- Home

- »

- Next Generation Technologies

- »

-

Precision Farming Market Size And Share Report, 2026-2033GVR Report cover

![Precision Farming Market (2026 - 2033)Report]()

Precision Farming Market (2026 - 2033)

Precision Farming Market Size, Share & Trends Analysis Report By Offering (Hardware, Software, Services), By Application (Yield Monitoring, Field Mapping, Crop Scouting, Weather Tracking & Forecasting), By Region, And Segment Forecasts (2026 - 2033)

Market Size, 2025

$15.1BMarket Estimate, 2026

$16.8BMarket Forecast, 2033

$38.8BCAGR, 2026–2033

12.7%Precision Farming Market Summary

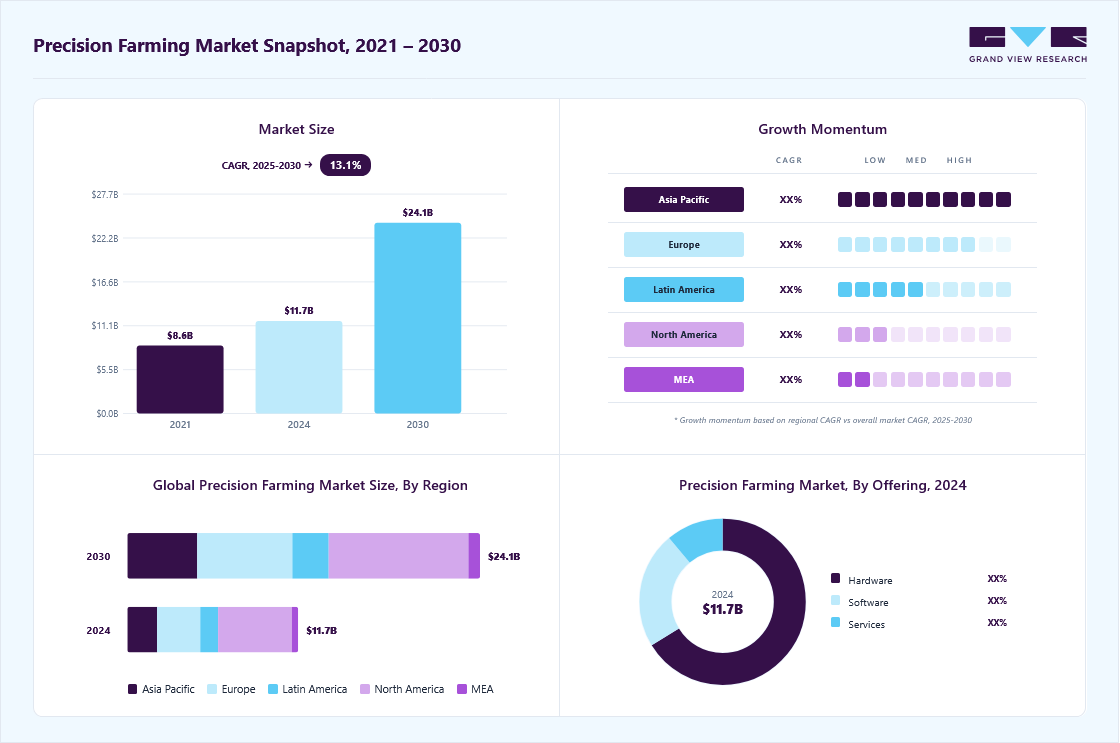

The global precision farming market size was valued at USD 15.1 billion in 2025 and is projected to grow from USD 16.8 billion in 2026 to USD 38.8 billion by 2033, at a CAGR of 12.7% from 2026 to 2033. North America dominated the precision farming market with the largest revenue share of 36.1% in 2025. The rise of precision farming is largely driven by the rapid expansion of the Internet of Things (IoT) and farmers' increasing use of advanced analytics.

Key Market Trends & Insights

- By offering: Hardware segment led the market with the largest revenue share of 66.7% in 2025.

- By application: Yield monitoring segment led the market with the largest revenue share of 43.1% in 2025.

Regional Highlights

- Largest regional market: North America (36.1% revenue share, 2025)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 15.1 Billion

- Estimated market size in 2026: USD 16.8 Billion

- Projected market size by 2033: USD 38.8 Billion

- CAGR (2026-2033): 12.7%

As a key offering of data science, advanced analytics employs a variety of tools and techniques to predict data trends and ensure optimal care for crops and soil. This enables farmers to make well-informed decisions and plan their activities more effectively. Modern technologies such as the Internet of Things (IoT), GPS, and remote sensing application control are widely utilized to gain a comprehensive understanding of various farming practices like irrigation and plowing. IoT is crucial in helping farmers overcome challenges associated with effective crop monitoring. IoT provides real-time data on environmental temperature and soil moisture levels by using sensors placed across the farmland. This information empowers farmers to make more informed decisions regarding harvesting schedules, crop pricing, and soil management, making it a significant driver in expanding the precision farming industry.")

Several other factors are also contributing to the adoption of sustainable agricultural technologies. These include improved farmer education and training, easier access to information, availability of financial support, and the rising demand for organic produce. Environmental degradation and natural resource depletion are major concerns hindering crop production. As a result, there is a growing emphasis on sustainable farming practices that focus on conserving natural resources. This trend fuels the need for enhanced crop nutrition and protection, accelerating market growth.

Innovations such as vertical farming, designed to optimize yield and minimize waste, have opened up new avenues for growth. Increased investment in technologies like autonomous tractors, GPS-based guidance systems, and sensing technologies is expected to further propel the precision agriculture market. Sensors for soil, climate, and water monitoring are strategically deployed across fields to give farmers real-time insights, enabling them to maximize yields and minimize losses. These sensor technologies are also gaining traction in industries beyond agriculture, including healthcare, automotive, pharmaceuticals, and sports.

In the post-COVID-19 era, the adoption of precision farming and remote sensing solutions is expected to rise. Companies are increasingly shifting toward wireless platforms that support real-time decision-making for crop health monitoring, yield assessment, irrigation planning, field mapping, and harvest management.

Market Dynamics

Precision farming is gaining traction as agricultural producers increasingly adopt technologies such as GPS-guided equipment, variable rate application systems, remote sensing, soil monitoring, yield mapping, and farm analytics platforms. These solutions enable farmers to optimize resource use, improve crop productivity, and enhance decision-making by providing real-time field data and actionable insights. The growing focus on sustainable agriculture, rising pressure to maximize yields from limited arable land, and increasing adoption of digital farming technologies are expected to continue driving growth in the precision farming market.

The growing adoption of connected and automated farm equipment is driving the precision farming market growth by enabling farmers to improve operational efficiency, reduce labor dependency, and make data-driven agricultural decisions. Modern tractors, harvesters, sprayers, and irrigation systems are increasingly equipped with sensors, GPS guidance, telematics, and automation capabilities, enabling real-time monitoring and control of farming activities. These technologies help optimize field operations, reduce resource wastage, and improve productivity across large agricultural areas. Automated equipment also ensures greater accuracy in planting, fertilization, spraying, and harvesting processes. As farms increasingly embrace digital transformation, demand for precision farming solutions continues to grow significantly. According to the U.S. Department of Agriculture, guidance and autosteering technologies integrated into tractors, harvesters, and other agricultural equipment were adopted by approximately 50% of midsize farms and 68% of large-scale crop-producing farms in 2025. Furthermore, precision agriculture solutions, including yield monitors and soil-mapping technologies, were employed by 68% of large-scale crop-producing farms, underscoring the growing reliance on data-driven technologies to enhance farm productivity and decision-making.

High initial investment and deployment costs represent a significant restraint in the precision farming market because the implementation of precision agriculture systems requires substantial capital expenditure on advanced technologies, equipment, and digital infrastructure. Farmers often need to invest in GPS-guided machinery, variable-rate application systems, drones, sensors, automated irrigation equipment, satellite-based monitoring tools, and farm management software. The combined cost of these technologies can be considerably higher than traditional farming methods, making adoption challenging for many agricultural producers. Small and medium-sized farms, in particular, often face financial constraints that limit their ability to invest in advanced precision farming solutions. As a result, high upfront costs continue to slow market penetration in many regions.

The growing integration of satellite imagery and geospatial analytics presents a significant opportunity for the precision farming market, enabling farmers to gain comprehensive visibility into field conditions, crop performance, and environmental changes across large agricultural areas. High-resolution satellite imagery provides valuable information on crop health, vegetation indices, soil moisture, nutrient variability, and land-use patterns, while geospatial analytics transforms this data into actionable insights. These capabilities enable farmers to make more informed decisions about planting, irrigation, fertilization, and harvesting. By improving operational accuracy and resource utilization, satellite-enabled precision farming solutions help increase productivity and profitability. As access to satellite data becomes more affordable and frequent, adoption opportunities within precision agriculture continue to expand.

Analyst Perspective

The precision farming market sits at a strong intersection of agricultural modernization, rising global food demand, and the need for greater operational efficiency across farming operations. The central competitive moat, however, will belong to the provider that integrates field monitoring, equipment connectivity, agronomic analytics, automation, and farm management capabilities into a unified ecosystem, transforming fragmented farm data into actionable intelligence that enables higher yields, lower input costs, and improved sustainability outcomes throughout the agricultural value chain.

Offering Insights

Based on offerings, the hardware segment led the market with the largest revenue share of 66.7% in 2025. The hardware segment has been further segmented into automation and control systems, sensing devices, antennas, and access points. Hardware offerings such as automation and control systems, sensing devices, and drones play a major role in helping farmers. For instance, the GIS guidance system is very beneficial for growers as it can visualize agricultural workflows and the environment. Furthermore, VRT technology helps farmers determine areas that need more pesticides and seeds, distributing them equally across the field.

The services segment is anticipated to grow at a CAGR of 15.7% during the forecast period. Cloud computing focuses on shared networks, servers, and storage devices, owing to which the high costs incurred in maintaining hardware and software infrastructure are eliminated. As a result, the software segment is anticipated to register a CAGR of over 15.5% during the forecast period. Predictive analytics software guides farmers about crop rotation, soil management, optimal planting times, and harvesting times.

Application Insights

Based on application, the yield monitoring segment led the market with the largest revenue share of 43.1% in 2025. The segment is further segregated into on-farm yield monitoring and off-farm yield monitoring. On-farm yield monitoring allows farmers to obtain real-time information during harvest and create a historical spatial database. This segment is expected to account for the largest share of the market for precision farming as it offers equitable landlord negotiations, environmental compliance documentation, and track records for food safety.

The weather tracking & forecasting segment is anticipated to grow at a CAGR of 17.6% during the forecast period. The use of sensors helps weather forecasters to provide accurate weather readings and forecasting. In addition, the introduction of machine learning techniques and advanced data analytics services has increased the reliability and accuracy of weather forecasts, thus propelling the market's growth.

Regional Insights

North America dominated the precision farming market with the largest revenue share of 36.1% in 2025. The region is an early adopter of technologies. Factors such as increasing government initiatives that support the adoption of modern agriculture technologies and developed infrastructure have contributed to the high revenue of the regional market. Furthermore, in May 2022, the Government of Canada announced an investment of USD 441.9 thousand to develop an integrated system for precision fruit tree farming. The investment also aimed to achieve sustainable solutions to tackle the rising challenges in Canada’s apple industry.

U.S. Precision Farming Market Trends

The precision farming market in the U.S. held the largest share in the North America region in 2025, due to favorable government initiatives. For instance, the National Institute of Food and Agriculture (NIFA)-part of the U.S. Department of Agriculture-conducts geospatial, sensor, and precision technology programs to create awareness among farmers. In partnership with Land-Grand universities, NIFA helps farmers develop robust sensors, associated software, and instrumentation for modeling, observing, and analyzing a wide range of complex biological materials and processes.

Europe Precision Farming Market Trends

The European Union’s focus on sustainable agriculture through the Common Agricultural Policy (CAP) and the European Green Deal is driving the market growth in Europe. These policies encourage farmers to adopt more environmentally responsible practices, including the use of precision technologies that minimize input usage and reduce environmental impact. By using satellite-guided equipment, drones, and sensor-based systems, farmers can apply fertilizers and pesticides more accurately, improving efficiency while meeting strict environmental regulations. These policy frameworks provide financial support and incentives for adopting precision farming, making it economically viable for both large and small-scale farmers.

The precision farming market in the UK is expected to account for a significant revenue share in the Europe precision farming industry. Precision farming in the UK is gaining traction as technology advances and farmers seek more efficient and sustainable agricultural practices. This approach uses various technologies such as GPS, sensors, drones, and data analytics to optimize crop yields, minimize input usage, and reduce environmental impact.

The precision farming market in Germany is expected to account for a significant revenue share in the European precision farming market. Farmers in Germany are increasingly adopting precision farming techniques to enhance productivity, reduce costs, and mitigate risks associated with unpredictable weather patterns and soil variability.

The precision farming market in France is expected to account for a significant revenue share in the European precision farming market. Government support and incentives, such as grants for adopting precision farming technologies and subsidies for sustainable farming practices, further encourage uptake among France farmers.

Asia Pacific Precision Farming Market Trends

Asia Pacific is expected to witness significant growth over the forecasted period, with a CAGR of over 15.5% from 2025 to 2030. Numerous government initiatives are being undertaken in developing countries such as India, Sri Lanka, and Nigeria to encourage the implementation of modern precision farming technologies, thereby maximizing productivity. Moreover, an effective administrative framework also enables farmers to gain adequate knowledge of the proper use and maintenance of precision farming equipment.

The precision farming market in China is expected to account for a significant revenue share in the Asia Pacific precision farming market. It is experiencing significant growth, driven by the increasing adoption of advanced agricultural technologies and growing emphasis on sustainable farming practices.

The precision farming market in India is expected to account for a significant revenue share in the Asia Pacific precision farming market. With a large agricultural sector and rising demand for food security, Indian farmers are turning to precision farming techniques to improve crop yields, optimize resource utilization, and reduce environmental impact.

The precision farming market in Japan is expected to account for a significant revenue share in the Asia Pacific precision farming market. Integrating artificial intelligence (AI), drones, and big data analytics further enhances the efficiency and effectiveness of precision farming practices in Japan.

Key Precision Farming Company Insights

Some of the key players operating in the market include Trimble, Inc., AGCO Corporation, Raven Industries Inc., and Deere and Company, among others, are leading participants in the precision farming market.

-

Deere & Company manufactures and constructs agricultural and forestry machinery, drivetrains, diesel engines for heavy equipment, and lawn care machinery. It also manufactures and provides other heavy manufacturing equipment. The company serves diverse industries, such as agriculture, forestry, construction, landscaping and grounds care, engines and drivetrains, government and military, and sports turf.

-

AGCO Corporation is a U.S.-based manufacturer of agricultural equipment. The Company develops and sells products and solutions such as tractors, combines, foragers, hay tools, self-propelled sprayers, smart farming technologies, seeding equipment, and tillage equipment.

Prospera Technologies and Agrible, Inc. are some of the emerging market participants in the precision farming market.

-

Porspera Technologies is a global service provider of agriculture technology for managing and optimizing irrigation and crop health. The company provides AI-based sensors and cameras that aid farmers in crop monitoring.

-

Agrible is a U.S.-based agriculture solution provider. The company helps customers in more than 30 countries optimize water use, crop protection, fertilization, fieldwork, research trials, food supply chains, and sustainability initiatives.

Key Precision Farming Companies:

The following are the leading companies in the precision farming market. These companies collectively hold the largest market share and dictate industry trends.

- Ag Leader Technology

- AgJunction, Inc.

- CropMetrics LLC

- Trimble, Inc.,

- AGCO Corporation

- Raven Industries Inc.

- Deere and Company

- Topcon Corporation

- AgEagle Aerial Systems Inc. (Agribotix LLC)

- DICKEY-john Corporation

- Farmers Edge Inc.

- Grownetics, Inc.

- Proagrica (SST Development Group, Inc.)

- The Climate Corporation

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (John Deere; Trimble Inc.; AGCO Corporation; CNH Industrial)

- Mature players in the precision farming market focus on connected farming ecosystems. They integrate GPS, sensors, AI, and farm equipment into unified platforms. Their solutions support field mapping, yield monitoring, and input optimization. They also strengthen market presence through dealer and distribution networks.

- Mature players benefit from strong farmer relationships and global reach. Their platforms deliver accurate data for farm planning and operations. Large R&D investments support continuous technology advancement. Integrated hardware and software solutions improve customer retention.

- These solutions often require a high upfront investment. System deployment can be complex for smaller farms. Connectivity limitations may affect performance in rural areas. Training requirements can also slow adoption among traditional users.

Emerging Players (CropX; Taranis; Prospera Technologies; FarmWise)

- Emerging players focus on AI-driven analytics and precision monitoring tools. They use drones, sensors, and imaging technologies for crop intelligence. Many offer cloud-based platforms through subscription models. Their strategy emphasizes affordable and data-centric farm management.

- Emerging players provide specialized solutions for targeted farming challenges. Their platforms are flexible and easier to implement. Strong AI capabilities improve real-time agronomic decision-making. They also innovate rapidly in niche precision agriculture segments.

- Emerging players have limited global distribution and service capabilities. Their solutions often depend on third-party hardware ecosystems. Funding limitations can restrict long-term growth and expansion. Lower brand awareness may affect adoption by large farming enterprises.

Recent Developments

-

In February 2025, Topcon Corporation partnered with Bonsai Robotics to advance automation in the agricultural sector, specifically for permanent crops. This partnership will integrate Bonsai Robotics' cutting-edge vision-based autonomous driving technology with Topcon Agriculture's leading expertise in sensors, connectivity, and smart implements. Combining Bonsai's autonomous navigation systems with Topcon's advanced autosteering, telematics, and integration, the joint effort aims to deliver comprehensive solutions that streamline labor-intensive tasks, enable data-driven decision-making, and enhance precision harvesting even in the most challenging environments.

-

In April 2024, AGCO Corporation and Trimble announced a joint venture (JV) agreement, forming a new company called PTx Trimble. This venture merges Trimble’s precision agriculture division with AGCO’s JCA Technologies, aiming to deliver enhanced solutions for factory-installed and aftermarket applications in the mixed-fleet precision agriculture sector. With PTx Trimble, AGCO strengthens its advanced technology portfolio across key areas such as guidance systems, autonomy, precision spraying, connected farming, data management, and sustainable agricultural practices.

-

In July 2023, Deere & Company, a global agriculture and construction equipment manufacturer, announced the acquisition of Smart Apply Inc., an agriculture technology solution provider. Deere & Company is focused on using Smart Apply’s precision spraying solution to assist growers in addressing the challenges related to regulatory requirements, input costs, labor, etc. The acquisition is expected to help the Company attract new customers.

-

In April 2023, AGCO Corporation, a global agriculture equipment provider, and Hexagon, an industrial technology solution provider, declared their strategic collaboration. The collaboration is focused on expanding AGCO’s factory-fit and aftermarket guidance offerings.

-

In May 2023, AgEagle Aerial Systems Inc., a global agriculture technology solution provider, announced the establishment of a new supply agreement with Wingtra AG. The two-year agreement is expected to securely supply RedEdge-P sensor kits for incorporation with WingtraOne VTOL drones.

Precision Farming Market Report Scope

Report Attribute

Details

Market size in 2025

USD 15.1 billion

Estimated Market size in 2026

USD 16.8 billion

Projected Market size by 2033

USD 38.8 billion

Growth rate

CAGR of 12.7% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company market share analysis, competitive landscape, growth factors, and trends

Segments covered

Offerings, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; Saudi Arabia; South Africa; UAE

Key companies profiled

Ag Leader Technology; AgJunction, Inc.; CropMetrics LLC; Trimble, Inc.; AGCO Corporation; Raven Industries Inc.; Deere and Company; Topcon Corporation; AgEagle Aerial Systems Inc. (Agribotix LLC); DICKEY-john Corporation; Farmers Edge Inc.; Grownetics, Inc.; Proagrica (SST Development Group, Inc.); The Climate Corporation

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Precision Farming Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global precision farming market report based on offering, application, and region:

-

Offering Outlook (Revenue, USD Million; 2021 - 2033)

-

Hardware

-

Automation & Control Systems

-

Drones

-

Application Control Devices

-

Guidance System

-

GPS

-

GIS

-

-

Remote Sensing

-

Handheld

-

Satellite Sensing

-

-

Driverless Tractors

-

Mobile Devices

-

VRT

-

Map-based

-

Sensor-based

-

-

Wireless Modules

-

Bluetooth Technology

-

Wi-Fi Technology

-

Zigbee Technology

-

RF Technology

-

-

-

Sensing Devices

-

Soil Sensor

-

Nutrient Sensor

-

Moisture Sensor

-

Temperature Sensor

-

-

Water Sensors

-

Climate Sensors

-

Others

-

-

Antennas & Access Points

-

-

Software

-

Web-based

-

Cloud-based

-

-

Services

-

System Integration & Consulting

-

Maintenance & Support

-

Managed Types

-

Data Types

-

Analytics Types

-

Farm Operation Types

-

-

Assisted Professional Types

-

Supply Chain Management Types

-

Climate Information Types

-

-

-

-

Application Outlook (Revenue, USD Million; 2021 - 2033)

-

Yield Monitoring

-

On-Farm

-

Off-Farm

-

-

Field Mapping

-

Crop Scouting

-

Weather Tracking & Forecasting

-

Irrigation Management

-

Inventory Management

-

Farm Labor Management

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Research Methodology

Segment Definition

Segment – Offerings

Revenue capture definition

Hardware

The largest revenue-generating offering segment is capturing income through the sale of GPS-guided equipment, sensors, drones, yield monitors, weather stations, automated steering systems, and IoT-enabled field devices. Revenue growth is driven by increasing mechanization and the adoption of connected technologies that enable real-time farm monitoring and precision decision-making.

Software

Revenue is generated through consulting, system integration, data interpretation, equipment maintenance, training, and precision agriculture advisory services. Many growers rely on external expertise to maximize technology utilization, creating sustained demand for implementation and support services.

Services

Revenue is captured through yield monitoring equipment, sensor technologies, and analytics platforms that measure crop performance during harvest. Software providers further monetize this application by offering yield trend analysis, productivity benchmarking, and data-driven recommendations for future planting strategies.

Segment - Application

Revenue capture definition

Yield Monitoring

Revenue is captured through yield monitoring equipment, sensor technologies, and analytics platforms that measure crop performance during harvest. Software providers further monetize this application by offering yield trend analysis, productivity benchmarking, and data-driven recommendations for future planting strategies.

Field Mapping

Revenue is generated through GPS-enabled mapping solutions, drone surveys, satellite imagery services, and geospatial analytics platforms. Farmers invest in field-mapping technologies to identify soil variability, optimize land use, and support precision input management across agricultural operations.

Crop Scouting

Revenue is generated through drone-based monitoring services, multispectral imaging systems, AI-powered crop health analytics, and pest-detection platforms. The ability to identify diseases, nutrient deficiencies, and stress conditions early allows technology providers to command premium pricing for actionable agronomic insights.

Weather Tracking & Forecasting

Weather tracking & forecasting revenue is captured through connected weather stations, climate monitoring sensors, predictive forecasting software, and subscription-based meteorological data services. Increasing weather volatility and climate-related risks are driving the adoption of advanced forecasting tools that support timely farm management decisions.

Irrigation Management

Revenue is generated through smart irrigation controllers, soil moisture sensors, automated water management systems, and optimization software platforms. Precision irrigation solutions help farmers reduce water consumption while improving crop productivity, creating strong demand in water-stressed agricultural regions.

Inventory Management

Revenue is earned through digital platforms that track seeds, fertilizers, pesticides, fuel, machinery parts, and harvested produce across farming operations. Software vendors capture recurring revenue by providing inventory visibility, procurement optimization, and supply chain management capabilities.

Farm Labor Management

Revenue is generated through workforce scheduling software, mobile farm management applications, productivity tracking tools, and labor analytics platforms. Growing labor shortages and rising wage costs are encouraging farms to adopt digital solutions that improve workforce efficiency, compliance, and operational planning.

Estimation Model

Layer Name

Key Question

Description

Agricultural Potential Layer

Who can benefit from precision farming technologies?

Identify cultivated farmland, commercial farming operations, and high-value crop segments where precision agriculture solutions can improve efficiency and productivity.

Technology Accessibility Layer

Who can access precision farming solutions?

Apply farm mechanization levels, digital infrastructure availability, and connectivity access to determine the reachable market for precision farming technologies.

Adoption & Utilization Layer

Who actively uses precision farming technologies?

Analyze the adoption of guidance systems, variable rate technologies, field mapping, yield monitoring, and farm management solutions to identify active users.

Monetisation Layer

How much revenue is generated?

Assess revenue-generation potential by analyzing spending on precision farming equipment and services, while incorporating recurring subscription and support revenues.

Delivered Customizations

This report has been delivered with the following In-depth customizations

CLIENT REQUEST

CUSTOMIZATION DELIVERED

VALUE ADDS

Precision Agriculture & Smart Farming Adoption Trends

Conducted a focused analysis of precision farming technologies covering GPS-guided equipment, variable rate technology, field mapping, soil monitoring, crop scouting, smart irrigation, and farm data analytics across commercial farming operations.

Helps stakeholders identify high-growth technology applications, evaluate farm digitization trends, and assess commercialization opportunities in data-driven agriculture solutions.

Connected Farm Management & Resource Optimization Trends

Evaluated adoption trends for IoT sensors, drones, AI-powered crop monitoring, weather analytics, and automated farm management platforms, including integration with machinery and decision-support systems.

Provides insights into productivity improvement opportunities, resource optimization strategies, and commercially attractive precision agriculture solutions supporting sustainable farming practices.

Digital Agriculture Ecosystem & Farm Automation Opportunity Assessment

Assessed demand for cloud-based farm management software, predictive analytics, autonomous farming technologies, and integrated precision agriculture platforms, along with connectivity, implementation, and farmer adoption challenges.

Supports investment and expansion strategies by identifying underserved farming segments, evaluating technology readiness, and strengthening long-term growth opportunities in smart and sustainable agriculture.

Frequently Asked Questions About This Report

The global precision farming market size was valued at USD 15.1 billion in 2025 and is estimated to reach USD 16.8 billion in 2026.

Major companies operating in the precision farming market include Ag Leader Technology; AgJunction, Inc.; CropMetrics LLC; Trimble, Inc.; AGCO Corporation; Raven Industries Inc.; Deere and Company; Topcon Corporation; AgEagle Aerial Systems Inc. (Agribotix LLC); DICKEY-john Corporation; Farmers Edge Inc.; Grownetics, Inc.; Proagrica (SST Development Group, Inc.); The Climate Corporation.

The hardware segment led the market with a 66.7% revenue share in 2025, while the software segment is expected to register the fastest growth.

North America dominated the precision farming market, accounting for a 36.1% revenue share in 2025.

The yield monitoring segment held the largest revenue share in 2025, while weather tracking & forecasting is expected to be the fastest-growing segment.

The global precision farming market is expected to grow at a CAGR of 12.7% from 2026 to 2033, reaching USD 38.8 billion by 2033.

Key factors driving the precision farming market include growing adoption of connected and automated farm equipment and growing integration of satellite imagery and geospatial analytics.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.