- Home

- »

- Plastics, Polymers & Resins

- »

-

Polyamide Market Size, Share & Growth Report, 2026-2033GVR Report cover

![Polyamide Market (2026 - 2033)Report]()

Polyamide Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Polyamide 6, Polyamide 66, Bio-based Polyamide, Specialty Polyamides), By End-use (Engineering Plastics, Fibers), By Region (North America, Europe, Acia Pacific), And Segment Forecasts

Market Size, 2025

$43.6BMarket Estimate, 2026

$46.4BMarket Forecast, 2033

$64.1BCAGR, 2026–2033

4.7%Polyamide Market Summary

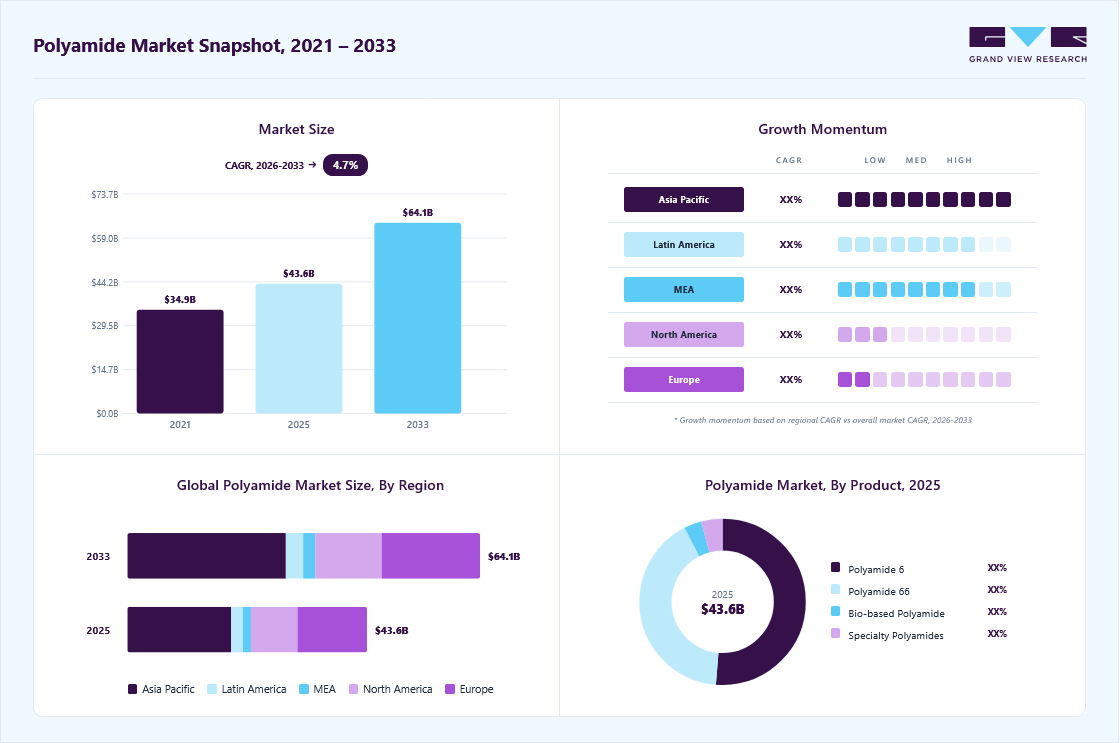

The global polyamide market size was valued at USD 43.57 billion in 2025 and is projected to grow from USD 46.42 billion in 2026 to USD 64.11 billion by 2033, growing at a CAGR of 4.7% from 2026 to 2033. The Asia Pacific market held the largest share of 43.35% of the global market in 2025. A growing focus on improving energy efficiency in industrial machinery is driving the use of polyamides, as they offer strong wear resistance and longer component life.

Key Market Trends & Insights

- By product: The polyamide 6 segment dominated the polyamide market, accounting for the largest revenue share of 51.20% in 2025, and is forecasted to grow at a 4.3% CAGR from 2026 to 2033.

- By end-use: Engineering plastics dominated the market across the end-use segmentation in terms of revenue, accounting for a market share of 58.59% in 2025, and is forecasted to grow at a 4.5% CAGR from 2026 to 2033.

Regional Highlights

- Largest regional market: Asia Pacific (43.35% revenue share, 2025)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 43.57 Billion

- Estimated market size in 2026: USD 46.42 Billion

- Projected market size by 2033: USD 64.11 Billion

- CAGR (2026-2033): 4.7%

Rising production of consumer appliances is also driving demand, as manufacturers prefer durable and lightweight polyamide resins for structural and functional parts. The polyamide market is shifting from commodity uses to engineering applications that demand temperature resistance and mechanical strength. Growth in the polyamide imide market reflects the increasing demand for high-temperature insulators and coatings in the automotive electrification and industrial equipment sectors. The demand for the high-performance polyamide is also driven by the electronics and aerospace industries, where weight savings and performance are critical. At the same time, the broader polyamide resin market is diversifying into composite and additive manufacturing grades to capture new end uses.")

Market Dynamics

The polyamide market is witnessing consistent growth, fueled by rising demand from sectors such as automotive, electrical and electronics, industrial, and consumer goods. Its superior mechanical strength, thermal stability, chemical resistance, and lightweight characteristics make it a favored option for engineering purposes, especially in the context of automotive lightweighting and components for electric vehicles. Increasing investments in infrastructure and industrial manufacturing are further propelling market growth. Moreover, innovations in bio-based polyamides and a growing focus on sustainable materials are opening up new avenues for expansion. Nonetheless, fluctuations in raw material costs and environmental issues linked to traditional petrochemical-based polyamides could hinder market development.

The polyamide market is being strongly driven by increasing demand for lightweight, high-strength engineering materials across automotive, electrical, industrial, and consumer applications. Polyamides provide an effective balance of mechanical strength, thermal resistance, chemical durability, and processability, making them suitable replacements for metals and heavier traditional materials. This transition is accelerating as manufacturers focus on reducing component weight, improving fuel efficiency, and increasing design flexibility in end-use products.

Automotive electrification continues to strengthen demand momentum for polyamide compounds and specialty grades. Electric vehicles require lightweight materials that can withstand higher thermal loads and electrical insulation requirements in battery systems, connectors, and under-the-hood components. Polyamides are increasingly used in cooling systems, cable management, structural parts, and electrical housings because they maintain dimensional stability under demanding operating conditions. Growth in advanced mobility solutions is therefore creating long-term demand for high-performance polyamide formulations.

Automotive electrification continues to strengthen demand momentum for polyamide compounds and specialty grades. Electric vehicles require lightweight materials that can withstand higher thermal loads and electrical insulation requirements in battery systems, connectors, and under-the-hood components. Polyamides are increasingly used in cooling systems, cable management, structural parts, and electrical housings because they maintain dimensional stability under demanding operating conditions. Growth in advanced mobility solutions is therefore creating long-term demand for high-performance polyamide formulations.

The polyamide market offers substantial growth prospects driven by the growing demand for sustainable, lightweight, and high-performance materials in major end-use sectors. The increasing implementation of electric vehicles, progress in bio-based polyamide technologies, and the rising necessity for durable engineering plastics in automotive, electrical and electronics, and industrial sectors are opening up new opportunities for market growth. Moreover, strict regulations focused on lowering vehicle emissions and enhancing energy efficiency are prompting manufacturers to substitute traditional metal components with advanced polyamide solutions, which further boosts the long-term potential of the market.

Market Concentration & Characteristics

The market growth stage is medium, and the pace of growth is accelerating. The polyamide industry exhibits fragmentation, with key players dominating the market landscape. Major companies such as BASF; Evonik AG; Arkema; Solvay; Domo Chemicals; DSM-Firmenich; Lanxess; DuPont; TORAY INDUSTRIES, INC.; Ascend Performance Materials; Koch IP Holdings, LLC.; Advansix; Celanese Corporation; Huntsman International LLC; and Mitsui Chemicals play a significant role in shaping the market dynamics. These leading players often drive innovation within the market, introducing new products, technologies, and applications to meet the evolving demands of the industry.

Innovation in polyamides for electronic protection devices centers on tailored chemistries and compound engineering that meet stricter safety and miniaturization demands. Suppliers are developing flame-retardant and low-smoke PA grades, as well as polyamide imide coatings, for high-temperature circuit protection. Nano-fillers and compatibilizers are improving mechanical strength without raising part weight. These moves enable smaller, safer housings for EV chargers, telecom, and industrial breakers while shortening OEM qualification cycles.

Buyers evaluate alternatives that strike a balance between cost, moisture behavior, and thermal performance. PBT and PC/PBT blends offer lower moisture uptake and good electrical properties for connectors. PPS and PEEK offer superior chemical and hydrolysis resistance for hot, harsh environments, albeit at a higher cost. Polycarbonate and ABS remain popular choices where impact resistance and lower cost are priorities. Material choice depends on part function, qualification timelines, and total cost of ownership.

Analyst Perspective

The polyamide industry is experiencing consistent growth, fueled by the rising need for lightweight, durable, and high-performance materials in sectors like automotive, electrical and electronics, industrial, and consumer markets. Producers are increasingly turning to polyamides as alternatives to traditional materials such as metals due to their outstanding mechanical strength, thermal resistance, and design versatility. The ongoing emphasis on lightweight vehicles, electrification, and industrial efficiency continues to boost the demand for advanced polyamide grades. Although market growth is driven by technological innovations and the rise of bio-based options, challenges such as fluctuations in raw material prices and sustainability requirements still pose significant considerations for players in the industry.

Product Insights

The polyamide 6 segment dominated the polyamide market, accounting for the largest revenue share of 51.20% in 2025, and is forecasted to grow at a 4.3% CAGR from 2026 to 2033. Demand for engineered Nylon 6 is rising as manufacturers replace metal parts with lighter thermoplastics to cut vehicle weight and improve fuel efficiency. Growth in automotive electrification and consumer electronics is driving demand for tougher, glass-filled PA6 grades that can withstand heat and mechanical stress. Capacity additions in Asia and localized supply chains are supporting faster delivery to OEMs and tier suppliers, strengthening the polyamide PA 6 market.

The bio-based polyamide segment is anticipated to grow at a substantial CAGR of 8.8% through the forecast period. Sustainability commitments from brand owners and stricter scope 3 targets are accelerating the adoption of bio-based polyamides in industrial and consumer applications. Improvements in renewable feedstock sourcing and lower carbon footprints for products such as bio-based PA11 are persuading automotive and sports goods makers to switch to certified grades. This regulatory and procurement pressure is creating market pull for bio-polyamide and for suppliers with traceable supply chains.

End-use Insights

Engineering plastics dominated the market across the end-use segmentation in terms of revenue, accounting for a market share of 58.59% in 2025, and is forecasted to grow at a 4.5% CAGR from 2026 to 2033. Growth in advanced electrical and industrial equipment is strengthening the polyamide 12 market within the engineering plastics sector. PA12 is chosen when chemical resistance, low moisture uptake, and dimensional stability are important considerations. Telecom infrastructure, pneumatic tubing, and oilfield components are shifting from metal to PA12 to lower weight and assembly costs. OEM qualification cycles are long, yet once approved, PA12 secures recurring order streams and higher average selling prices.

The fibers segment is expected to expand at a substantial CAGR of 5.0% through the forecast period. Electrification trends create new demand for polyamide in e-mobility market applications, including wiring, connectors, and cooling ducts. EV platforms require materials that can withstand higher temperatures and harsh chemistries while maintaining weight savings. Polyamide fibers gain share as braided hoses and thermal management textiles, which improve vehicle efficiency and battery life. Close collaboration between fiber manufacturers and OEMs is accelerating the adoption of modular design across powertrain and thermal subsystems.

Regional Insights

The Asia Pacific polyamide market held the largest revenue share of 43.35% in 2025 and is expected to grow at the fastest CAGR of 5.2% over the forecast period. Growth across the Asia Pacific reflects the rapid industrial electrification and expansion of high-value manufacturing in electronics and EV supply chains. The polyamide imide resin market is benefiting from increased demand for high-temperature insulating varnishes and molding resins used in motors and power electronics. Regional capacity additions and technology transfers are strengthening local availability and lowering qualification barriers for OEMs.

The Automotive Plastics Market in China. held the largest share in the Asia Pacific region in 2025. China’s polyamide market growth is underpinned by large-scale vehicle electrification, textile output, and packaging demand. Local producers scale PA6 and specialty grades to supply domestic OEMs and export markets. Investments in bio-based feedstocks and higher value compounding aim to capture premium segments. Strong upstream chemical integration keeps raw material costs and supply more competitive than many other regions.

North America Polyamide Market Trends

Demand for engineered polyamides in North America is driven by the rapid electrification of transport and a resilient aerospace repair cycle. OEMs and tier suppliers specify glass-filled and high-temperature grades to meet weight, thermal, and durability targets. Supply chain regionalization is lifting local compounding and finishing capacity. Investment in domestic capacity shortens lead times and strengthens supplier-customer collaboration for qualification.

In the U.S., the reshoring of electronics and automotive components is expected to boost demand for high-performance polyamide grades. Federal incentives for clean vehicle production and the energy transition increase volume requirements for battery housings and high-voltage connectors. Buyers prioritize suppliers with qualified personnel, local technical support, and a traceable resin supply. This raises near-term demand for specialty polyamide resin and engineered compounds.

Europe Polyamide Market Trends

Stricter emissions targets and circularity regulations are the core growth drivers for the polyamide industry in Europe. Automakers and aerospace firms specify lightweight, recyclable, and bio-based resins to meet fleet CO2 reduction targets and extended producer responsibility requirements. Demand for certified low-carbon feedstocks is rising among brand owners. These forces push converters and compounders to invest in closed-loop processes and validated recycled content.

Key Polyamide Company Insights

The polyamide industry is highly competitive, with several key players dominating the landscape. Major companies include BASF; Evonik AG; Arkema; Solvay; Domo Chemicals; DSM-Firmenich; Lanxess; DuPont; TORAY INDUSTRIES, INC.; Ascend Performance Materials; Koch IP Holdings, LLC; Advansix; Celanese Corporation; Huntsman International LLC; and Mitsui Chemicals. The market is characterized by a competitive landscape with several key players driving innovation and market growth. Major companies in this sector are investing heavily in research and development to enhance the performance, cost-effectiveness, and sustainability of their products.

Key Polyamide Companies

The following key companies have been profiled for this study on the polyamide market.

-

BASF

-

Evonik AG

-

Arkema

-

Solvay

-

Domo Chemicals

-

DSM-Firmenich

-

Lanxess

-

DuPont

-

TORAY INDUSTRIES, INC.

-

Ascend Performance Materials

-

Koch IP Holdings, LLC.

-

Advansix

-

Celanese Corporation

-

Huntsman International LLC

-

Mitsui Chemicals

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: BASF; DuPont; Solvay; LANXESS

- Broad engineering polymer portfolios serving automotive, electrical, industrial, textile, and consumer sectors.

- Strong integration across specialty chemicals, intermediates, and advanced material value chains.

- Continuous investment in bio-based polyamides, recycled compounds, and high-performance specialty grades.

- Established global brands with strong technical credibility and customer relationships.

- Advanced R&D infrastructure supporting customized formulations and high-performance compounds.

- Large-scale manufacturing and global distribution capabilities improve supply reliability.

- Large operational structures can slow responsiveness to niche customer requirements.

- High exposure to feedstock volatility and regulatory compliance costs.

- Premium product positioning may face pricing pressure from regional suppliers.

- Dependence on industrial and automotive cycles can impact revenue consistency.

Emerging Players: Evonik AG; Arkema; Domo Chemicals; Ascend Performance Materials

- Focus on specialty polyamide grades, intermediates, and application-specific compounds.

- Expansion of regional manufacturing and customer-focused technical support capabilities.

- Strategic emphasis on lightweight mobility, electrical systems, industrial machinery, and sustainable material applications.

- Strong specialization in selected engineering plastics and intermediate segments.

- Faster decision-making and improved responsiveness to customer-specific requirements.

- Competitive production economics in selected regional markets.

- Strong technical support for niche and performance-driven applications.

- Smaller global manufacturing footprint compared with diversified multinational competitors.

- Limited economies of scale in high-volume commodity segments.

- Higher dependence on selected end use sectors increases concentration risk.

- Lower brand visibility in large multinational procurement contracts.

Recent Developments

-

In October 2025, BASF launched two new sustainable nylon 6 grades, Ultramid LowPCF and Ultramid BMB, in North America, with reduced cradle-to-gate carbon footprint of ~30% and ~50% respectively, expanding the polyamide resin market with lower-carbon solutions.

-

In April 2025, TE Connectivity and BASF announced a collaboration to produce automotive connectors using Ultramid Ccycled polyamide, a circular polyamide solution derived from post-consumer waste, marking a step forward in sustainable materials for the polyamide market.

Polyamide Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 43.57 billion

Estimated market size in 2026

USD 46.42 billion

Projected market size by 2033

USD 64.11 billion

Growth rate

CAGR of 4.7% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Volume in Kilotons, Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, trends

Segments covered

Product, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; France; UK; Spain; Italy; China; Japan; India; South Korea; Brazil; Argentina; Saudi Arabia; South Africa; UAE

Key companies profiled

BASF; Evonik AG; Arkema; Solvay; Domo Chemicals; DSM-Firmenich; Lanxess; DuPont; TORAY INDUSTRIES, INC.; Ascend Performance Materials; Koch IP Holdings, LLC.; Advansix; Celanese Corporation; Huntsman International LLC; Mitsui Chemicals

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Polyamide Market Report Segmentation

This report forecasts volume & revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global polyamide market report based on product, end-use, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Polyamide 6

-

Polyamide 66

-

Bio-based Polyamide

-

Specialty Polyamides

-

-

End-use Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Engineering Plastics

-

Automotive

-

Electrical & Electronics

-

Consumer Goods & Appliances

-

Packaging

-

Others

-

-

Fibers

-

Textile

-

Carpet

-

Others

-

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

UAE

-

-

Research Methodology

Segment Definition

Segment - Product

Revenue capture definition

Polyamide 6

The PA6 segment accounts for the largest share of market revenue, driven by its widespread adoption across automotive, electrical & electronics, industrial machinery, and consumer goods applications. PA6 offers an optimal balance of mechanical strength, toughness, processability, and cost-effectiveness, making it a preferred engineering plastic for components such as automotive under-the-hood parts, electrical housings, gears, bearings, and industrial equipment. Revenue growth is supported by increasing demand for lightweight materials and the expanding use of reinforced PA6 grades in high-performance applications.

Polyamide 66

The PA66 segment generates substantial revenue from applications requiring superior heat resistance, stiffness, wear resistance, and dimensional stability. The material is extensively utilized in automotive engine components, electrical connectors, industrial machinery parts, and high-temperature engineering applications where enhanced performance is critical. Demand is driven by the growing need for durable materials capable of operating under harsh thermal and mechanical conditions, particularly in automotive and industrial sectors.

Bio-based Polyamide

The bio-based polyamide segment captures revenue through the increasing adoption of sustainable engineering materials across automotive, consumer goods, textiles, and industrial applications. Derived partially or fully from renewable feedstocks, these materials offer performance characteristics comparable to conventional polyamides while helping manufacturers achieve sustainability and carbon reduction objectives. Revenue growth is supported by stringent environmental regulations, rising consumer preference for eco-friendly products, and corporate commitments toward circular economy initiatives.

Specialty Polyamides

The specialty polyamide segment generates revenue from high-value applications that require advanced performance characteristics such as enhanced chemical resistance, low moisture absorption, high thermal stability, and superior mechanical properties. These materials are widely used in aerospace, medical devices, electronics, oil & gas, and specialty automotive components where standard polyamides may not meet performance requirements. Market growth is driven by increasing demand for customized material solutions in technically demanding and high-specification applications.

Segment-End-use

Revenue capture definition

Engineering Plastics

The engineering plastics segment captures the largest share of polyamide market revenue, driven by extensive use in automotive, electrical & electronics, industrial machinery, consumer goods, and construction applications. Polyamides are valued for their high mechanical strength, wear resistance, thermal stability, and lightweight characteristics, making them suitable for manufacturing functional components such as gears, bearings, connectors, housings, and under-the-hood automotive parts. Revenue growth is supported by the ongoing replacement of metals with high-performance engineering plastics to improve efficiency and reduce overall product weight.

Fibers

The fibers segment generates significant revenue through the widespread use of polyamide fibers in textiles, apparel, carpets, industrial fabrics, tire cords, and technical textile applications. Polyamide fibers offer excellent durability, abrasion resistance, elasticity, and tensile strength, making them suitable for both consumer and industrial end uses. Demand is further supported by the growing consumption of performance textiles, sportswear, automotive fabrics, and industrial reinforcement materials across developed and emerging markets.

Estimation Model

Layer Name

Key Question

Description

Polymer Demand Base Layer

What drives polyamide demand?

Analyzes the core demand drivers for polyamides across end-use industries such as automotive, electrical & electronics, textiles, packaging, and industrial applications. It identifies the sectors and applications contributing to overall market consumption.

Distribution Penetration Layer

Where are polyamides distributed and utilized?

Evaluates the distribution channels through which polyamide resins and compounds reach end users. This includes direct sales, distributors, compounders, and regional supply networks that influence market accessibility.

Supply Chain Intensity Layer

How much polyamide volume is consumed and supplied?

Assesses the flow and volume of polyamides across the value chain, from raw material suppliers to end-use industries. It highlights consumption intensity, supply-demand dynamics, and regional trade patterns.

Revenue Layer

How is polyamide market revenue generated?

Examines how market revenue is generated across different polyamide grades, applications, and end-use sectors. It evaluates pricing trends, product mix, and value creation opportunities within the market.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Competitive Benchmarking

Conducted a detailed benchmarking assessment of major polyamide manufacturers based on product portfolio strength, production capacity, regional presence, technology capabilities, sustainability initiatives, end use penetration, pricing positioning, and strategic developments. The analysis also compared company positioning across automotive, electrical, industrial, textile, and consumer applications.

Supported competitive intelligence and strategic positioning analysis. Identified strengths, capability gaps, and differentiation opportunities among key market participants. Improved understanding of regional and application-level competitive intensity. Enabled informed partnership, sourcing, and investment decisions.

Pricing Analysis

Delivered comprehensive pricing evaluation for polyamide resins and compounds across major regions. The study assessed feedstock cost trends, supply-demand dynamics, regional production economics, import-export pricing differences, energy cost impacts, and pricing variations across PA6, PA66, and specialty polyamide grades. It also analyzed the influence of sustainability-focused formulations and recycled content adoption on market pricing.

Supported procurement optimization and supplier negotiation strategies. Improved visibility into raw material dependencies and regional pricing trends. Assisted in managing cost volatility linked to petrochemical feedstocks and energy markets. Enabled identification of competitive sourcing opportunities.

Opportunity Assessment

Assessed high-growth opportunities across automotive electrification, lightweight industrial components, electrical systems, consumer appliances, textiles, and sustainable packaging applications. The analysis examined regional investment trends, emerging application areas, bio-based polyamide adoption, and evolving demand for high-performance engineering plastics.

Supported long-term growth planning and expansion strategy development. Identified emerging revenue pockets and high-potential application segments. Improved understanding of sustainability-driven market opportunities and regional demand shifts. Enabled prioritization of investment and product development initiatives.

Frequently Asked Questions About This Report

The global polyamide market size was estimated at USD 43.6 billion in 2025 and is expected to reach USD 46.4 billion in 2026.

Some key players operating in the polyamide market include BASF; Evonik AG; Arkema; Solvay; Domo Chemicals; DSM-Firmenich; Lanxess; DuPont; TORAY INDUSTRIES, INC.; Ascend Performance Materials; Koch IP Holdings, LLC.; Advansix; Celanese Corporation; Huntsman International LLC; Mitsui Chemicals

Key factors that are driving the polyamide market growth include increasing demand in the automobile industry and electrical & electronics sectors across the world.

The global polyamide market is expected to grow at a compound annual growth rate of 4.7% from 2026 to 2033 to reach USD 64.1 billion by 2033.

Asia-Pacific dominated the Polyamide market with a share of over 43.3% in 2025. This is attributable to the region's robust manufacturing sector, particularly in countries such as China, Japan, South Korea, and India. Additionally, the expansion of the automotive sector is benefiting the market in the region.

The Asia Pacific polyamide market held the largest revenue share of 43.3% in 2025, and is expected to grow at the fastest CAGR of 5.2% over the forecast period. Growth across the Asia Pacific reflects the rapid industrial electrification and expansion of high-value manufacturing in electronics and EV supply chains.

China is the fastest-growing region in the polyamide market over the forecast period, underpinned by large-scale vehicle electrification, textile output, and packaging demand. Local producers scale PA6 and specialty grades to supply domestic OEMs and export markets.

Engineering Plastics end-use dominated the market across the end-use segmentation in terms of revenue, accounting for a market share of 58.6% in 2025. Growth in advanced electrical and industrial equipment is strengthening the polyamide 12 market within the engineering plastics sector.

The bio-based polyamide segment is anticipated to grow at the fastest CAGR of 8.8% through the forecast period. Sustainability commitments from brand owners and stricter scope 3 targets are accelerating the adoption of bio-based polyamides in industrial and consumer applications.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.