- Home

- »

- Advanced Interior Materials

- »

-

Polyester Staple Fiber Market Size Report, 2026-2033GVR Report cover

![Polyester Staple Fiber Market (2026 - 2033)Report]()

Polyester Staple Fiber Market (2026 - 2033)

Size, Share & Trends Analysis Report By Source, By Product (Solid Polyester Staple Fiber, Hollow Polyester Staple Fiber), By Application (Automotive, Home Textiles, Construction, Filtration), By Region, And Segment Forecasts

Market Size, 2025

$24.2BMarket Estimate, 2026

$25.0BMarket Forecast, 2033

$33.3BCAGR, 2026–2033

4.1%Polyester Staple Fiber Market Summary

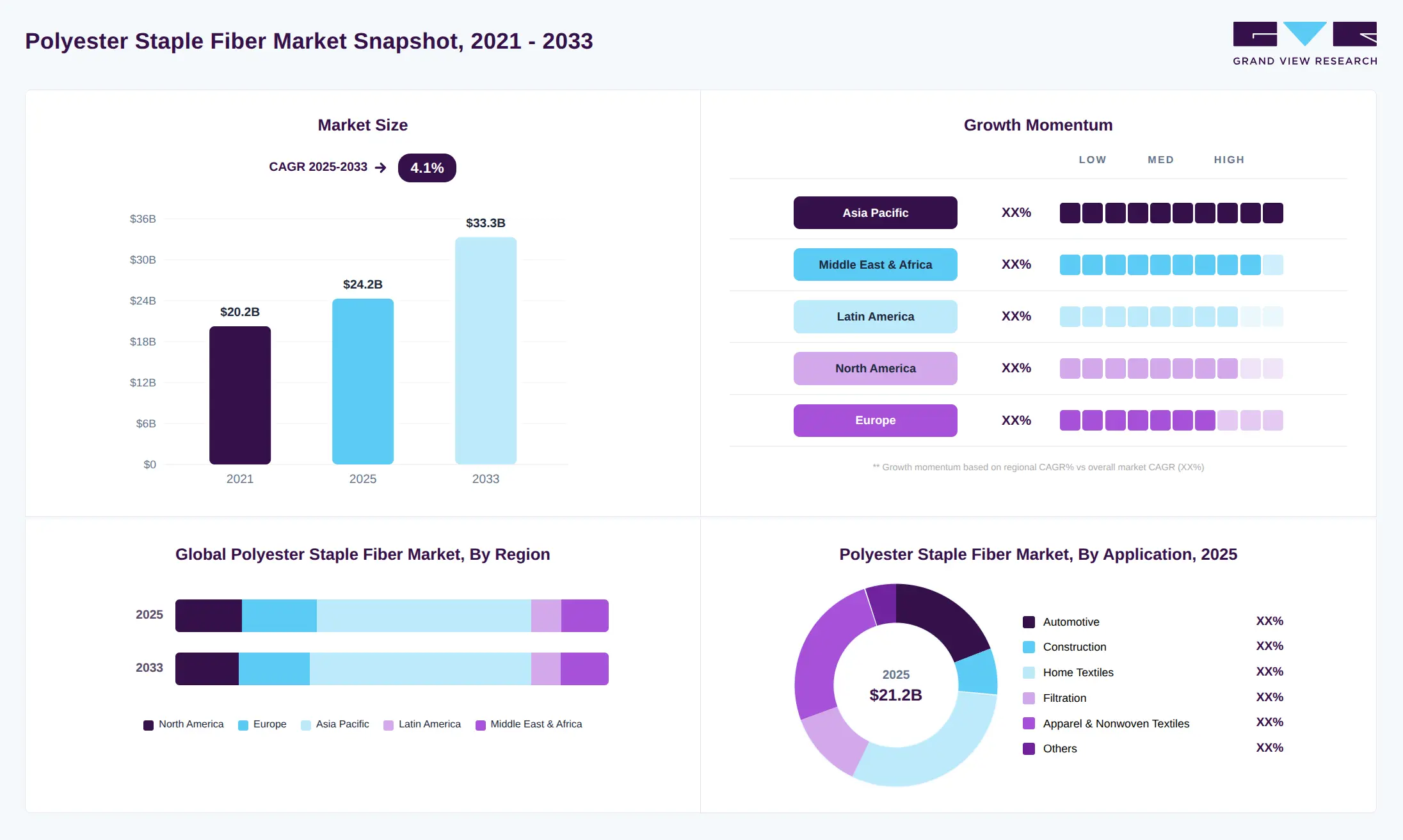

The global polyester staple fiber market size was valued at USD 24.2 billion in 2025 and is projected to grow from USD 25.0 billion in 2026 to USD 33.3 billion by 2033, at a CAGR of 4.1% from 2026 to 2033. The Asia Pacific held the largest share of 49.4% of the global market in 2025. The demand for polyester staple fiber (PSF) is rising steadily due to its widespread use in the textile and apparel industry, particularly for manufacturing affordable, durable clothing.

Key Market Trends & Insights

- By source: Virgin polyester staple fiber segment held the largest market share of 87.3% in 2025.

- By product: Solid polyester staple fiber segment held the largest market share of 58.9% in 2025.

- By application: Home textiles segment accounted for the largest revenue share of 31.7% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (49.4% revenue share, 2025)

- By country: China is expected to grow during the forecast period.

Market Size & Forecast

- Market size in 2025: USD 24.2 Billion

- Estimated market size in 2026: USD 25.0 Billion

- Projected market size by 2033: USD 33.3 Billion

- CAGR (2026-2033): 4.1%

Increasing population and urbanization have led to higher consumption of garments and home textiles such as carpets, curtains, and upholstery, driving PSF demand. Additionally, the growing preference for blended fabrics that combine polyester with cotton or viscose enhances fabric strength and wrinkle resistance, further boosting adoption. The expansion of the fast fashion industry has also accelerated the need for low-cost synthetic fibers like PSF.")

Key drivers include the cost-effectiveness of polyester compared to natural fibers, making it a preferred choice for manufacturers aiming to maintain margins. The increasing penetration of e-commerce platforms has expanded textile and apparel sales globally, indirectly supporting PSF demand. Industrial applications such as filtration, geotextiles, and construction materials are also boosting consumption. The rising demand for recycled polyester staple fiber, driven by sustainability concerns, is another significant growth driver. Furthermore, advancements in fiber engineering, including hollow and conjugated fibers, are improving product functionality and expanding application areas. Rapid industrialization in emerging economies is further supporting textile manufacturing, thereby driving PSF demand. Growth in technical textiles is also creating new opportunities for market expansion.

Technological advancements are driving the development of high-performance PSF with enhanced properties, including moisture-wicking, flame resistance, and antibacterial features. The increasing focus on sustainability has led to the growth of recycled polyester fibers derived from PET bottles. Manufacturers are also investing in bio-based polyester alternatives to reduce environmental impact. Automation and digitalization in textile manufacturing are improving production efficiency and quality consistency. The rise of circular economy practices is encouraging fiber recycling and reuse. Smart textiles incorporating functional fibers are gaining traction in sectors such as healthcare and sportswear.

Market Dynamics

The growing demand from the textile and apparel industry is a primary driver of the polyester staple fiber (PSF) market, as polyester remains one of the most widely used fibers globally. Its popularity stems from its cost-effectiveness, durability, wrinkle resistance, and ease of blending with other fibers such as cotton and viscose. Compared to natural fibers, PSF offers consistent quality and performance at a lower cost, making it highly attractive for large-scale textile production.

Rapid urbanization and population growth, particularly in emerging economies, are significantly increasing the demand for affordable clothing and home textiles. As middle-class populations expand and disposable incomes rise, consumer spending on apparel and lifestyle products continues to grow. This has led to higher consumption of polyester-based fabrics in everyday wear, sportswear, and household textiles such as bed linens, curtains, and carpets, thereby driving PSF demand.

Raw material price volatility is a significant restraint on the polyester staple fiber (PSF) market, primarily because of its strong reliance on petrochemical derivatives. Virgin PSF is produced using purified terephthalic acid (PTA) and monoethylene glycol (MEG), both of which are directly linked to crude oil prices. Fluctuations in crude oil markets, driven by geopolitical tensions, supply disruptions, and changing demand patterns, lead to unpredictable variations in raw material costs, making it difficult for manufacturers to maintain stable production costs.

Market Concentration & Characteristics

The polyester staple fiber market is moderately fragmented, with a mix of large multinational corporations and regional players competing on price, quality, and innovation. Leading companies dominate through extensive production capacities, integrated supply chains, and strong distribution networks. However, smaller manufacturers continue to operate in niche markets or regional segments. The presence of numerous players in Asia Pacific contributes to competitive pricing and high market fragmentation. Strategic collaborations, mergers, and capacity expansions are common as companies aim to strengthen their market position. Vertical integration, particularly in raw material sourcing such as purified terephthalic acid (PTA), is a key competitive strategy.

Polyester staple fiber faces competition from natural fibers such as cotton, wool, and silk, which are preferred for their comfort and biodegradability. Other synthetic fibers, such as nylon and acrylic, also serve as substitutes in certain applications. Increasing consumer awareness regarding sustainability and environmental impact is shifting preferences toward organic and biodegradable fibers. However, PSF maintains a competitive advantage due to its lower cost, durability, and versatility. The volatility in cotton prices often influences the substitution dynamics between natural and synthetic fibers. Innovations in alternative fibers such as bamboo and hemp may pose a long-term threat. Despite these factors, PSF remains well-positioned due to its wide range of applications.

Source Insights

Virgin polyester staple fiber dominated the polyester staple fiber industry, accounting for a revenue share of 87.3% in 2025, due to its consistent quality, superior strength, and wide applicability in textile manufacturing. Its uniformity and reliability make it highly preferred for producing high-performance fabrics and industrial textiles. Manufacturers favor virgin PSF for applications where durability and finish are critical, such as apparel and home furnishings. Additionally, stable supply chains of petrochemical raw materials further support its large-scale production. Despite rising sustainability concerns, virgin PSF continues to hold a strong market share due to its cost-efficiency and established infrastructure.

The recycled polyester staple fiber segment is projected to register a CAGR of 6.5% over the forecast period, driven by increasing environmental awareness and regulatory pressure to reduce plastic waste. The use of recycled PET bottles as raw material aligns with circular economy goals and sustainability initiatives adopted by major brands. Growing demand from eco-conscious consumers and global fashion brands is accelerating adoption. Technological advancements in recycling processes are improving fiber quality, making rPSF comparable to virgin alternatives. Governments and organizations are also promoting recycling practices, further boosting segment growth.

Product Insights

The solid polyester staple fiber segment held the largest revenue share of 58.9% in 2025, owing to its extensive use in textiles, particularly in spinning yarns for apparel and home textiles. Its strength, uniform structure, and ease of processing make it suitable for a wide range of applications. Solid fibers provide better tensile properties and are widely used in weaving and knitting processes. The segment benefits from high demand in fast fashion and mass textile production. Additionally, its cost-effectiveness and versatility ensure continued dominance in the market.

The hollow polyester staple fiber segment is projected to register a CAGR of 4.4% over the forecast period, driven by its lightweight structure and superior insulation properties. These fibers are widely used in applications such as pillows, cushions, quilts, and insulation materials. Their ability to trap air enhances thermal insulation, making them ideal for home furnishing and winter apparel. Increasing demand for comfort-based and functional textiles is driving this segment. Moreover, growth in the furniture and bedding industry is further supporting the adoption of hollow PSF.

Application Insights

Home textiles dominated the polyester staple fiber industry, accounting for the largest revenue share of 31.7% in 2025, due to the widespread use of PSF in products such as bed linens, curtains, carpets, and upholstery. Rising urbanization and improving living standards are increasing consumer spending on home décor and furnishings. The durability, affordability, and ease of maintenance of polyester fibers make them a preferred choice in this segment. Additionally, growth in the real estate and hospitality sectors is further fueling global demand for home textiles.

Filtration is one of the fastest-growing end-use segments in the polyester staple fiber market, driven by increasing demand for air and liquid filtration across industrial, automotive, and healthcare sectors. PSF is widely used in non-woven filter media due to its strength, chemical resistance, and durability. Rising concerns regarding air pollution and water treatment are significantly boosting demand for filtration materials. Additionally, stringent environmental regulations are encouraging industries to adopt advanced filtration solutions. The growth of industrial activities and focus on clean air and water are key factors supporting this segment’s expansion.

Regional Insights

Asia Pacific dominated the global polyester staple fiber market with the largest revenue share of 49.4% in 2025, due to the presence of major textile manufacturing hubs in countries such as China, India, and Indonesia. The region benefits from low labor costs, abundant raw material availability, and strong export-oriented industries. Rapid urbanization and rising disposable incomes are driving domestic textile consumption. Government support for manufacturing and infrastructure development further strengthens the market. The presence of leading PSF producers and integrated supply chains enhances production efficiency. Additionally, increasing investments in recycling facilities are supporting the growth of recycled PSF in the region.

The China polyester staple fiber market is expected to grow during the forecast period. China remains the largest producer and consumer of polyester staple fiber, driven by its massive textile manufacturing base. The country is witnessing a shift toward high-quality and sustainable fiber production, including recycled PSF. Government regulations focusing on environmental sustainability are encouraging manufacturers to adopt cleaner technologies. The domestic demand for textiles and apparel continues to grow, supported by rising incomes. China is also expanding its export capabilities, supplying PSF to global markets. Technological advancements and automation are improving production efficiency. Additionally, consolidation among key players is strengthening market competitiveness.

North America Polyester Staple Fiber Market Trends

The North America polyester staple fiber industry’s growth is driven by demand from the technical textiles, automotive, and home furnishing sectors. Increasing focus on sustainability is boosting the adoption of recycled polyester fibers. The region is witnessing innovations in high-performance fibers used in filtration and industrial applications. Growth in the construction sector is also supporting demand for geotextiles. Manufacturers are focusing on product differentiation and quality to remain competitive. The presence of established players and advanced technologies supports market growth. Additionally, regulatory emphasis on environmental compliance is shaping production practices.

U.S. Polyester Staple Fiber Market Trends

The U.S. PSF market is characterized by strong demand for non-woven fabrics used in hygiene and medical applications. Increasing investments in recycling infrastructure are promoting the use of recycled PSF. The automotive industry is a key contributor, utilizing PSF in interior components. Technological innovation in fiber properties is enhancing product applications. Consumer preference for sustainable textiles is influencing market trends. The presence of advanced manufacturing capabilities supports high-quality production. Additionally, government policies encouraging domestic manufacturing are aiding market growth.

Europe Polyester Staple Fiber Market Trends

Europe’s polyester staple fiber industry is driven by stringent environmental regulations and a strong focus on sustainability. The region is witnessing increased adoption of recycled and bio-based polyester fibers. Demand from the automotive and construction sectors is supporting market growth. Innovations in eco-friendly production processes are gaining traction. The presence of well-established textile industries contributes to steady demand. Consumers are increasingly favoring sustainable and ethically produced textiles. Additionally, circular economy initiatives are encouraging the recycling and reuse of polyester materials.

The Germany polyester staple fiber market plays a significant role in Europe, driven by its strong industrial and automotive sectors. The country is focusing on high-performance and technical textiles, boosting PSF demand. Sustainability initiatives are encouraging the use of recycled fibers. Advanced manufacturing technologies and R&D capabilities support innovation in fiber production. The demand for durable, lightweight materials in automotive applications is a key growth driver. Germany’s emphasis on environmental compliance is shaping market practices. Additionally, collaborations between industry and research institutions are driving technological advancements.

Central and South America Polyester Staple Fiber Market Trends

The polyester staple fiber industry in Central and South America is growing as the textile and apparel industries expand in countries such as Brazil and Mexico. Increasing urbanization and rising consumer spending are driving demand for affordable textiles. The region is witnessing the gradual adoption of recycled polyester fibers. Government initiatives supporting industrial development are contributing to market growth. The availability of raw materials and improving manufacturing capabilities are enhancing production. However, economic fluctuations may impact market expansion. Despite challenges, the region presents growth opportunities for PSF manufacturers.

Middle East & Africa Polyester Staple Fiber Market Trends

The Middle East & Africa PSF market is driven by growing investments in textile manufacturing and industrial development. The increasing demand for nonwoven fabrics in hygiene and medical applications is supporting growth. The region is gradually adopting sustainable practices, including recycling initiatives. Infrastructure development and construction activities are boosting demand for geotextiles. Government efforts to diversify economies are encouraging industrial expansion. The presence of petrochemical resources supports raw material availability.

Key Polyester Staple Fiber Company Insights

Some of the key players operating in the market include Xin Feng Ming Group and Reliance Industries Limited.

-

Xinfengming Group Co., Ltd. is a China-based, vertically integrated polyester manufacturer with operations spanning PTA production to polyester fibers, including staple fiber. The company focuses on large-scale, cost-efficient production supported by advanced manufacturing technologies. It serves key end-use industries, including textiles and home furnishings.

-

Reliance Industries Limited is India’s largest private sector company and a Fortune Global 500 enterprise, with a diversified presence across energy, petrochemicals, retail, and digital services. The company has evolved from a textile and polyester business into a fully integrated player spanning oil-to-chemicals, advanced materials, and consumer-focused sectors.

TEIJIN FRONTIER and Sinopec Yizheng are some of the emerging participants in the polyester staple fiber market.

-

TEIJIN FRONTIER is the global converting company that specializes in synthetic fibers and textiles with the integrated manufacturing system, developing raw materials through to finished products.

-

Sinopec Yizheng Chemical Fibre Company Limited is a major state-owned polyester and chemical fiber manufacturer based in Jiangsu, China, and a subsidiary of Sinopec. The company is primarily engaged in the production of polyester fibers, including polyester staple fiber, as well as key raw materials such as PTA.

Key Polyester Staple Fiber Companies:

The following key companies have been profiled for this study on the polyester staple fiber market.

- Xin Feng Ming Group

- Sinopec Yizheng

- Indorama Corporation

- Reliance Industries Limited

- Toray Industries, Inc.

- Unifi, Inc.

- Far Eastern New Century Corporation

- TEIJIN FRONTIER

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Reliance Industries Limited; Indorama Corporation; Toray Industries, Inc.; Far Eastern New Century Corporation - Focus on backward integration into raw materials like PTA and MEG to ensure cost control and supply stability.

- Invest heavily in R&D and product innovation, especially in high-performance, specialty, and sustainable fibers.

- Strong brand credibility and long-term relationships with major textile, automotive, and industrial clients.

- Ability to offer diversified product portfolios, including virgin, recycled, and specialty PSF variants.

- High dependence on petrochemical feedstocks, making them vulnerable to raw material price volatility.

- Slower adaptability to rapid sustainability shifts due to legacy infrastructure and large-scale operations.

Emerging Players: Jin Feng Ming Group; Sinopec Yizheng; Unifi, Inc. - Focus on capacity expansion and cost competitiveness, particularly in price-sensitive markets.

- Emphasize recycled fiber production and sustainability-led offerings to capture growing eco-conscious demand.

- Greater flexibility and agility in adapting to changing market trends and customer requirements.

- Competitive advantage in cost-efficient manufacturing, often supported by favorable local policies.

- Limited global presence and brand recognition compared to established players.

- Lower technological depth and R&D capabilities, restricting entry into high-performance segments.

Recent Developments

-

In April 2025, Reliance announced a ~1 MMTPA expansion in its polyester value chain to strengthen its presence in specialty fibers and downstream applications.

-

In January 2024, Far Eastern New Century expanded its recycled polyester production through bottle-to-fiber recycling initiatives.

Polyester Staple Fiber Market Report Scope

Report Attribute

Details

Market size in 2025

USD 24.2 billion

Estimated market size in 2026

USD 25.0 billion

Projected market size by 2033

USD 33.3 billion

Growth rate

CAGR of 4.1% from 2026 to 2033

Base year for estimation

2024

Actual estimates/Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, volume forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Source, product, application, and region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain, Austria; Poland; Romania; Turkey; Netherlands; Belgium; Hungary; Czech Republic; China; India; Japan; South Korea; Australia; Brazil; Argentina; Saudi Arabia; UAE; South Africa

Key companies profiled

Xin Feng Ming Group; Sinopec Yizheng; Reliance Industries Limited; Indorama Corporation; Toray Industries, Inc.; Unifi, Inc.; Far Eastern New Century Corporation; TEIJIN FRONTIER

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Polyester Staple Fiber Market Report Segmentation

This report forecasts volume & revenue growth at the global, regional & country levels and provides an analysis of the industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the polyester staple fiber market report based on source, product, application, and region:

-

Source Outlook (Volume, Kilotons; Revenue, USD Billion, 2021 - 2033)

-

Virgin Polyester Staple Fiber

-

Recycled Polyester Staple Fiber

-

-

Product Outlook (Volume, Kilotons; Revenue, USD Billion, 2021 - 2033)

-

Solid Polyester Staple Fiber

-

Hollow Polyester Staple Fiber

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Billion, 2021 - 2033)

-

Automotive

-

Home Textiles

-

Construction

-

Filtration

-

Apparel & Nonwoven Textiles

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Austria

-

Poland

-

Romania

-

Turkey

-

Netherlands

-

Belgium

-

Hungary

-

Czech Republic

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Central and South America

-

Brazil

-

Argentina

-

-

Middle East and Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Environment & Social Sustainability

Assessment of polyester staple fiber environmental footprint across the value chain, including feedstock sourcing, energy use, emissions, water consumption, waste generation, and recyclability. Review of social sustainability parameters such as labor practices, worker safety, traceability, compliance, and community impact.

Identify ESG hotspots and improvement areas across the polyester staple fiber value chain. Support sustainability positioning for customers, investors, and internal stakeholders. Enable benchmarking against best practices and evolving regulatory expectations.

Business Opportunity Mapping

Mapping of high-potential end-use sectors, applications, customer segments, and geographies for polyester staple fiber. Analysis of demand trends, whitespace opportunities, competitive intensity, and market attractiveness across key opportunity pockets.

Prioritize the most attractive growth segments and target markets. Reveal unmet needs and whitespace opportunities for expansion. Support go-to-market, product positioning, and partnership strategy development.

Feasibility of New Manufacturing Plant

Evaluation of market demand, plant economics, raw material availability, capacity considerations, technology pathways, and location attractiveness for a new polyester staple fiber facility. Assessment of competitive landscape, capex/opex drivers, and key investment risks.

Validate investment attractiveness and project viability. Inform capacity sizing, site selection, and commercialization strategy. Highlight key risk mitigation levers and critical return drivers for decision-making.

Frequently Asked Questions About This Report

The virgin polyester staple fiber segment led the market with an 87.3% revenue share in 2025, while the recycled polyester staple fiber segment is projected to grow at the fastest rate during the forecast period.

The solid polyester staple fiber segment held the largest revenue share of 58.9% in 2025.

The home textiles segment accounted for the largest revenue share of 31.7% in 2025, while the filtration segment is projected to witness significant growth during the forecast period.

Asia Pacific dominated the polyester staple fiber market with a 49.4% revenue share in 2025.

The global polyester staple fiber market size was valued at USD 24.2 billion in 2025 and is estimated at USD 25.0 billion for 2026.

The global polyester staple fiber market is expected to grow at a CAGR of 4.1% from 2026 to 2033, reaching USD 33.3 billion by 2033.

Asia Pacific dominated the global polyester staple fiber market with a revenue share of 49.4% in 2025.

Some of the key players operating in the polyester staple fiber market include Xin Feng Ming Group, Sinopec Yizheng, Indorama Corporation, Reliance Industries Limited, Toray Industries, Inc., Unifi, Inc., Far Eastern New Century Corporation, and TEIJIN FRONTIER.

Key factors driving the polyester staple fiber market include growing demand from the textile and apparel industry, increasing consumption of home textiles, rising adoption of recycled polyester fibers, expansion of industrial applications such as filtration and geotextiles, advancements in fiber engineering, and growing demand for affordable and durable synthetic fibers.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.