- Home

- »

- Next Generation Technologies

- »

-

Satellite Launch Services Market Growth Report, 2026-2033GVR Report cover

![Satellite Launch Services Market Size, Share & Trends Report]()

Satellite Launch Services Market (2026 - 2033) Size, Share & Trends Analysis Report By Service, (Pre-Launch, Post-Launch), By Payload, By Launch Platform, By Launch Type, By Launch Vehicle, By End Use, By Region, And Segment Forecasts

Market Size, 2025

$10.4BMarket Estimate, 2026

$12.1BMarket Forecast, 2026

$27.7BCAGR, 2026–2026

12.5%Satellite Launch Services Market Summary

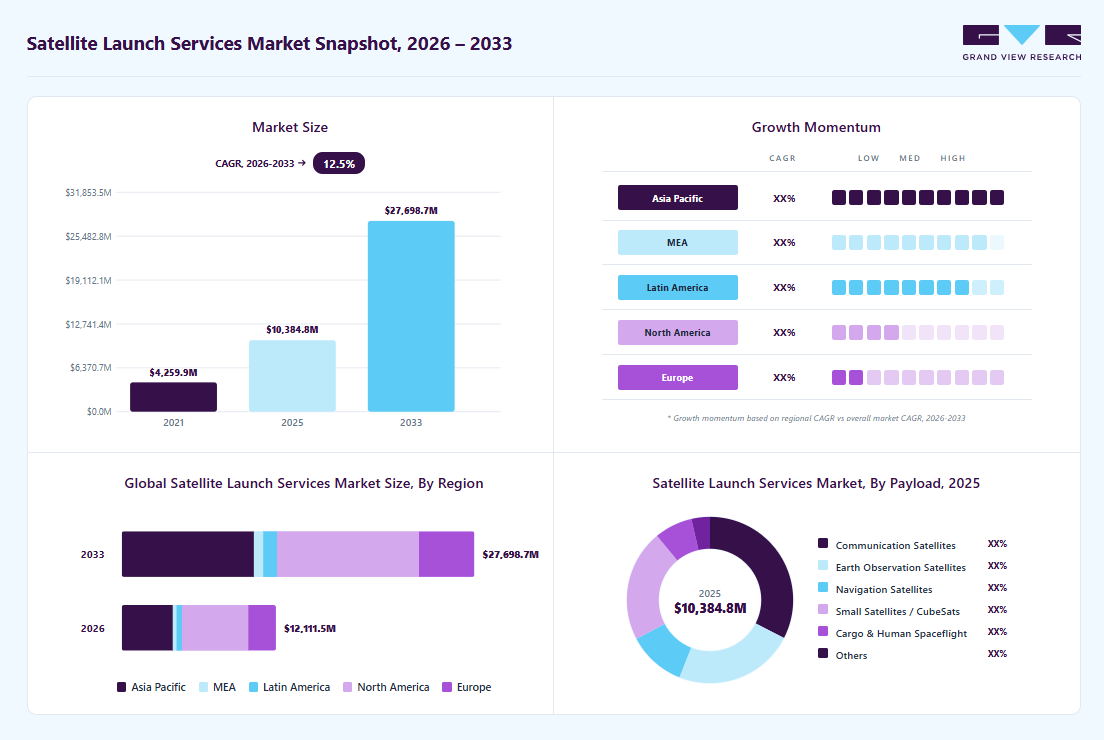

The global satellite launch services market size was valued at USD 10.4 billion in 2025 and is projected to grow from USD 12.1 billion in 2026 to USD 27.7 billion by 2033, at a CAGR of 12.5% from 2026 to 2033. The North America held the largest share of 43.0% of the global market in 2025. The market growth is driven by the surging demand for LEO mega-constellations, reusable rocket innovations slashing costs, smallsat and CubeSat proliferation for Earth observation and broadband, rising government and defense investments through programs such as NSSL and Galileo, and emerging AI and space data.

Key Market Trends & Insights

- By service: Pre-launch segment held the dominant position and accounted for the largest revenue share of 74.0% in 2025.

- By payload: Communication satellites segment accounted for the largest market revenue share in 2025.

- By end use: Government segment accounted for the largest market share in 2025.

- By launch vehicle: Medium launch vehicle segment accounted for the largest revenue share in 2025.

Regional Highlights

- Largest regional market: North America(43.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. dominated the market in 2025.

Market Size & Forecast

- Market size in 2025: USD 10.4 Billion

- Estimated market size in 2026: USD 12.1 Billion

- Projected market size by 2033: USD 27.7 Billion

- CAGR (2026-2033): 12.5%

Additionally, the growing advancements in reusable rocket technology, satellite miniaturization, and rideshare launch models are enabling more frequent satellite deployments worldwide, thereby driving the satellite launch services industry growth.")

The rise in demand for satellite-based services is transforming the satellite industry by driving significant growth in launch needs and orbital deployments. Industries such as telecommunications, Earth observation, navigation, defense, broadband internet, IoT connectivity, and maritime/aviation services increasingly depend on large constellations of satellites, especially smallsats in Low Earth Orbit, to provide real-time data, global connectivity, precise positioning, and geospatial intelligence. This increase results from applications such as precision agriculture for monitoring crop yields, disaster response for tracking hazards, urban planning for mapping infrastructure, environmental surveillance for detecting climate impacts, asset tracking via IoT/M2M networks, and in-flight/maritime broadband.

In addition, the trend toward developing smaller, more affordable satellites, known as smallsats, is drastically transforming the satellite industry. These compact satellites are easier and cheaper to produce and launch, allowing more startups, universities, and research organizations to access satellite technology, which was previously out of reach. This rapid rise in SmallSat (under 500 kg) and CubeSat (10×10×10 cm) deployments is one of the most significant drivers of demand in the satellite launch services market, primarily owing to their affordability and broader accessibility.

Furthermore, the growing advancements in launch vehicle technologies are emerging as a significant driver for the growth of the satellite launch vehicles industry, enabling more efficient, reliable, and cost-effective access to space. Modern launch systems are increasingly incorporating advanced propulsion systems, lightweight composite materials, autonomous flight control systems, and digital design techniques to improve launch performance and reduce operational costs. These technological improvements enable launch vehicles to carry heavier payloads, perform more precise orbital insertions, and support a broader range of satellite missions.

Moreover, companies are investing in satellite launch services to deploy satellite constellations, reduce launch costs through reusable rocket technology, and meet surging demand for broadband internet, Earth observation, and defense applications. This investment trend is driven by private-sector innovation from players like SpaceX, Rocket Lab, and Blue Origin, alongside government initiatives that expand commercial space access. These factors are expected to collectively drive the expansion of the satellite launch services industry in the coming years.

Service Insights

The pre-launch segment accounted for the largest share of 74% in 2025, primarily driven by the increasing complexity of satellite missions and the rising demand for mission assurance, integration, and regulatory compliance services prior to launch. Satellite operators require detailed trajectory planning, payload integration, environmental testing, and launch window optimization to ensure successful orbital deployment. These pre-launch services are critical for mitigating risks and enabling reliable mission success.

The post-launch segment is expected to grow at the highest CAGR of 14.5% from 2026 to 2033, fueled by increasing demand for in-orbit support services, satellite deployment validation, orbit-raising maneuvers, and mission performance monitoring. With operators investing heavily in satellite constellations, ensuring optimal orbital insertion and long-term operational efficiency has become essential. These post-launch capabilities are vital for sustaining constellation performance and scalability, which is further driving the segmental growth.

Payload Insights

The communication satellites segment accounted for the largest market revenue share in 2025. The segment growth is propelled by surging global demand for broadband connectivity, 5G backhaul, and direct-to-device satellite communication services. Expanding satellite internet constellations are accelerating launch frequency, particularly for high-throughput satellites operating in LEO and GEO, thereby driving adoption of communication satellites.

The small satellites/cubesat segment is expected to grow rapidly from 2026 to 2033, driven by the low-cost, lightweight satellites designed for research, Earth imaging, IoT connectivity, and technology demonstration missions. Universities, startups, and commercial operators are increasingly adopting CubeSats due to their shorter development cycles and reduced capital requirements, thereby driving the segmental expansion.

Launch Platform Insights

The land segment accounted for the largest market share in 2025, driven by the strong global reliance on established ground-based spaceports that offer proven infrastructure, higher payload capacity handling, and scalable launch frequency. Land-based launch complexes enable heavy-lift missions, large constellation deployments, and deep-space exploration programs due to their robust assembly, fueling, and testing facilities, which are expected to drive segmental growth in the coming years.

The sea segment is anticipated to grow at the fastest CAGR in the coming years. The growth is propelled by the strategic advantage of launching from equatorial ocean locations, which improves payload efficiency and allows optimized orbital insertion. Sea-based platforms offer mobility, enabling operators to select ideal launch coordinates while minimizing risks to populated areas. The suitability of the sea launch platform is an essential factor driving segmental growth.

Launch Type Insights

The single-use segment accounted for the largest share of revenue in 2025. The growth is propelled by mission-specific reliability requirements, particularly for high-value government, defense, and deep-space exploration payloads. Expendable launch vehicles often provide higher payload-to-orbit capacity without the structural compromises required for recovery systems. The unmatched reliability for critical missions, cost predictability for low-volume programs, and accessibility for new entrants in regions. These dynamics ensure that the single-use segment maintains a robust position in the satellite launch services market.

The reusable segment is expected to expand quickly from 2026 to 2033, driven by the growing focus on cost savings, sustainability, and increased launch frequency. Reusable rocket technology greatly reduces per-mission costs by recovering and refurbishing boosters for multiple flights. Commercial satellite operators prefer this approach because it offers more predictable pricing and shorter scheduling cycles. Advances in vertical landing, autonomous guidance systems, and heat-shield durability are boosting adoption, thereby driving segmental expansion.

Launch Vehicle Insights

The medium launch vehicle segment accounted for the largest revenue share in 2025, driven by balanced payload capacity, cost efficiency, and versatility across commercial and institutional missions. Medium-lift rockets are widely used for communication, navigation, and Earth observation satellites that require moderate payload mass. Their adaptability to both single and multi-satellite deployments enhances mission flexibility, thereby driving segmental growth.

The small launch vehicle segment is expected to grow rapidly from 2026 to 2033, driven by the accelerating deployment of small satellite constellations for Earth observation, IoT connectivity, remote sensing, and technology validation. Small launch vehicles provide dedicated, timely orbital access for CubeSats and microsatellites, eliminating delays and orbital constraints associated with rideshare launches. Their comparatively lower manufacturing, infrastructure, and operational costs make them highly attractive to startups, research institutions, and emerging space nations seeking affordable access to space. These factors collectively drive segmental growth.

End Use Insights

The government segment accounted for the largest market share in 2025, driven by expanding national space programs, scientific exploration initiatives, and long-term strategic infrastructure development plans. Governments worldwide are significantly increasing investments in satellite systems to strengthen capabilities in weather forecasting, climate monitoring, secure communications, and digital connectivity. The growing emphasis on sovereign space access and independent launch capabilities has intensified public-sector procurement of domestic launch services. These factors collectively drive segmental growth.

The commercial segment is expected to grow rapidly from 2026 to 2033, primarily driven by rapid private-sector expansion across satellite broadband, IoT connectivity, Earth observation analytics, and data-driven space services. Commercial operators are aggressively deploying large-scale satellite constellations to provide global internet coverage, enterprise communication networks, and real-time geospatial intelligence solutions, thereby driving the segmental growth.

Regional Insights

The satellite launch services industry in North America dominated the global market with a revenue share of over 43% in 2025. The region benefits from well-established launch infrastructure, advanced reusable rocket technologies, and close collaboration between government space agencies and private launch providers. Increasing investments in missile warning systems, secure communication satellites, and Earth observation programs are significantly accelerating launch demand.

U.S. Satellite Launch Services Market Trends

The U.S. satellite launch services industry accounted for the largest market share of over 93% in 2025. The market is propelled by NASA-led exploration programs, multi-billion-dollar defense contracts, and aggressive deployment of commercial broadband constellations. The country leads in reusable launch vehicle innovation, significantly lowering per-launch costs and increasing mission frequency. Strong federal funding for space resilience and next-generation missile detection systems is fueling demand for reliable and secure launch services.

Europe Satellite Launch Services Market Trends

The satellite launch services industry in Europe accounted for a share of over 18% from 2026 to 2033. In Europe, the market is driven by strong institutional backing from the European Space Agency, expansion of sovereign launch capabilities, and rising commercial satellite deployments. Europe is focusing on reducing its reliance on foreign launch providers by accelerating the development of next-generation heavy-lift and reusable launch systems. Increased investment in climate monitoring, navigation upgrades, and secure government communication satellites further strengthens launch activity.

The UK satellite launch services industry is expected to grow rapidly in the coming years, driven by increased investment in small-satellite manufacturing, spaceport development initiatives, and defense-related space programs. The country is positioning itself as a hub for small satellite launches and responsive space missions.

The satellite launch services industry in Germany is driven by rising investments in Earth observation programs, industrial satellite manufacturing, and advanced propulsion research. The government’s emphasis on climate data analytics and defense modernization is increasing demand for dedicated satellite missions. Germany’s strong aerospace engineering ecosystem supports technological advancement in satellite payload systems. Increasing collaboration with European launch providers enhances access to space for institutional missions.

Asia Pacific Satellite Launch Services Market Trends

The satellite launch services industry in the Asia Pacificis anticipated to register the fastest CAGR of 14.6% from 2026 to 2033, driven by expanding government-backed space programs, rapid deployment of communication and Earth observation satellites, and increasing investments in sovereign launch capabilities. Countries across the Asia Pacific are prioritizing independent access to space to strengthen national security, digital connectivity, and climate monitoring infrastructure.

The Japan satellite launch services industry is gaining momentum, fueled by investments in next-generation launch vehicles, national security satellite programs, and disaster monitoring systems. Japan is enhancing its launch autonomy through upgrades to the H3 rocket program, aiming to strengthen payload capacity and cost efficiency. Rising emphasis on climate observation and space-based communication resilience is further fueling launch demand.

The satellite launch services industry in China is witnessing robust expansion, driven by aggressive expansion of state-backed satellite constellations, defense modernization programs, and strategic investments in heavy-lift and reusable launch vehicle technologies. The country continues to strengthen its BeiDou navigation system and deploy large-scale communication and remote sensing satellites.

Key Satellite Launch Services Company Insights

Some of the key players operating in the market are Arianespace and SpaceX, among others.

-

Arianespace is a subsidiary of ArianeGroup, a joint venture between Airbus and Safran, and operates as the world's first commercial space transportation company. The company provides reliable satellite launches to geostationary transfer orbit, low earth orbit, and other trajectories using the Ariane rocket family, including the operational Ariane 6 medium-to-heavy-lift vehicle, as well as the Vega light launcher for smaller payloads.

-

SpaceX is a spacecraft manufacturer and launch service provider known for developing reusable rockets, such as the Falcon 9, and the Dragon spacecraft. The company has become the first private entity to return a spacecraft from low Earth orbit and transport astronauts to the International Space Station (ISS). With its Falcon 1, Falcon 9, and Falcon Heavy rockets, the company has achieved numerous milestones, including the first successful landing of an orbital-class rocket and the development of fully reusable launch vehicles.

Some of the emerging players operating in the market include International Launch Services (ILS) and Rocket Lab, among others.

-

International Launch Services (ILS) provides comprehensive commercial satellite launch services and offers end-to-end support from contract signing through mission management, payload integration, and on-orbit delivery for global operators, having facilitated over 400 missions with a focus on GTO and LEO deployments. ILS serves commercial and government customers worldwide, emphasizing dependable access to space through proven Russian launch vehicles while maintaining U.S.-based sales and operations expertise.

-

Rocket Lab offers dependable launch services through its Electron rocket, spacecraft platforms like Photon for satellite missions, satellite subsystems including solar arrays and reaction wheels, and in-orbit operational support encompassing telemetry management, collision avoidance, and end-of-life disposal planning. The company has a presence in New Zealand, the U.S., and global markets serving commercial constellations, government agencies, and defense clients.

Key Satellite Launch Services Companies:

The following key companies have been profiled for this study on the satellite launch services market

- Arianespace

- Blue Origin

- China Aerospace Science and Technology Corporation

- Firefly Aerospace

- International Launch Services (ILS)

- Indian Space Research Organization (ISRO)

- Rocket Lab

- SpaceX

- United Launch Alliance

- Relativity Space

Recent Developments

-

In February 2026, SpaceX acquired xAI in a record USD 1.25 trillion all-stock deal valuing SpaceX at USD 1 trillion and xAI at USD 250 billion, integrating AI capabilities for space-based data centers and Starlink ahead of a planned IPO.

-

In February 2026, United Launch Alliance announced plans for 18-22 launches throughout the year, targeting 2-4 Atlas V missions and 16-18 Vulcan Centaur flights split between Cape Canaveral and Vandenberg.

-

In January 2026, Blue Origin announced New Glenn-3 to launch AST SpaceMobile’s next-generation Block 2 BlueBird satellite to low Earth orbit, expanding its orbital launch commitments in the satellite connectivity market.

Satellite Launch Services Market Report Scope

Report Attribute

Details

Market size in 2025

USD 10.4 billion

Estimated market size in 2026

USD 12.1 billion

Projected market size by 2033

USD 27.7 billion

Growth rate

CAGR of 12.5% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million and CAGR from 2026 to 2033

Report Product

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Service, payload, launch platform, launch type, launch vehicle, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Japan; India; South Korea; Australia; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Arianespace; Blue Origin; China Aerospace Science and Technology Corporation; Firefly Aerospace; International Launch Services (ILS); Indian Space Research Organization (ISRO); Rocket Lab; SpaceX; United Launch Alliance; Relativity Space

Customization scope

Free report customization (equivalent to up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet you exact research needs. Explore purchase options

Global Satellite Launch Services Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends across sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global satellite launch services market report based on service, payload, launch platform, launch type, launch vehicle, end use, and region.

-

Service Outlook (Revenue, USD Million, 2021 - 2033)

-

Pre-Launch

-

Post-Launch

-

-

Payload Outlook (Revenue, USD Million, 2021 - 2033)

-

Communication Satellites

-

Earth Observation Satellites

-

Navigation Satellites

-

Small Satellites / CubeSats

-

Cargo & Human Spaceflight

-

Others

-

-

Launch Platform Outlook (Revenue, USD Million, 2021 - 2033)

-

Land

-

Air

-

Sea

-

-

Launch Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Re-Usable

-

Single-Use

-

-

Launch Vehicle Outlook (Revenue, USD Million, 2021 - 2033)

-

Small Launch Vehicle

-

Medium Launch Vehicle

-

Heavy Launch Vehicle

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Government

-

Military

-

Commercial

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa (MEA)

-

UAE

-

South Africa

-

Kingdom of Saudi Arabia (KSA)

-

-

Frequently Asked Questions About This Report

The global satellite launch services market size was valued at USD 10.4 billion in 2025 and is estimated at USD 12.1 billion for 2026.

The global satellite launch services market is expected to grow at a CAGR of 12.1% from 2026 to 2033, reaching USD 27.7 billion by 2033.

Asia Pacific is anticipated to grow at the fastest CAGR during the forecast period.

Key players in satellite launch services market include Arianespace, Blue Origin, China Aerospace Science and Technology Corporation, Firefly Aerospace, International Launch Services (ILS), Indian Space Research Organization (ISRO), Rocket Lab, SpaceX, United Launch Alliance, and Relativity Space.

The surging demand for LEO mega-constellations, reusable rocket innovations slashing costs, smallsat and CubeSat proliferation for Earth observation and broadband, rising government and defense investments through programs such as NSSL and Galileo, and emerging AI and space data are the key factors driving the market growth.

The pre-launch segment accounted for the largest share of 74% in 2025, while the post-launch segment is expected to grow at the highest CAGR of 14.5% from 2026 to 2033.

The communication satellites segment accounted for the largest market share in 2025.

The single-use segment accounted for the largest share of revenue in 2025.

The government segment accounted for the largest share of revenue in 2025.

North America dominated the market with a revenue share of 43.0% in 2025.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.