- Home

- »

- Clinical Diagnostics

- »

-

Pyrogen Testing Market Size & Share Report, 2026-2033GVR Report cover

![Pyrogen Testing Market (2026 - 2033)Report]()

Pyrogen Testing Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Instruments, Consumables, Services), By Test Type (LAL Test, In Vitro Pyrogen Test, Rabbit Test), By End-use (Pharmaceutical And Biotechnology Companies, Medical Devices Companies), And Segment Forecasts

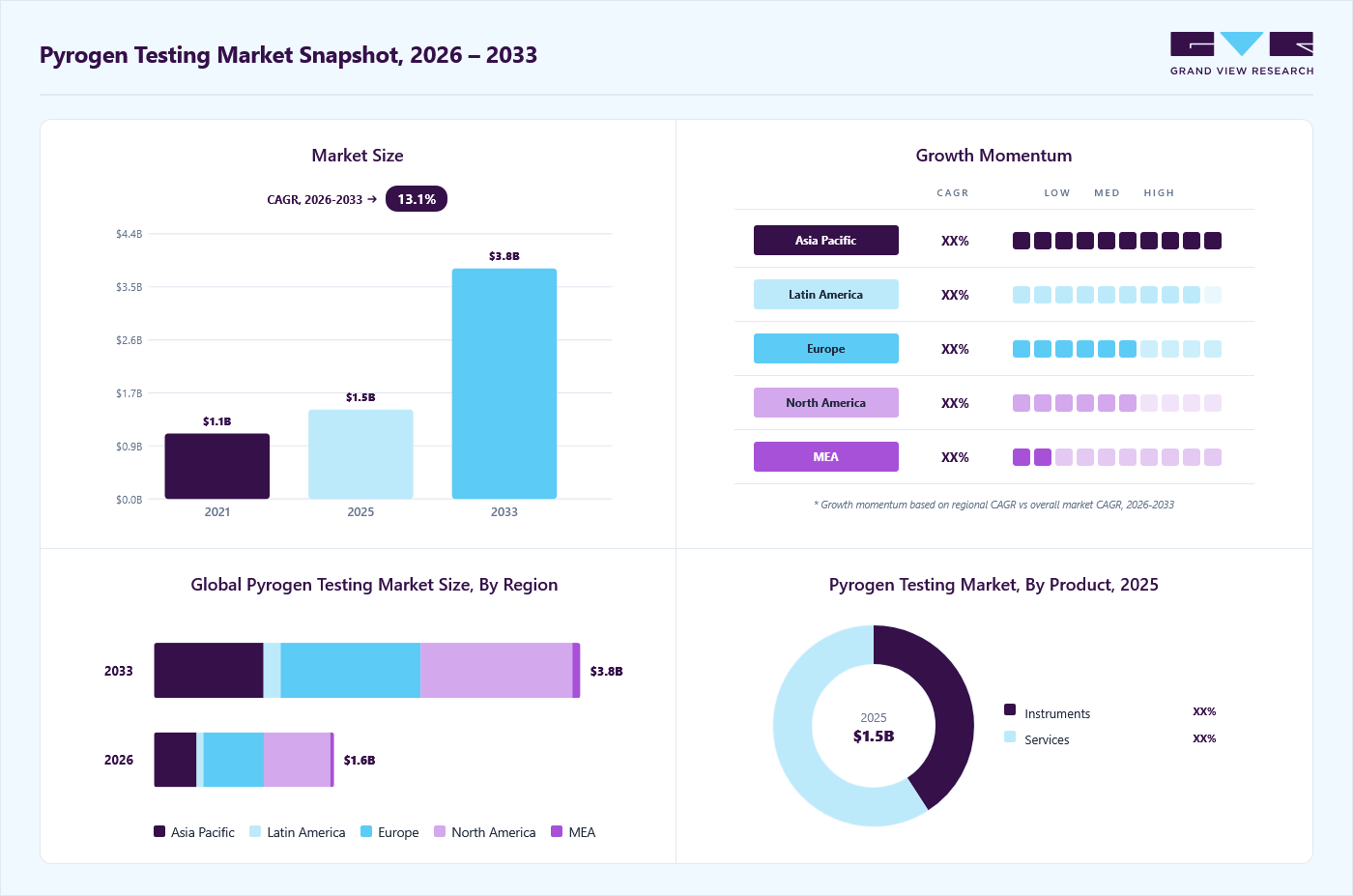

Market Size, 2025

$1.5BMarket Estimate, 2026

$1.6BMarket Forecast, 2033

$3.8BCAGR, 2026–2033

13.1%Pyrogen Testing Market Summary

The global pyrogen testing market size was valued at USD 1.5 billion in 2025 and is projected to grow from USD 1.6 billion in 2026 to USD 3.8 billion by 2033, at a CAGR of 13.1% from 2026 to 2033. The market in North America dominated with a revenue share of 37.0% in 2025. The increasing demand for pyrogen testing products in the pharmaceutical and biotechnology industries is a significant driver of market growth.

Key Market Trends & Insights

- By product: Consumables segment led the market with the largest revenue share of 43.1% in 2025.

- By type: In vitro pyrogen test segment led the market with the largest revenue share of 56.1% in 2025.

- By end use: Pharmaceutical and biotechnology companies segment led the market with the largest revenue share of 61.0% in 2025.

Regional Highlights

- Largest regional market: North America (37.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 1.5 Billion

- Estimated market size in 2026: USD 1.6 Billion

- Projected market size by 2033: USD 3.8 Billion

- CAGR (2026-2033): 13.1%

The rapid expansion of these industries, coupled with the rising number of new therapeutic launches, is expected to propel the demand for pyrogen testing products further. This growth highlights the critical role of pyrogen testing in ensuring the safety and efficacy of pharmaceutical and biotechnological products.")

Several regulatory bodies and governments are taking various initiatives to train and create awareness about pyrogen testing. Government initiatives worldwide are pivotal in accelerating this transition. In June 2024, the 179th session of the European Pharmacopoeia (Ph. Eur.) Commission marked a significant advancement for animal welfare and contemporary pyrogen testing practices. During this session, the Commission approved the removal of the Rabbit Pyrogen Test (RPT) from 57 revised texts and introduced a comprehensive new general chapter on Pyrogenicity. This decision effectively abolished the RPT requirement across all Ph. Eur. texts, solidifying the transition toward in vitro testing methodologies, such as the Monocyte Activation Test (MAT).

Increasing investment in R&D by the government and manufacturing companies for product development is one of the major factors contributing to the market's growth. New product development and launch is a key strategy acquired by manufacturers to maintain their dominance and to get maximum revenue-share in the sector. As stated by the European Federation of Pharmaceutical Industries and Associations (EFPIA), in 2023, the research-based pharmaceutical industry invested around USD 48.65 billion in R&D in Europe in 2022. Hence, the need for pyrogen testing products is anticipated to upsurge during the forecast period.

Furthermore, the market is driven by the increasing demand for therapeutic drugs. Several companies are actively involved in developing new drug therapies. For instance, in 2023, the FDA approved 55 new drugs. Pyrogen testing in drug development specifies the absence or presence of pyrogens in parenteral pharmaceutical products. Moreover, the sterility of any drug does not indicate that it is pyrogen-free. Therefore, drugs that are expected to be sterile must be tested for the presence of pyrogens to control fevered reactions in patients.

Market Dynamics

The pyrogen testing market is witnessing growth due to the expansion of pharmaceutical and biotechnology manufacturing activities, particularly the increasing production of biologics, vaccines, and sterile injectable drugs that require stringent safety and quality testing. Market growth is constrained by the high costs associated with advanced pyrogen testing platforms and the regulatory validation requirements necessary for method implementation. Growth opportunities are emerging from the increasing adoption of animal-free pyrogen testing technologies, including recombinant-based assays, supported by evolving regulatory acceptance. Rising investments in biologics manufacturing and the growing demand for sterile injectable therapies are further creating favorable conditions for market expansion.

Growing Pharmaceutical and Biotechnology Industry is a major driver of the Pyrogen Testing Market because the expansion of drug manufacturing, biologics production, and injectable therapeutics has significantly increased the need for stringent safety and contamination testing. Pyrogen testing is mandatory for injectable pharmaceuticals, vaccines, intravenous drugs, and implantable medical products to ensure that fever-causing contaminants are absent before patient administration. According to the European Federation of Pharmaceutical Industries and Associations, the global pharmaceutical market continued to expand strongly in 2024, with pharmaceutical production and medicine demand rising due to aging populations, chronic disease prevalence, and increasing access to healthcare. The United States remained the world’s largest pharmaceutical market in 2024, accounting for nearly 49% of global pharmaceutical sales, while emerging manufacturing hubs such as India and China continued rapid expansion, increasing the requirement for endotoxin and pyrogen testing in manufacturing facilities.

The biotechnology industry has also accelerated demand for pyrogen testing due to the increasing production of biologics and advanced therapies. According to the U.S. Food and Drug Administration, 50 novel drugs were approved in December 2024 (full-year approvals for 2024), many of which included injectable biologics, monoclonal antibodies, and specialty therapies requiring mandatory pyrogen safety assessments during development and commercial manufacturing. Since biologic medicines are highly sensitive to microbial contamination and are commonly administered through injections or infusions, manufacturers must conduct extensive pyrogen testing to comply with regulatory standards and patient safety protocols. The increasing approvals of biologics and biosimilars have therefore expanded quality-control requirements across pharmaceutical and biotech production sites.

In addition, the rapid growth of vaccine and sterile injectable production is further strengthening the role of pyrogen testing. Data from the India Brand Equity Foundation released in January 2025 showed that India, one of the world’s fastest-growing pharmaceutical manufacturing centers, supplies approximately 20% of the global generic medicine demand by volume and remains a major vaccine producer worldwide. As sterile injectable manufacturing expands, pharmaceutical companies are increasing investments in endotoxin and pyrogen testing systems to meet international safety standards for exports. This growing manufacturing footprint across pharmaceutical and biotechnology industries continues to create sustained demand for pyrogen testing technologies and services.

High Cost of Advanced Testing Technologies acts as a major restraint in the pyrogen testing Market because pharmaceutical and biotechnology companies must invest heavily in sophisticated endotoxin and pyrogen detection systems, validation protocols, and skilled laboratory personnel. Advanced testing methods such as recombinant factor C (rFC) assays, kinetic chromogenic systems, and automated endotoxin detection platforms involve substantial capital expenditure, making adoption difficult for small and medium-sized manufacturers. For example, pricing data released in March 2026 for commercially available endotoxin testing instruments showed automated systems costing over USD 10,000 per unit, excluding recurring reagent, calibration, and validation expenses, creating a significant financial burden for laboratories with limited budgets.

Additionally, regulatory validation requirements further increase operational costs for pharmaceutical firms transitioning to advanced pyrogen testing methods. In March 2026, the U.S. Food and Drug Administration updated its guidance on pyrogen and endotoxin testing, emphasizing that manufacturers adopting recombinant reagent-based assays must verify method suitability and conduct product-specific validation before implementation. These additional compliance and verification requirements increase both testing costs and implementation timelines, particularly for companies moving away from traditional Limulus Amebocyte Lysate (LAL)-based methods. As a result, cost-intensive technology adoption remains a significant challenge limiting faster expansion of the pyrogen testing market.

Adoption of Recombinant Technologies represents a major opportunity in the pyrogen testing market as pharmaceutical manufacturers increasingly shift from traditional animal-based pyrogen testing to recombinant and in vitro alternatives. Recombinant Factor C (rFC) technology, which replaces horseshoe crab-derived reagents used in conventional Limulus Amebocyte Lysate (LAL) testing, is gaining momentum due to higher sustainability, improved specificity, and reduced biological variability. In May 2025, the United States Pharmacopeia introduced Chapter Bacterial Endotoxins Test Using Recombinant Reagents, formally supporting recombinant reagent-based testing methods and expanding industry confidence in animal-free endotoxin testing approaches.

Regulatory developments are further accelerating this transition. In June 2024, the European Pharmacopoeia Commission decided to abolish the traditional rabbit pyrogen test effective July 2025, encouraging manufacturers to adopt validated alternatives such as recombinant Factor C (rFC) and monocyte activation tests (MAT). Furthermore, from January 2026, animal-based pyrogen testing was officially removed from European Pharmacopoeia texts, making modern recombinant and in vitro approaches the preferred standard for endotoxin detection in many pharmaceutical applications. These regulatory shifts are creating strong growth opportunities for providers of recombinant pyrogen testing technologies and automated endotoxin testing platforms.

Additionally, recombinant technologies are seeing increased commercial adoption in biologics manufacturing. According to the U.S. Food and Drug Administration, as of 2025, recombinant Factor C testing had already been used in more than 20 clinical products under Investigational New Drug (IND) development, with rFC-based endotoxin tests approved in multiple biologics applications. This increasing acceptance highlights a growing opportunity for pyrogen testing companies to develop innovative recombinant testing kits and support pharmaceutical manufacturers transitioning toward sustainable, high-precision safety testing methods.

Market Concentration & Characteristics

The market growth stage is medium, and the market growth is accelerating. The innovation in the pyrogen testing market is driven by factors such as technological advancements, increasing demand for pyrogen testing, and the need for animal-free and reliable testing methods.

The pyrogen testing market is also characterized by the leading players' interest in merger and acquisition (M&A) activity. This is due to several factors, including the desire to gain access to new pyrogen technologies, expand the customer base in the pyrogen testing market, the need to consolidate in a rapidly growing market, and its usage in R&D.

The pyrogen testing market is significantly influenced by regulations, which drive the adoption of these testing assays and kits. Strict guidelines from regulatory bodies such as the FDA mandate the use of pyrogen testing to ensure the safety and efficacy of pharmaceutical products. Moreover, it has led to a growing emphasis on animal-free pyrogen testing.

In the pyrogen testing market, regional expansion involves pyrogen testing companies strategically extending their activities beyond current geographic locations. Hence, the market players undertake various business initiatives, such as partnerships, geographical expansion, and collaboration, to gain a regional customer base.

Analyst Perspective

The Pyrogen Testing Market is expected to witness steady growth due to increasing pharmaceutical and biotechnology production, rising biologics and vaccine manufacturing, and stricter regulatory requirements for product safety. Growing demand for injectable therapeutics and sterile medical devices continues to strengthen the need for reliable pyrogen and endotoxin testing solutions. Additionally, regulatory emphasis on contamination-free manufacturing is supporting market expansion across pharmaceutical and medical device industries. Increasing regulatory support for sustainable, animal-free testing methods is expected to create new growth opportunities for technology providers. However, high implementation costs and complex validation requirements may continue to challenge smaller market participants. Companies investing in automation, recombinant technologies, and global regulatory compliance are likely to strengthen their competitive positioning over the forecast period.

Product Insights

Based on product, the consumables segment led the market with the largest revenue share of 43.1% in 2025, the consumables segment was the largest segment with a share of 43.60% and is estimated to maintain its dominance during the forecast period. The growing adoption of in vitro and non-animal testing methods has intensified the demand for advanced consumables. In June 2024, FUJIFILM Wako Chemicals launched the PYROSTAR Neo+ and LumiMAT, advancing the market with innovative, sustainable consumables. These products exemplify the shift toward recombinant and animal-free testing methods, reflecting the industry's focus on innovation, regulatory compliance, and sustainability.

The instruments segment is expected to show significant growth during the forecast period owing to the technological advancement in products. For instance, the PyroDetect System is a verified non-animal substitute to replace the rabbit test that offers high quality in vitro detection of both non-endotoxin and endotoxin contamination.

Type Insights

Based on type, the pyrogen testing industry has been segmented into LAL tests, in vitro tests, and rabbit tests. The in vitro pyrogen test segment led the market with the largest revenue share of 56.1% in 2025. The growth is attributed to the rising demand for animal-free detection tests and their high reproducibility and reliability during detection. For instance, In February 2023, the European Pharmacopoeia (Ph. Eur.) published 59 texts involving the rabbit pyrogen test replacement approach for public consultation in Pharmeuropa 35.1. LAL test is further categorized into turbidimetric, chromogenic, and gel clot tests.

Furthermore, the in vitro pyrogen test segment had a significant market share in the pyrogen testing market in 2024. This testing method has gained widespread acceptance due to its ability to detect endotoxins and pyrogens in a controlled, animal-free environment, supported by advancements in recombinant technology. Notable innovations such as recombinant Factor C (rFC) and Monocyte Activation Test (MAT) systems have significantly enhanced the efficiency, reliability, and sustainability of endotoxin detection processes. Advancements in automation, recombinant technologies, and efficient endotoxin detection systems are pivotal in this transition, delivering faster, more accurate, and reproducible results that reduce time-to-market for pharmaceutical and medical device companies.

End-use Insights

Based on end use, the pharmaceutical and biotechnology companies segment led the market with the largest revenue share of 61.0% in 2025. The growth is attributed to the rising production of pharmaceuticals, biopharmaceuticals, and other biologic products. Key players offering pyrogen testing instruments include Lonza Group, Thermo Fisher Scientific, and FUJIFILM Wako Chemicals, which are known for their broad portfolio of endotoxin detection products, including LAL-based assays and in vitro pyrogen detection

The medical devices companies' segment is expected to grow significantly over the forecast period. The consideration of applying pyrogen testing for medical devices arises from their potential indirect or direct exposure to human blood cells. Pyrogenicity tests are imperative to assess the safety of products that come into direct or indirect contact with blood circulation, cerebrospinal fluid (CSF), the lymphatic system, and those that interact systemically with the human body. Official methods for assessing the medical devices' pyrogenicity and materials include the in vitro bacterial endotoxin test and the in vivo rabbit pyrogenicity test.

Regional Insights

North America dominated the pyrogen testing market with the largest revenue share of 37.0% in 2025. The growth is attributed to the rising number of chronic diseases needing developments in drug therapy. The growing adoption of ethical and efficient in vitro pyrogen tests has become a cornerstone of this dominance. Traditional animal-based tests, like the Rabbit Pyrogen Test, are being steadily replaced by advanced alternatives such as the Monocyte Activation Test and LAL-based assays, which include chromogenic, turbidimetric, and gel clot methods.

U.S. Pyrogen Testing Market Trends

The pyrogen testing market in the U.S. held the largest share in the North America region in 2025. A recent development in January 2024 exemplifies this evolution: Charles River Laboratories International, Inc. introduced the Endosafe Trillium rCR cartridge, a groundbreaking advancement in BET technology. This innovation integrates their flagship Endosafe cartridge with recombinant cascade reagent (rCR) technology, providing an animal-free alternative that enhances testing efficiency, accelerates manufacturing processes, and supports sustainability initiatives.

Europe Pyrogen Testing Market Trends

The Europe pyrogen testing market is characterized by its robust yet intricate landscape, driven by stringent regulatory frameworks, growing pharmaceutical and biotechnology industries, and the increasing adoption of innovative testing methods. Valued significantly in recent years, the market shows strong growth potential fueled by rising investments in healthcare research, expansion of drug development activities, and heightened focus on patient safety

The pyrogen testing market in UK is expected to grow over the forecast period due to a significant approval of drugs. Demand is primarily driven by pharmaceutical, biotechnology, and medical device sectors, where ensuring product sterility and safety is paramount.

The pyrogen testing market in France is expected to grow over the forecast period. The growth is attributed to the growing initiatives in the therapeutic drugs field. The country is undertaking several initiatives to increase the access of drugs to the targeted patients in France.

The pyrogen testing market in Germany is expected to grow over the forecast period. The pharmaceutical and biotechnology sectors, which heavily rely on pyrogen testing to ensure the safety of their products, continue to expand in the country. For instance, the 12th PharmaLab Congress will be held in Düsseldorf/Neuss, Germany, from November 25-27, 2024, focusing on advancements in analytical and microbiological quality control for the pharmaceutical industry.

Asia Pacific Pyrogen Testing Market Trends

Asia Pacific is estimated to grow at the fastest CAGR of 12.4% over the forecast period. Many manufacturers target Asian countries, such as China & India, for drug discovery, development, and production. In addition, clinical research organizations are focusing on Asian countries for clinical trials. The availability of less stringent government regulations for drug development, the vast genome pool, and the rapidly developing healthcare infrastructure in this region are some of the major factors responsible for the growth of the sector in this region.

The pyrogen testing market in China is expected to grow over the forecast period. The growth is attributed to the increasing presence of key players in the country, owing to the reasonable manufacturing cost. Government policies promoting quality and safety in medical devices and drugs have led to the widespread use of LAL and turbidimetric tests for batch release testing, while the country’s focus on biotechnology innovation encourages the adoption of rabbit tests for specialized products.

The pyrogen testing market in Japan is dominated by global leaders such as Charles River Laboratories and bioMérieux SA, alongside regional players like FUJIFILM Wako Pure Chemical Corporation, which has a strong presence due to its expertise in pyrogen detection kits. In June 2024, FUJIFILM Wako Pure Chemicals Corporation introduced the LumiMAT Pyrogen Detection Kit (LumiMAT) and PYROSTAR Neo+ as innovative alternatives to traditional methods for detecting pyrogens and endotoxins.

Key Pyrogen Testing Company Insights

Some of the leading players in the pyrogen testing market are Lonza and Charles River Laboratories. These companies are actively engaged in business initiatives, such as product launches and acquisition of companies. Moreover, these companies have a global presence, which helps them to get access to affordable manufacturing facilities and a broad customer base. These factors cumulatively strengthen their presence in the pyrogen testing market. The emerging players in the pyrogen testing market mostly focus on partnerships and collaborations to increase their presence in the pyrogen testing market. Companies generally offer a compact product portfolio and focus on capturing local markets.

Key Pyrogen Testing Companies

The following key companies have been profiled for this study on the pyrogen testing market.

-

Charles River Laboratories

-

Novo Nordisk

-

Merck KGaA

-

GenScript

-

bioMérieux SA

-

Lonza Group

-

Thermo Fisher Scientific, Inc.

-

Seikagaku Biobusiness Corporation

-

FUJIFILM Wako Chemicals U.S.A. Corporation (Pyrostar)

-

MiCAN Technologies Inc.

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Well-Established Players (Charles River Laboratories, Novo Nordisk, Merck KGaA)

- Matured players emphasize product portfolio expansion, regulatory compliance, acquisitions, automation, global distribution networks, and long-term contracts with pharmaceutical and medical device manufacturers.

- Matured players benefit from strong brand recognition, established regulatory expertise, extensive customer networks, broad product portfolios, and advanced R&D capabilities ensuring reliability and trust.

- Matured players may experience slower innovation, high operational costs, dependence on legacy testing methods, and challenges adapting quickly to recombinant and animal-free technologies.

Emerging Players (Seikagaku Biobusiness Corporation, MiCAN Technologies Inc.)

- Emerging players focus on recombinant technologies, niche testing solutions, strategic partnerships, flexible pricing, and regional expansion to gain market presence and attract pharmaceutical and biotech customers.

- Emerging players gain advantage through innovation in animal-free testing, cost-effective solutions, customization, and rapid adoption of advanced pyrogen detection technologies tailored to evolving regulations.

- Emerging players often face limited financial resources, lower global reach, restricted regulatory expertise, and difficulties competing with established firms in large-scale pharmaceutical contracts.

Recent Developments

-

In December 2024, Ellab acquired PharmaProcess in Italy and Switzerland, enhancing its life science services. The partnership integrates PharmaProcess' regulatory expertise with Ellab’s compliance solutions, providing end-to-end support for pharmaceutical and biotech clients in these regions.

-

In September 2024, Lonza Walkersville began the expansion of its endotoxin assay production facility in Walkersville, MD. The 18,000-square-foot upgrade will enhance manufacturing capacity to meet the rising demand for endotoxin assays used in ensuring the safety and compliance of injectable drugs and medical devices.

-

In June 2024, FUJIFILM Wako Pure Chemicals launched two new pyrogen and endotoxin tests: LumiMAT Pyrogen Detection Kit, a next-generation monocyte activation test, and PYROSTAR Neo+, a recombinant protein reagent for bacterial endotoxin detection, available globally in July 2024.

-

In October 2023, Lonza announced the launch of two monocyte activation test (MAT) systems: PyroCell MAT Human Serum (HS) Rapid System and PyroCell MAT Rapid System.

Pyrogen Testing Market Report Scope

Report Attribute

Details

Market size in 2025

USD 1.5 billion

Estimated market size in 2026

USD 1.6 billion

Projected market size by 2033

USD 3.8 billion

Growth rate

CAGR of 13.1% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, product, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Norway; Denmark; Sweden; China; Japan; India; South Korea; Australia; Thailand; Brazil; Argentina; Saudi Arabia; South Africa; UAE; Kuwait

Key companies profiled

Charles River Laboratories; Ellab A/S; Merck KGaA; GenScript; bioMérieux SA; Lonza; Thermo Fisher Scientific, Inc.; Associates of Cape Cod, Inc.; FUJIFILM Wako Chemicals U.S.A. Corporation (Pyrostar); MiCAN Technologies Inc.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Pyrogen Testing Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global pyrogen testing market report based on product, test type, end-use, and region.

-

Product Outlook (Revenue, USD Billion, 2021 - 2033)

-

Consumables

-

Instruments

-

Services

-

-

Test Type Outlook (Revenue, USD Billion, Number of Tests, in Thousands, 2021 - 2033)

-

LAL test

-

Chromogenic test

-

Turbidimetric test

-

Gel clot test

-

-

In vitro pyrogen test

-

Recombinant Factor C (rFC) testing

-

Monocyte Activation Test (MAT)

-

-

Rabbit test

-

-

End-use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Pharmaceutical and biotechnology companies

-

Medical devices companies

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

U.K.

-

France

-

Italy

-

Spain

-

Sweden

-

Denmark

-

Norway

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Research Methodology

The pyrogen testing market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each pyrogen testing segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Products

Revenue capture definition

Consumables

The Consumables segment in the Pyrogen Testing Market includes reagents, assay kits, endotoxin detection chemicals, cartridges, and testing media used repeatedly during pyrogen analysis. Revenue capture comes from recurring purchases by pharmaceutical, biotechnology, and medical device laboratories for routine testing and quality assurance.

Instrument

The Instruments segment comprises equipment and automated systems used for pyrogen and endotoxin detection, including readers, incubators, spectrophotometers, and endotoxin testing analyzers. Revenue capture is generated through sales, installations, upgrades, and maintenance of testing instruments across laboratories.

Services

The Services segment includes outsourced pyrogen testing, laboratory validation, consulting, regulatory compliance support, and maintenance services. Revenue capture derives from contract testing agreements, quality control services, and technical support provided to pharmaceutical and biotechnology companies.

Segment - Type

Revenue capture definition

LAL Test (Limulus Amebocyte Lysate Test)

Revenue generated from sales of LAL reagents, assay kits, instruments, consumables, software, validation services, and endotoxin testing performed by laboratories and contract testing providers.

In Vitro Pyrogen Test

Revenue derived from recombinant assay kits, cell-based testing solutions, instruments, consumables, laboratory services, automation systems, and regulatory validation support for non-animal testing methods.

Rabbit Test

Revenue generated from rabbit pyrogen testing services, laboratory procedures, animal maintenance, compliance testing, and associated consumables used in regulated pharmaceutical safety assessments.

Segment - End Use

Revenue capture definition

Pharmaceutical and Biotechnology Companies

Revenue generated from pyrogen testing kits, reagents, instruments, consumables, validation services, and outsourced testing conducted for pharmaceutical and biotechnology product development and manufacturing.

Medical devices companies

Revenue derived from testing reagents, endotoxin detection systems, consumables, compliance services, and contract laboratory testing for medical device sterilization and quality assurance.

Others

Revenue captured from laboratory testing services, research-related pyrogen assays, consumables, reagents, outsourced quality testing, and regulatory support activities.

Estimation Model

The research methodology for the pyrogen testing market involves a combination of primary and secondary research to ensure accurate market estimation and forecasting. Secondary research includes data collection from company annual reports, regulatory publications, scientific journals, government databases, and industry associations to assess market trends, segmentation, and competitive landscapes. Primary research involves interviews with pharmaceutical manufacturers, biotechnology companies, laboratory professionals, regulatory experts, and industry executives to validate findings. Market size estimation is conducted using top-down and bottom-up approaches, while data triangulation and statistical modeling are applied to ensure forecast accuracy, reliability, and comprehensive market insights.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Pyrogen Testing Competitive Landscape & Technology Assessment

Assessed the global pyrogen testing market across LAL tests, recombinant technologies, in vitro pyrogen tests, and rabbit pyrogen tests. Evaluated key companies, product portfolios, and technological advancements.

Helped identify growth opportunities, benchmark competitors, evaluate technology adoption, and assess market positioning across pyrogen testing segments.

Pyrogen Testing Product Benchmarking Study

Benchmarked leading pyrogen testing platforms, endotoxin detection systems, recombinant factor C (rFC) technologies, assay kits, and analytical capabilities across major manufacturers.

Enabled evaluation of technology competitiveness, product differentiation, regulatory readiness, and investment opportunities in advanced pyrogen testing solutions.

Pyrogen Testing End-User Adoption & Commercialization Assessment

Evaluated adoption trends across pharmaceutical and biotechnology companies, medical device manufacturers, CROs, research laboratories, and healthcare institutions.

Supported commercialization planning by identifying high-potential customer segments, adoption drivers, regulatory trends, and market expansion opportunities.

Regulatory Compliance & Validation Strategy Analysis

Analyzed regulatory requirements for pyrogen testing across pharmaceutical and medical device industries, including endotoxin validation and alternative testing methods.

Helped companies improve compliance readiness, reduce approval risks, and optimize product validation strategies for global market access.

Regional Market Opportunity & Expansion Assessment

Assessed pyrogen testing demand across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, highlighting manufacturing and investment trends.

Assisted in identifying high-growth regional markets, investment hotspots, expansion opportunities, and country-level demand potential.

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

The consumables segment led with a 43.1% revenue share in 2025, and is also the fastest-growing segment.

In vitro pyrogen test held the largest revenue share in 2025, and is also the fastest-growing type area.

Some key players operating in the pyrogen testing market include Charles River Laboratories; Ellab A/S; Merck KGaA; GenScript; bioMérieux SA; Lonza; Thermo Fisher Scientific, Inc.; Associates of Cape Cod, Inc.; FUJIFILM Wako Chemicals U.S.A. Corporation (Pyrostar).

Key factors that are driving the market growth include increasing demand for pyrogen testing products in the pharmaceutical and biotechnology industry is a major factor contributing to the growth of the market. Rapidly growing pharmaceutical and biotechnology industries along with the escalating number of new therapeutics launches are expected to boost the demand for pyrogen testing products.

Pharmaceutical and Biotechnology Companies held the largest share in 2025 and is the fastest-growing model.

The global pyrogen testing market size was estimated at USD 1.5 billion in 2025 and is expected to reach USD 1.6 billion in 2026.

The global pyrogen testing market is expected to grow at a compound annual growth rate of 13.1% from 2026 to 2033 to reach USD 3.8 billion by 2033.

North America dominated the pyrogen testing market with a share of 37.0% in 2025. This is attributable to the presence of many large biotechnology and biopharmaceutical companies, rising number of chronic diseases needing developments in drug therapy. Also, North America's highly developed healthcare & research infrastructure and a large focus on new drug development have fueled the regional market growth.

About the Author(s)

Clinical Diagnostics Research Team

Healthcare · Clinical DiagnosticsThis report was authored by the clinical diagnostics research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the clinical diagnostics segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.