounds fail during development. These high costs create significant barriers for companies, particularly smaller firms with limited capital, restricting their ability to innovate. As a result, only a fraction of potential drug candidates successfully reaches commercialization, slowing overall pharmaceutical market growth.

Regulatory requirements imposed by health authorities play a critical role in ensuring drug safety and efficacy, but they also add complexity and cost to the development process. Agencies such as regulatory bodies require comprehensive clinical data, strict quality standards, and detailed documentation before granting approvals. Meeting these requirements often involves additional testing, extended timelines, and increased administrative efforts. Variations in regulatory frameworks across different countries further complicate global drug launches, forcing companies to navigate multiple approval systems simultaneously. Delays in approvals can significantly impact revenue projections and return on investment. Consequently, regulatory hurdles can discourage innovation and limit the number of new therapies entering the market, particularly affecting smaller biotechnology companies with fewer regulatory resources and expertise.

High failure rates during clinical trials represent another major financial challenge for pharmaceutical companies. Many drug candidates that show promise in early research stages fail to demonstrate safety or effectiveness during later trial phases. Late-stage failures are particularly costly because substantial investments have already been made in development, manufacturing preparation, and regulatory submissions. This risk forces companies to adopt cautious investment strategies and prioritize projects with higher probability of success, potentially limiting exploration of novel therapies. Investors may also hesitate to fund early-stage pharmaceutical research due to uncertain returns. These challenges contribute to rising drug prices, as companies attempt to recover development costs from successful products, creating additional market constraints and affordability concerns.

Smaller pharmaceutical and biotechnology companies face disproportionate challenges in managing development costs and regulatory requirements compared to large multinational corporations. Limited financial resources, lack of infrastructure, and reduced access to advanced technologies make it difficult for smaller firms to sustain long development cycles. Many rely on partnerships, licensing agreements, or acquisitions by larger companies to bring their innovations to market. While collaborations can support innovation, they may also reduce independent competition within the industry. Additionally, high compliance costs associated with manufacturing standards, quality assurance, and post-approval monitoring create ongoing financial burdens. These combined challenges can slow innovation, reduce market diversity, and ultimately restrain the overall growth potential of the pharmaceutical market.

Market Concentration & Characteristics

The pharmaceutical market is highly innovation-driven, with companies investing heavily in research and development to develop new drugs, biologics, and advanced therapies. Breakthrough innovations, particularly in oncology, rare diseases, and personalized medicine, provide significant competitive advantages. Patents and intellectual property rights protect these innovations, incentivizing continued investment. The pace of innovation varies, with biotech firms often leading in novel therapies while large pharmaceutical companies focus on scaling and global commercialization. Continuous technological advancements, including AI-driven drug discovery and precision medicine, accelerate product development. High innovation intensity is essential for maintaining market leadership and sustaining long-term growth.

Entering the pharmaceuticals market requires substantial capital investment, sophisticated research capabilities, and regulatory expertise. Stringent clinical trial requirements, long development timelines, and high R&D costs create significant hurdles for new players. Established brand reputation and trust in the safety and efficacy of existing products further discourage new entrants. Access to specialized talent, advanced manufacturing facilities, and robust distribution networks is critical for competitiveness. High barriers limit market fragmentation, often resulting in a concentrated market dominated by leading multinational companies. Emerging firms often rely on niche therapeutic areas or partnerships with larger players to overcome entry challenges.

Pharmaceutical companies operate under strict regulatory oversight that governs drug approval, safety, marketing, and pricing. Compliance with authorities such as the FDA, EMA, and CDSCO ensures product quality but increases development timelines and operational costs. Regulations also dictate post-marketing surveillance, reporting adverse effects, and adherence to Good Manufacturing Practices. Policy changes can impact pricing strategies, reimbursement frameworks, and market access globally. Regulatory complexity favors established companies with experience and resources to navigate compliance. Overall, regulations serve both as a quality safeguard and as a barrier to rapid market entry.

Substitutes in the pharmaceutical industry include generic drugs, biosimilars, over-the-counter alternatives, and emerging non-pharmacological therapies. Generic versions often challenge branded drugs once patents expire, leading to price competition and reduced revenue for originator companies. Biosimilars are increasingly significant in biologics, providing lower-cost alternatives with comparable efficacy. Non-drug interventions, such as digital therapeutics and lifestyle-based treatments, are gradually influencing treatment patterns. Companies respond by developing innovative formulations, combination therapies, or extended patent strategies. The presence of substitutes encourages continuous innovation and strategic differentiation to maintain market share.

Pharmaceutical companies pursue geographical expansion to access new markets, diversify revenue, and leverage global healthcare demand. Expansion strategies include partnerships, acquisitions, licensing agreements, and the establishment of local manufacturing facilities. Emerging markets such as India, China, and Latin America offer growth opportunities driven by rising healthcare spending and increasing chronic disease prevalence. Regulatory harmonization and local market knowledge are crucial for successful entry. Multinational firms balance global scale with local adaptation in pricing, product mix, and marketing strategies. Strategic geographical expansion strengthens brand presence, mitigates market concentration risk, and enhances long-term profitability.

Molecule Type Insights

The conventional drugs (small molecules) segment dominated the pharmaceutical market, accounting for the largest revenue share of 54.24% in 2025, driven by strong demand for cost-effective therapies, well-established manufacturing processes, and a broad range of approved products across major therapeutic areas, including cardiovascular, metabolic, and infectious diseases. Small molecules benefit from extensive clinical and commercial experience, relatively simpler regulatory pathways in many regions, and high adoption in both hospital and outpatient settings. Additionally, the availability of numerous generic small-molecule drugs continues to expand patient access while supporting revenue growth. Investments in process optimization and supply chain efficiency have further strengthened the competitiveness of conventional drugs compared with newer biologics and advanced modalities, particularly in markets where healthcare budgets remain constrained. For instance, in July 2025 the World Health Organization reported that an estimated 19.8 million people died from cardiovascular diseases in 2022, representing around 32 percent of global deaths, with 85 percent of these fatalities attributed to heart attack and stroke, more than three quarters occurring in low and middle income countries, and at least 38 percent of the 18 million premature deaths under age 70 from noncommunicable diseases in 2021 linked to cardiovascular conditions, underscoring the critical role of accessible small molecule therapies in early detection, long term management, and risk reduction through medicines and counselling.

The biologics & biosimilars (large molecules) segment is projected to grow at a CAGR of 7.17% over the forecast period, driven by rising adoption of targeted therapies, increasing prevalence of chronic conditions such as autoimmune disorders and cancer, and sustained investment in research and development. Advances in biotechnology have expanded pipelines of monoclonal antibodies, recombinant proteins, and other complex biologic modalities, improving efficacy and safety outcomes. Regulatory support for biosimilars in key markets has reduced entry barriers, supporting affordability and wider patient access. At the same time, collaborations between biopharmaceutical companies and contract development and manufacturing organizations continue to enhance production capacity and commercialization timelines. For instance, in February 2025, the World Health Organization reported that cancer caused nearly 10 million deaths globally in 2020, representing almost one in six deaths worldwide, highlighting the urgent need for innovative biologic and biosimilar therapies to address the substantial and growing global disease burden.

Product Insights

The branded segment dominated the pharmaceutical industry, accounting for the largest revenue share of 66.49% in 2025, driven by strong demand for innovative therapies, robust patent portfolios held by major pharmaceutical companies, and higher price points compared with unbranded alternatives. Branded products benefit from significant investment in clinical development and marketing, which helps maintain physician preference and patient loyalty. In many therapeutic areas, new drug launches and label expansions for existing therapies continued to support revenue growth. At the same time, exclusivity protections under intellectual property laws in key markets enabled premium pricing before generic or biosimilar competition emerged. For instance, in December 2025, WIRED reported that the U.S. Food and Drug Administration had approved a daily pill version of the branded anti-obesity drug Wegovy from Novo Nordisk. Clinical data published in the New England Journal of Medicine showed an average weight loss of 13.6% at 64 weeks, with nearly 30% of participants losing 20% or more, and up to 16.6% under ideal adherence with a 25-milligram dose. The 1.5 milligram starting dose was planned at about USD 149 per month in early January 2026, with U.S. production underway. Both formulations contained semaglutide, while Rybelsus, approved in 2019 at 14 milligrams, was not approved for obesity, reinforcing branded innovation leadership.

The generic segment is projected to grow at a CAGR of 7.20% over the forecast period, fueled by increasing patent expirations of blockbuster drugs, rising demand for cost-effective treatment options, and supportive government initiatives promoting affordable healthcare. As healthcare systems face mounting budget pressures, generics provide substantial cost savings compared with branded counterparts while maintaining comparable efficacy and safety profiles. Growing penetration in emerging markets, expansion of domestic manufacturing capabilities, and streamlined regulatory pathways for abbreviated approvals are accelerating adoption. In contrast, pharmacy substitution policies and favorable reimbursement frameworks in developed markets continue to strengthen utilization rates. For instance, in September 2025, the Association for Accessible Medicines reported that generics accounted for 90% of all prescriptions filled in the United States but only 12% of total prescription drug spending. In 2024, 3.9 billion generic prescriptions were filled compared with 435 million brand prescriptions, with spending of USD 98 billion on generics versus USD 700 billion on branded drugs. Generics generated USD 467 billion in savings in 2024 and USD 3.4 trillion over the previous decade, including USD 142 billion in Medicare savings, equal to USD 2,643 per beneficiary, underscoring their significant economic impact and expanded patient access nationwide.

Type Insights

The prescription segment dominated the market with the largest revenue share of 86.53% in 2025, driven by the high prevalence of chronic and complex diseases requiring physician supervision and regulated dispensing. Prescription medicines, particularly in therapeutic areas such as oncology, cardiovascular disorders, diabetes, and autoimmune diseases, command higher price points due to advanced formulations and targeted mechanisms of action. Continued innovation in specialty drugs, biologics, and combination therapies further strengthened prescription drug revenues across developed and emerging markets. In addition, favorable reimbursement frameworks, expanding health insurance coverage, and growing access to hospital and specialty care settings supported sustained demand for prescription-based treatments, reinforcing the segment’s leading market position.

The OTC segment is projected to grow at a CAGR of 7.80% over the forecast period, driven by rising consumer preference for self-medication, increased awareness of preventive healthcare, and expanding availability of non-prescription products across retail and online pharmacies. The growing incidence of minor ailments, such as colds and flu, gastrointestinal disorders, allergies, and pain-related conditions, continues to drive steady demand for OTC formulations. In addition, product innovations in convenient dosage forms, attractive packaging, and combination therapies are enhancing consumer adoption. Regulatory switches from prescription to OTC status in several markets, along with aggressive marketing campaigns and digital health platforms, are further accelerating segment growth, particularly in emerging economies where access to primary healthcare services remains limited.

Disease Insights

The cancer segment dominated the market, accounting for the largest revenue share of 18.61% in 2025, driven by the rising global incidence of multiple malignancies and growing adoption of advanced therapeutic modalities. Increasing approvals of targeted therapies, immunotherapies, monoclonal antibodies, and personalized medicine approaches significantly expanded treatment options and improved patient outcomes. Substantial investment in oncology research and development, alongside a robust clinical pipeline of innovative drug candidates, further strengthened revenue generation. Favorable reimbursement policies in developed markets, expanding access to care in emerging economies, and greater awareness of early diagnosis and screening programs also supported sustained leadership. For instance, in January 2025, CA: A Cancer Journal for Clinicians reported that 2,041,910 new cancer cases and 618,120 deaths were projected in the United States in 2025. Mortality declined through 2022, averting nearly 4.5 million deaths since 1991, yet disparities persisted. Women aged 50 to 64 had an incidence rate of 832.5 per 100,000, compared with 830.6 in men. Younger women showed 82% higher incidence, 141.1 versus 77.4 per 100,000, and lung cancer rates reached 15.7 versus 15.4 per 100,000, underscoring ongoing clinical need.

The obesity segment is projected to grow at a CAGR of 12.73% over the forecast period, fueled by the rising global prevalence of overweight and obese populations, increasing awareness of obesity related comorbidities such as type 2 diabetes and cardiovascular diseases, and the expanding adoption of novel pharmacological therapies. The introduction of advanced anti-obesity medications, particularly glucagon-like peptide 1 receptor agonists and combination therapies, has significantly improved clinical outcomes and boosted prescription volumes. The growing emphasis on preventive healthcare, supportive regulatory approvals, and broader insurance coverage for weight management treatments in key markets are further accelerating demand. At the same time, increased patient willingness to seek medical intervention beyond lifestyle modifications supports long-term growth. For instance, in September 2025, UNICEF reported that obesity had surpassed underweight as the most prevalent form of malnutrition among school-age children and adolescents globally, affecting approximately 188 million young people aged 5 to 19 years, or about 1 in 10 children. Obesity prevalence rose from 3% in 2000 to 9.4% in 2025, underweight rates declined from 13% to 9.2%, and about 391 million children and adolescents were classified as overweight, with high rates in Pacific Island nations such as Niue (38%), the Cook Islands (37%), Nauru (33%), and notable prevalence in Chile (27%), the United States (21%), and the United Arab Emirates (21%), highlighting the global rise in childhood obesity and associated health risks.

Route of Administration Insights

The oral segment dominated the market, accounting for the largest revenue share of 57.35% in 2025, driven by high patient compliance, ease of administration, and cost-effective manufacturing processes. Oral formulations such as tablets, capsules, and syrups remain the preferred choice for treating a wide range of acute and chronic conditions due to their convenience and non-invasive nature. Extensive availability of generic and branded oral drugs across therapeutic areas, including cardiovascular, metabolic, infectious, and gastrointestinal disorders, further supported segment growth. In addition, advancements in modified-release technologies, taste-masking techniques, and improved bioavailability profiles have enhanced therapeutic effectiveness, reinforcing the dominance of the oral route in the global market.

The parenteral segment is projected to grow at a CAGR of 7.63% over the forecast period, fueled by the increasing demand for biologics, biosimilars, and specialty drugs that require injectable administration. The rising prevalence of chronic and life-threatening conditions such as cancer, autoimmune disorders, and metabolic diseases has accelerated the adoption of intravenous, intramuscular, and subcutaneous therapies. Parenteral formulations offer a rapid onset of action and higher bioavailability than oral alternatives, making them essential in emergency care and hospital settings. Additionally, advancements in drug delivery technologies, including prefilled syringes, autoinjectors, and long-acting injectable formulations, are enhancing patient convenience and expanding their use in outpatient and home care environments. Growing investments in sterile manufacturing infrastructure and regulatory approvals for complex injectable products are further supporting segment expansion.

Age Group Insights

The adults segment dominated the pharmaceutical market, accounting for the largest revenue share of 62.91% in 2025, driven by the high prevalence of chronic diseases such as cardiovascular disorders, diabetes, cancer, and respiratory conditions within the adult population. Increased healthcare utilization, higher prescription volumes, and greater access to insurance coverage across developed and emerging markets significantly contributed to segment growth. Adults are also the primary recipients of specialty therapies, biologics, and long-term treatment regimens, which often entail higher costs. In addition, growing awareness regarding preventive healthcare, routine screenings, and early disease management further strengthened demand for pharmaceutical products among the adult demographic, reinforcing the segment’s leading market position.

The geriatric segment is projected to grow at a CAGR of 6.55% over the forecast period, fueled by the rapidly expanding aging population and the rising burden of age-associated chronic diseases such as cardiovascular disorders, neurodegenerative conditions, osteoporosis, diabetes, and cancer. Older adults typically require long-term pharmacological management, often involving multiple medications, which significantly increases overall drug consumption. Improvements in life expectancy, greater access to healthcare services, and expanding insurance coverage in both developed and emerging markets are further supporting treatment uptake within this demographic. In addition, increased focus on geriatric-specific formulations, including dose-adjusted therapies and easy-to-administer drug-delivery systems, is expected to enhance adherence and drive sustained segment growth.

Distribution Channel Insights

The hospital pharmacy segment dominated the market, accounting for the largest revenue share of 53.38% in 2025, driven by the high volume of inpatient and outpatient treatments that require specialized, high-value medications. Hospitals serve as primary centers for the administration of complex therapies, including biologics, oncology drugs, injectable formulations, and critical care medicines, which collectively significantly contribute to revenue. The growing number of surgical procedures, rising hospital admissions for acute and chronic conditions, and expanding specialty care services further supported the segment's dominance. In addition, strong procurement networks, centralized purchasing systems, and integration with reimbursement frameworks enhanced drug distribution efficiency within hospital settings, reinforcing the leading position of hospital pharmacies in the market.

The retail pharmacy segment is projected to grow at a CAGR of 6.30% over the forecast period, fueled by increasing accessibility to prescription and over-the-counter medications, expanding pharmacy networks, and rising consumer preference for convenient point-of-sale healthcare services. Retail pharmacies play a critical role in chronic disease management, repeat prescription fulfillment, and patient counseling, particularly for conditions such as diabetes, hypertension, and respiratory disorders. The expansion of organized pharmacy chains, integration of digital prescription management systems, and home delivery services further support growth. In addition, growing health awareness, rising self-medication trends, and favorable reimbursement policies across several regions are expected to strengthen retail pharmacy penetration and sustain segment growth.

Regional Insights

The North America pharmaceutical industry held the largest global share of 41.80% in 2025, driven by high research intensity, advanced healthcare infrastructure, and high per capita drug spending. The region benefits from a robust pipeline of innovative biologics, specialty drugs, and precision therapies. Major pharmaceutical companies maintain headquarters and large-scale manufacturing facilities across the region. Rapid adoption of advanced treatment options and specialty medicines strengthens revenue generation. High prevalence of chronic diseases increases long-term prescription volumes. Established distribution networks and strong commercialization capabilities further reinforce regional leadership.

U.S. Pharmaceutical Market Trends

The U.S. pharmaceutical industry held the largest share within North America in 2025, attributed to the extensive clinical research activity and rapid product launches. The presence of leading biopharmaceutical innovators supports continuous pipeline expansion. High healthcare expenditure per capita sustains demand for branded and specialty drugs. Strong intellectual property frameworks encourage investment in novel therapies and biologics. A mature reimbursement structure facilitates broad patient access to advanced medications. Growing focus on personalized medicine and cell and gene therapies further enhances market growth.

Europe Pharmaceutical Market Trends

Europe represents a significant share of the pharmaceutical industry, supported by advanced healthcare systems and established pharmaceutical manufacturing clusters. The region maintains strong capabilities in biosimilars and specialty generics production. Rising incidence of chronic and age-related diseases sustains demand for long-term therapies. Collaborative research networks across countries accelerate clinical development timelines. Expansion of innovative biologics and orphan drugs contributes to steady revenue growth. Well-developed supply chains ensure stable product availability across member states.

The UK pharmaceutical market benefits from strong life sciences research and a concentrated base of global pharmaceutical companies. Advanced clinical trial infrastructure supports both early- and late-stage drug development. Growing demand for oncology and rare disease treatments drives specialty drug sales. Strategic collaborations between academia and industry support innovation output. The increasing adoption of biologics and advanced therapies is strengthening market value. Export-oriented manufacturing activities contribute to sustained industry presence.

The pharmaceutical market in Germany is expected to grow over the forecast period. Germany stands as a leading pharmaceutical hub in Europe, supported by strong industrial manufacturing capabilities. The country maintains a broad base of mid-sized and multinational pharmaceutical firms. The high demand for prescription medicines reflects an aging population and rising rates of chronic conditions. Strong expertise in chemical synthesis and biologics production enhances export competitiveness. Continuous product innovation across cardiology and oncology sustains revenue streams. Efficient distribution channels support consistent domestic market performance.

The France pharmaceutical market holds a stable position within Europe, driven by advanced therapeutic research and diversified product portfolios. Strong presence of multinational drug manufacturers strengthens local production capacity. Demand for specialty medicines and vaccines contributes to steady growth. An increased focus on biotechnology research is expanding the development of targeted therapies. Established hospital networks sustain prescription drug volumes. Strategic partnerships within Europe enhance cross-border commercialization activities.

Asia Pacific Pharmaceutical Market Trends

The Asia Pacific pharmaceutical industry is expected to register the fastest CAGR of 7.06% over the forecast period, driven by expanding healthcare access and rising income levels. Rapid urbanization increases demand for modern treatment solutions. The growing burden of chronic and infectious diseases accelerates pharmaceutical consumption. Expansion of local manufacturing capacity improves supply chain resilience. Rising investments in biotechnology and biosimilars strengthen regional competitiveness. Large patient populations create strong long-term growth potential across diverse therapeutic areas.

The Japan pharmaceutical market is mature, characterized by strong innovation in specialty and orphan drugs. The country maintains advanced capabilities in biologics and regenerative medicine research. An aging population drives sustained demand for cardiovascular and oncology therapies. High healthcare standards support the adoption of advanced treatment options. Domestic pharmaceutical companies maintain strong global partnerships for product development. Stable distribution systems ensure the consistent availability of prescription medications.

The pharmaceutical market in China is rapidly expanding, driven by large-scale manufacturing and growing research capacity. The rising prevalence of chronic diseases increases demand for innovative and generic medicines. Expansion of domestic biopharmaceutical firms strengthens competitive dynamics. Increased clinical trial activity accelerates product commercialization timelines. Strong production capabilities enhance export potential across emerging markets. Growing urban healthcare infrastructure supports higher prescription volumes.

Latin America Pharmaceutical Market Trends

Latin America demonstrates steady growth in the pharmaceutical industry, driven by expanding access to essential medicines and specialty drugs. Rising awareness of chronic disease management supports long-term treatment adoption. Local manufacturing initiatives improve regional supply stability. Increasing demand for branded generics strengthens competitive positioning. Multinational companies expand distribution networks to capture untapped patient populations. Gradual modernization of healthcare facilities supports consistent market expansion.

The Brazil pharmaceutical market leads Latin America, driven by a large patient base and diversified therapeutic demand. Strong domestic pharmaceutical production enhances market self-sufficiency. The rising prevalence of metabolic and cardiovascular diseases sustains prescription growth. Expansion of branded generic portfolios improves affordability and volume sales. Increasing clinical research activities attract multinational partnerships. Broad retail pharmacy networks strengthen nationwide drug distribution.

Middle East & Africa Pharmaceutical Market Trends

The Middle East & Africa region shows moderate growth in the pharmaceutical industry, supported by expanding healthcare infrastructure and rising disease awareness. The increasing demand for specialty and hospital-administered drugs drives revenue growth. Growing urban populations contribute to higher pharmaceutical consumption. Expansion of regional manufacturing capabilities improves product availability. Multinational companies pursue distribution partnerships to expand market presence. Focus on advanced therapies in urban centers supports gradual market development.

The Saudi Arabian pharmaceutical market is a key region in the Middle East & Africa, driven by rising demand for innovative and specialty medicines. Expansion of domestic pharmaceutical manufacturing enhances supply chain efficiency. The increasing prevalence of lifestyle-related diseases supports long-term prescription demand. Growth in hospital infrastructure strengthens specialty drug utilization. Strategic collaborations with international pharmaceutical firms expand product portfolios. Strong distribution systems ensure broad access to branded and generic medications.

Key Pharmaceutical Company Insights

F. Hoffmann-La Roche Ltd. and Novartis AG continue to strengthen their global pharmaceutical presence through strong biologics portfolios, advanced oncology therapies, and expanding personalized medicine platforms. AbbVie Inc. and Johnson & Johnson Services, Inc. focus on diversified therapeutic segments, including immunology, oncology, and neuroscience, supported by robust research pipelines and strategic acquisitions. Merck & Co., Inc. and Pfizer Inc. emphasize innovative vaccine development, specialty medicines, and next-generation biologics to sustain competitive positioning across major markets. Bristol-Myers Squibb Company and Sanofi advance their portfolios through immunotherapies, rare disease treatments, and expanded global commercialization capabilities. GlaxoSmithKline plc. and AstraZeneca prioritize respiratory, oncology, and vaccine segments while investing in precision-based treatment approaches. Takeda Pharmaceutical Co., Ltd. enhances its market footprint through plasma-derived therapies, gastrointestinal treatments, and targeted acquisitions that expand its global therapeutic reach.

Key Pharmaceutical Companies:

The following key companies have been profiled for this study on the pharmaceutical market.

- F. Hoffmann-La Roche Ltd

- Novartis AG

- AbbVie Inc.

- Johnson & Johnson Services, Inc.

- Merck & Co., Inc.

- Pfizer Inc.

- Bristol-Myers Squibb Company

- Sanofi

- GlaxoSmithKline plc.

- AstraZeneca

- Takeda Pharmaceutical Co., Ltd.

Recent Developments

-

In December 2025, Sanofi announced it would acquire Dynavax Technologies for approximately USD 2.2 billion, offering USD 15.50 per share in cash, with the deal approved by Dynavax’s board. The acquisition added Dynavax’s marketed adult hepatitis B vaccine HEPLISAV‑B and a phase 1/2 shingles vaccine candidate to Sanofi’s portfolio, targeting nearly 100 million unvaccinated U.S. adults born before 1991.

-

In October 2025, Novartis announced it would acquire Avidity Biosciences, Inc. for approximately USD 12 billion, with Avidity shareholders receiving USD 72 per share, a 46 percent premium over the closing price on October 24, 2025. The transaction, expected to close in the first half of 2026, included a SpinCo for Avidity’s cardiology programs, offering one SpinCo share per ten Avidity shares.

-

In March 2025, Roche announced an exclusive collaboration with Zealand Pharma to co‑develop and commercialize petrelintide, a long‑acting amylin analog for obesity, with USD 1.65 billion in upfront payments and potential milestones of USD 3.6 billion, totaling USD 5.3 billion. Profits and losses would be shared 50/50 in the U.S. and Europe, with Zealand Pharma receiving tiered royalties in other regions. Petrelintide, in phase 2, is targeted for once‑weekly administration for a condition expected to affect over 4 billion people globally by 2035.

Pharmaceutical Market Report Scope

Report Attribute

Details

Market size in 2025

USD 1,738.0 billion

Estimated market size in 2026

USD 1,837.0 billion

Projected market size by 2033

USD 2,776.7 billion

Growth rate

CAGR of 6.1% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, trends

Segments covered

Molecule type, product, type, disease, route of administration, age group, distribution channel, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; China; Japan; India; Australia; South Korea; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key company profiled

F. Hoffmann-La Roche Ltd; Novartis AG; AbbVie Inc.; Johnson & Johnson Services, Inc.; Merck & Co., Inc.; Pfizer Inc.; Bristol-Myers Squibb Company; Sanofi; GlaxoSmithKline plc.; AstraZeneca; Takeda Pharmaceutical Co., Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Pharmaceutical Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global pharmaceutical market report based on molecule type, product, type, disease, route of administration, age group, distribution channel, and region:

-

Molecule Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Biologics & Biosimilars (Large Molecules)

-

Monoclonal Antibodies

-

Vaccines

-

Cell & Gene Therapy

-

Others

-

-

Conventional Drugs (Small Molecules)

-

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Branded

-

Generic

-

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Prescription

-

OTC

-

-

Disease Outlook (Revenue, USD Million, 2021 - 2033)

-

Cardiovascular diseases

-

Cancer

-

Diabetes

-

Infectious diseases

-

Neurological disorders

-

Respiratory diseases

-

Autoimmune diseases

-

Mental health disorders

-

Gastrointestinal disorders

-

Women’s health Diseases

-

Genetic and rare genetic diseases

-

Dermatological conditions

-

Obesity

-

Renal diseases

-

Liver conditions

-

Hematological disorders

-

Eye conditions

-

Infertility conditions

-

Endocrine disorders

-

Allergies

-

Others

-

-

Route of Administration Outlook (Revenue, USD Million, 2021 - 2033)

-

Oral

-

Tablets

-

Capsules

-

Suspensions

-

Other

-

-

Topical

-

Parenteral

-

Intravenous

-

Intramuscular

-

-

Inhalations

-

Other

-

-

Age Group Outlook (Revenue, USD Million, 2021 - 2033)

-

Children & Adolescents

-

Adults

-

Geriatric

-

-

Distribution Channel Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospital Pharmacy

-

Retail Pharmacy

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

Conventional drugs (small molecules) segment dominated the market with the largest revenue share of 54.2% in 2025.

Key players operating in the market are F. Hoffmann-La Roche Ltd, Novartis AG, AbbVie Inc., Johnson & Johnson Services, Inc., Merck & Co., Inc., Pfizer Inc, Bristol-Myers Squibb Company, Sanofi, GlaxoSmithKline plc., AstraZeneca, and Takeda Pharmaceutical Co., Ltd.

Key factors that are driving the market growth include rising chronic disease prevalence, aging populations, and increased healthcare spending. Advancements in biologics, personalized medicine, and RNAi-based therapeutics are further enhancing treatment outcomes.

The global pharmaceuticals market size was estimated at USD 1,738.0 billion in 2025 and is expected to reach USD 1,837.0 billion in 2026.

The global pharmaceuticals market is expected to grow at a compound annual growth rate of 6.1% from 2026 to 2033 to reach USD 2,776.7 billion by 2033.

North America dominated with a 41.8% revenue share in 2025.

The branded segment led with a 66.5% revenue share in 2025.

Prescription held the largest revenue share 86.5% in 2025.

Cancer held the largest share (over 18.6%) in 2025.

About the Author(s)

Pharmaceuticals Research Team

Healthcare · PharmaceuticalsThis report was authored by the pharmaceuticals research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the pharmaceuticals segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.