- Home

- »

- Advanced Interior Materials

- »

-

Precision Gearbox Market Size, Growth Report, 2026-2033GVR Report cover

![Precision Gearbox Market (2026 - 2033)Report]()

Precision Gearbox Market (2026 - 2033)

Size, Share & Trends Analysis Report By Gear Technology (Planetary, Harmonic, Cycloidal), By Application (Military & Aerospace, Machine Tools, Materials Handling, Packaging, Robotics, Medical), By Region, And Segment Forecasts

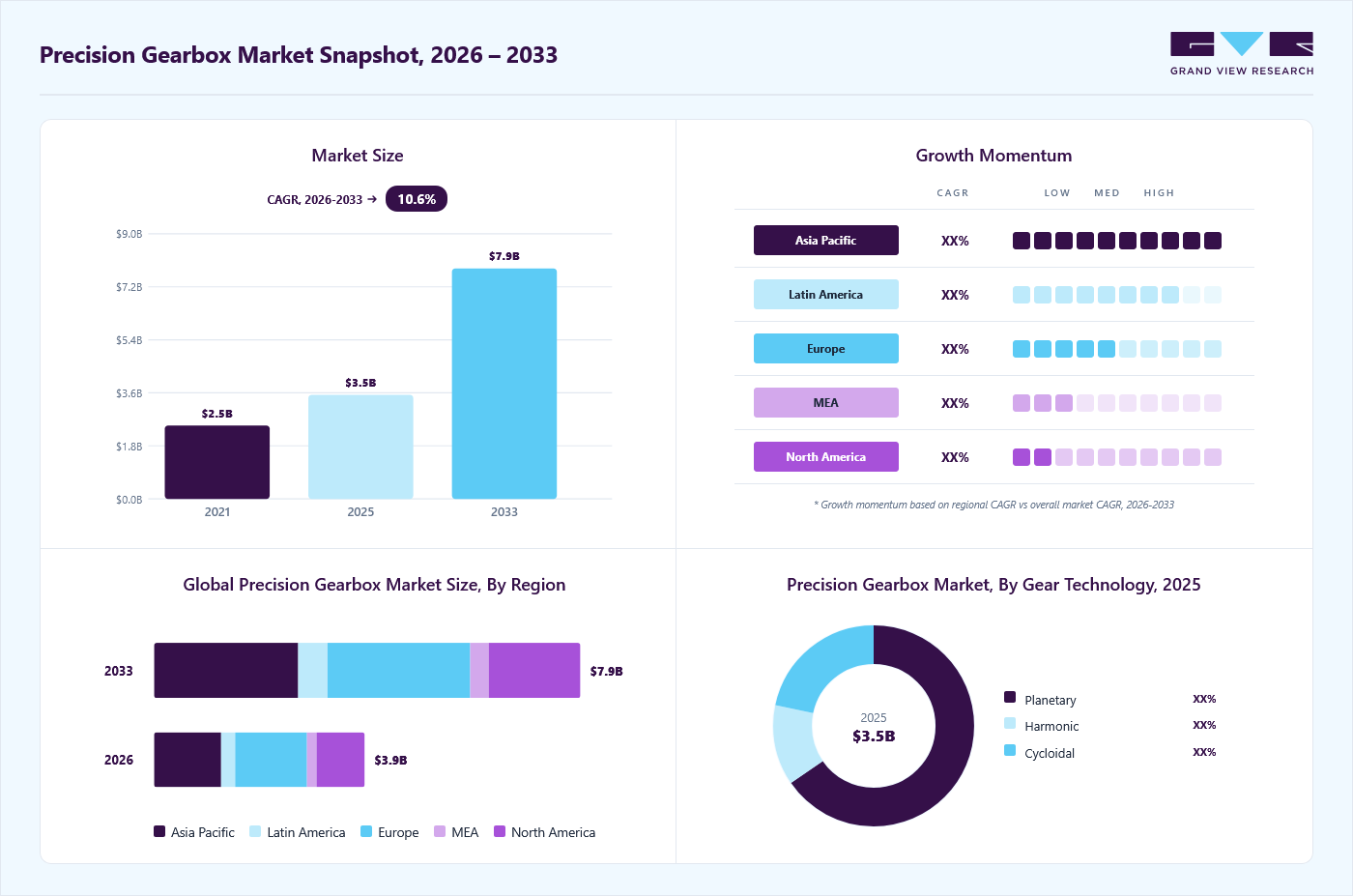

Market Size, 2025

$3.5BMarket Estimate, 2026

$3.9BMarket Forecast, 2033

$7.9BCAGR, 2026–2033

10.6%Precision Gearbox Market Summary

The global precision gearbox market size was valued at USD 3.5 billion in 2025 and is projected to grow from USD 3.9 billion in 2026 to USD 7.9 billion by 2033, at a CAGR of 10.6% from 2026 to 2033. Europe dominated the global market, accounting for the largest revenue share of 34.1% in 2025. The industry is driven by the expanding adoption of industrial automation and robotics across manufacturing sectors.

Key Market Trends & Insights

- By gear technology: Planetary segment dominated the market in 2025 holding 65.3% market share.

- By application: Robotics segment dominated the market in 2025, holding the largest revenue share of 18.4%.

Regional Highlights

- Largest regional market: Europe (34.1% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The Germany precision gearbox industry is a major contributor to the global market.

Market Size & Forecast

- Market size in 2025: USD 3.5 Billion

- Estimated market size in 2026: USD 3.9 Billion

- Projected market size by 2033: USD 7.9 Billion

- CAGR (2026-2033): 10.6%

As factories shift toward high-precision motion control systems, demand for gearboxes that offer accurate positioning and repeatability continues to rise. Growth is also supported by the increasing use of collaborative robots in electronics, automotive, and packaging operations, where compact and reliable transmission components are essential for consistent performance.

")

Ongoing investments in smart manufacturing are encouraging industries to upgrade traditional production systems with automated and digitally connected equipment. This modernization increases the need for precise motion control components, including precision gearboxes, to ensure accurate and reliable machine performance. As both developed and emerging economies expand advanced manufacturing facilities, the replacement of older machinery with modern systems continues to create consistent demand for high-precision transmission solutions across multiple industrial sectors.

Market Concentration & Characteristics

The precision gearbox industry is fragmented due to the presence of numerous global and regional manufacturers offering specialized products for different industrial needs. Many companies focus on niche applications such as robotics, medical devices, and semiconductor equipment, leading to varied product designs and performance standards. Competition is influenced by customization capabilities, distribution networks, and after-sales technical support, allowing smaller suppliers to compete alongside established multinational gearbox producers in the market.

Manufacturers are developing lightweight materials, advanced gear designs, and low-backlash systems to enhance positioning accuracy in robotics and automation. Integration with digital monitoring technologies is also increasing, allowing predictive maintenance and performance tracking. These innovations help industries achieve higher productivity and reduce operational downtime in automated environments.

Merger and acquisition activities in the market are driven by the need to expand product portfolios and strengthen technological capabilities. Companies acquire specialized gearbox or motion control firms to gain access to advanced engineering expertise and new customer segments. These activities also support geographic expansion into emerging industrial markets. Strategic partnerships and consolidations help firms improve supply chain efficiency and enhance their competitive positioning in the global automation sector.

Regulations are shaping the industry by encouraging the adoption of energy-efficient and reliable mechanical systems in industrial operations. Standards related to machinery safety, energy consumption, and equipment reliability require manufacturers to design gearboxes that meet strict operational and environmental guidelines. Compliance with international quality certifications also influences product design and testing processes. These regulatory requirements promote higher product standards and drive continuous technological improvements in gearbox manufacturing.

Drivers, Opportunities & Restraints

Increasing adoption of industrial robots across manufacturing industries is driving the market. Robotics applications require high-accuracy motion control to perform repetitive tasks with minimal error, making precision gearboxes essential components. As industries such as automotive, electronics, and packaging expand automation to improve productivity and product quality, the demand for reliable and compact precision gearboxes continues to rise steadily worldwide.

Rapid expansion of collaborative robots and small-scale automation systems is a significant opportunity in the market. These applications require compact, lightweight, and highly precise gear mechanisms that can operate safely alongside human workers. Growing adoption of automation among small and medium-sized enterprises creates new demand for cost-effective precision gearbox solutions. This trend opens pathways for manufacturers to introduce customized products suited to emerging automation needs.

A significant challenge is the high manufacturing cost associated with advanced materials and tight tolerance requirements. Producing gearboxes with minimal backlash and long service life demands sophisticated machining and quality control processes, increasing overall product costs. These higher costs can limit adoption among cost-sensitive industries and smaller manufacturers. Maintaining consistent product quality while controlling expenses remains a critical operational challenge for many suppliers.

Gear Technology Insights

The planetary segment dominated the industry in 2025 due to its high torque density and compact structure, making it suitable for industrial automation and packaging machinery. Its ability to handle heavy loads with consistent precision supports adoption across robotics and material handling systems. Increasing demand for reliable motion control in automated production lines continues to drive steady growth of planetary gearboxes.

The harmonic segment is projected to grow rapidly at 13.2% CAGR during the forecast period due to its capability to provide zero backlash and high positioning accuracy, which is essential for robotics and semiconductor equipment. Its lightweight design supports use in compact robotic arms and precision-driven applications. Rising investments in advanced robotics and electronics manufacturing are expected to significantly strengthen demand for harmonic gearboxes in high-precision environments.

Application Insights

The robotics segment dominated the market in 2025, holding the largest revenue share of 18.4%, as industries increase the deployment of industrial and collaborative robots for precise and repetitive tasks. Precision gearboxes are essential for accurate motion control and smooth operation in robotic arms. Rising automation in automotive, electronics, and packaging sectors is expected to steadily increase demand for high-performance gearboxes designed for robotic applications.

The medical segment is projected to grow significantly due to the increasing use of precision equipment such as surgical robots, diagnostic devices, and imaging systems. These applications require compact and highly accurate gear mechanisms to ensure reliable movement and patient safety. Expanding healthcare infrastructure and adoption of advanced medical technologies are expected to support continuous demand for precision gearboxes in medical applications.

Regional Insights

North America precision gearbox market is expected to grow significantly due to the increasing adoption of advanced automation and robotics across manufacturing sectors. Industries such as automotive, aerospace, and electronics are upgrading production systems to improve efficiency and precision. Investments in smart factories and modernization of existing facilities are supporting demand for reliable motion control components. The presence of established robotics manufacturers and continuous technological upgrades in industrial operations further contributes to stable regional growth in precision gearbox usage.

U.S. Precision Gearbox Market Trends

The precision gearbox market in the U.S. is driven by strong investments in robotics and automated manufacturing systems. Industries are focusing on improving production accuracy and reducing operational downtime, increasing the need for high-performance gear solutions. Expansion of e-commerce and logistics automation also contributes to demand for precision-driven equipment.

Mexico precision gearbox market is growing due to the expansion of manufacturing facilities, particularly in the automotive and electronics sectors. The country’s role as a production hub encourages the adoption of automated machinery to maintain efficiency and product quality. Increasing foreign investments in industrial plants support the installation of modern robotics and motion control systems.

Europe Precision Gearbox Market Trends

The precision gearbox market in Europe dominated the global industry due to strong industrial automation and engineering expertise across major economies. Manufacturers are adopting advanced robotics and precision equipment to maintain production efficiency and quality standards. The region’s focus on energy-efficient machinery and advanced manufacturing technologies supports the adoption of modern gearbox systems.

Germany precision gearbox market holds a strong position in mechanical engineering and industrial automation. The country’s focus on high-quality manufacturing encourages the use of precision components in robotics and machinery. Automotive and industrial equipment producers are investing in advanced production technologies to improve efficiency and accuracy. Continuous innovation in automation systems and the presence of well-established machinery manufacturers support the steady expansion of precision gearbox demand across various industrial sectors.

The precision gearbox market in the UK is experiencing growth as industries adopt automation to enhance productivity and maintain operational efficiency. Modernization of production lines and increasing use of robotics in specialized manufacturing processes support the adoption of high-performance gear systems. Government support for advanced manufacturing initiatives further strengthens the demand for reliable precision gearbox technologies in the country.

Asia Pacific Precision Gearbox Market Trends

The precision gearbox market in Asia Pacific is expected to grow significantly during the forecast period, driven by large-scale industrialization and increasing investments in automation technologies. Expanding manufacturing activities in the automotive, electronics, and consumer goods industries require reliable motion control systems. The region’s growing focus on robotics integration and production efficiency supports strong demand for advanced gearbox solutions.

China precision gearbox market is witnessing strong growth, driven by its large manufacturing base and increasing adoption of industrial robotics. Industries are investing in automated production systems to improve efficiency and meet global quality standards. Government initiatives supporting smart manufacturing and advanced equipment production encourage the use of high-precision components. The rapid expansion of electronics and automotive manufacturing sectors continues to increase the need for durable and accurate gearbox systems across industrial applications.

Rising industrial automation and expanding manufacturing activities across sectors such as automotive, electronics, and packaging are driving the precision gearbox market in India. Companies are gradually upgrading production facilities to improve efficiency and reduce manual dependency. Government initiatives promoting domestic manufacturing and modernization of industrial infrastructure support the adoption of robotics and automated systems. As industries focus on improving productivity and maintaining consistent product quality, demand for precision gearboxes is steadily increasing.

Middle East & Africa Precision Gearbox Market Trends

The precision gearbox market in the Middle East & Africa is poised for significant growth, supported by increasing investments in industrial development and automation projects. Expansion of manufacturing facilities and infrastructure development requires reliable machinery components for efficient operations. Industries such as oil and gas equipment manufacturing and packaging are adopting precision-driven systems to enhance productivity.

Saudi Arabia precision gearbox market is experiencing growth due to ongoing industrial diversification and investment in advanced manufacturing facilities. The country’s focus on expanding non-oil industries encourages the use of automated machinery and precision-driven equipment. Development of new industrial zones and modernization of production facilities support the adoption of reliable motion control systems.

Latin America Precision Gearbox Market Trends

The precision gearbox market in Latin America is driven by the gradual adoption of automation in manufacturing industries. Expansion of the automotive and food processing sectors increases the demand for reliable machinery components. Companies are investing in upgrading production lines to enhance efficiency and maintain product consistency.

Brazil precision gearbox market is growing due to expanding industrial automation in automotive, agriculture equipment, and food processing sectors. Manufacturers are gradually integrating modern machinery to improve productivity and reduce operational errors. Investments in upgrading industrial facilities support the adoption of advanced motion control components.

Key Precision Gearbox Companies Insights

Some of the key players operating in the market include Harmonic Drive LLC, NIDEC-SHIMPO CORPORATION, Stöber Antriebstechnik GmbH and Co. KG

-

Harmonic Drive LLC is engaged in the designing and manufacturing of precision servo actuators, gear component sets, and gearheads. It offers standard and custom-engineered solutions to various application industries, including robotics, medical, defense, aerospace, energy, and machine tooling.

-

NIDEC-SHIMPO CORPORATION manufactures variable speed drives, speed reducers, ceramic art equipment, various measuring instruments, and other machinery tools. It serves various application industries including metal cutting & forming, assembly & test automation, packaging & filling, printing & converting, medical & healthcare, robotics, and semiconductor & circuit

Key Precision Gearbox Companies:

The following key companies have been profiled for this study on the precision gearbox market.

- Harmonic Drive LLC

- NIDEC-SHIMPO CORPORATION

- Stöber Antriebstechnik GmbH and Co. KG

- WITTENSTEIN SE

- GAM ENTERPRISES, INC.

- DieQua Corporation

- Neugart GmbH

- Apex Dynamics, Inc.

- Sumitomo Drive Technologies

- Nabtesco Corporation

- Cone Drive

- Hiwin Corporation

- Wilhelm Vogel GmbH

- Sureservo

- PARKER HANNIFIN CORP

Recent Developments

-

In March 2026, Neugart introduced a new performance class of precision gearboxes with its PSNpro, PSFNpro, and PSBNpro series, designed to deliver improved efficiency and durability. These gearboxes use advanced gear technologies and new materials to enhance performance. Improved tooth flank quality helps reduce load concentration and allows the transmission of higher torque while maintaining the same service life, supporting demanding industrial automation and robotics applications.

-

In January 2025, Sumitomo Heavy Industries launched the DA Series gear head for servo motors under its Fine CYCLO precision gearbox lineup. The zero-backlash design supports accurate positioning and easy installation. It is intended for high-precision applications such as machine tools and semiconductor manufacturing equipment requiring stable and reliable motion control.

Precision Gearbox Market Report Scope

Report Attribute

Details

Market size in 2025

USD 3.5 Billion

Estimated market size in 2026

USD 3.9 Billion

Projected market size by 2033

USD 7.9 Billion

Growth rate

CAGR of 10.6% from 2026 to 2033

Base year

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Gear technology, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Spain; Italy; Russia; China; Japan; India; Australia; South Korea; Brazil; Argentina; Saudi Arabia; South Africa

Key companies profiled

Harmonic Drive LLC; NIDEC-SHIMPO Corporation; Stöber Antriebstechnik GmbH & Co. KG; WITTENSTEIN SE; GAM Enterprises, Inc.; DieQua Corporation; Neugart GmbH; Apex Dynamics, Inc.; Sumitomo Drive Technologies; Nabtesco Corporation; Cone Drive; Hiwin Corporation; Wilhelm Vogel GmbH; SureServo; Parker Hannifin Corp.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Precision Gearbox Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global precision gearbox market report based on gear technology, application, and region.

-

Gear Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Planetary

-

High Precision

-

Low Precision

-

Standard Precision

-

-

Harmonic

-

High Precision

-

Low Precision

-

Standard Precision

-

-

Cycloidal

-

High Precision

-

Low Precision

-

Standard Precision

-

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Military & Aerospace

-

Food & Beverage, and Tobacco

-

Machine Tools

-

Materials Handling

-

Packaging

-

Robotics

-

Medical

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Russia

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The global precision gearbox market size was estimated at USD 3.5 billion in 2025 and is expected to be USD 3.9 billion in 2026.

Europe dominated with a 34.1% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Robotics segment held the largest revenue share of 18.4% in 2025, while medical segment is is the fastest-growing application.

Planetary dominated the market in 2025, accounting for the highest revenue share at 65.3% due to its high torque density and compact structure, making it suitable for industrial automation and packaging machinery. Its ability to handle heavy loads with consistent precision supports adoption across robotics and material handling systems

The global precision gearbox market, in terms of revenue, is expected to grow at a compound annual growth rate of 10.6% from 2026 to 2033 to reach 7.9 billion by 2033

Some of the key players operating in the global precision gearbox market include Harmonic Drive LLC, NIDEC-SHIMPO Corporation, Stöber Antriebstechnik GmbH & Co. KG, WITTENSTEIN SE, GAM Enterprises, Inc., DieQua Corporation, Neugart GmbH, Apex Dynamics, Inc., Sumitomo Drive Technologies, Nabtesco Corporation, Cone Drive, Hiwin Corporation, Wilhelm Vogel GmbH, SureServo, Parker Hannifin Corp

Key factors driving the global precision gearbox market include rising adoption of industrial automation and robotics, increasing demand for accurate motion control in manufacturing, expansion of semiconductor and electronics production, and ongoing modernization of industrial machinery to improve efficiency and operational precision

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.