- Home

- »

- Next Generation Technologies

- »

-

Server Market Size, Share And Trends Report, 2026-2033GVR Report cover

![Server Market (2026 - 2033)Report]()

Server Market (2026 - 2033)

Size, Share, & Trends Analysis By Product (Rack, Blade, Tower, Micro, Open Compute Project), By Channel (Direct, Reseller), By Enterprise Size (Micro, Small), By End Use (IT & Telecom, BFSI, Healthcare, Energy, Others), By Region, and Segment Forecasts

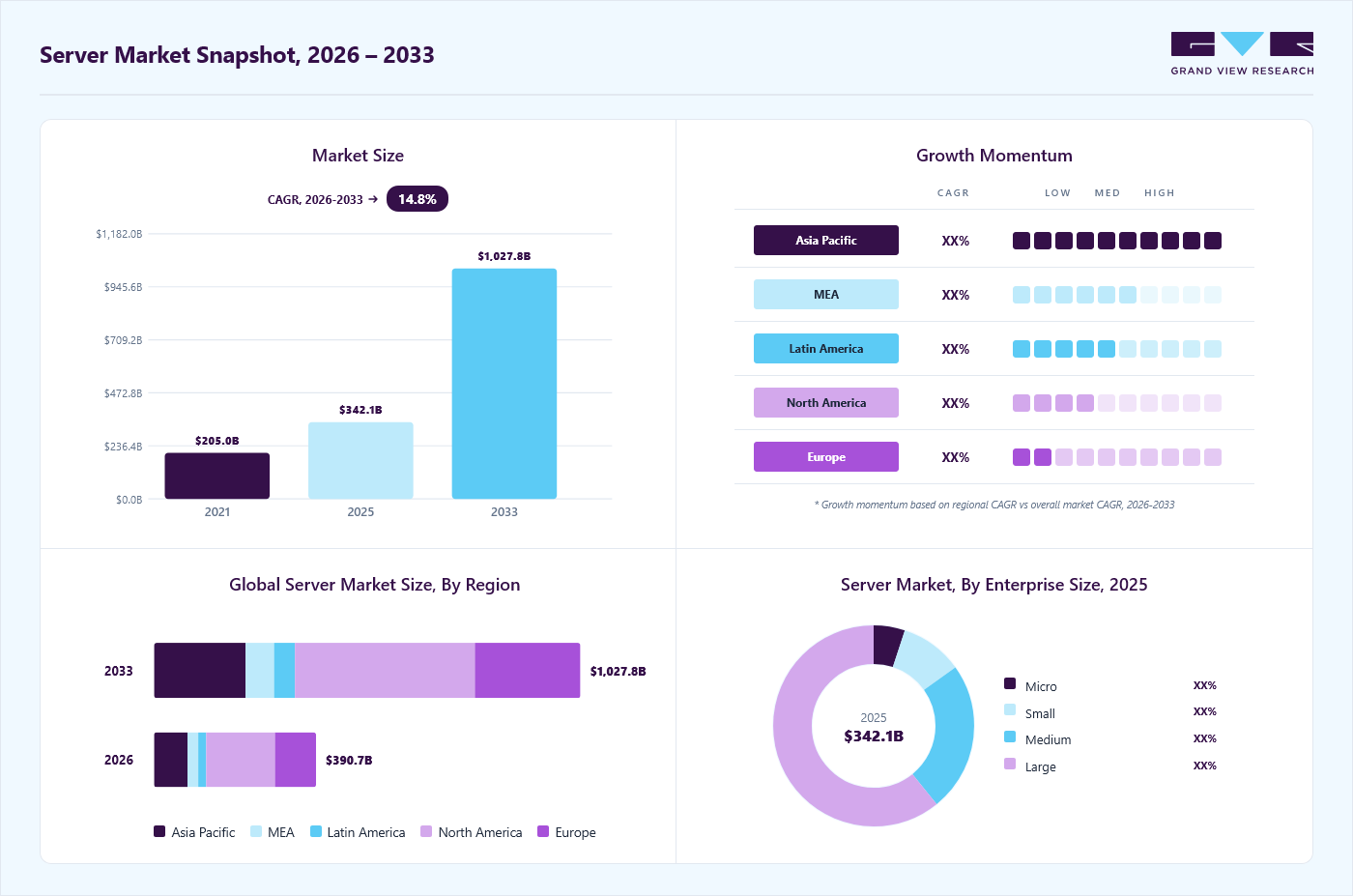

Market Size, 2025

$342.1BMarket Estimate, 2026

$390.7BMarket Forecast, 2033

$1,027.8BCAGR, 2026–2033

14.8%Server Market Summary

The global server market size was valued at USD 342.1 billion in 2025 and is projected to grow from USD 390.7 billion in 2026 to USD 1,027.8 billion by 2033, at a CAGR of 14.8% from 2026 to 2033. The market in North America dominated with a revenue share of 42.5% in 2025. The market growth is attributed to the widespread adoption of smartphones and the surging count of data centers worldwide.

Key Market Trends & Insights

- By product: Rack segment held the largest market share of 37.4% in 2025.

- By channel: Reseller segment held the largest market share in 2025.

- By enterprise size: Large segment held the largest market share in 2025.

- By end-use: IT & telecom segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (42.5% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 342.1 Billion

- Estimated market size in 2026: USD 390.7 Billion

- Projected market size by 2033: USD 1,027.8 Billion

- CAGR (2026-2033): 14.8%

Server manufacturers and hyperscale operators are increasingly adopting advanced, high-performance server solutions designed to handle AI, HPC, and enterprise workloads, incorporating GPU acceleration, modular architectures, and energy-efficient designs. Enterprises and cloud providers are investing in specialized servers equipped with high-speed memory, GPUs, and storage optimization to support AI inference, data analytics, and cloud-native workloads. The growing demand for AI, digital twins, and large-scale data processing is driving the need for high-density, energy-efficient, and modular server architectures that can deliver both speed and flexibility across on-premises, cloud, and edge deployments.")

In addition, regional production facilities, workload-specific server optimization, and collaboration between OEMs and enterprises are enabling faster deployment and improved customization to meet evolving enterprise requirements. For instance, in August 2025, HPE, in collaboration with AMD, launched a new Saudi-made server at Alfanar, aimed at providing Middle East customers with more flexibility, speed, and choice. Similarly, in September 2025, Edgecore Networks introduced the AGS8600 high-performance GPU AI server designed for AI and HPC workloads, highlighting the shift toward AI-ready, high-performance infrastructure tailored to emerging enterprise and research applications.

Product Insights

The rack segment accounted for the largest revenue share of 37.4% in the global server market in 2025, driven by rising enterprise demand for scalable, space-efficient, and performance-optimized server configurations. Rack servers provide superior processing density and easier integration into data center infrastructures, making them the preferred choice for hyperscalers, cloud providers, and enterprises managing AI, HPC, and virtualization workloads. Their modular design supports flexible deployment and workload optimization, further strengthening the segment’s market dominance. Driving this momentum, vendors are launching next-generation rack servers with enhanced AI automation, integrated security, and energy efficiency to address evolving workload demands. For instance, in February 2025, Hewlett Packard Enterprise (HPE) introduced its next-generation ProLiant servers, engineered for advanced security, AI automation, and higher performance. These servers are designed to deliver cloud-native experiences and intelligent operations across hybrid environments, underscoring the market shift toward high-density, AI-ready rack architectures optimized for agility, reliability, and sustainability.

The blade server segment is expected to register a significant CAGR during the forecast period, driven by rising demand for high-density, modular compute systems across enterprise and hyperscale data centers. Blade architectures provide superior compute density, efficient cooling, and streamlined management, making them ideal for virtualization, HPC, and AI workloads. Growing adoption of edge data centers and AI-driven applications is further accelerating the shift toward compact, energy-efficient server designs. Leading manufacturers are introducing next-generation blade solutions with enhanced interconnects and thermal efficiency to meet the performance and scalability needs of modern workloads. For instance, in August 2025, GigaComputing announced the launch of its new blade server solution featuring next-generation cooling and modular interconnects to support edge data centers and high-performance compute applications, underscoring the growing focus on high-density, power-efficient architectures that can handle complex and distributed computing environments.

Channel Insights

The reseller segment accounted for the largest market share in 2025, driven by the strong presence of value-added distributors and IT solution partners catering to diverse enterprise and SMB requirements. Resellers play a pivotal role in bridging server manufacturers with end users by offering customized configurations, integration services, and post-deployment support. The rapid adoption of hybrid and edge computing, coupled with increasing enterprise focus on flexible procurement models, has further strengthened this channel’s growth. Moreover, the expansion of cloud solution provider (CSP) partnerships and regional reseller ecosystems is enabling faster delivery of tailored server solutions across industries. For instance, leading OEMs such as HPE and Dell Technologies continue to expand their global partner programs, empowering resellers to deliver advanced server platforms with AI-ready, secure, and workload-optimized configurations, reinforcing the reseller segment’s dominance in the overall market.

The direct segment is expected to grow at the fastest CAGR over the forecast period, driven by increasing demand for customized, large-scale server deployments among hyperscale’s, cloud service providers, and government agencies. Direct sales channels, comprising Original Design Manufacturers and direct OEM engagements, enable enterprises to procure tailor-made server configurations optimized for specific workloads such as AI, high-performance computing, and data analytics. The rise of hyperscale data centers and workload-specific infrastructure is further accelerating the preference for direct procurement models that offer greater flexibility, shorter lead times, and cost efficiencies. For instance, major players such as Hewlett Packard Enterprise and Lenovo are expanding direct partnerships with regional enterprises and hyperscalers to deliver high-performance, AI-optimized server solutions that ensure scalability, energy efficiency, and seamless integration with existing IT ecosystems, supporting the segment’s rapid growth trajectory. Consequently, the direct channel is poised to play a pivotal role in shaping the future of the global server market by enabling enterprise-grade, tailored infrastructure solutions.

Enterprise Size Insights

The large segment accounted for the largest market share in 2025 in the server market, owing to the increasing demand for high-performance and secure server solutions to support complex workloads such as artificial intelligence and high-performance computing. Large enterprises require robust infrastructure to handle vast amounts of data and ensure seamless operations across multiple regions and departments. As digital transformation accelerates, these organizations are investing in advanced server technologies to enhance agility, improve operational efficiency, and maintain a competitive edge in the market. For instance, in February 2025, F5 unveiled its multi-terabit VELOS hardware, including the CX1610 chassis and BX520 blade, designed to optimize application delivery and security for large enterprises and service providers. This solution offers up to 6 Tbps of throughput, supporting demanding AI workloads and 5G deployments. The VELOS platform integrates advanced security features, such as firewall protection and DDoS mitigation, ensuring the integrity and availability of critical applications. By providing scalable and resilient infrastructure, VELOS enables large enterprises to meet the growing demands of modern applications and maintain high-performance standards across their operations.

The medium enterprise segment is expected to grow at a substantial CAGR over the forecast period, driven by increasing adoption of scalable and flexible server solutions among mid-sized organizations. Medium enterprises are rapidly digitalizing their operations and deploying cloud services, virtualization, and AI-driven applications, which require reliable and high-performance server infrastructure. The growing need for cost-efficient, workload-optimized servers that can support business expansion and multi-location operations is further accelerating demand in this segment. Overall, the medium enterprise segment is poised to become a key growth driver in the global server market as organizations continue to modernize and optimize their IT infrastructure.

End Use Insights

The IT & Telecom segment accounted for the largest market share in 2025 in the global server market, driven by the escalating demand for high-speed data processing, cloud computing, and robust network infrastructure. This sector's growth is fueled by the proliferation of 5G technologies, the expansion of data centers, and the increasing reliance on digital services, necessitating scalable and efficient server solutions. Telecom operators and IT service providers are investing heavily in server infrastructure to support the surge in data traffic and to enable the deployment of advanced applications such as artificial intelligence and machine learning. For instance, in September 2025, Dell Technologies introduced the PowerEdge XR8720T, a high-performance server designed to address the complexities of cloud radio access networks (Cloud RAN). This server is engineered to deliver the necessary computational power and low-latency performance required for the deployment of 5G infrastructure, highlighting the critical role of advanced server technologies in supporting the evolving demands of the IT and Telecom sector.

The BFSI segment is anticipated to register the fastest growth in the global server market, driven by increasing demand for high-performance, secure, and scalable server solutions to support complex financial applications, real-time analytics, and regulatory compliance. Financial institutions are investing in advanced server infrastructure to enhance operational efficiency, improve customer experience, and enable digital transformation initiatives. For instance, in August 2025, Narmi and Grasshopper Bank launched the first Model Context Protocol (MCP) server by a U.S. bank, enabling AI-driven insights for financial institutions. This innovation allows customers to securely connect their accounts to large language models like Anthropic's Claude, providing personalized financial analysis and real-time insights. Such advancements underscore the growing reliance on AI-powered server solutions in the BFSI sector to meet evolving customer expectations and regulatory requirements. Subsequently, the BFSI segment's rapid growth in the server market reflects the industry's commitment to adopting cutting-edge technologies that drive innovation, enhance security, and deliver superior financial services.

Regional Insights

North America server market accounted for the largest market share of 42.5% in 2025 in the global server market, primarily driven by the region’s advanced data center infrastructure, early adoption of high-performance computing, and the presence of leading server manufacturers and hyperscale cloud providers such as Hewlett Packard Enterprise, Dell Technologies, and IBM. Enterprises across industries including IT and Telecom, BFSI, and healthcare are increasingly deploying servers to support AI workloads, cloud computing, virtualization, and large-scale data analytics. Additionally, the region is witnessing growing investments in energy-efficient, modular, and AI-ready server architectures to meet the demands of hybrid and multi-cloud environments. Furthermore, North America is experiencing a surge in strategic collaborations, acquisitions, and technology partnerships aimed at enhancing server capabilities in areas such as GPU acceleration, edge computing, and real-time processing, reinforcing the region’s leadership in high-performance and scalable server infrastructure.

U.S. Server Market Trends

Server market in the U.S. is witnessing rapid adoption of high-performance, AI-optimized, and GPU-accelerated servers to support workloads such as artificial intelligence, machine learning, cloud computing, and high-performance computing. Enterprises and hyperscale data centers are increasingly deploying modular and energy-efficient server architectures to enhance scalability, reduce operational costs, and support hybrid and multi-cloud strategies. There is also a growing focus on advanced security, automation, and real-time management capabilities, with servers being integrated into edge computing and distributed IT environments. Moreover, strategic partnerships between OEMs, cloud providers, and technology innovators are driving innovation in workload-specific server solutions, enabling U.S. organizations to maintain high-performance, resilient, and flexible IT infrastructure.

Europe Server Market Industry Trends

The server market in Europe is anticipated to register significant growth from 2026 to 2033, driven by the increasing adoption of artificial intelligence (AI) and machine learning (ML) applications, which is fueling demand for high-performance computing infrastructure, leading to a surge in deployments of GPU-accelerated servers. Additionally, the expansion of data centers, particularly in countries such as Germany, the UK, and Spain, is supporting the growing need for scalable server solutions. The rise of edge computing is also influencing server architecture, with a shift towards distributed models that require low-latency processing capabilities. Furthermore, the emphasis on sustainability is prompting organizations to invest in energy-efficient server technologies and renewable energy-powered data centers. Consequently, these trends contribute to the dynamic evolution of the European server market.

The UK server market is being shaped by the rapid expansion of 5G networks and the associated demand for low-latency, edge-deployed server infrastructure to support mobile connectivity and IoT applications. Enterprises in financial services, healthcare, and government sectors are increasingly adopting secure, high-performance servers to manage sensitive data and comply with strict UK and EU data protection regulations. Additionally, there is a growing focus on hybrid cloud integration and AI-driven analytics, with organizations investing in modular and GPU-optimized servers to enable advanced workload processing. Strategic government initiatives supporting digital transformation and smart city projects are also driving demand for resilient, energy-efficient server deployments tailored to critical infrastructure.

Server market in Germany is being driven by strong industrial and manufacturing demand for high-performance and reliable IT infrastructure to support Industry 4.0 initiatives, including automation, IoT, and real-time analytics. Enterprises are increasingly deploying servers optimized for virtualization, AI, and edge computing to enhance operational efficiency and manage large volumes of industrial data. Sustainability is also a key focus, with organizations prioritizing energy-efficient and low-carbon server solutions in line with Germany’s green data center initiatives. Additionally, government and enterprise investments in secure cloud infrastructure and digitalization projects are further boosting demand for scalable, high-density server architectures across the country.

Asia Pacific Server Market Trends

Asia Pacific is expected to register the fastest CAGR of 15.4% from 2026 to 2033, driven by the expansion of hyperscale data centers, cloud adoption, and increasing investments in AI and high-performance computing across the region. Countries such as China, Japan, and India are seeing heightened demand for GPU-accelerated and high-density servers to support AI workloads, big data analytics, and edge computing applications. Governments and enterprises are also focusing on digital transformation initiatives, smart city projects, and 5G deployment, which require robust, scalable, and energy-efficient server infrastructure. Additionally, regional manufacturing and localized server production are enabling faster delivery and customization, supporting the diverse IT needs of enterprises and cloud service providers in the region.

The server market in Japan is poised for robust growth from 2026 to 2033, driven by rapid adoption of AI, robotics, and automation technologies across manufacturing, automotive, and electronics sectors. Enterprises are increasingly deploying high-performance GPU-optimized servers to support real-time data processing, predictive maintenance, and smart factory applications. There is also strong demand for energy-efficient and compact server solutions due to limited data center space and rising electricity costs. In addition, Japan is witnessing accelerated deployment of edge computing infrastructure to support IoT networks, 5G applications, and latency-sensitive workloads, while domestic OEMs and technology partners focus on providing localized, high-reliability server solutions tailored to enterprise and industrial requirements.

China server market is projected to expand significantly from 2026 to 2033, supported by the rapid expansion of hyperscale cloud providers such as Alibaba Cloud, Tencent Cloud, and Huawei Cloud, which are investing heavily in AI-optimized and high-density server infrastructure to support large-scale e-commerce, fintech, and smart city applications. Government initiatives focused on domestic technology self-reliance are accelerating demand for locally manufactured servers with advanced security and workload-specific optimizations. The rise of edge computing to support 5G networks, autonomous vehicles, and industrial automation is further boosting the deployment of compact, low-latency server solutions in urban and industrial hubs. In addition, financial services and logistics enterprises are increasingly adopting GPU-accelerated servers to enhance real-time analytics and AI-driven decision-making.

The server market in India is poised for rapid expansion from 2026 to 2033, propelled by rapid digitalization across IT, telecom, and government sectors, with enterprises increasingly deploying high-performance servers to support cloud computing, AI, and big data analytics. The expansion of hyperscale data centers by domestic and global cloud providers, including Reliance Jio, TCS, and AWS India, is fueling demand for energy-efficient, GPU-optimized, and modular server architectures. Additionally, initiatives such as the Digital India program and the push for localized IT manufacturing under the Make in India initiative are accelerating the adoption of locally assembled and customized server solutions. Edge computing deployments to support 5G rollout, IoT applications, and smart city projects are also driving demand for compact, low-latency servers in industrial and urban hubs.

Key Server Company Insights

Key players operating in the server industry are Cisco Systems Inc., Dell Technologies, Fujitsu, Hewlett Packard Enterprise (HPE), and others. Companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals.

Key Server Companies:

The following key companies have been profiled for this study on the server market.

- CiscoSystems Inc.

- Dell Technologies

- Fujitsu

- Hewlett Packard Enterprise (HPE)

- Hitachi

- Huawei

- IBM Corporation

- Inspur

- Lenovo

- Microsoft Corporation

- NEC

- Oracle Corporation

- Samsung Electronics

- Supermicro

Recent Developments

-

In October 2025, Fujitsu announced an expanded strategic collaboration with NVIDIA to create full-stack AI infrastructure, aiming to deliver comprehensive solutions for AI workloads.

-

In January 2025, Lenovo acquired Infinidat, which is expected to enhance its product portfolio and solution system, particularly providing more comprehensive support for Lenovo's partners in the high-end storage segment.

-

In March 2024, Dell Technologies announced a strategic partnership with Nvidia at the GTC developers’ event, unveiling the "Dell AI Factory with Nvidia" platform. This partnership aims to integrate Dell's hardware and software with Nvidia's AI infrastructure. Similarly, Dell revealed that its PowerEdge XE9680 rack servers likely to support a range of new Nvidia GPUs, including the B100, B200, and H200 Tensor Core models.

Server Market Report Scope

Report Attribute

Details

Market size in 2025

USD 342.1 billion

Estimated market size in 2026

USD 390.7 billion

Projected market size by 2033

USD 1,027.8 billion

Growth rate

CAGR of 14.8% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD Million/Billion and CAGR from 2026 to 2033

Report Coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Product, channel, enterprise size, end use, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

Cisco Systems Inc.; Dell Technologies; Fujitsu; Hewlett Packard Enterprise (HPE); Hitachi; Huawei; IBM Corporation; Inspur; Lenovo; Microsoft Corporation; NEC; Oracle Corporation; Samsung Electronics; Supermicro

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Server Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the server market report based on product, channel, enterprise size, end use, and region:

-

Product Outlook (Revenue, USD Billion, 2021 - 2033)

-

Rack

-

Blade

-

Tower

-

Micro

-

Open Compute Project

-

-

Channel Outlook (Revenue, USD Billion, 2021 - 2033)

-

Direct

-

Reseller

-

Systems Integrator

-

Others

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Micro

-

Small

-

Medium

-

Large

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

IT & Telecom

-

BFSI

-

Government & Defense

-

Healthcare

-

Energy

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

Key players include Cisco Systems Inc.; Dell Technologies; Fujitsu; Hewlett Packard Enterprise (HPE); Hitachi; Huawei; IBM Corporation; Inspur; Lenovo; Microsoft Corporation; NEC; Oracle Corporation; Samsung Electronics; Supermicro

North America dominated with a 42.5% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

IT & Telecom held the largest share in 2025 and BFSI is the fastest-growing.

The global server market size was valued at USD 342.1 billion in 2025 and is estimated at USD 392.7 billion for 2026.

The global server market is expected to grow at a CAGR of 14.8% from 2026 to 2033, reaching USD 1,027.8 billion.

Rack segment led with a 37.4% revenue share in 2025.

Large enterprises held the largest revenue share in 2025

Reseller segment held the largest revenue share in 2025, while direct segment is the fastest-growing area.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.