- Home

- »

- Advanced Interior Materials

- »

-

Pressure Sensitive Tapes Market Size, Industry Report, 2033GVR Report cover

![Pressure Sensitive Tapes Market Size, Share & Trends Report]()

Pressure Sensitive Tapes Market (2026 - 2033) Size, Share & Trends Analysis Report By Product (Specialty Tapes, Packaging Tapes, Consumer Tapes), By Region (North America, Europe, Asia Pacific, Central & South America, Middle East & Africa), And Segment Forecasts

Market Size, 2025

$74.5BMarket Estimate, 2026

$78.2BMarket Forecast, 2033

$110.6BCAGR, 2026–2033

5.1%Pressure Sensitive Tapes Market Summary

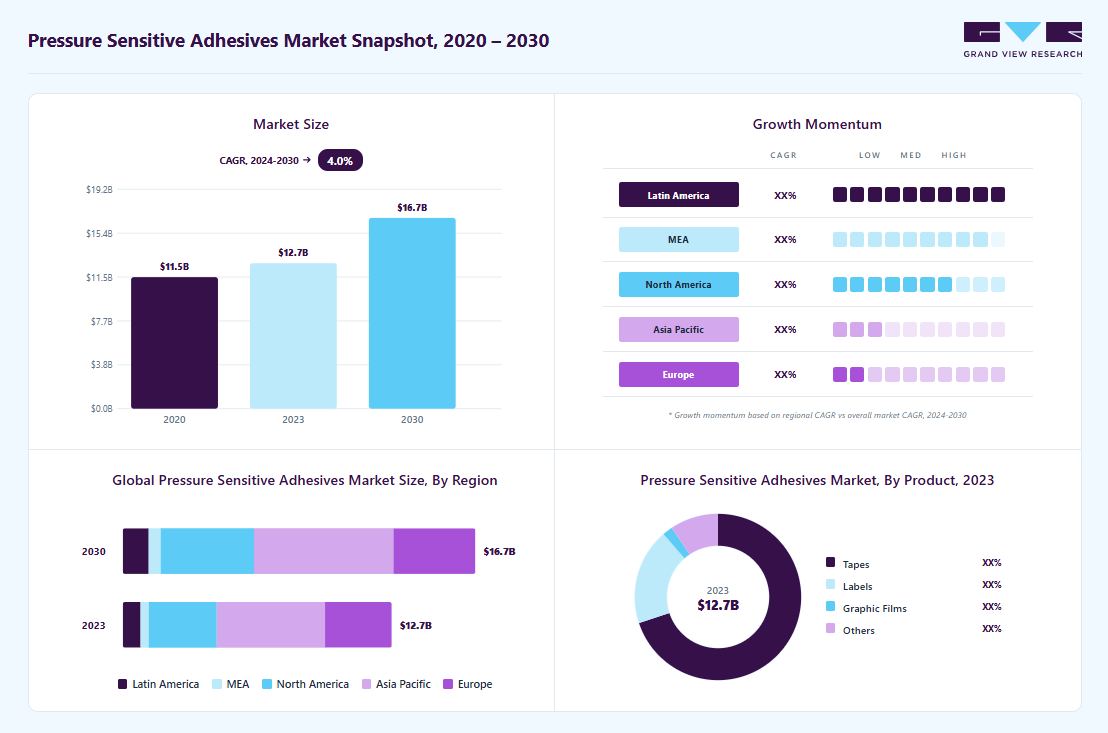

The global pressure sensitive tapes market size was estimated at USD 74.5 billion in 2025 and is projected to reach USD 110.6 billion by 2033, growing at a CAGR of 5.1% from 2026 to 2033. The demand for pressure sensitive tapes is increasing due to their widespread applicability across the packaging, automotive, healthcare, and electronics industries.

Key Market Trends & Insights

- Asia Pacific dominated the global pressure sensitive tapes market with the largest revenue share of 43.3% in 2025.

- The pressure sensitive tapes industry in China accounted for the largest market revenue share in the Asia Pacific in 2025.

- By product, the packaging tapes segment led the market with the largest revenue share of 50.5% in 2025.

Market Size & Forecast

- 2025 Market Size: USD 74.5 Billion

- 2033 Projected Market Size: USD 110.6 Billion

- CAGR (2026-2033): 5.1%

- Asia Pacific: Largest market in 2025

These tapes offer ease of use, requiring no heat, water, or solvent activation, which enhances operational efficiency. The booming e-commerce sector has significantly accelerated the need for packaging tapes, especially for sealing and securing shipments. In addition, the growing adoption of lightweight materials in automotive manufacturing is boosting the use of tapes as substitutes for mechanical fasteners. Rising healthcare needs, particularly in wound care and surgical applications, are further contributing to demand. The market is also benefiting from increased global industrialization and urbanization.Key drivers include the rapid growth of the packaging industry, driven by e-commerce and logistics expansion. Pressure-sensitive tapes are preferred due to their convenience and efficiency compared to adhesives and sealants. The automotive sector is another major driver, with increasing adoption in electric vehicles for bonding, insulation, and thermal management. Technological advancements in adhesive chemistry, particularly acrylic and silicone-based adhesives, are enhancing product performance and durability. Growth in the medical sector, especially in wound care and surgical applications, is further accelerating demand.

")

The pressure sensitive tapes industry is witnessing strong innovation in adhesive technologies, including the development of high-performance acrylic and silicone-based adhesives. There is a growing trend toward sustainable and biodegradable tapes due to environmental concerns. Customized, application-specific tapes are gaining traction, particularly in the automotive, electronics, and healthcare sectors. The use of pressure-sensitive tape in electric vehicles for battery insulation and thermal protection is an emerging trend. In addition, advancements in water-based adhesive technologies with low VOC emissions are gaining popularity. Smart tapes with enhanced properties such as temperature resistance and durability are also being developed. Digitalization and automation in manufacturing are further improving product quality and efficiency.

Market Concentration & Characteristics

The pressure sensitive tapes industry exhibits moderate to high concentration with the presence of several global players such as 3M, Avery Dennison, and Tesa SE. The industry is characterized by significant merger and acquisition activities, as established players aim to strengthen their market position and expand their product portfolios. High capital investment requirements and strong distribution networks act as barriers to entry for new players. Large companies dominate due to their technological capabilities and global presence. However, regional players also contribute to competition by offering cost-effective solutions. Innovation and product differentiation remain key competitive strategies.

The market faces competition from substitutes such as liquid adhesives, sealants, and mechanical fasteners. These alternatives are widely used across industries such as construction, automotive, and aerospace for bonding and sealing applications. However, pressure-sensitive tapes offer advantages such as ease of application, reduced processing time, and cleaner usage, which help mitigate substitution threats. Despite this, high-performance adhesives and fasteners still dominate in heavy-duty applications. The choice between tapes and substitutes depends on application requirements such as strength, durability, and cost. Continuous innovation in tape technology is helping reduce the impact of substitutes.

Product Insights

The packaging tapes segment led the market with the largest revenue share of 50.5% in 2025, due to the rapid expansion of e-commerce, logistics, and global trade activities. These tapes are widely used for carton sealing, bundling, and labeling applications, making them essential in the packaging industry. The increasing demand for secure and efficient packaging solutions, especially in the food & beverage and consumer goods sectors, has significantly boosted segment growth. In addition, their cost-effectiveness, ease of application, and compatibility with automated packaging systems have further strengthened their dominance. Growing cross-border trade and warehousing activities continue to drive consistent demand for packaging tapes globally.

The specialty tapes segment is expected to grow at the fastest CAGR of 5.3% over the forecast period, driven by rising demand for high-performance applications across industries such as automotive, electronics, and healthcare. These tapes are designed for specific functionalities, such as insulation, bonding, masking, and protection, and offer superior performance compared to conventional tapes. Increasing adoption of electric vehicles for thermal management and lightweight bonding solutions is a key growth driver. In addition, advancements in adhesive technologies and the growing need for customized solutions are further supporting segment expansion. The shift toward high-value, application-specific products is expected to accelerate the growth of specialty products in the coming years.

Regional Insights

Asia Pacific dominated the global pressure sensitive tapes market with the largest revenue share of 43.3% in 2025 and is projected to grow at the fastest CAGR during the forecast period, due to rapid industrialization, urbanization, and strong manufacturing activity. Countries like China, India, and Japan are key contributors, driven by expanding automotive, electronics, and packaging industries. The region accounted for over 36% market share, supported by cost-effective production and high consumption. The growing e-commerce and logistics sectors further boost demand for packaging tape. Increasing healthcare expenditure and infrastructure development are also contributing to market growth. The presence of major manufacturing hubs enhances supply chain efficiency.

China Pressure Sensitive Tapes Market Trends

The pressure sensitive tapes market in China accounted for the largest market revenue share in the Asia Pacific in 2025, driven by its strong manufacturing base and dominance in electronics and automotive production. The country is a major exporter of consumer goods, increasing the demand for packaging tapes. Rapid industrial growth and infrastructure expansion further support market growth. In addition, rising environmental awareness is encouraging the adoption of eco-friendly adhesive technologies. The growing electric vehicle sector is also boosting demand for advanced tape solutions. China’s role as a global manufacturing hub ensures consistent market expansion.

North America Pressure Sensitive Tapes Market Trends

The pressure-sensitive tapes market in North America is experiencing steady growth, driven by advanced manufacturing and strong demand from the packaging and automotive sectors. The region benefits from technological advancements and high adoption of innovative adhesive solutions. Growth in e-commerce has significantly increased the demand for packaging tapes. In addition, infrastructure development and construction activities contribute to market expansion. The presence of key global players further strengthens the regional market.

The pressure sensitive tapes market in the U.S. is primarily driven by the booming e-commerce sector, increasing the need for packaging solutions. Demand is also supported by the strong automotive and electronics industries. Pressure-sensitive tapes are widely used for bonding, insulation, and fastening applications. Government investments in infrastructure projects further boost demand. Technological innovation and product development remain key drivers of growth.

Europe Pressure Sensitive Tapes Market Trends

The pressure sensitive tapes market in Europe is supported by the strong automotive industry and increasing demand for packaging solutions. Countries like Germany and France play a significant role due to their industrial base. The region is also witnessing some shift toward sustainable, eco-friendly adhesive products. Increasing healthcare demand is further driving the use of medical tapes. Regulatory standards related to environmental safety are influencing product innovation.

The Germany pressure sensitive tapes market held a significant share in Europe in 2025, due to its robust automotive and manufacturing sectors. The demand for pressure sensitive tapes is high in packaging and medical applications. An aging population is increasing the need for healthcare-related tapes. In addition, advancements in automotive engineering are boosting demand for high-performance tapes. Germany’s strong industrial ecosystem supports consistent market growth.

Central & South America Pressure Sensitive Tapes Market Trends

The pressure sensitive tapes market in Central & South America is growing due to increasing demand from the packaging and consumer goods industries. Expanding e-commerce and food & beverage sectors are key contributors. Countries like Brazil are witnessing rising adoption of sustainable packaging solutions. Industrial growth and urbanization are further supporting demand. The market is expected to grow steadily as economic conditions improve.

Middle East & Africa Pressure Sensitive Tapes Market Trends

The pressure sensitive tapes market in the Middle East & Africa is driven by infrastructure development and construction activities. Growing investments in real estate and industrial projects are boosting demand for tapes. The adoption of sustainable packaging solutions is also increasing in the region. In addition, the expansion of logistics and transportation sectors supports market growth. Government initiatives for economic diversification further contribute to demand.

Key Pressure Sensitive Tapes Company Insights

Some of the key players operating in the market include Nitto Denko and Tesa SE

-

Nitto Denko Corporation is a prominent player in the global market, specializing in advanced materials and high-performance adhesive solutions. The company focuses on niche, technology-driven applications across the electronics, automotive, and industrial sectors.

-

Tesa SE is a leading global manufacturer of pressure sensitive adhesive solutions and a key player in the global market. The company offers a wide portfolio of specialty, industrial, and consumer tapes catering to sectors such as automotive, electronics, packaging, and construction.

LINTEC Corporation and Berry Global are among the emerging market participants in the pressure-sensitive tapes industry.

-

LINTEC Corporation is a key participant, known for its expertise in adhesive materials, specialty papers, and labeling solutions. The company provides a wide range of pressure-sensitive tapes used in electronics, automotive, and packaging applications, with a strong focus on precision and functional performance.

-

Berry Global Inc. is a prominent player in the global market, primarily through its expertise in plastic packaging and engineered materials. The company offers a range of adhesive tapes and films used in packaging, industrial, and hygiene applications.

Key Pressure Sensitive Tapes Companies:

The following key companies have been profiled for this study on the pressure sensitive tapes market.

- Tesa SE

- 3M

- Nitto Denko

- LINTEC Corporation

- Avery Dennison

- Intertape Polymer

- Berry Global

- Henkel

- Lohmann

- H.B. Fuller

- Scapa

- Arkema

- Alamo Tape

- Adhesive Applications

- Adhesives Research

- Flexcon

- Lamart

- Mactac

- Pro Tapes

- Specialty Tapes (STM)

- Shurtape Technologies, LLC

- Vybond

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: 3M; Avery Dennison; Nitto Denko; Tesa SE; H.B. Fuller - Focus on portfolio diversification across specialty, packaging, and industrial tapes to reduce dependency on a single segment

- Heavy investment in R&D and sustainable adhesive technologies (water-based, solvent-free, bio-based)

- Expansion through global manufacturing networks and long-term OEM partnerships

- Strong brand recognition and customer trust built over decades

- Advanced technology capabilities and proprietary formulations

- Well-established distribution and supply chain infrastructure across regions

- High operational and compliance costs, especially due to global regulations

- Slower decision-making and innovation cycles compared to smaller players

- Exposure to raw material price volatility impacting margins at scale

Emerging Players: Adhesives Research; Lamart; Mactac; Pro Tapes Specialties; Tapes (STM); Shurtape Technologies, LLC - Focus on niche and application-specific segments such as medical, electronics, or custom tapes

- Emphasis on flexible manufacturing and customized solutions

- Growth through regional expansion and partnerships with local distributors

- High agility and faster response to market changes

- Ability to offer cost-competitive and tailored products

- Strong focus on specialized or underserved market segments

- Limited global presence and brand visibility

- Lower R&D capabilities and technological depth

- Dependence on few customers or regional markets, increasing business risk

Recent Developments

-

In January 2026, Henkel announced the acquisition of ATP Adhesive Systems, a company specializing in high-performance water-based and specialty pressure-sensitive tapes. This move significantly strengthens Henkel’s position in sustainable PSA solutions by expanding its portfolio across water-based, hot melt, and solvent-based adhesive technologies.

-

In November 2024, Atlas Tapes SA announced the acquisition of PPM Industries Group, an Italy-based adhesive tape manufacturer. The deal expanded Atlas Tapes’ manufacturing footprint and product portfolio across packaging, masking, and specialty tapes.

Pressure Sensitive Tapes Market Report Scope

Report Attribute

Details

Market size value in 2026

USD 78.2 billion

Revenue forecast in 2033

USD 110.6 billion

Growth rate

CAGR of 5.1% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Volume in million square meters, revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; Italy; France; Spain; China; Japan; India; Australia; Brazil

Key companies profiled

Tesa SE; 3M; Nitto Denko; LINTEC Corporation; Avery Dennison; Intertape Polymer; Berry Global; Henkel; Lohmann; H.B. Fuller; Alamo Tape; Arkema; Adhesive Applications; Adhesives Research; Flexcon; Lamart; Mactac; Pro Tapes; Specialty Tapes (STM); Shurtape Technologies, LLC; Vybond

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Pressure Sensitive Tapes Market Report Segmentation

This report forecasts revenue growth at regional & country levels and provides an analysis on the industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global pressure sensitive tapes market report based on the product and region:

-

Product Outlook (Volume, Million Square Meters; Revenue, USD Billion, 2021 - 2033)

-

Specialty Tapes

-

By Technology

-

Hot Melt

-

Water-based

-

Solvent-based

-

Radiation-cured

-

-

By Backing Material

-

Woven/Nonwoven

-

Polyvinylchloride (PVC)

-

Polypropylene (PP)

-

Polyethylene Terephthalate (PET)

-

Foam

-

Metal

-

Other Backing Materials

-

-

By Adhesive Chemistry

-

Acrylic

-

Rubber

-

Silicone

-

Other Adhesive Chemistry

-

-

By Application

-

Automotive

-

Aerospace

-

White goods

-

Electronics

-

Semiconductors

-

Electrical

-

Paper & printing

-

Construction

-

Medical

-

Hygiene

-

Retail & Graphics

-

Other Applications

-

-

-

Packaging Tapes

-

By Technology

-

Solvent-based

-

Water-based

-

Hot-melt

-

Others

-

-

By Backing Material

-

Biaxially Oriented Polypropylene (BOPP)

-

Polyvinyl Chloride (PVC)

-

Paper

-

Polyethylene (PE)

-

Polyethylene Terephthalate (PET)

-

Others

-

-

By Adhesive Chemistry

-

Acrylic

-

Rubber-based

-

Silicone

-

Others

-

-

By Packaging Type

-

Carton Sealing

-

Masking

-

Labeling

-

Strapping

-

Bundling

-

Security Tapes

-

Others

-

-

-

Consumer Tapes

-

By Technology

-

Solvent-based

-

Water-based

-

Hot melt

-

Others

-

-

By Backing Material

-

Paper

-

Polypropylene (PP)

-

Polyvinyl Chloride (PVC)

-

Foam

-

Fabric

-

Others

-

-

By Adhesive Chemistry

-

Acrylic

-

Rubber-based

-

Silicone

-

Others

-

-

-

-

Regional Outlook (Volume, Million Square Meters; Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia

-

-

Central & South America

-

Brazil

-

-

Middle East and Africa

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Product Portfolio Benchmarking

The report was customized to benchmark leading pressure sensitive tape manufacturers across product categories such as packaging tapes, masking tapes, double-sided tapes, electrical tapes, specialty tapes, and medical tapes. It compared players based on adhesive technology, backing material, application coverage, performance attributes, pricing positioning, and innovation focus.

The report was customized to benchmark leading pressure sensitive tape manufacturers across product categories such as packaging tapes, masking tapes, double-sided tapes, electrical tapes, specialty tapes, and medical tapes. It compared players based on adhesive technology, backing material, application coverage, performance attributes, pricing positioning, and innovation focus. Regional Segmentation

The study incorporated region-specific analysis of the pressure sensitive tapes market across target geographies, covering demand by end-use industries such as packaging, automotive, electronics, healthcare, construction, and consumer goods. It also assessed regional growth drivers, regulatory trends, local manufacturing presence, and channel dynamics.

The study incorporated region-specific analysis of the pressure sensitive tapes market across target geographies, covering demand by end-use industries such as packaging, automotive, electronics, healthcare, construction, and consumer goods. It also assessed regional growth drivers, regulatory trends, local manufacturing presence, and channel dynamics.

Supplier-Buyer Mapping

A customized supplier-buyer mapping section was developed to identify key tape manufacturers, converters, distributors, large-volume buyers, OEMs, and end-use customers across priority applications. It assessed supply relationships, procurement behavior, buyer concentration, and potential partnership opportunities.

A customized supplier-buyer mapping section was developed to identify key tape manufacturers, converters, distributors, large-volume buyers, OEMs, and end-use customers across priority applications. It assessed supply relationships, procurement behavior, buyer concentration, and potential partnership opportunities.

Frequently Asked Questions About This Report

The global pressure sensitive tapes market size was estimated at USD 74.5 billion in 2025 and is expected to reach USD 78.2 billion in 2026.

The global pressure sensitive tapes market is expected to grow at a compound annual growth rate of 5.1% from 2026 to 2033 to reach USD 110.6 billion by 2033.

The packaging tapes segment accounted for largest pressure sensitive tapes market share of 50.5% in 2025, driven by the rapid expansion of e-commerce, logistics, and global trade activities.

Rising demand from e-commerce packaging, increasing adoption in automotive and electronics for lightweight bonding, and growing use in healthcare applications are key factors driving the pressure sensitive tapes market.

Some key players in the pressure sensitive tapes market include Tesa SE, 3M, Nitto Denko, LINTEC Corporation, Avery Dennison, Intertape Polymer, Berry Global, Henkel, H.B. Fuller, Lohmann, Scapa, Arkema, Alamo Tape, Adhesive Applications, Adhesives Research, Flexcon, Lamart, Mactac, Pro Tapes, Specialty Tapes (STM), Shurtape Technologies, LLC, and Vybond.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.