- Home

- »

- Plastics, Polymers & Resins

- »

-

Polyurethane Market Size, Share & Trends Report 2026-2033GVR Report cover

![Polyurethane Market (2026 - 2033)Report]()

Polyurethane Market (2026 - 2033)

Size, Share & Trends Analysis Report By Raw Material (Toluene Di-isocyanate, Polyols), By Product (Rigid Foam, Flexible Foam, Coatings), By Application (Furniture and Interiors, Construction), By Region, And Segment Forecasts

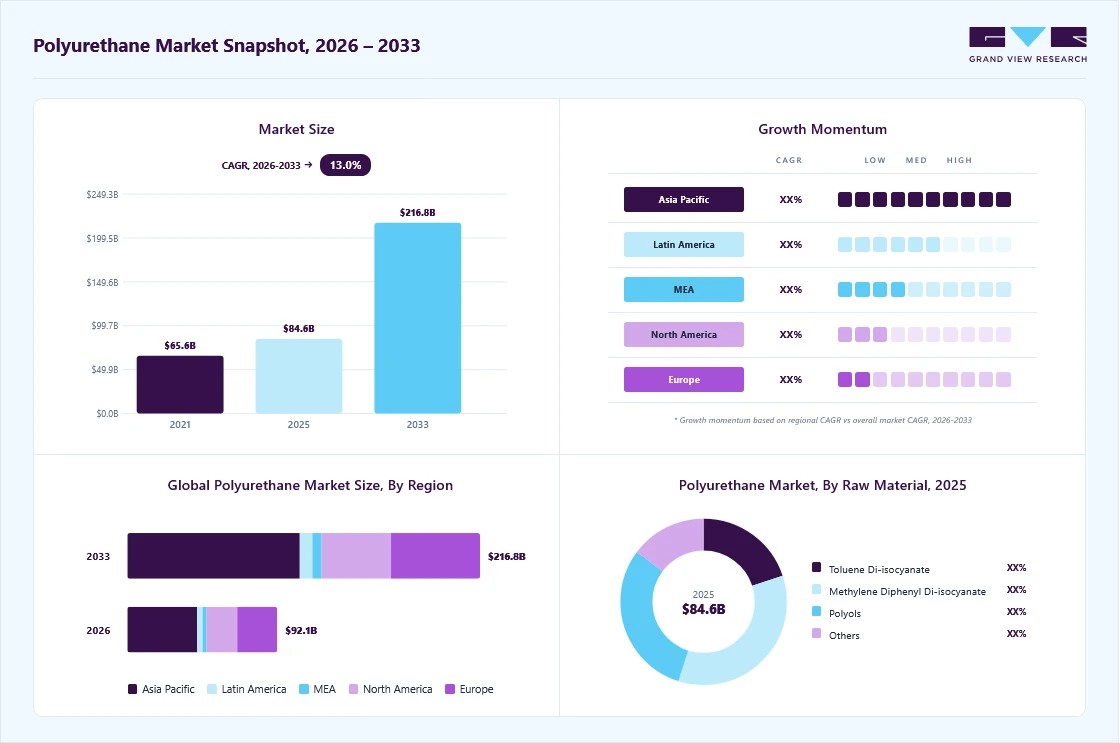

Market Size, 2025

$84.6BMarket Estimate, 2026

$92.1BMarket Forecast, 2033

$216.8BCAGR, 2026–2033

13.0%Polyurethane Market Summary

The global polyurethane market size was valued at USD 84.6 billion in 2025 and is projected to grow from USD 92.1 billion in 2026 to USD 216.8 billion by 2033, at a CAGR of 13.0% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 46.3% in 2025. The increasing demand for building insulation, considering sustainability concerns, is expected to drive polyurethane demand over the forecast period.

Key Market Trends & Insights

- By raw material: Methylene diphenyl di-isocyanate segment held the largest market share of 34.9% in 2025.

- By product: Rigid foam segment held the largest market share of 31.7% in 2025.

- By application: Construction segment held the largest market share of 26.5% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (46.3% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 84.6 Billion

- Estimated market size in 2026: USD 92.1 Billion

- Projected market size by 2033: USD 216.8 Billion

- CAGR (2026-2033): 13.0%

Sustainability in building developments is a broad field that encompasses several steps implemented during the primary construction stages, as their potential environmental impact is significant. The rising demand for the product from the automotive, construction, and packaging sectors in the country is expected to drive the market over the forecast period.

")

The construction sector is expanding rapidly, driven by strong market fundamentals for commercial real estate and rising state and federal funding for institutional buildings and public works.

Market Concentration & Characteristics

Market growth is driven by high demand for building insulation amid sustainability concerns across the residential and non-residential sectors. Sustainability in building developments is a broad field that encompasses several steps that must be implemented during the primary construction stages, as their potential environmental impact is significant.

With growing demand patterns, companies such as China National Building Material Industry Corporation and Sika AG are increasing their production capacities. Moreover, the industry is largely characterized by the dominance of regional players, leading within their respective regional markets.

Green buildings are increasingly entering the construction market owing to the increasing investments in smart energy-efficient commercial and residential buildings. These buildings offer profitable opportunities along with environmental and federal regulations, providing a meaningful response to growing consumer expectations for sustainability.

In addition, polyurethane manufacturers are largely supported by their local governments. Controlled studies have demonstrated that polyurethane adhesives used with mechanical fasteners in house framing can provide good resistance during severe weather events. Increased effectiveness in building materials has ultimately generated higher demand for polyurethane in the building & construction industry.

Raw Material Insights

The Methylene Diphenyl Di-isocyanate material segment held the largest share of over 34.90% in 2025. MDI is an essential aromatic di-isocyanate utilized as a key raw ingredient in the production of polyurethane, where it reacts with polyols to create both rigid and flexible foams, as well as coatings, adhesives, sealants, and elastomers. The demand for MDI is primarily influenced by the expanding construction insulation, automotive lightweight materials, appliances, and furniture industries, all of which benefit from polyurethane’s durability, thermal efficiency, and design adaptability.

Polyols is anticipated to grow at the fastest CAGR from 2026 to 2033. Polyols are compounds with multiple hydroxyl functional groups. Polyester polyols are the most common polyurethane raw material. They are employed in the manufacturing of several polymers, including polyurethane, which finds application in the building, automotive, furniture, and other industries. The polyol-based market is driven by several factors that contribute to its growth and development.

Product Insights

Rigid foam products accounted for 31.72% of revenue in 2025 and are likely to dominate the market over the forecast period. Rigid foam polyurethane types are high-performance, closed-cell plastics used in end-use industries such as transportation, packaging, and industrial insulation and appliances, owing to their structural stability, which helps manufacturers design thermally insulating products. Rigid foams offer sound insulation, higher mechanical strength, and thermal resistance, making them highly suitable for extreme weather conditions and harsh environments.

Moreover, the polyurethane-based flexible foams are expected to grow significantly in the coming years. They are a type of polymer foam widely used across various applications due to their flexibility, resilience, and comfort. TDI and MDI are the most used isocyanates in the production of polyurethane-based flexible foams. The automotive industry uses flexible foams extensively in seating, headrests, and interior components. Urbanization and rising automotive demand are driving demand for PU-based flexible foam products in the automotive industry.

Application Insights

The construction segment dominated the market, accounting for the largest revenue share of 26.52% in 2025. The demand for polyurethane in construction end-use is expected to grow significantly over the forecast period, owing to its various beneficial characteristics, including excellent thermal insulation, light weight, chemical inertness, and resistance to bacteria and pests. Growing urbanization and industrialization, especially in emerging economies such as China and India, and rising infrastructure development in the Middle East are expected to fuel the construction industry's growth, in turn creating demand for polyurethane foam and insulation.

The furniture and interiors segment is also expected to experience significant growth. Flexible foam is used for cushioning in a variety of consumer and commercial products, such as furniture, bedding, carpet cushion, fibers, and textiles. Foams and other PU products are expected to gain significance in the region on account of rising consumer awareness of the sustainability of lightweight, low-cost polyurethane. Growing residential construction and infrastructure activities are also driving demand for rigid polyurethane foam in Mexico.

Regional Insights

Asia Pacific dominated the market, accounting for 49.28% of revenue in 2025. The market is driven by the growth of major end-use industries, including automotive, electronics and appliances, packaging, furniture and interior, and construction. The Asia Pacific region is characterized by a large pool of skilled labor, low costs, and easy access to land. A shift in the production landscape toward emerging economies, particularly China and India, is expected to positively influence growth in the Asia Pacific market over the forecast period. Per capita consumption in India, Vietnam, Thailand, and Indonesia is gradually increasing, likely to remain a key driver of market growth. Traditionally, China's market was driven by high demand in infrastructure applications and by increased use in the production of automotive components, electronics, and consumer products.

China Polyurethane Market Trends

The polyurethane market in China dominated the Asia Pacific market in 2025, bolstered by significant manufacturing capabilities, swift urban development, and a wide range of downstream sectors, including construction, furniture, appliances, and automotive.

Europe Polyurethane Market Trends

The polyurethane market in Europe is likely to grow at a CAGR of over 3.5% from 2026 to 2033. Increasing infrastructure spending and the rising number of government initiatives, such as smart cities and subsequent FDI in the construction and development sector, are driving growth in the construction industry. The furniture and construction industries in Europe have witnessed significant growth owing to stringent regulatory frameworks aimed at reducing greenhouse gas (GHG) emissions. This factor has led to increased investment in rigid PU foam by regional automotive manufacturers.

Germany polyurethane market is driven by a robust automotive industry, construction sector, and industrial foundation. The demand is primarily influenced by uses in energy-efficient building insulation, lightweight automotive parts, furniture, and coatings, highlighting the country’s focus on sustainability and high-performance materials. Furthermore, Germany is home to key chemical manufacturers such as BASF and Covestro, which drive innovation, capacity expansion, and advanced polyurethane technologies across various end-use sectors.

North America Polyurethane Market Trends

The polyurethane market in North America is primarily propelled by its use in construction insulation, lightweight automotive parts, furniture, and appliances, with a significant push from the growing demand for energy-efficient materials. Sustainability regulations and the implementation of advanced manufacturing techniques additionally bolster the expansion.

The U.S. polyurethane market is propelled by robust needs in sectors such as construction, insulation, automotive, lightweight parts, furniture, and appliance production.

Key Polyurethane Company Insights

Key companies are adopting a range of organic and inorganic growth strategies, such as capacity expansion, mergers & acquisitions, and joint ventures, to maintain and expand their market share.

-

In February 2026, Mearthane Products Corp. announced the purchase of Axillon Aerospace's industrial composites operations, thereby enhancing its abilities in polyurethane molding and composites production.

-

In October 2025, Pearl Group reached a notable milestone in its expansion efforts by opening Pearl Deutschland in Leverkusen, Germany. This tactical growth marks the latest advancement in Pearl's ambitious PearlX2 initiative, which aims to double the business's size by 2026.

Key Polyurethane Companies:

The following key companies have been profiled for this study on the polyurethane market.

- Dow, Inc.

- BASF SE

- Covestro AG

- Huntsman International LLC

- Eastman Chemical Company

- Mitsui & Co. Plastics Ltd.

- Mitsubishi Chemical Corporation

- Recitel NV/SA

- Woodbridge

- DIC Corporation

- RTP Company

- The Lubrizol Corporation

- RAMPF Holding GmbH & Co. KG

- Tosoh Corporation

Polyurethane Market Report Scope

Report Attribute

Details

Market size in 2025

USD 84.6 billion

Estimated market size in 2026

USD 92.1 billion

Projected market size by 2033

USD 216.8 billion

Growth rate

CAGR of 13.0% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative Units

Volume in kilotons, revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Volume forecast, revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Raw material, product, application, region

Regional scope

North America; Europe; Asia Pacific; CSA; MEA

Country scope

U.S.; Canada; Mexico; Germany; France; UK; Italy; Spain; Denmark; Sweden; Norway; China; India; Japan; South Korea; Singapore; Taiwan; Thailand; Vietnam; Brazil; Argentina; Saudi Arabia; UAE; South Africa

Key companies profiled

Dow, Inc.; BASF SE; Covestro AG; Huntsman International LLC; Eastman Chemical Company; Mitsui & Co. Plastics Ltd.; Mitsubishi Chemical Corporation; Reticel NV/SA; Woodbridge; DIC Corporation; RTP Company; The Lubrizol Corporation; RAMPH Holding GmbH & Co. KG; Tosoh Corporation

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Polyurethane Market Report Segmentation

This report forecasts revenue and volume growth at the global, regional, and country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2018 to 2030. For this study, Grand View Research has segmented the global polyurethane market report based on raw material, product, application, and region:

-

Raw Material Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Toluene Di-isocyanate

-

Methylene Diphenyl Di-isocyanate

-

Polyols

-

Others

-

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Rigid Foam

-

Flexible Foam

-

Coatings

-

Adhesives & Sealants

-

Elastomers

-

Others

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Furniture and Interiors

-

Construction

-

Electronics & Appliances

-

Automotive

-

Footwear

-

Packaging

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Singapore

-

Taiwan

-

Thailand

-

Vietnam

-

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The Polyurethane Market size was estimated at USD 84.6 billion in 2025 and is expected to reach USD 92.1 billion in 2026.

The construction application segment led the global polyurethane market in 2025, accounting for more than 26.5% of revenue.

The methylene diphenyl di-isocyanate segment led with a 34.9% revenue share in 2025, while polyols is the fastest-growing segment.

Rigid foam products held the largest revenue share 31.7% in 2025.

The Polyurethane Market is expected to grow at a compound annual growth rate of 13.0% from 2026 to 2033, reaching USD 216.8 billion by 2033.

Asia Pacific was the largest market, with a revenue share of over 46.3% in 2025.

Some of the key players operating in the Polyurethane Market include Dow, Inc.; BASF SE; Covestro AG; Huntsman International LLC; Eastman Chemical Company; Mitsui & Co. Plastics Ltd.; and Mitsubishi Chemical Corporation.

Key factors driving the Polyurethane Market are increasing construction spending, driven by the growing need for sustainable infrastructure, and the increasing demand for furniture and bedding products.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.