- Home

- »

- Advanced Interior Materials

- »

-

Rainscreen Cladding Market Size, Industry Report, 2033GVR Report cover

![Rainscreen Cladding Market Size, Share & Trends Report]()

Rainscreen Cladding Market (2026 - 2033) Size, Share & Trends Analysis Report By Raw Material (Fiber Cement, Terracotta, Metal, Ceramic), By Application (Residential, Official, Commercial, Industrial), By Construction (New Construction, Refurbishment), By Region, And Segment Forecasts

Market Size, 2025

$165.0BMarket Estimate, 2026

$176.5BMarket Forecast, 2033

$289.5BCAGR, 2026–2033

7.3%Rainscreen Cladding Market Summary

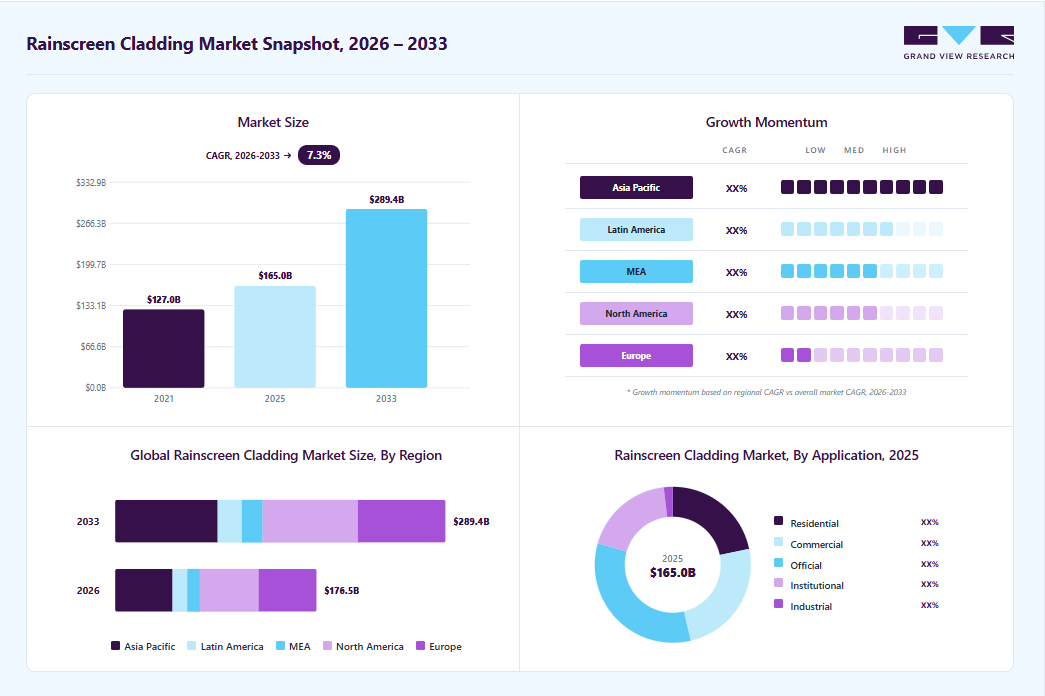

The global rainscreen cladding market size was valued at USD 165.0 billion in 2025 and is projected to grow from USD 176.5 billion in 2026 to USD 289.5 billion by 2033, at a CAGR of 7.3% from 2026 to 2033. The Europe held the largest share of 29.3% of the global market in 2025. The global demand for rainscreen cladding has been increasing steadily in recent years due to a combination of structural, environmental, and architectural trends in the construction industry.

Key Market Trends & Insights

- By raw material: Terracotta segment dominated the market, with a revenue share of 36.1% in 2025.

- By application: Offices construction segment held the largest market share of 33.2% in 2025.

- By construction: New construction segment held the largest revenue share in 2025.

Regional Highlights

- Largest regional market: Europe (29.3% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

Market Size & Forecast

- Market size in 2025: USD 165.0 Billion

- Estimated market size in 2026: USD 176.5 Billion

- Projected market size by 2033: USD 289.5 Billion

- CAGR (2026-2033): 7.3%

Rainscreen cladding systems are exterior wall systems designed with a ventilated cavity that protects the building envelope from rain penetration while improving insulation and energy efficiency. As modern buildings increasingly prioritize durability, sustainability, and design flexibility, rainscreen cladding has emerged as a preferred façade solution across residential, commercial, and institutional infrastructure.The U.S. rainscreen cladding market is primarily driven by increasing construction activities in residential, commercial, official, institutional, and industrial constructions. The rapid development of infrastructures, increasing investments, and the need for expansion are expected to increase construction practices across the country; which is likely to drive the product demand.

")

The market is expected to observe the moderate competition, as the rainscreen claddings need a variety of raw materials and an efficient workforce for production & installation. Industry players face challenges from new entrants for raw material supply and technology used for the process, thus, integrating throughout the chain to sustain in the highly competitive market.

Product quality is an essential element for rainscreen structures, as numerous applications need panels of different raw materials. Manufacturers are focusing on innovative techniques for producing claddings complying with industry standards. Building standards are also followed while designing the rainscreen structures for building applications.

Industry players are focusing on structural framework designs for rainscreen claddings owing to the un-uniform shape of buildings. Requirements for thermal insulation and rainwater drain vent of buildings may hamper the framework design as other components are added to the rainscreen cladding structures. Ready-to-install frames and claddings are produced to save construction time.

Market Concentration & Characteristics

Market growth stage is medium, and pace of the market growth is accelerating. Furthermore, the market is fragmented in nature owing to the presence of a significant number of panel manufacturers and suppliers. A large number of players are present at domestic and international levels owing to the wide availability of raw material in natural and synthetic forms.

Technical innovations in the Rainscreen Claddings have influenced the market on a positive note. For instance, Trespa International B.V. introduced enhanced products using its Electron Beam Curing (EBC) technology. These are suitable for color stability, weather resistance, chemical resistance, and scratch resistance. The same trend is being followed by the industry participants to gain market share in the rainscreen cladding market.

Mergers & acquisitions and joint ventures are undertaken by the players in order to extend their business portfolio and reduce overall costing of the product. For instance, MF Murray Companies is integrated across the value chain from raw material production to installation of the rainscreen cladding structures to sustain in the competitive market.

The market is subject to regulatory scrutiny for instance regulations by approved document B of the Building Regulations (Part B) states fire resistance performance of rainscreen cladding panels. Similarly, Building Regulations 2004 8 (1) (2) states regulations for fitness of material components used in rainscreen cladding.

Substitutes for panels including composite panels, acoustic panels and non-combustible panels are other insulation types. However, rainscreen claddings are preferred owing to its properties of UV protection, weather and aesthetic protection. These panels are preferred by medical, industrial, commercial for weather protection and energy efficiency. Hence, the product substitutes are expected to remain low in forecast period.

A large number of buyers are present in the end use industries including residential, commercial, infrastructure and industrial. Increasing infrastructure spending in emerging economies is expected to increase the levels of end-user concentration.

Raw Material Insights

Terracotta segment dominated the market in 2025 and accounted for the largest revenue share of 36.1% of the global revenue. These materials are widely used for manufacturing panels for rainscreen cladding structures owing to their high durability, low maintenance cost, and fire & weatherproof properties. These panels can be glazed or unglazed and are available in different colors, shapes, and sizes.

Composite materials are gaining popularity in the construction industry owing to their flexibility that allows the claddings to be molded into complex shapes. Copper, zinc, and aluminum composite materials are 100% recyclable and help enhance the aesthetic appearance of buildings with panels of different colors and sizes.

Metals are used for the construction of panels and the framework that is attached to the building wall and supports the entire cladding structure. Stainless steel and aluminum are widely used for framework design owing to their high tensile strength, durability, corrosion resistance, superior flatness, rigidity & stability under changing thermal conditions, and low maintenance.

The demand for fiber cement panels is expected to grow at a steady CAGR during the forecast period owing to its high durability, fire & weatherproof properties, low maintenance cost, and resistance to the growth of fungi, mold, and bacteria. These panels are commercially available in various colors and shapes, which helps improve the aesthetic appeal of the construction structure.

Construction Insights

New construction accounts for the larger share because rainscreen cladding systems are increasingly being integrated into modern building designs from the initial planning stage. Architects and developers prefer incorporating ventilated façade systems in new buildings as they allow better integration with insulation layers, structural supports, and aesthetic façade materials. This approach ensures optimal moisture management, thermal efficiency, and long-term durability of the building envelope. Rapid urbanization, expansion of commercial infrastructure, and the construction of high-rise residential buildings, particularly in developing regions such as Asia-Pacific and parts of the Middle East, are significantly contributing to the higher demand for rainscreen cladding in new construction projects.

Application Insights

Offices construction sector led the market in 2025 and accounted for the largest revenue share of 33.2% of the global revenue. Rapid industrialization and expansion of companies are expected to drive the demand for new construction, which is likely to fuel the product demand in new office buildings and for the renovation of existing buildings.

Commercial construction segment includes buildings for hypermarkets, supermarkets, departmental stores, shopping malls, hospitals & clinics, restaurants & hotels, resorts, and others. These are generally large buildings or clusters of buildings that require rainscreen cladding made from rigid and durable material for protection against extreme weather conditions.

The residential construction segment is classified into single-family houses (standalone homes) and multi-family houses (apartment buildings, clusters, and complexes). The rainscreen cladding structure for these buildings requires fewer components as the structures are small as compared to other segments.

Rainscreen claddings in the institutional and industrial segments provide aesthetic appeal and thermal insulation to the construction including government buildings, factories, warehouses, and schools & other educational institutes. Construction of healthcare facilities and growing medical tourism, particularly in the Asia Pacific region, are expected to increase the product demand.

Regional Insights

The Europe region led the market in 2025 and accounted for the largest revenue share of more than 29.3% of the global revenue. This is attributed to the region’s strong emphasis on sustainable construction and energy-efficient buildings. Governments across Europe are implementing strict building performance standards that require improved insulation, moisture control, and reduced energy consumption in both residential and commercial structures. Rainscreen cladding systems help achieve these goals by creating a ventilated façade that improves thermal efficiency while protecting buildings from rain penetration and temperature fluctuations. Additionally, many European cities have a large stock of aging buildings that are undergoing renovation and façade upgrades to meet modern environmental and safety standards, further driving the adoption of rainscreen cladding solutions.

Germany Rainscreen Cladding Market Trends

In Germany, the demand for rainscreen cladding is driven by the country’s focus on high-quality engineering standards and advanced building technologies. The German construction sector prioritizes durable, long-lasting materials that can withstand harsh weather conditions while maintaining energy performance. Rainscreen cladding systems provide effective moisture management and structural protection, which aligns well with Germany’s building practices. Furthermore, the country has been investing heavily in upgrading building envelopes to reduce carbon emissions from the built environment, encouraging the use of high-performance façade systems such as ventilated rainscreen cladding.

North America Rainscreen Cladding Market Trends

In North America, the increasing demand for rainscreen cladding is largely influenced by the growing focus on resilient building envelopes that can withstand diverse and extreme weather conditions. Buildings in the region are frequently exposed to heavy rainfall, snow, and temperature fluctuations, which can cause long-term structural damage if not properly managed. Rainscreen cladding systems help protect buildings by allowing water to drain and air to circulate behind the façade, preventing moisture buildup and improving overall building durability.

The demand for rainscreen cladding in the U.S. is rising due to the increasing adoption of modern architectural façade designs and high-performance building materials in commercial and institutional construction. Developers and architects are seeking exterior systems that not only enhance building protection but also provide flexibility in design and material selection. Rainscreen cladding allows for the use of various façade materials while improving building performance, making it an attractive solution for office buildings, educational institutions, healthcare facilities, and high-end residential developments across the country.

Asia Pacific Rainscreen Cladding Market Trends

Across the Asia Pacific region, the demand for rainscreen cladding is growing due to expanding construction activities and increasing investments in urban infrastructure. Many countries in the region are witnessing rapid population growth and urban migration, leading to the development of new residential housing, commercial buildings, and industrial facilities. Developers are adopting rainscreen cladding systems to improve building performance, reduce maintenance requirements, and enhance the aesthetic appeal of modern structures, making them a popular choice in large construction projects throughout the region.

China has a high growth in rainscreen cladding demand due to rapid urbanization and large-scale infrastructure development. Major cities across the country continue to see the construction of high-rise residential towers, commercial complexes, and public infrastructure, all of which require advanced façade systems for durability and weather protection. Rainscreen cladding is increasingly used in these projects because it provides improved protection against moisture and environmental stress while supporting modern architectural designs commonly used in large urban developments.

Key Rainscreen Cladding Company Insights

The market is highly competitive owing to the presence of numerous local and global players. Variations in raw material prices and strategies of new entrants are the challenges for existing players in the market. Continuous R&D and innovative techniques for the process are the factors to sustain in the competitive environment. Key players in the industry are focusing on mergers, acquisitions, and joint ventures to sustain the competition and reduce the overall cost of rainscreen cladding. Structural designing and installation services are offered by the players to fulfill the demand of the consumers that need innovative rainscreen cladding designs for buildings.

Competition in the market is therefore driven less by price and more by factors such as product certification, fire safety compliance, sustainability credentials, and the ability to provide complete façade systems that simplify installation for developers and architects. Additionally, companies are strengthening their market positions through strategic partnerships, acquisitions, and regional manufacturing expansion to improve supply chains and better serve high-growth construction markets across Europe, North America, and Asia-Pacific.

-

In April 2022, Kingspan Insulation plc announced to expand its business at 200 Kingspan Way in Frederick County, Kingspan Insulation LLC, a division of the Kingspan Group, a manufacturer of advanced insulation and cutting-edge building solutions, will invest USD 27.0 million, according to Governor Glenn Youngkin. To further increase its presence on the East Coast, the company will increase production capacity by constructing a new facility to produce the highly sought-after, extremely energy-efficient OPTIM-R® vacuum insulated panels.

-

In September 2021, Kingspan Group announced the acquisition of Minnesota Diversified Products, Inc., a US-based company. The acquisition broadened Kingspan's clientele in the US and its core building insulation business in a market that is anticipated to experience rapid expansion.

Key Rainscreen Cladding Companies:

The following key companies have been profiled for this study on the rainscreen cladding market.

- Kingspan Insulation plc

- Carea Ltd.

- M.F. Murray Companies, Inc.

- Celotex Ltd.

- CGL Facades Co.

- Rockwool International A/S

- Eco Earth Solutions Pvt. Ltd.

- FunderMax

- Everest Industries Ltd.

- OmniMax International, Inc.

- Trespa International B.V.

- Middle East Insulation LLC

- Euro Panels Overseas N.V.

- Centria International

- Dow Building Solutions

Rainscreen Cladding Market Report Scope

Report Attribute

Details

Market size in 2025

USD 165.0 billion

Estimated Market size in 2026

USD 176.5 billion

Projected Market size by 2033

USD 289.5 billion

Growth Rate

CAGR of 7.3% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Volume in million square meters and revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Raw material, application, construction, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S., Canada, Mexico, Germany, UK, France, Russia, Spain, Italy, Austria, Poland, Belgium, Denmark, Turkey, Switzerland, China, India, Japan, South Korea, Indonesia, Singapore, Malaysia, Vietnam, Thailand, Brazil, Argentina, Colombia, Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman, Egypt, South Africa

Key companies profiled

Kingspan Insulation plc, Carea Ltd., M.F. Murray Companies, Inc., Celotex Ltd., CGL Facades Co., Rockwool International A/S, Eco Earth Solutions Pvt. Ltd., FunderMax, Everest Industries Ltd., OmniMax International, Inc., Trespa International B.V., Middle East Insulation LLC, Euro Panels Overseas N.V., Centria International, Dow Building Solutions

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Rainscreen Cladding Market Report Segmentation

This report forecasts revenue and volume growth at country levels and provides an analysis on the industry trends in each of the sub-segments from 2018 to 2030. For the purpose of this study, Grand View Research has segmented the global rainscreen cladding market based on raw material, application, construction, and region.

-

Raw Material Outlook (Volume, Million Square. Meters, Revenue, USD Billion; 2021 - 2033)

-

Fiber Cement

-

Composite Material

-

Metal

-

High Pressure Laminates

-

Terracotta

-

Ceramic

-

Others

-

-

Application Outlook (Volume, Million Square Meters, Revenue, USD Billion; 2021 - 2033)

-

Residential

-

Commercial

-

Official

-

Institutional

-

Industrial

-

-

Construction Outlook (Volume, Million Square Meters, Revenue, USD Billion; 2021 - 2033)

-

New Construction

-

Refurbishment

-

-

Regional Outlook (Volume, Million Square Meters, Revenue, USD Billion; 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Russia

-

Austria

-

Poland

-

Belgium

-

Denmark

-

Turkey

-

Switzerland

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Malaysia

-

Indonesia

-

Thailand

-

Singapore

-

Vietnam

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

Qatar

-

Kuwait

-

Bahrain

-

Oman

-

Egypt

-

South Africa

-

-

Latin America

-

Brazil

-

Argentina

-

Mexico

-

Colombia

-

-

Frequently Asked Questions About This Report

New construction held the largest market share in 2025.

The global rainscreen cladding market size was valued at USD 165.0 billion in 2025 and is estimated at USD 176.5 billion for 2026.

The global rainscreen cladding market is expected to grow at a CAGR of 7.3% from 2026 to 2033, reaching USD 289.5 billion.

The key factors that are driving the global rainscreen cladding market include, the rainscreen cladding improves the esthetics of the building while protecting it from heavy rainfall and high air pressure.

The terracotta segment led with a 36.1% revenue share in 2025, while metal is the fastest-growing raw material segment.

The offices construction sector held the largest revenue share of 33.2% in 2025.

Key players include Kingspan Insulation plc, Carea Ltd., M.F. Murray Companies, Inc., Celotex Ltd., CGL Facades Co., Rockwool International A/S, Eco Earth Solutions Pvt. Ltd., FunderMax, Everest Industries Ltd., OmniMax International, Inc., Trespa International B.V., Middle East Insulation LLC, Euro Panels Overseas N.V., Centria International, Dow Building Solutions

Europe dominated with a 29.3% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.