- Home

- »

- Next Generation Technologies

- »

-

Portfolio Management Software Market Report, 2026-2033GVR Report cover

![Portfolio Management Software Market (2026 - 2033)Report]()

Portfolio Management Software Market (2026 - 2033)

Size, Share & Trends Analysis Report By Function (Investment Tracking, Performance Analysis, Risk Management, Asset Allocation, Portfolio Execution), By Deployment (Cloud, On-premise), By End-use, By Region, And Segment Forecasts

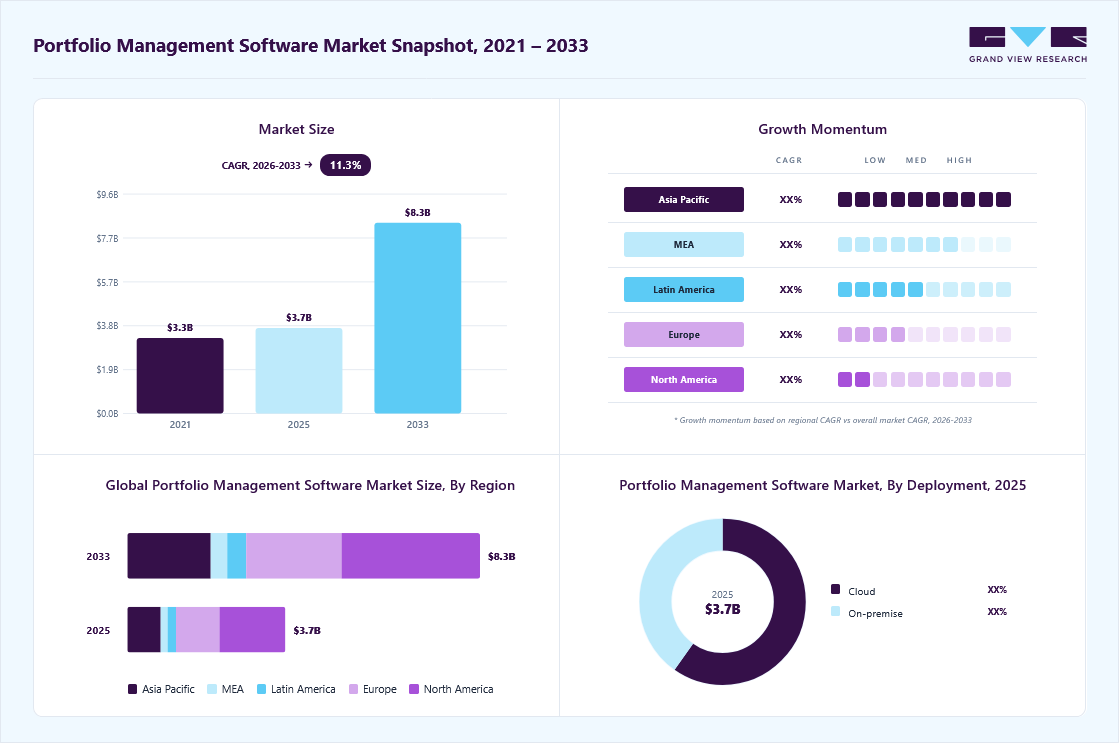

Market Size, 2025

$3.7BMarket Estimate, 2026

$3.9BMarket Forecast, 2033

$8.3BCAGR, 2026–2033

11.3%Portfolio Management Software Market Summary

The global portfolio management software market size was valued at USD 3.7 billion in 2025 and is projected to grow from USD 6.3 billion in 2026 to USD 9.9 billion by 2033, at a CAGR of 11.3% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 41.7% in 2025. The growth is driven by the increasing complexity of investment portfolios and the growing need for efficient asset management solutions.

Key Market Trends & Insights

- By function: The investment tracking segment accounted for the largest share of 23.6% in 2025.

- By deployment: The cloud deployment segment held the largest market share in 2025.

- By end-user: The large enterprises segment dominated the market in 2025.

Regional Highlights

- Largest regional market: North America (41.7% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 3.7 Billion

- Estimated market size in 2026: USD 3.9 Billion

- Projected market size by 2033: USD 8.3 Billion

- CAGR (2026-2033): 11.3%

Financial institutions, wealth managers, and individual investors are increasingly seeking platforms that enable real-time tracking, performance monitoring, and risk assessment across multiple asset classes. The rise in global wealth creation, coupled with expanding participation in financial markets, is further accelerating demand. In addition, the shift toward data-driven decision-making and the need for improved operational efficiency are reinforcing the adoption of portfolio management solutions.Technological advancements are playing a pivotal role in transforming the market landscape. The integration of artificial intelligence (AI) and machine learning (ML) is enabling predictive analytics, automated portfolio rebalancing, and enhanced risk modeling. Cloud computing enables scalable, flexible deployments, while API-driven architectures enable seamless integration with third-party financial systems. In addition, the growing use of big data analytics and real-time dashboards is improving transparency and enabling more informed investment decisions, thereby enhancing the overall value proposition of portfolio management software.

")

Investment activity in the market is increasing significantly, driven by both private and institutional funding. Financial technology companies are attracting substantial venture capital to develop innovative, user-centric portfolio management platforms. Established financial institutions are also investing in digital transformation initiatives, including upgrading legacy systems and adopting advanced software solutions. Strategic partnerships, mergers, and acquisitions are further shaping the competitive landscape, as companies aim to expand their product offerings and geographic presence. This influx of capital is accelerating innovation and fostering the development of next-generation portfolio management tools.

Despite strong growth prospects, the market faces several restraints that may hinder its expansion. High implementation costs and integration challenges with existing legacy systems can limit adoption, particularly among smaller organizations. Data security and privacy concerns remain significant, especially as the use of cloud-based platforms increases. In addition, the lack of standardization across financial systems and the complexity of managing diverse data sources can create operational challenges.

Market Dynamics

The growing diversification of investment portfolios across multiple asset classes is a major driver for the portfolio management software market. Institutional investors, hedge funds, pension funds, and wealth managers are increasingly allocating capital across equities, fixed income securities, commodities, ETFs, derivatives, private equity, real estate, and digital assets to optimize returns and reduce portfolio risk. Managing these highly diversified portfolios through traditional tools such as spreadsheets or disconnected legacy systems has become operationally inefficient and prone to errors.

In addition, globalization of investment activities has significantly increased cross-border capital allocation, requiring firms to manage multi-currency transactions, region-specific taxation structures, and varying regulatory requirements. Portfolio managers now require centralized software platforms capable of providing real-time visibility into asset allocation, portfolio exposure, liquidity positions, and investment performance across geographies. The increasing volume of market data, trading activities, and portfolio rebalancing operations is also driving the need for automated analytics and workflow management solutions.

One of the major restraints in the portfolio management software market is the high implementation and maintenance costs associated with advanced investment management platforms. Large-scale deployment often requires significant investment in software licensing, cloud infrastructure, cybersecurity, customization, and employee training. Small and medium-sized asset management firms, family offices, and independent financial advisors frequently face budget constraints, limiting the adoption of enterprise-grade solutions.

In addition, integration of portfolio management software with existing legacy systems, trading platforms, accounting tools, CRM systems, and compliance databases remains technically complex and time-consuming. Many financial institutions operate on fragmented IT infrastructures developed over several years, making system migration challenging and increasing operational disruption risks during deployment. Data synchronization issues, interoperability limitations, and customization requirements further increase implementation timelines and overall project costs.

The increasing adoption of artificial intelligence, machine learning, and predictive analytics in investment management is creating significant growth opportunities for the portfolio management software market. Financial institutions, wealth managers, and fintech platforms are increasingly focusing on delivering personalized investment strategies, automated portfolio recommendations, and real-time financial insights to improve client engagement and portfolio performance. AI-enabled portfolio management platforms can analyze large volumes of market, behavioral, and macroeconomic data to support dynamic asset allocation, predictive risk assessment, and automated portfolio rebalancing.

The rapid expansion of digital wealth management platforms and robo advisory services is further accelerating demand for scalable and cloud-based portfolio management solutions. Growing participation from retail investors, particularly among younger and digitally active demographics, is encouraging investment firms to develop mobile-enabled and user-friendly portfolio management applications. This trend is creating strong opportunities for SaaS based solution providers offering subscription-driven and low-cost investment management platforms.

Market Concentration & Characteristics

The market is moderately fragmented, with the presence of global financial technology companies, enterprise software providers, wealth management platform vendors, and specialized investment management solution providers competing across institutional and retail investment segments. Major players such as BlackRock, Inc., and Oracle Corporation dominate the market through comprehensive product portfolios, strong institutional client bases, advanced analytics capabilities, and global operational presence. These companies primarily compete on the basis of platform integration, scalability, automation capabilities, compliance management, and real-time investment analytics.

The market also includes a large number of regional fintech firms, SaaS based portfolio management startups, and niche vendors specializing in wealth management, ESG analytics, robo-advisory platforms, risk management, and AI-driven investment solutions. Market fragmentation is increasing due to the rapid adoption of cloud native financial platforms, digital wealth management services, open banking infrastructure, and API based financial ecosystems, which are lowering entry barriers for emerging technology providers. Smaller and midsized vendors are gaining traction by offering customizable, cost-effective, and mobile-enabled portfolio management solutions targeted toward independent financial advisors, family offices, SMEs, and retail investors.

In addition, the increasing integration of artificial intelligence, predictive analytics, blockchain, and automated investment advisory capabilities is enabling specialized technology providers to differentiate themselves in high-growth segments of the market. However, large enterprise vendors continue to strengthen their competitive positioning through strategic acquisitions, partnerships with financial institutions, expansion of cloud capabilities, and integrated end-to-end investment management offerings. As regulatory requirements, cybersecurity standards, and demand for enterprise-wide investment visibility continue to increase, gradual consolidation is expected in institutional and large-scale portfolio management software segments over the forecast period.

Function Insights

The investment tracking segment accounted for the largest share of 23.6% in 2025. The growth of the segment is driven by the increasing need for real-time visibility into portfolio performance across multiple asset classes. Investors, both institutional and retail, require continuous monitoring of equities, fixed income, alternatives, and digital assets within a unified platform. This demand has intensified with the expansion of global investment portfolios, making manual tracking inefficient and prone to errors.

The performance analysis segment is expected to grow at the fastest CAGR during the forecast period. The growth of the performance analysis function is driven by the increasing demand for data-driven investment decision-making. Investors are increasingly relying on advanced analytical tools that provide detailed insights into returns, risk-adjusted performance, and benchmarking against relevant market indices. This shift toward evidence-based strategies has led to a higher adoption of performance analytics modules within portfolio management platforms.

Deployment Insights

The cloud segment held the largest market share in 2025. The growth of cloud-based deployment is driven by the increasing demand for scalable and cost-efficient solutions. Cloud platforms enable financial institutions and investors to access portfolio data in real time from any location, supporting remote operations and global investment management. The subscription-based pricing model reduces upfront capital expenditure and allows organizations to scale usage based on business needs. In addition, continuous updates, seamless integration with third-party applications, and faster deployment cycles make cloud solutions highly attractive, particularly for SMEs and digitally evolving financial firms.

The on-premise segment is expected to grow at a significant CAGR during the forecast period. The growth of on-premise deployment is driven by the need for greater data control, security, and compliance with stringent regulatory requirements. Large enterprises and institutional investors often prefer on-premises solutions to maintain full ownership of sensitive financial data and ensure compliance with internal governance policies. These systems offer greater customization and enable organizations to align software infrastructure with specific operational workflows.

End-use Insights

The large enterprises segment dominated the market in 2025. The rising complexity of managing diversified, multi-asset portfolios across global markets is driving the adoption of portfolio management software among large enterprises. Large financial institutions and asset managers require advanced tools to handle high transaction volumes, complex asset allocation strategies, and real-time performance monitoring. This has led to increased demand for integrated platforms that offer robust analytics, risk management, and compliance capabilities.

The individual investors segment is projected to grow at the fastest CAGR of 12.6% over the forecast period. The rapid increase in retail participation in financial markets and the proliferation of digital investment platforms are largely driving the growth of portfolio management software among individual investors. With greater access to mobile trading apps and online advisory services, individual investors are seeking intuitive tools that enable real-time portfolio tracking, performance analysis, and goal-based investing. The shift toward self-directed investing, supported by improved financial literacy and low-cost brokerage platforms, is further accelerating adoption.

Regional Insights

The North America portfolio management software market held a largest share in 2025. The market in the region is characterized by high maturity, strong digital infrastructure, and widespread adoption of advanced financial technologies. The region benefits from the presence of leading asset management firms and fintech innovators, driving continuous demand for sophisticated analytics, risk management, and automation tools.

U.S. Portfolio Management Software Market Trends

The portfolio management software market in the U.S. held a dominant position in 2025, driven by a highly developed financial ecosystem and a strong presence of institutional investors. The country exhibits significant demand for advanced portfolio management solutions that support real-time analytics, regulatory compliance, and multi-asset portfolio tracking.

Europe Portfolio Management Software Market Trends

The portfolio management software industry in Europe was identified as a lucrative region in 2025. The market in the region is driven by stringent regulatory requirements, including frameworks such as MiFID II and ESG-related mandates. Financial institutions across the region are increasingly adopting software solutions to enhance transparency, reporting accuracy, and risk management capabilities.

The UK portfolio management software market is expected to grow rapidly in the coming years, driven by the UK's position as a global financial hub. The demand for portfolio management software is driven by a strong asset management industry and increasing emphasis on regulatory compliance and client reporting.

The portfolio management software industry in Germany held a substantial share in 2025. Germany's market is characterized by a strong institutional investor base and a growing emphasis on risk management and regulatory adherence. The adoption of portfolio management software is driven by the need for efficient asset allocation and performance monitoring.

Asia Pacific Portfolio Management Software Market Trends

The portfolio management software market in Asia Pacific is anticipated to grow at the fastest CAGR of 12.9% during the forecast period. The Asia Pacific region is the fastest-growing market for portfolio management software, driven by rapid digitalization and expanding financial markets. Increasing wealth creation, rising participation of retail investors, and growing adoption of fintech solutions are driving the growth of the market in the region.

The India portfolio management software industry is expected to grow rapidly in the coming years, driven by the expansion of its fintech ecosystem and rising participation by retail investors. The adoption of portfolio management software is driven by the need for efficient investment tracking, risk management, and compliance with evolving regulations.

The portfolio management software market in China held a substantial market share in 2025. The country's market is experiencing strong growth driven by the expansion of its wealth management sector and the growing adoption of digital financial services. The market is driven by rising high-net-worth individuals and growing demand for sophisticated investment management tools.

Key Portfolio Management Software Companies Insights

Some of the key companies in the portfolio management software market include Planview, BlackRock, Inc., Oracle Corporation, Quicken Inc., and others. Organizations are focusing on increasing their customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies.

-

Planview is an enterprise software company that provides an end-to-end platform for strategic portfolio management (SPM) and digital product development. The company specializes in helping organizations plan, prioritize, and manage projects, products, and services across business and technology functions, using a connected suite of cloud‑based tools enhanced with AI‑driven insights.

-

BlackRock, Inc. is an asset‑management and financial‑technology firm best known for managing trillions of dollars in client assets and for its proprietary portfolio‑management software platform, Aladdin. In the context of portfolio‑management software, BlackRock operates primarily through its BlackRock Solutions division, which builds and licenses Aladdin, an integrated investment, risk, and operating system used by asset managers, banks, insurers, and central banks around the world.

Key Portfolio Management Software Companies:

The following key companies have been profiled for this study on the portfolio management software market.

- Planview

- BlackRock, Inc.

- Oracle Corporation

- Quicken Inc.

- FinFolio Inc.

- SS&C Technologies Holdings, Inc.

- Beiley Software, Inc.

- Miles Software

- MProfit Software Private Limited

- Ziggma Analytics Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: BlackRock, Oracle Corporation, SS&C Technologies Holdings, Inc., Planview

- Mature players focus on delivering comprehensive and integrated portfolio management ecosystems covering portfolio construction, risk analytics, trading, compliance, accounting, and reporting.

- Their operating strategies emphasize long-term enterprise contracts with institutional investors, asset managers, banks, pension funds, and insurance firms.

- Strong institutional client relationships and extensive global operational presence.

- Advanced risk management, regulatory compliance, and real-time investment analytics capabilities.

- High implementation, licensing, and customization costs may restrict adoption among smaller investment firms.

- Complex enterprise architectures can increase deployment timelines and reduce operational agility.

Emerging Players: Miles Software, MProfit Software Private Limited, Ziggma Analytics Inc.

- Emerging players primarily focus on cloud-native, SaaS-based portfolio management solutions targeting wealth managers, RIAs, fintech firms, family offices, and retail investment platforms.

- Higher agility and faster innovation cycles compared to established enterprise vendors.

- Strong expertise in cloud deployment, user-centric platform design, and digital wealth management technologies.

- Limited global reach and smaller enterprise customer base compared to mature market leaders.

- Lower financial resources may restrict large-scale R&D investments and international expansion capabilities.

Recent Developments

-

In September 2025, Murex and StarQube partnered to deliver a data‑driven portfolio management system integrated into Murex’s MX.3 for Investment Management platform, combining Murex’s cross‑asset front‑to‑back infrastructure with StarQube’s advanced analytics and portfolio‑construction modules. The solution leverages Murex’s Investment Book of Record (IBOR) and StarQube’s conic optimizer to let portfolio managers design, backtest, and execute bespoke strategies across public and private assets, while embedding rules, ESG constraints, and regulatory requirements directly into the optimization process.

-

In October 2024, Talos, an institutional‑grade digital‑asset trading platform, unveiled a new Portfolio Management System (PMS) that consolidates portfolio construction, portfolio and risk management, and treasury and settlement tools into a single, integrated environment linked to its flagship order and execution management system (OEMS). The PMS is designed so that portfolio managers, traders, risk teams, and operations can manage the entire digital‑asset investment lifecycle, from spot and derivatives trading to position tracking, P&L monitoring, and OTC settlement, on one unified platform, giving institutions a real‑time, consolidated view of positions, exposure, and risk across multiple strategies.

Portfolio Management Software Market Report Scope

Report Attribute

Details

Market size in 2025

USD 3.7 billion

Estimated market size in 2026

USD 3.9 billion

Projected market size by 2033

USD 8.3 billion

Growth rate

CAGR of 11.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report deployment

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Function, deployment, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

Planview; BlackRock, Inc.; Oracle Corporation; Quicken Inc.; FinFolio Inc.; SS&C Technologies Holdings, Inc.; Beiley Software, Inc.; Miles Software; MProfit Software Private Limited; Ziggma Analytics Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Portfolio Management Software Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global portfolio management software market report based on function, deployment, end-use, and region.

-

Function Outlook (Revenue, USD Million, 2021 - 2033)

-

Investment Tracking

-

Performance Analysis

-

Risk Management

-

Asset Allocation

-

Portfolio execution

-

Others

-

-

Deployment Outlook (Revenue, USD Million, 2021 - 2033)

-

Cloud

-

On-premise

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Large Enterprises

-

Small and Medium Enterprises

-

Individual Investors

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Portfolio Management Software Market Analysis

- Segmentation of PPM software across enterprise, IT, and financial portfolio use cases

- Demand assessment across SMEs and large enterprises

- Deployment trends (cloud vs on-premise) and pricing model evaluation

- Identified high-growth application areas (IT & enterprise portfolio management)

- Supported vendor positioning and product roadmap prioritization

End-User Adoption

- Analysis of portfolio planning, resource allocation, and project tracking workflows

- Evaluation of adoption drivers across industries (BFSI, IT, healthcare, manufacturing)

- Improved understanding of buyer adoption behavior and decision criteria

- Enabled targeting of high-value enterprise segments

Competitive Landscape Assessment

- Benchmarking of leading PPM software providers

- Feature comparison across project tracking, analytics, and automation capabilities

- Supported competitive intelligence and differentiation strategy

- Identified whitespace opportunities in advanced analytics and AI-enabled portfolio optimization

Frequently Asked Questions About This Report

The investment tracking segment led with a 23.6% revenue share in 2025, while performance analysis is the fastest-growing segment.

The cloud deployment held the largest revenue share in 2025.

The large enterprises held the largest share in 2025 and individual investors segment is the fastest-growing.

Asia Pacific is the fastest-growing region over the forecast period.

The global portfolio management software market size was valued at USD 3.7 billion in 2025 and is expected to reach USD 3.9 billion in 2026.

The global portfolio management software market is expected to grow at a compound annual growth rate of 11.3% from 2026 to 2033 to reach USD 8.32 billion by 2033.

North America held a significant share of 41.7% of the market in 2025.

Key players include Planview; BlackRock, Inc.; Oracle Corporation; Quicken Inc.; FinFolio Inc.; SS&C Technologies Holdings, Inc.; Beiley Software, Inc.; Miles Software; MProfit Software Private Limited; Ziggma Analytics Inc.

The increasing complexity of investment portfolios and the growing need for efficient asset management solutions is driving growth of the portfolio management software market.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.