- Home

- »

- Communications Infrastructure

- »

-

Satellite Communication Market Size, Growth Report, 2026-2033GVR Report cover

![Satellite Communication Market (2026 - 2033)Report]()

Satellite Communication Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Equipment, Service), By Satellite Constellations, By Frequency Band, By Application, By Vertical, By Region, And Segment Forecasts

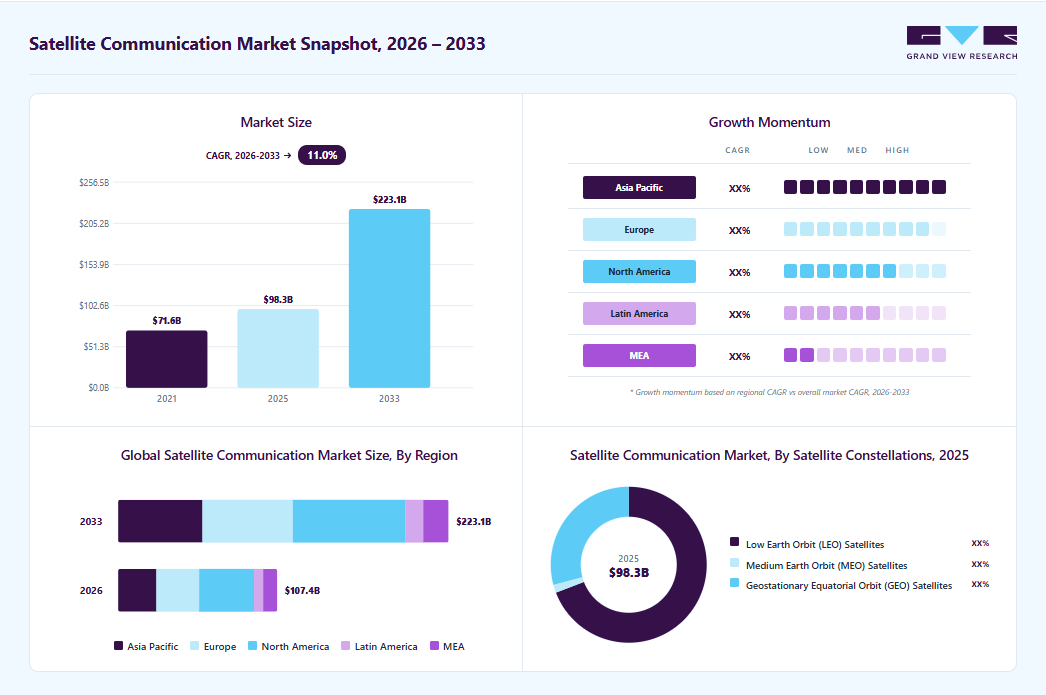

Market Size, 2025

$98.3BMarket Estimate, 2026

$107.4BMarket Forecast, 2033

$223.1BCAGR, 2026–2033

11.0%Satellite Communication Market Summary

The global satellite communication market size was valued at USD 98.3 billion in 2025 and is projected to grow from USD 107.4 billion in 2026 to USD 223.1 billion by 2033, growing at a CAGR of 11.0% from 2026 to 2033. North America dominated the global market with the largest revenue share of 34.5% in 2025. The promising growth prospects of the market can be attributed to the growing demand for High-throughput Satellite (HTS) systems, which provide significantly increased capacity and data speeds compared to traditional systems.

Key Market Trends & Insights

- By component: Services segment dominated the market, with a revenue share of 58.6% in 2025.

- By satellite constellations: LEO segment held the largest market share of 69.2% in 2025.

- By frequency band: Ku-band deployment segment held the largest revenue share in 2025.

- By application: Broadcasting segment held the largest revenue share in 2025.

- By vertical: Media & broadcasting segment accounted for the largest revenue share in 2025.

Regional Highlights

- Largest regional market: North America (34.5% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 98.3 Billion

- Estimated market size in 2026: USD 107.4 Billion

- Projected market size by 2033: USD 223.1 Billion

- CAGR (2026-2033): 11.0%

HTS systems enable faster and more efficient data transmission, making them ideal for bandwidth-intensive applications such as video streaming, remote sensing, and Internet of Things (IoT) connectivity. New frequency bands, such as high-frequency and very high-frequency bands, are also rapidly expanding the available satcom spectrum. These bands offer improved bandwidth and increased capacity, enabling higher data rates and supporting bandwidth-intensive applications. Several solution providers across the globe are focusing on developing solutions that offer better connectivity for a myriad of use cases. For instance, in June 2023, Get SAT Ltd, a provider of miniaturized Satcom terminals, launched its latest product line, MoComm.")

The line of multi-orbit communication solutions features the innovative multi-orbit communication capability. This feature enables smooth and efficient switching between satellite constellations, ensuring uninterrupted connectivity. MoComm operates seamlessly in both Ku and Ka bands. The Ka-band functionality empowers users to seamlessly transfer data traffic between the O3b Medium Earth Orbit (MEO) constellation and any Geostationary Orbit (GEO) constellation. The Ku-band has received certification for compatibility with Low Earth Orbit (LEO) and any GEO constellation, further expanding its versatility and applicability.

Increasing use of Satcom in government and defense sectors is contributing to the growing demand for HTS capacity. Government agencies are increasingly relying on sensor data and ISR platforms to transform their operational environments. These platforms facilitate the sharing of real-time HD video and other valuable information obtained from Remotely Piloted Air Systems (RPAS) or Unmanned Aerial Vehicles (UAVs). In response to this growing demand, leading industry players such as Viasat, Inc., and SES S.A. are making significant investments aimed at pioneering novel solutions tailored to various government and defense applications.

The growing deployment of satellite constellations dedicated to IoT connectivity is also contributing to industry growth. These constellations consist of several small satellites working together to provide global coverage for IoT devices, LEO satellites, enabling seamless communication and data exchange across vast geographic areas. This trend is driven by the applications of IoT technology in areas such as agriculture, logistics, environmental monitoring, and asset tracking, where uninterrupted connectivity is essential.

Another emerging trend is the development of LEO satellite networks specifically designed for IoT applications. LEO satellites offer advantages such as lower latency, improved signal strength, and higher data throughput, making them well-suited for IoT data transmission. These networks leverage advanced technologies such as narrowband and low-power communication protocols to optimize IoT device connectivity, ensuring efficient utilization of satellite resources.

Furthermore, the satellite communication industry is witnessing the adoption of advanced technologies such as Artificial Intelligence (AI), which are driving the emergence of Intelligent Transport Systems (ITS). These systems enable real-time vehicle tracking, facilitating the swift exchange of information for both users and freight operators. SATCOM integration in transportation ensures continuous and seamless data transmission between vehicles and transport hubs, reducing the reliance on terrestrial networks.

Market Dynamics

The satellite communication market is witnessing steady growth driven by rising demand for global connectivity, increasing deployment of satellite-based broadband services, and growing utilization of satellite networks across defense, maritime, aviation, and remote communication applications. The market is benefiting from advancements in satellite technology, including high-throughput satellites (HTS), low Earth orbit (LEO) constellations, and improved data transmission capabilities. However, high infrastructure costs and spectrum-related challenges continue to restrain market growth. In addition, emerging opportunities for direct-to-device connectivity and expanding space-based internet services are expected to contribute to the growth of the market. Continued investments in satellite infrastructure and next-generation communication technologies are expected to support long-term market expansion.

The increasing need for reliable internet access in remote, rural, and underserved regions is a major driver of the satellite communication market. Many areas across the world continue to face limitations in terrestrial communication infrastructure, creating demand for satellite-based connectivity solutions. Satellite communication enables internet access, voice services, and data transmission in locations where fiber-optic and cellular networks are unavailable or economically unfeasible. Governments, telecom operators, and private companies are increasingly leveraging satellite networks to bridge the digital divide and improve connectivity. The deployment of high-throughput satellites and low Earth orbit satellite constellations is enhancing coverage, bandwidth, and service quality. Rising demand for remote education, telemedicine, digital banking, and online services is further accelerating satellite communication adoption. This growing requirement for universal connectivity continues to support market growth.

Increasing digital transformation initiatives across developing economies are further strengthening demand for satellite-enabled broadband services. Governments are investing in programs aimed at expanding internet access to remote communities and improving digital inclusion. Satellite communication providers are launching advanced services that deliver higher speeds and lower latency compared to traditional satellite systems. Businesses operating in remote regions also rely on satellite connectivity to support operational efficiency and communication needs. The growing importance of internet accessibility for economic development is creating sustained demand for satellite infrastructure. These factors are expected to contribute significantly to market growth during the forecast period.

High capital investment requirements is one of the major restraints affecting the satellite communication market. Developing, launching, and maintaining satellite systems involves substantial expenditures related to satellite manufacturing, launch services, ground infrastructure, and operational management. The significant upfront investment required can create barriers for new market entrants and limit adoption among smaller service providers. Continuous technological upgrades and satellite replacement cycles further increase financial requirements. In addition, the complexity of satellite deployment and network management contributes to elevated operational costs. These financial challenges affect the pace of market expansion, particularly in cost-sensitive regions. High infrastructure costs continue to influence investment decisions across the industry.

The economic viability of satellite projects often depends on long-term utilization rates and revenue generation capabilities. Service providers must carefully manage capital expenditures while maintaining network performance and competitiveness. Delays in satellite deployment or operational issues can significantly impact return on investment. The industry also faces rising competition from terrestrial communication technologies in certain markets. Cost optimization remains a critical focus area for satellite operators seeking to improve profitability. Infrastructure-related challenges are expected to remain a key market restraint.

The development of direct-to-device satellite communication services presents a significant growth opportunity for the market. Emerging technologies are enabling satellites to connect directly with standard smartphones and consumer devices without requiring specialized satellite terminals. This capability has the potential to expand communication access in remote regions, improve emergency connectivity, and enhance network resilience. Telecommunications companies and satellite operators are increasingly collaborating to develop integrated satellite-cellular communication ecosystems. Direct-to-device services support messaging, voice communication, and data connectivity across areas lacking terrestrial network coverage. Growing interest in ubiquitous connectivity is accelerating investments in this technology. This emerging market segment is expected to create substantial growth opportunities in the coming years.

Analyst Perspective

The satellite communication market is driven by rising demand for global connectivity, advancements in satellite technology, and growing investments in next-generation satellite networks. Companies are focusing on expanding coverage, improving network efficiency, and enhancing communication capabilities across commercial and government applications. Increasing adoption across aviation, maritime, defense, and remote enterprise operations continue to strengthen market demand.

Component Insights

Based on component, the services segment led the market with the largest revenue share of 58.6% in 2025. The segment growth can be attributed to the global expansion of the media and entertainment industries, coupled with the increasing demand for satellite television in emerging nations. Efforts to enable seamless data transmission to end-user locations also favor the increased demand for Satcom services across the globe. However, the high upfront costs associated with satellite acquisition often make it financially challenging for many firms to invest in the technology outright. As a result, an increasing number of companies are opting for satellite services through leasing arrangements. Domestic Direct-to-Home (DTH) operators, for instance, are typically limited to using satellites ordered by their respective space agencies or leasing capacity from foreign satellites. Technological advancements play a crucial role in reducing manufacturing costs, thereby lowering lease expenditure and driving revenue market growth.

The equipment segment is expected to grow at the fastest CAGR during the forecast period, owing to the growing need for uninterrupted communication across industries and the increasing use of connected and autonomous vehicles. Satcom equipment ensures the smooth functioning of diverse applications, such as telecommunications, navigation, weather monitoring, and surveillance systems, by enabling effective communication with satellites orbiting the Earth. The introduction of LEO satellites and satellite constellations for telecommunication purposes is also expected to drive the equipment segment growth.

Satellite Constellations Insights

Based on satellite constellations, the low earth orbit (LEO) segment led the market with the largest revenue share of 69.2% in 2025. The increasing demand for global internet coverage, particularly in underserved or remote areas where traditional broadband infrastructure is either too costly or challenging to deploy, is driving the growth of low-earth-orbit satellites for communication. LEO satellites, positioned closer to Earth than geostationary satellites, enable faster data transmission speeds and reduced latency, making them ideal for high-speed internet.

The geostationary equatorial orbit (GEO) satellites segment is expected to grow at a significant CAGR during the forecast period. Geostationary equatorial orbit satellites are ideal for broadcasting, as they ensure continuous, reliable service, which is critical for television and radio networks, broadcasts, and direct-to-home (DTH) services. With no need for complex tracking systems, stationary GEO satellites provide stable, high-quality signals to fixed-ground antennas, supporting media distribution to vast audiences with minimal disruption.

Frequency Band Insights

Based on frequency band, the Ku-band segment led the market with the largest revenue share of 25.4% in 2025. The Ku-band frequency segment covers frequencies ranging from 10.7 to 14.5 GHz. The application of Ku-band frequencies in fixed satellite television data services drives market growth. The Ku-band is ideal for delivering high-quality broadcast signals, making it an ideal choice for fixed satellite television services. This frequency band allows for strong, stable connections that can transmit data over long distances with minimal interference, providing reliable television broadcasts.

The Ka-band is projected to grow at the fastest CAGR over the forecast period. The Ka-band frequency segment covers frequencies ranging from 17.3 to 30 GHz. The capability of the Ka-band to support high data rates drives the growth of the segment in the market. The higher frequencies in the Ka-band allow for greater bandwidth, which translates to faster internet speeds and enhanced data throughput compared to lower-frequency bands such as Ku and C-band.

Application Insights

Based on application, the broadcasting segment led the market with the largest revenue share of 22.8% in 2025. This segment growth can be attributed to the growing demand for satellite communications in pay-TV and radio applications. DTH providers use satcom to deliver services to customers and ensure seamless connectivity, even in remote and inaccessible areas. Growing consumer expectations for high-quality audio and video content have driven significant advancements in Satcom equipment.

Airtime is projected to grow at the fastest CAGR over the forecast period, owing to the rising demand for reliable and affordable communication services for flights and aircraft. Satcom solutions offer seamless connectivity and high-speed internet access onboard aircraft, catering to the needs of both the crew and business applications. The growing use of satcom for aircraft navigation and remote troubleshooting is also expected to contribute to the segment's promising growth prospects.

Vertical Insights

Based on vertical, the BFSI segment led the market with the largest revenue share of 16.3% in 2025. The media & broadcasting industry is one of the leading consumers of satellite communication technology. Media and broadcasting businesses leverage the technology to transmit live news, satellite television and radio, sports events, concerts, and various other programs to their audience. Moreover, satellites are used to broadcast video channels that can be received by both broadcast networks and cable operators, benefitting consumers globally.

The government & defense segment is projected to grow at the fastest CAGR over the forecast period. Increasing emphasis on secure and resilient satcom solutions to meet the evolving needs of government agencies and defense organizations is a key factor contributing to the growth of the segment. This includes the adoption of advanced encryption techniques, anti-jamming capabilities, and robust cybersecurity measures to safeguard sensitive data and ensure uninterrupted communication in critical situations.

Regional Insights

North America dominated the global satellite communication market with the largest revenue share of 34.5% in 2025. Growing demand for satellite broadband services, especially for providing reliable connectivity in remote, hard-to-reach, and underserved regions of North America, is likely to drive regional growth over the forecast period. The region is also home to key industry players such as Viasat, Inc., Intelsat, Telesat, and Harris Technologies, Inc. Their strong focus on innovations and investments in research and development, advanced technologies, and strategic partnerships is fueling the expansion of the industry in the region.

U.S. Satellite Communication Market Trends

The satellite communication market in the U.S. held the largest share in the North America region in 2025, supported by its advanced space infrastructure, strong presence of leading satellite operators, and continuous investments in next-generation satellite technologies. The market is characterized by large-scale deployment of LEO and hybrid satellite constellations aimed at enhancing broadband coverage, network resilience, and latency performance across commercial and government applications. Strategic partnerships between satellite service providers, technology companies, and public institutions continue to play a critical role in market expansion. Initiatives focused on student connectivity, distance learning, and rural broadband access, powered by satellite internet, are accelerating adoption and strengthening digital inclusion efforts across underserved regions. In parallel, rising demand for secure communications across defense, emergency response, aviation, and maritime sectors, along with sustained government funding for space and defense programs, reinforces the U.S. position as a global leader in the market.

Europe Satellite Communication Market Trends

The satellite communication market in Europe emerged as a high-potential region in 2025, supported by strong institutional backing, defense modernization programs, and growing demand for secure and resilient connectivity across civil, commercial, and government applications. A shift toward technological self-reliance and long-term sustainability increasingly characterizes the regional market. European governments and space agencies are advancing sovereign satellite initiatives, multi-orbit architectures, and public-private partnerships to strengthen strategic autonomy and reduce reliance on non-European satellite operators. Rising investments in low Earth orbit (LEO) and hybrid GEO-LEO constellations, along with policy-driven support for secure communications and broadband coverage in remote areas, continue to enhance the region’s SATCOM ecosystem.

The UK satellite communication market is expected to grow at a robust pace over the forecast period, driven by rising investments in research and development, defense-oriented satellite programs, and commercial broadband initiatives. Active collaboration with international partners and private space companies is accelerating innovation across satellite manufacturing, ground infrastructure, and next-generation payload technologies. Government-backed programs aimed at strengthening national space capabilities, combined with increasing demand for maritime, aviation, and secure government communications, are reinforcing the UK’s position as a key European SATCOM hub.

The satellite communication market in Germany is anticipated to witness steady and strategic growth, supported by the country’s strong industrial base, advanced engineering capabilities, and emphasis on secure digital infrastructure. Germany is prioritizing the development of sovereign and dual-use satellite systems to support defense communications, disaster management, and critical infrastructure connectivity. Increased funding for space research, coupled with close cooperation between government agencies, aerospace companies, and research institutions, is driving innovation in satellite payloads, ground stations, and data processing technologies. Growing demand for high-reliability SATCOM solutions across government, automotive, industrial IoT, and mobility applications further strengthens Germany’s role as a central contributor to Europe’s market.

Asia Pacific Satellite Communication Market Trends

The satellite communication market in the Asia Pacific accounted for 23.9% share of the overall market in 2025. This can be attributed to the relentless pursuit of innovation, research and development, and strategic initiatives by prominent market players aimed at enhancing their market presence. Growing reliance on satcom-dependent services in sectors such as telecommunications, media and broadcasting, agriculture, and energy and utility is also a notable driver of market growth. Moreover, the region is home to numerous organizations dedicated to advancing satellite communications.

India satellite communication market is expected to grow rapidly over the forecast period, driven by rising demand for satellite-based broadband and connectivity solutions across rural, remote, and underserved regions. Policy reforms encouraging private sector participation, along with growing collaboration between domestic players and national space agencies, are accelerating the deployment of new satellite systems and ground infrastructure. Increasing use of SATCOM for disaster management, maritime connectivity, defense communications, and enterprise networking further supports market growth, positioning India as a fast-emerging SATCOM hub in Asia.

The satellite communication market in China held a substantial market share in 2025 and continues to expand at a strong pace. The market is characterized by large-scale satellite constellation rollouts, rapid adoption of advanced payload and launch technologies, and a high level of state-backed investment. A strong emphasis on military, defense, and secure government communications, combined with expanding commercial applications such as broadband, navigation, and remote sensing, reinforces China’s strategic importance in the global satellite communication landscape.

Japan satellite communication market is expected to witness steady growth, supported by the country’s focus on technological precision, resilience, and space-based disaster preparedness. Japan is actively investing in next-generation satellite systems to strengthen national security, emergency response capabilities, and high-reliability communications for aviation and maritime sectors. Close coordination between government bodies, research institutions, and leading technology companies is driving innovation in satellite payloads, ground systems, and data services, establishing Japan as a technologically advanced and reliable SATCOM market in the Asia-Pacific region.

Key Satellite Communication Company Insights

Some of the key companies in the market include Viasat, Inc., SES S.A., L3 Harris Technologies, Inc., EchoStar Corporation, and SKY Perfect JSAT Group. Organizations are focusing on increasing their customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies.

-

Viasat, Inc. is engaged in providing communications technologies and services. The company offers end-to-end platforms for ground infrastructure, Ka-band satellites, and user terminals to provide high-speed, high-quality broadband solutions to enterprises, governments, and consumers across the globe.

-

Intelsat S.A. offers satcom services for transmitting data, video, and voice signals. The company provides these services to various media companies, wireless & fixed telecom operators, data networking service providers, ISPs, and multinational corporations.

Key Satellite Communication Companies:

The following key companies have been profiled for this study on the satellite communication market.

-

Viasat, Inc.

-

SES S.A

-

Intelsat S.A.

-

Telesat Corporation

-

EchoStar Corporation

-

L3Harris Technologies, Inc.

-

Thuraya Telecommunications Company (Yashat)

-

SKY Perfect JSAT Holdings Inc.

-

Gilat Satellite Networks Ltd.

-

Cobham Limited

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Viasat, Inc., SES S.A, L3 Harris Technologies, Inc., EchoStar Corporation)

- These players are focusing on adopting strategic initiatives such as service launches, geographical expansions, collaborations, and partnerships to gain their foothold in the market.

- These players are engaging in R&D initiatives and are conducting intensive research to improve their satellite communication offerings. These companies are providing high-speed and high-quality broadband solutions to enterprises, government and consumers across the globe.

- Despite their prominent brand names and significant market shares; these players are facing intense competition in the market. Since the market has fragmented, holding a large share is difficult in a competitive environment and requires companies to improve their offerings and prices constantly.

Emerging Players (Intelsat S.A., Telesat Corporation, Kuiper Systems LLC (Amazon Kuiper))

- These players are adopting various strategic initiatives to gain a larger market share. For instance, these companies are undertaking geographical expansions to increase their global customer base and achieve larger profits.

- These players are offering additional services to increase customer satisfaction. Market players are also pursuing strategic partnerships and collaborations as part of their efforts to expand their offerings and enhance their production processes.

- These players have successfully captured market share in their respective regions but failed to capture the global market share. The players are engaging in strategic initiatives to gain a more extensive global customer base.

Recent Developments

-

In May 2025, Intelsat expanded its partnership with AXESS Networks to deliver seamless satellite connectivity across the Americas. The collaboration integrates Intelsat and Hispasat satellite assets, enabling multi-satellite services with enhanced coverage, reliability, and service quality for enterprise and mobility customers.

-

In April 2025, SpinLaunch, a space technology company, announced a USD 12 million strategic investment from Kongsberg Defence & Aerospace to support the development and commercialization of its revolutionary Low-Earth Orbit (LEO) satellite broadband constellation, Meridian Space. This partnership highlights SpinLaunch’s commitment to delivering affordable and sustainable satellite communication services globally.

-

In March 2025, Orange Africa and the Middle East partnered with Eutelsat to accelerate satellite internet deployment across Africa and the Middle East. Using the EUTELSAT KONNECT satellite, the initiative targets rural and underserved regions with high-speed, secure broadband connectivity for consumers and enterprises.

-

In January 2025, ReOrbit signed a memorandum of understanding with Ananth Technologies to explore the design and development of GEO communication satellites. The collaboration focuses on integrating software-enabled satellite platforms with advanced manufacturing and AIT capabilities to strengthen the secure communications infrastructure.

-

In December 2024, Parsons and Globalstar announced an exclusive partnership and successfully demonstrated a software-defined satellite communication solution using Globalstar’s LEO constellation. The milestone supports resilient, mission-critical communications for public, government, and defense sectors, particularly in RF-congested and operationally complex environments.

-

In April 2023, SES S.A. and Corporación Nacional de Telecomunicaciones (CNT), a telecommunications provider, partnered to support Ecuador's digital inclusion efforts in the Galapagos Islands. They have announced a significant expansion agreement for medium Earth orbit satellite capacity. This expansion aims to provide enhanced broadband connectivity and 3G/4G/5G mobile services to businesses, residents, and tourists across the isolated Galapagos Islands in the eastern Pacific Ocean, contributing to the development and connectivity of the region.

Satellite Communication Market Report Scope

Report Attribute

Details

Market size in 2025

USD 98.3 billion

Estimated Market size in 2026

USD 107.4 billion

Projected Market size by 2033

USD 223.1 billion

Growth rate

CAGR of 11.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Component, satellite constellations, frequency band, application, vertical, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; China; Japan; India; Australia; South Korea; Brazil; Mexico; KSA; UAE; South Africa

Key companies profiled

Viasat, Inc.; SES S.A; Intelsat S.A.; Telesat Corporation; EchoStar Corporation; L3Harris Technologies, Inc.; Thuraya Telecommunications Company; SKY Perfect JSAT Holdings Inc.; Gilat Satellite Networks Ltd.; Cobham Limited

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Satellite Communication Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global satellite communication market report based on component, satellite constellations, frequency band, application, vertical, and region:

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Equipment

-

Satcom Transmitter/Transponder

-

Satcom Antenna

-

Satcom Transceiver

-

Satcom Receiver

-

Satcom Modem/Router

-

Others (Block-up converters, controllers)

-

-

Services

-

-

Satellite Constellations Outlook (Revenue, USD Billion, 2021 - 2033)

-

Low Earth Orbit (LEO) Satellites

-

Medium Earth Orbit (MEO) Satellites

-

Geostationary Equatorial Orbit (GEO) Satellites

-

-

Frequency Band Outlook (Revenue, USD Billion, 2021 - 2033)

-

L-band

-

S-band

-

C-band

-

X-band

-

Ku-band

-

Ka-band

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Asset Tracking/Monitoring

-

Airtime

-

M2M

-

Voice

-

Data

-

-

Drones Connectivity

-

Data Backup and Recovery

-

Navigation and Monitoring

-

Tele-medicine

-

Broadcasting

-

Others

-

-

Vertical Outlook (Revenue, USD Billion, 2021 - 2033)

-

Energy & Utility

-

Government & Defense

-

Government (Civil Uses)

-

Emergency Responders

-

Defense

-

-

Transport & Cargo

-

Fleet Management

-

Rail services

-

-

Maritime

-

Mining and Oil & Gas

-

Oil & Gas

-

Mining

-

-

Agriculture

-

Communication Companies

-

Corporates/Enterprises

-

Media & Broadcasting

-

Events

-

Aviation

-

Environmental & Monitoring

-

Forestry

-

End User - Consumer

-

Healthcare

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Research Methodology

The satellite communication market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each satellite communication segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Component

Revenue capture definition

Equipment

This segment captures revenue generated from hardware used for satellite communication transmission, reception, and network connectivity. It includes SATCOM Transmitter/Transponder, SATCOM Antenna, SATCOM Transceiver, SATCOM Receiver, SATCOM Modem/Router, and Others.

- SATCOM Transmitter/Transponder: A SATCOM transponder is a wireless monitoring, communication, or control device that identifies and automatically responds to an incoming signal.

- SATCOM Transceiver: A transceiver is a device which can be used for both transmission and receiving purposes.

- SATCOM Antenna: The antenna is the most visible part of the satellite communication system. It transmits and receives the modulated carrier signal at the radio frequency (RF) portion of the electromagnetic spectrum.

- SATCOM Receiver: A satellite receiver is a device that wirelessly receives and decodes radio signals.

- SATCOM Modem/Router: A satellite modem is a modem used to establish data transfers using a communications satellite as a relay.

- Others: It includes other equipment used in satellite communication such as block-up converters and controllers

Services

This segment captures revenue generated from satellite communication services provided to commercial, government, and consumer users. It includes connectivity services, managed services, bandwidth leasing, network operations, and communication support services.

Segment - Satellite Constellations

Revenue capture definition

Low Earth Orbit (LEO) Satellites

LEO satellites orbit at altitudes ranging from 160 km to 2,000 km above the Earth's surface. These satellites are positioned much closer to Earth than other orbital types, allowing them to provide low-latency, high-speed communication services.

Medium Earth Orbit (MEO) Satellites

These satellites are located between 2,000 and 36,000 km above the Earth, placing them in the "Goldilocks zone" for optimal latency, transmission speeds, and coverage.

Geostationary Equatorial Orbit (GEO)

Satellites

These satellites orbit approximately 36,000 km above the Earth, where their orbital speed matches the Earth’s rotation. This positioning allows them to provide the broadest coverage area, but it comes with the trade-offs of higher latency and weaker signal strength.

Segment - Frequency Band

Revenue capture definition

L-band

L-band refers to the frequencies operating in the range of 1 - 2 GHz. These frequencies are commonly used for mobile satellite communication and navigation systems. L-band signals are known for their reliability in varying weather conditions, making them ideal for applications, such as Global Positioning System (GPS), satellite radio broadcasts, and satellite phone services.

S-band

The S-band refers to the frequencies operating in the range of 2 to 4 GHz and is used for satellite communications due to its balance between available bandwidth and atmospheric penetration. This makes the S-band ideal for applications such as weather satellites and certain mobile communication systems.

C-band

C-band refers to the frequencies operating in the range of 4 - 8 GHz. C-band is a favored band for satellite communications, particularly for offering certain internet services, owing to the balance C-band frequencies can strike between signal quality and vulnerability to rain fade, a phenomenon whereby signal degradation occurs during rainy conditions. Conventionally, C-band has been used for voice and data communications and backhauling.

X-band

X-band refers to the frequencies operating in the range of 8 - 12 GHz. X-band is used for various satellite internet applications, including military, radar, and certain satellite broadcasting services. Being less susceptible to atmospheric interference compared to lower-frequency bands, such as the C-band and K-band, the X-band is used for facilitating high-quality data transmission.

Ku-band

The Ku-band refers to the frequencies operating in the range of 12 to 18 gigahertz (GHz) in the electromagnetic spectrum. It is used for a variety of applications, including broadband internet services, video distribution, Direct-to-home (DTH) television broadcasting, and corporate network communications, among others.

Ka-band

The Ka-band refers to the frequencies operating in the range of 26 to 40 GHz. It is largely used for enabling high-speed satellite internet. Offering a significantly larger bandwidth, the Ka-band supports next-generation satellite communication applications and is essential for delivering fast, high-capacity internet services.

Segment - Application

Revenue capture definition

Asset Tracking/Monitoring

This includes the satellite communication used for tracking & monitoring assets across various industry verticals that include oil & gas, mining, and energy & utility industry, among others.

Airtime

The airtime segment is further segmented into M2M, voice, and data.

- M2M: It includes the use of satellites for applications wherein one or more machines interact with each other. These applications are also based on the Internet of Things (IoT) technology, wherein different devices and machines interact with each other to exchange data.

- Voice: It includes the use of satellites for voice communications across a variety of industries including marine, government, defense, aviation, among others.

- Data: It includes the use of satellite for data communication purposes that include broadband services used in industries including aeronautical, maritime, government & defense, as well as end-user/consumer, among others.

Drones Connectivity

This segment includes the satellite communications used primarily in the government & defense industry for operating drones or UAVs.

Data Backup and Recovery

This segment includes the usage of satellite communications by corporates/organizations for data backup & storage applications.

Navigation and Monitoring

This segment consists of the satellite communications used for the purpose of providing navigation services such as GPS services used in automobiles, ships, and marine, among others. Further, it also includes satellites used for earth observation services as well as monitoring services in the agriculture sector.

Tele-medicine

This segment involves the use of satellite communication used in the healthcare sector. Satcom is considered to be the most effective way of providing healthcare services in the remote areas where telecommunications are non-existent or poor.

Broadcasting

Broadcasting constitutes the major application for satellite communications. Various DTH providers use satellite communication services for offering their services to the end-users.

Others

The others segment includes the other applications of satellite communication such as tele-education and weather forecasting.

Segment - Vertical

Revenue capture definition

Energy & Utility

This segment includes the use of satellite communications in the energy & utility sector for various applications including smart grids, wind power plants, among others, for various purposes such as asset tracking & monitoring, lone worker safety, and remote communications, among others.

Government & Defense

The segment has been further divided into government, emergency responders, and defense

- Government: This segment covers the use of satellite communications for civil use case applications in the government sector including the judicial, legislative, and executive departments.

- Emergency Responders: This segment includes the use of satellite communication by the various emergency responders including the police departments, fire departments, rescue teams, among others.

- Defense: This segment includes the use of satellite communications primarily for military applications that include voice and data sharing, Intelligence, surveillance, and Reconnaissance (ISR), among others.

Transport & Cargo

The segment has been further divided into fleet management, rail services, and maritime.

- Fleet Management: This segment includes the use of satellite communications for the management and tracking of the assets, and other applications related to the logistics industry.

- Rail services: This segment includes the use of satellites for providing broadband communication services on the trains.

Maritime

Maritime: This segment includes the use of satellite communications for various commercial and mission critical maritime applications that include broadband connectivity on ships, leisure vessels, tankers, shipping containers, among others; asset monitoring & tracking, navigation, among others.

Mining and Oil & Gas

The segment has been further divided into oil & gas, and mining

- Oil & Gas: This segment includes the use of satellite communications for various applications in the oil & gas industry such as asset management and tracking in the oil rigs and gas stations due to their remote locations, workforce monitoring, remote planning, among others.

- Mining: This segment includes the use of satellite communications for various applications in the mining sector such as asset management and tracking in the mining sites, workforce monitoring, site surveillance, among others.

Agriculture

This segment includes the use of satellite communications used in the agriculture industry for applications that include weather monitoring, asset management, field mapping, crop management & animal monitoring, among others.

Communication Companies

This segment includes the use of satellite communications by the telecom service providers for backhaul applications.

Corporates/Enterprises

This segment includes the use of satellite communications for broadband applications as well as data backup and recovery applications.

Media & Broadcasting

This segment includes the use of satellite communications by the media delivery channels such as dish and DTH operators for broadcasting applications.

Events

This segment includes the use of satellite communications for providing connectivity in various events such as concerts, conferences, among others.

Aviation

This segment includes the use of satellite communication for various applications in the aviation industry such as in-flight connectivity, air traffic management, asset tracking, among others. Satcom also enables various uses in the cockpit and the cabin including safety communications, and weather & flight-plan updates.

Environmental & Monitoring

This segment includes the use of satellite communication for environmental monitoring and earth observation applications, among others.

Forestry

This segment includes the use of satellite communication for forest applications that include lone worker safety, real-time connectivity, asset monitoring, forest mapping, among others.

End User - Consumer

This segment includes the use of satellite communications for providing voice and data connectivity to the individual end-users that are in the remote areas with limited or no terrestrial connectivity.

Healthcare

This segment includes the use of satellite communication for various commercial and mission critical applications such as remote patient monitoring, remote device management, among others.

Others

This segment includes the satellite communications used in the retail and construction industry for various applications.

Estimation Model

Layer Name

Key Question

Description

Connectivity Demand Base / Demand Layer

Who requires communication and connectivity services that can be supported by satellite networks?

Establish the total potential demand base by identifying governments, defense organizations, telecom operators, enterprises, transportation providers, broadcasters, utilities, and consumers requiring reliable communication services.

Addressable Market Layer

Who can realistically be reached and served by satellite communication providers?

Refine the total connectivity ecosystem into the realistically serviceable market by considering factors such as satellite coverage availability, ground infrastructure deployment, regulatory approvals, spectrum access, technology compatibility, and affordability.

Satellite Communication Adoption & Utilization Layer

Who is actively utilizing satellite communication solutions and generating network demand?

Estimate annual demand generation by analyzing satellite service adoption rates, bandwidth consumption, airtime utilization, equipment deployment, enterprise connectivity requirements, and application-specific usage across voice, data, M2M, broadcasting, navigation, telemedicine, and tracking services.

Revenue Layer

How is revenue generated from satellite communication demand?

Converts satellite communication demand into market revenue through the sale of satellite communication equipment and the provision of satellite-based services. Revenue is calculated by applying equipment prices, along with service-related revenues generated from subscriptions.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Entity-wise Value Chain Structure Analysis (% Share)

Delivered detailed value chain assessment of the satellite communication ecosystem, including Satellite Manufacturers, Launch Service Providers, Satellite Operators, and Satellite Service Providers

Evaluated the flow of value creation from satellite design and manufacturing through launch, operation, and end-user service delivery

Enabled identification of the most value-generating segments within the satellite communication ecosystem

Supported strategic investment and partnership decisions

Improved understanding of industry structure and revenue distribution

Analysis of Role of LEO Satellites in the Satellite Communication Industry

Delivered comprehensive analysis of the growing role of LEO satellites in transforming global satellite communications

Assessed the impact of LEO constellations on broadband connectivity, rural internet access, mobility services, IoT connectivity, and government communications

Evaluated competitive positioning of LEO systems relative to traditional GEO and MEO satellite networks in terms of latency, capacity, coverage, and service flexibility

Enabled understanding of emerging technology trends reshaping the satellite communication market

Supported strategic planning related to next-generation satellite networks

Identified high-growth opportunities associated with LEO satellite deployments

Competitive Benchmarking & Strategic Landscape Analysis

Delivered benchmarking of major satellite operators, equipment providers, and service companies based on fleet size, capacity, technology capabilities, geographic presence, and strategic initiatives

Analysis of partnerships, mergers & acquisitions, satellite launches, and product innovations

Supported competitive intelligence and strategic decision-making

Enabled identification of market gaps and expansion opportunities

Frequently Asked Questions About This Report

North America dominated the global market with the largest revenue share of 34.5% in 2025. The growing demand for satellite broadband services, especially for reliable connectivity in remote, hard-to-reach, and underserved regions of North America, is likely to drive regional growth over the forecast period.

Some key players operating in the SATCOM market include SES S.A.; Viasat, Inc.; Intelsat; Telesat; EchoStar Corporation; L3 Technologies, Inc.; Thuraya Telecommunications Company; SKY Perfect JSAT Group; GILAT SATELLITE NETWORKS; Cobham Limited.

Key factors that are driving the satellite communication market growth include the escalating demand for small satellites for earth observation services in various industries such as oil & gas, energy, agriculture, and defense and the increasing use of satellite communications by companies to collect operational data to improve efficiency and to realize sustainable ways of conducting business.

Asia Pacific is the fastest-growing region over the forecast period.

Based on component, the services segment led the market with the largest revenue share of 58.6% in 2025, while equipment is the fastest-growing component.

Based on frequency band, the Ku-band segment led the market with the largest revenue share of 25.4% in 2025, while Ka-band is the fastest-growing frequency band.

Based on application, the broadcasting segment led the market with the largest revenue share of 22.8% in 2025, while airtime is the fastest-growing application.

The global satellite communication market size was estimated at USD 98.3 billion in 2025 and is projected to reach USD 107.4 billion by 2026.

The global satellite communication market is expected to grow at a compound annual growth rate of 11.0% from 2026 to 2033 to reach USD 223.1 billion by 2033.

About the Author(s)

Communications Infrastructure Research Team

Technology · Communications InfrastructureThis report was authored by the communications infrastructure research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the communications infrastructure segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.