- Home

- »

- Plastics, Polymers & Resins

- »

-

Polymer Binders Market Size, Share & Trends Report, 2030GVR Report cover

![Polymer Binders Market Size, Share & Trends Report]()

Polymer Binders Market (2024 - 2030) Size, Share & Trends Analysis Report By Type (Acrylic, Vinyl Acetate, Latex, Polyurethane, Polyester), By Form, By Application, By Region, And Segment Forecasts

Market Size, 2023

$33.8BMarket Estimate, 2026

$43.6BMarket Forecast, 2030

$56.7BCAGR, 2024–2030

7.3%Polymer Binders Market Size & Trends

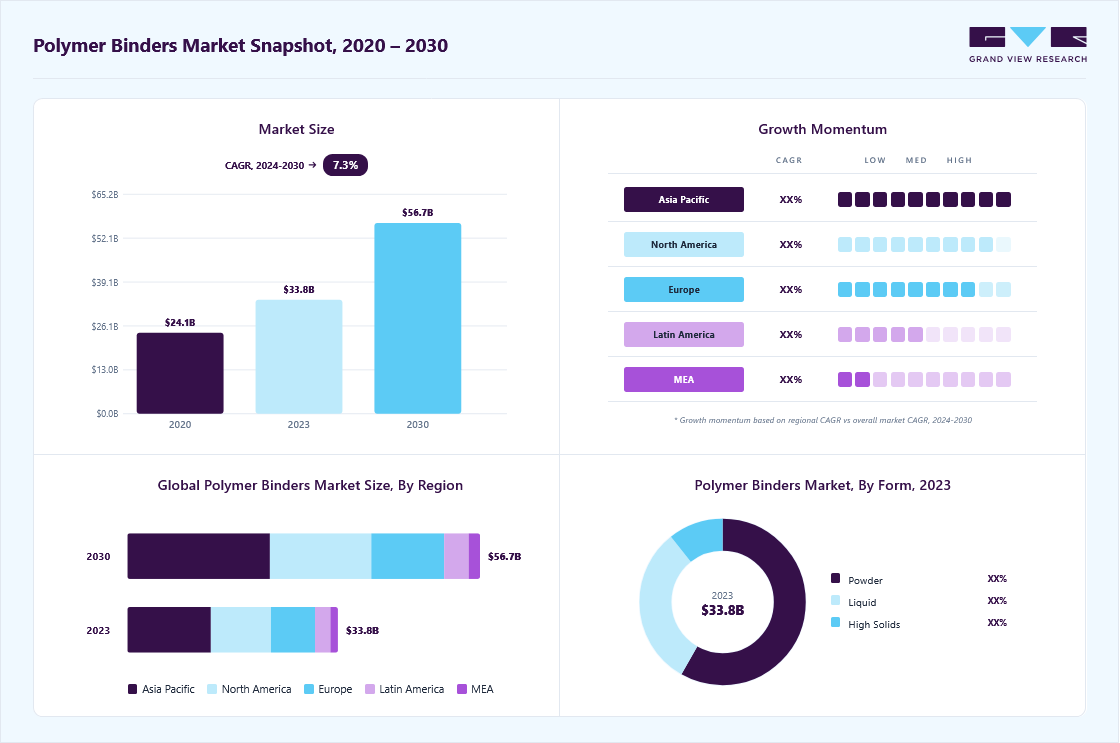

The global polymer binders market size was estimated at USD 33.84 billion in 2023 and expected to grow at a CAGR of 7.3% from 2024 to 2030. The polymer binders market is expected to experience significant growth in the coming years. The market is driven by growing demand in the construction, automotive and packaging industries, the development of water-based binders and environmental regulations promoting green products. In addition, increasing urbanization, infrastructure development, and innovation in polymer technology are expected to fuel the market growth.

Continuous research and development in polymers has resulted in improved binders with improved properties such as higher strength, better adhesion and increased durability. These innovations are expanding the applications of polymer binders and is expected to create new market opportunities for the key players.

Market Dynamics

The polymer binders industry is driven by increasing demand for high-performance coatings, adhesives, construction materials, textiles, and specialty paper applications across industrial and consumer sectors. Polymer binders play a critical role in improving adhesion strength, durability, flexibility, weather resistance, and surface performance in multiple end-use formulations. Rapid urbanization, infrastructure development, industrial manufacturing expansion, and growing consumption of advanced coating systems continue to strengthen long-term market demand globally.

A major second-order growth driver for the market is the expansion of the downstream paints, coatings, and construction chemicals industries, supported by infrastructure modernization and industrial development activities. Rising investments in residential construction, commercial buildings, transportation infrastructure, and protective industrial coatings are increasing demand for acrylic, styrene-butadiene, vinyl acetate, and polyurethane-based polymer binders. Growth in renovation activities and energy-efficient building systems is additionally supporting higher consumption of advanced architectural and industrial coating formulations.

One of the major restraints affecting the industry is volatility in petrochemical feedstock pricing. Polymer binders are primarily manufactured using acrylics, vinyl acetate monomers, styrene, butadiene, and polyurethane intermediates, making production economics highly sensitive to fluctuations in crude oil and natural gas markets. Changes in raw material pricing can significantly affect manufacturing costs, pricing stability, and profit margins across downstream applications.

Type Insights & Trends

Based on type, polymer binders market has been segmented into acrylic, vinyl acetate, latex, polyurethane, polyester, and others. Vinyl Acetate dominated polymer binders market with a share of over 33.23% in 2023.

Vinyl acetate polymer binders are widely utilized several construction applications including coatings, sealants, and adhesive. Strong adherence, flexibility, and water resistance are key characteristics that make them ideal for enhancing the performance and longevity of building materials.

Acrylic polymer binder is expected to grow at significant CAGR of 7.5%. The growing need for protective coatings in industrial applications, such as machinery and equipment is expected to fuel the demand for acrylic polymer binders. Moreover, the growing awareness and demand for sustainable and eco-friendly products is driving the use of acrylic polymer binders, which are thought to be less hazardous to the environment than solvent-based alternatives.

Form Insights & Trends

Based on type, polymer binders market is segmented into powder, liquid, and high solids. Powder segment accounted for highest revenue share of 58.14% in 2023. Powder-based polymer binders are vital in dry mix mortars, as offer improve workability, adhesion, and durability. The rising construction sector, particularly in emerging nations, drives up demand for these materials.

Liquid form is expected grow at highest CARG of 7.2% in coming years. Liquid-based binders protect against corrosion, chemicals, and wear, making them widely used in machinery, equipment, and infrastructure. Liquid polymer binders are essential in architectural paints and coatings, as they enhance adhesion, durability, and weather resistance. The need for high-performance coatings in residential and commercial structures is driving market growth.

Application Insights & Trends

Based on application, polymer binders market is segmented into paints & coatings, adhesives, textiles, construction, and others. Paints & coatings dominated polymer binders market in 2023 and accounted for a share of over 37.34%. The polymer binder market is critical in paint and coating applications, providing a range of benefits to meet the needs of diverse industries. Polymer binders increase the durability, adhesion, and mechanical qualities of paints and coatings. They helps in generating a cohesive coating that increases resistance to abrasion, chemicals, corrosion, and UV radiation, extending the lifespan of coated surfaces.

")

Adhesives segment is expected to grow at a significant CAGR of 7.4%. Polymer binders are an essential components in adhesive formulations, providing the necessary properties of adhesion, cohesion, flexibility and durability. The automotive industry requires high-performance adhesives for a variety of applications, including bonding various materials, sealing and component assembly. The shift towards lightweight and fuel-efficient vehicles is likely to create need for advanced polymer binders.

Regional Insights & Trends

North America polymer binders market is expected to grow at a significant rate of 7.4% over the forecast period. Growing demand for high-performance and environmentally friendly binders across several industries including construction across the region has augmented demand for polymer binders in the region.

U.S. Polymer Binders Market Trends

The U.S. dominated the polymer binders market in Asia Pacific and accounted for a share of over 7.6% in 2023. U.S. polymer binders market is expected to grow significantly over the forecast period backed by the rising demand from end-use industries such as automotive, packaging, construction, and healthcare.

Europe Polymer Binders Market Trends

The European polymer binders market has seen significant growth. The European market is seeing a growing focus on sustainability and the development of sustainable products. Strict environmental regulations and policies of the European Union aimed at reducing VOC (volatile organic compound) emissions and promoting sustainable development are expected to drive the demand for environmentally friendly bio-based polymer binders.

Asia Pacific Polymer Binders Market Trends

Asia Pacific dominated the polymer binders market in 2023 with revenue market share of 39.66%, and is expected to grow significantly in the coming years. The Asia Pacific region is a major automotive manufacturing hub, with significant production volumes in countries such as China, Japan, South Korea, and India. Growing demand for lightweight and high-performance materials in the automotive sector is projected to drive the need for advanced polymer binders in adhesives and coatings.

Key Polymer Binders Company Insights

The polymer binders market is a highly competitive industry with several key players operating globally, who have strong distribution networks and good knowledge about suppliers and regulations. The polymer binders market is a highly competitive sector with numerous major firms operating globally, each with strong distribution networks and a broad understanding of suppliers and regulations. Major players, in particular, compete on the basis of application development capability and new technologies used for product formulation. Major companies in particular, enter based on innovative technologies and application development competency engaged in product composition.

Key Polymer Binders Companies:

The following are the leading companies in the polymer binders market. These companies collectively hold the largest market share and dictate industry trends.

- BASF SE

- Wacker Chemie AG

- OMNOVA Solutions Inc.

- Celanese Corporation

- Arkema

- Dairen Chemical Corporation

- Toagosei Co. Ltd.

- Guangdong Yinyang Environment-Friendly New Materials Co., Ltd.

- Weifang Tainuo Chemical Co., Ltd.

- Mayfair Biotech Pvt. Ltd.

- VINAVIL S.p.A.

- The Lubrizol Corporation

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: BASF SE; Wacker Chemie AG; OMNOVA Solutions Inc.

- Broad portfolios of acrylic, vinyl acetate, styrene-butadiene, and specialty polymer binders for coatings, adhesives, textiles, paper, and construction applications.

- Significant investment in water-based technologies, low-VOC formulations, and sustainable binder development.

- Integrated manufacturing infrastructure and global supply capabilities supporting large-scale industrial demand.

- Strong polymer chemistry expertise and advanced emulsion technology capabilities.

- Established global manufacturing footprint and diversified end-use industry penetration.

- Large-scale production capabilities improve operational efficiency and supply reliability.

- High exposure to petrochemical feedstock and energy price volatility.

- Significant environmental compliance and sustainability-related investment requirements.

- Dependence on construction and industrial manufacturing cycles affects demand stability.

Emerging Players: Guangdong Yinyang Environment-Friendly New Materials Co., Ltd.; Weifang Tainuo Chemical Co., Ltd.; Mayfair Biotech Pvt. Ltd.

- Focus on region-specific polymer binder solutions and cost-competitive industrial formulations.

- Expansion into environmentally friendly binder systems and customized application-specific products.

- Flexible manufacturing strategies supporting regional coatings, textile, paper, and adhesive industries.

- Competitive pricing strategies and strong responsiveness to regional market requirements.

- Greater operational flexibility in customized formulation development.

- Strong positioning in selected regional coatings and adhesive markets.

- Smaller global manufacturing scale compared with multinational binder producers.

- Limited economies of scale in raw material procurement and technology investments.

- Higher dependence on regional construction and industrial demand conditions.

Recent Developments

-

In December 2024, Trinseo launched LIGOS BH 7340 SCE Binder, a biodegradable bio-hybrid binder for coated paper board products. LIGOS BH 7340 SCE binder can replace a significant portion of synthetic binder in coatings. The product offers several comparable to traditional paper or paperboard coatings with synthetic binders. This includes excellent coater run ability, cohesive coating strength, and glue ability.

-

In December 2023, the School of Energy and Chemical Engineeringcreated a unique binder technique that promises to transform battery performance.The company plans to significantly increase the performance of silicon cathode-based secondary batteries by producing high-electrical conductivity polymer binders using widely available.

-

In February 2023, WACKER AG introduces a polymer resin binder with improved solubility for use in printing inks, high-solids, and UV-curing systems.WACKER's VINNOL product line already includes a wide range of polymer resins that fulfill this same function in a variety of applications.

Polymer Binders Market Report Scope

Report Attribute

Details

Market size value in 2024

USD 37.10 billion

Revenue forecast in 2030

USD 56.68 billion

Growth rate

CAGR of 7.3% from 2024 to 2030

Historical data

2018 - 2022

Forecast period

2024 - 2030

Quantitative units

Revenue in USD million, volume in kilotons, and CAGR from 2024 to 2030

Report coverage

Revenue forecast, volume forecast, competitive landscape, growth factors and trends

Segments covered

Form, type, application, and region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country Scope

U.S.; Canada; Mexico; Germany; France; UK; Italy; Spain; The Netherlands, Denmark, China; India; Japan; South Korea; Indonesia; Brazil; Argentina; Saudi Arabia; South Africa; UAE

Key companies profiled

BASF SE; Wacker Chemie AG; OMNOVA Solutions Inc.; Celanese Corporation ; Arkema; Dairen Chemical Corporation; Toagosei Co. Ltd.; Guangdong Yinyang Environment-Friendly New Materials Co., Ltd.; Weifang Tainuo Chemical Co., Ltd.; Mayfair Biotech Pvt. Ltd.; VINAVIL S.p.A.; The Lubrizol Corporation

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Polymer Binders Market Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2030. For the purpose of this study, Grand View Research has segmented polymer binders market report on the basis of form, type, application, and region:

-

Type Outlook (Volume, Kilo Tons; Revenue, USD Million, 2018 - 2030)

-

Acrylic

-

Vinyl Acetate

-

Latex

-

Polyurethane

-

Polyester

-

Others

-

-

Form Outlook (Volume, Kilo Tons; Revenue, USD Million, 2018 - 2030)

-

Powder

-

Liquid

-

High Solids

-

-

Application Outlook (Volume, Kilo Tons; Revenue, USD Million, 2018 - 2030)

-

Paints & Coatings

-

Adhesives

-

Textiles

-

Construction

-

Others

-

-

Regional Outlook (Volume, Kilo Tons; Revenue, USD Million, 2018 - 2030)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

Italy

-

Spain

-

France

-

The Netherlands

-

Denmark

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Indonesia

-

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Pricing Analysis

Delivered comprehensive pricing analysis for acrylic binders, vinyl acetate binders, styrene-butadiene binders, polyurethane binders, and specialty water-based polymer systems across major global regions. The study evaluated monomer pricing trends, energy cost impacts, regional supply-demand balances, manufacturing economics, logistics costs, and downstream coatings and adhesive demand fluctuations influencing polymer binder pricing dynamics.

Supported procurement optimization and raw material sourcing strategies. Improved understanding of feedstock cost exposure, regional pricing trends, and margin structures across binder categories. Assisted in supplier comparison, contract planning, and pricing risk assessment. Enabled proactive response to petrochemical market fluctuations and changing industrial demand conditions.

Competitive Benchmarking

Conducted detailed benchmarking analysis of leading polymer binder manufacturers based on product portfolio breadth, regional presence, technology capabilities, production capacity, sustainability initiatives, end-use penetration, and strategic developments. The assessment compared company positioning across construction chemicals, paints and coatings, paper processing, adhesives, textile applications, and environmentally friendly binder technologies.

Supported competitive intelligence and strategic positioning analysis. Identified technology differentiation, operational strengths, and capability gaps among market participants. Improved understanding of sustainable binder positioning and regional manufacturing competitiveness. Enabled informed sourcing, partnership, and expansion planning decisions.

Cross-Segmentation

Delivered cross-segment analysis across binder chemistry, application, end-use industry, formulation technology, and regional demand trends. The study evaluated interactions between architectural coatings, industrial coatings, paper processing, nonwoven textiles, flexible packaging, construction chemicals, and low-VOC sustainable binder systems.

Improved understanding of high-growth application intersections and premium-value formulation opportunities. Supported product portfolio optimization and targeted commercialization planning. Enabled identification of emerging sustainability-driven demand combinations and advanced industrial application opportunities across the polymer binders value chain.

Frequently Asked Questions About This Report

The global polymer binders market size was estimated at USD 33.84 billion in 2023 and is expected to reach USD 37.10 billion in 2024.

The global polymer binders market is expected to grow at a compound annual rate of 7.3% from 2024 to 2030, reaching USD 56.68 billion by 2030.

Asia Pacific led the global polymer binders market, accounting for 39.7% of the global revenue in 2023.

Some of the major companies in the global polymer binders market include BASF SE, Wacker Chemie AG, OMNOVA Solutions Inc., Celanese Corporation, Arkema, Dairen Chemical Corporation, and Toagosei Co. Ltd, among others.

The market is driven by growing demand in the construction, automotive and packaging industries, the development of water-based binders and environmental regulations promoting green products. Additionally, increasing urbanization, infrastructure development, and innovation in polymer technology are expected to fuel the market growth.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.