- Home

- »

- Medical Imaging

- »

-

Spinal Imaging Market Size And Share Report, 2026-2033GVR Report cover

![Spinal Imaging Market (2026 - 2033)Report]()

Spinal Imaging Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (X-ray, CT, MRI), By Spinal Region (Cervical, Thoracic, Lumbar, Sacral), By Application, By End-use, By Region, And Segment Forecasts

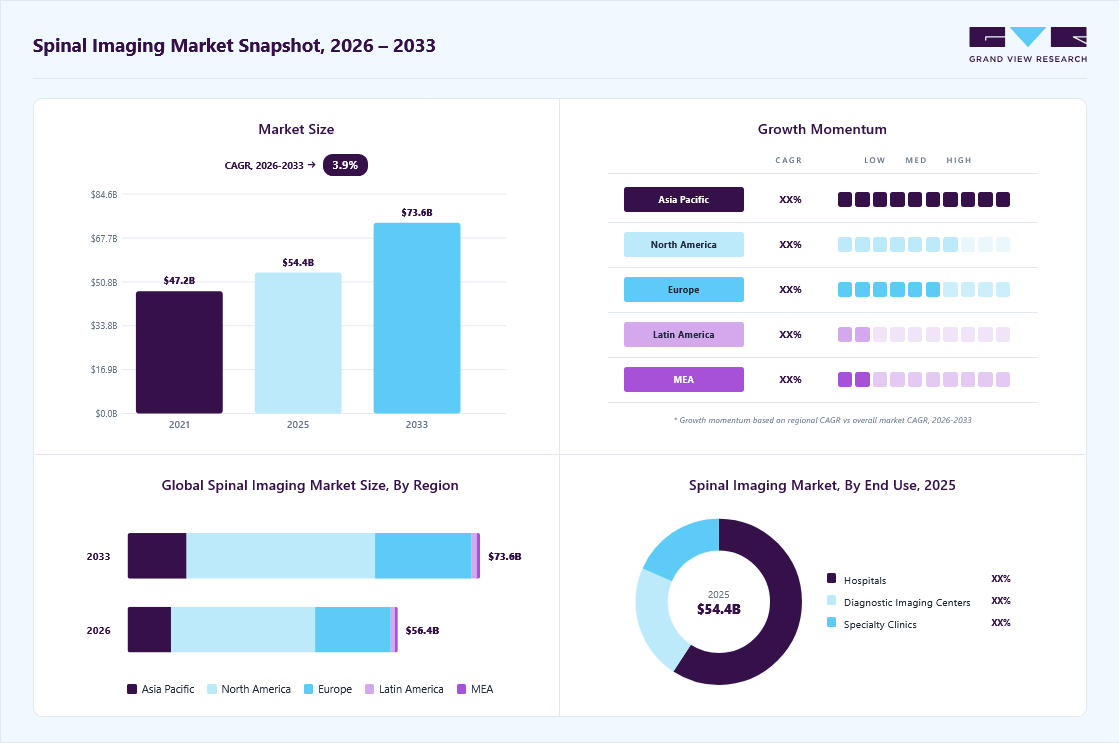

Market Size, 2025

$54.4BMarket Estimate, 2026

$56.4BMarket Forecast, 2033

$73.6BCAGR, 2026–2033

3.9%Spinal Imaging Market Summary

The global spinal imaging market size was valued at USD 54.4 billion in 2025 and is projected to grow from USD 56.4 billion in 2026 to USD 73.6 billion by 2033, at a CAGR of 3.9% from 2026 to 2033. The market in North America dominated with a revenue share of 53.3% in 2025. Driven by rising incidence of spinal conditions, including degenerative disc disease, spinal stenosis, and traumatic spinal injuries.

Key Market Trends & Insights

- By product: MRI segment held the largest market share of 46.7% in 2025.

- By spinal region: Lumbar region segment held the largest market share of 45.4% in 2025.

- By application: Degenerative & pain-related disorders segment held the largest market share of 54.6% in 2025.

- By end-use: Hospital segment held the largest market share of 59.1% in 2025.

Regional Highlights

- Largest regional market: North America (53.3% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 54.4 Billion

- Estimated market size in 2026: USD 56.4 Billion

- Projected market size by 2033: USD 73.6 Billion

- CAGR (2026-2033): 3.9%

The global aging population is more susceptible to these musculoskeletal and degenerative spine disorders. According to the World Health Organization (WHO) in 2024, over 15 million people worldwide have spinal cord injuries, mostly caused by trauma from falls, traffic accidents, or violence. These injuries often lead to additional health problems, early death, and reduced work capacity. As a result, hospitals and clinics increasingly rely on MRI, CT, and X-ray scans for diagnosis, treatment planning, recovery, and ongoing care.Continuous innovation in MRI and CT technologies, including high-resolution imaging, faster scan times, low-dose radiation CT, and AI-enabled image reconstruction, is significantly improving diagnostic accuracy and clinical efficiency in spinal imaging. Advanced imaging systems provide better visualization of soft tissues, nerves, and spinal structures, supporting early diagnosis, treatment planning, and post-operative assessment, thereby accelerating adoption across hospitals and diagnostic imaging centers.

")

Building on these technological advancements, the growing demand for minimally invasive and image-guided spine surgeries is a key growth driver for the spinal imaging industry. These procedures rely heavily on precise pre-operative, intra-operative, and post-operative imaging for accurate localization, navigation, and outcome assessment. Consequently, the expanding adoption of minimally invasive spine interventions is strengthening demand for advanced spinal imaging systems and integrated imaging-navigation platforms.

Market Concentration & Characteristics

The spinal imaging industry shows moderate innovation, primarily driven by incremental advancements in existing MRI and CT platforms rather than disruptive technological breakthroughs. Innovation is largely focused on enhancing image resolution, reducing scan times, lowering radiation exposure, and integrating AI-based image reconstruction and workflow automation to improve diagnostic accuracy and operational efficiency. For instance, in January 2025, Royal Philips launched the AI-enabled CT 5300 and next-generation BlueSeal MRI systems at the Asian Oceanian Congress of Radiology (AOCR 2025, which incorporate advanced AI reconstruction and workflow capabilities and a helium-free wide-bore design to improve diagnostic confidence and throughput in clinical settings.

Mergers and acquisitions in the spinal imaging and broader medical imaging market are moderately active, with strategic deals focused on strengthening imaging capabilities, expanding software and AI portfolios, and enhancing cloud-enabled diagnostic workflows. For Instance, in November 2025, GE HealthCare agreed to acquire medical imaging software provider Intelerad for approximately USD 2.3 billion. This acquisition shows GE HealthCare’s commitment to cloud-enabled and AI-powered solutions across care settings and supports the company’s goal to triple its cloud-enabled products by 2028.

Regulatory frameworks in spinal imaging are well-established and moderately stringent, designed to ensure patient safety, imaging accuracy, and radiation protection while supporting the clinical effectiveness of diagnostic technologies. Regulatory bodies such as the U.S. FDA, European Medicines Agency, and other national health authorities require rigorous clinical validation, quality standards, and compliance with radiation dose and data security guidelines for MRI, CT, and X-ray systems. Reflecting evolving regulatory acceptance of innovation, the U.S. FDA has significantly increased approvals of AI-enabled medical imaging devices, with radiology leading this trend. In 2025, the FDA authorizes 1350 AI-enabled devices, including other imaging tools in radiology. While these frameworks can increase approval timelines and development costs, they also promote standardization, technological reliability, and clinical trust. This enables the sustained adoption of advanced spinal imaging technologies across healthcare systems.

Product expansion in the spinal imaging market reflects ongoing efforts by manufacturers to broaden portfolios, enhance clinical capabilities, and address diverse diagnostic needs across healthcare settings. This includes next-generation imaging systems with improved technical specifications, such as higher spatial resolution, faster acquisition times, and reduced radiation doses. It also involves integrating advanced software features such as AI-driven image reconstruction and workflow automation, and adding complementary tools that support pre-operative planning and intra-operative guidance. Vendors are expanding into hybrid and multimodal imaging platforms, as well as cloud-based imaging and analytics solutions that enable remote interpretation, data management, and interoperability.

Regional expansion involves companies extending their presence across high-growth and mature markets to capture demand for advanced imaging systems. Key efforts focus on Asia Pacific, MEA, and Latin America, driven by rising spinal disorder prevalence and expanding healthcare infrastructure. In North America and Europe, companies strengthen distribution networks and partnerships with hospitals and imaging centers. Investments in localized sales, service, training, and regulatory compliance support effective market penetration, enabling vendors to increase revenue, enhance brand presence, and improve access to spinal imaging technologies globally.

Product Insights

The MRI segment dominated the market with the largest revenue share of 46.7% in 2025. This dominance is due to its ability to provide high-resolution images without ionizing radiation, making it a safer alternative to CT scans, especially for patients needing frequent imaging. MRI's excellent soft tissue contrast allows detailed imaging of spinal structures, intervertebral discs, and surrounding tissues, helping identify issues such as herniated discs, spinal stenosis, and infections. Upgrades in MRI technology, including diffusion tensor imaging (DTI) and functional MRI (fMRI), have expanded its ability to evaluate nerve function and pinpoint areas of pain or inflammation. These advantages have established MRI as the preferred imaging method for various spinal disorders.

The computed tomography (CT) segment is projected to grow significantly over the forecast period. CT excels at visualizing bony structures and calcifications, making it valuable for detecting fractures, spinal deformities, and certain infections. CT scans provide faster results and are more cost-effective than MRI, which is advantageous in emergencies or when cost is a concern. Advancements in CT technology, such as multi-detector CT (MDCT) and low-dose CT protocols, improve image quality while reducing radiation exposure, making CT a more attractive option for a wider range of patients. These factors, along with the increasing prevalence of spinal disorders and the need for rapid and accurate diagnosis, drive the growth of the CT segment in the spinal imaging market.

Spinal Region Insights

The lumbar region segment held the largest revenue share of 45.4% in 2025. This dominance is driven by the high prevalence of lower back pain and lumbar degenerative disorders, along with the frequent clinical need for imaging, as conditions such as lumbar disc herniation, spinal stenosis, spondylosis, and degenerative disc disease are most often diagnosed here. The lumbar spine bears the greatest mechanical load, it is susceptible to age-related degeneration and injury, resulting in increased imaging volumes for MRI and CT scans. In addition, rising spinal surgeries and interventional procedures fuel greater pre- and post-operative imaging demand. These factors combine to drive substantial market growth in this segment.

The cervical region segment is expected to grow significantly over the forecast period, 2026 to 2033. This is driven by the rising incidence of neck pain, cervical spondylosis, disc herniation, and trauma-related injuries. Increased screen time, sedentary lifestyles, and poor posture have contributed to a higher prevalence of cervical spine disorders across both working-age and elderly populations. The cervical spine is also highly vulnerable to road traffic accidents and sports-related injuries, necessitating prompt and accurate imaging. MRI and CT scans are widely used to evaluate cervical nerve compression, spinal cord involvement, and degenerative changes. In addition, the growing adoption of minimally invasive cervical spine surgeries has increased the need for pre- and post-procedural imaging, supporting sustained growth in the cervical region segment.

Application Insights

The degenerative & pain-related disorders segment held the largest revenue share of 54.6% in 2025. The rising prevalence of spinal disorders, including herniated disc, spinal stenosis, cauda equina syndrome, and radiculopathy, is expected to drive segment growth. MRI is the preferred imaging modality for diagnosing spinal nerve compression due to it produces superior soft-tissue images. Spinal cord compression is a leading indication for spinal surgery, and this trend is increasing the demand for spinal imaging tools. According to the National Spinal Cord Injury Statistical Center (NSCISC), 2024, in the United States, the population in 2023 was approximately 335 million. Annually, traumatic spinal cord injury (tSCI) was around 54 cases per one million people. This means roughly 18,000 new cases each year, further emphasizing the critical need for accurate spinal imaging for early diagnosis, treatment planning, and surgical intervention.

The post-operative follow-up segment is projected to grow at a CAGR of 4.6% over the forecast period. This growth is driven by an increase in spinal surgeries, along with a rising prevalence of post-surgical complications. Growth is supported by a higher incidence of risk factors such as diabetes, intravenous drug use, and an aging population, which elevate the likelihood of post-operative infections and delayed healing. In the United States, vertebral osteomyelitis has an estimated incidence of approximately 4.8 cases per 100,000 people annually, underscoring the need for close post-surgical monitoring. MRI remains the primary imaging modality in post-operative assessment due to its superior soft-tissue contrast and ability to detect infections and nerve involvement. Furthermore, the demand for spinal CT is increasing in follow-up care owing to its lower cost and improved compatibility with metallic implants, supporting its growing adoption in routine post-surgical imaging.

End-use Insights

The hospital segment held the largest revenue share of 59.1% in 2025. Hospitals are well-equipped to handle a variety of medical procedures, such as spinal imaging, due to their extensive infrastructure, equipment, and expertise. Their capacity to offer comprehensive care, such as diagnosis, treatment, and rehabilitation, makes them the preferred option for patients with spinal disorders. Moreover, the increasing complexity of spinal disorders and the need for advanced imaging techniques often require the resources and capabilities of hospitals to ensure accurate diagnosis and effective treatment. In addition, the increasing number of public-private participation (PPP) programs in developing healthcare infrastructure, especially in countries such as Chile, Dubai, and Saudi Arabia, is expected to boost the segment's growth.

Diagnostic imaging centers are expected to grow significantly over the forecast period. This growth is attributed to the increasing prevalence of spinal disorders, rising healthcare expenditures, and advancements in imaging technology. Furthermore, diagnostic imaging centers provide comprehensive facilities and expertise, allowing for accurate and effective diagnosis of spinal disorders. In addition, the growing trend of outsourcing imaging services to specialized centers can contribute to their rapid growth, as healthcare providers seek to improve patient outcomes and optimize resource allocation.

Regional Insights

North America spinal imaging market held the largest market share of 53.3% in 2025, attributed to a well-established healthcare system, advanced imaging technology, supportive reimbursement policies, and a significant focus on patient well-being. The region's high rate of spinal disorders, due to factors such as an aging population and inactive lifestyles, creates a constant demand for spinal imaging services. Moreover, continuous advancements in imaging technologies strengthen North America's status as a prominent region in the spinal imaging market.

U.S. Spinal Imaging Market Trends

Spinal imaging market in the U.S. dominated with a share of 96.5% in 2025. This dominance is due to its larger population size, which drives higher demand for medical devices. Moreover, the well-developed healthcare infrastructure, advanced imaging technologies, favorable government policies, and a strong focus on patient care have contributed to its leading position. In the United States, healthcare facilities perform approximately 40 million MRI scans annually, reflecting the country’s advanced healthcare infrastructure and widespread access to diagnostic imaging, which further supports the adoption and growth of spinal imaging technologies.

Europe Spinal Imaging Market Trends

The European spinal imaging market represents a significant region in the global market. The increasing geriatric population with a high prevalence of spinal conditions, such as disc herniation and stenosis, requires a constant need for accurate diagnostic procedures. In addition, reliable healthcare systems that offer beneficial reimbursement policies guarantee patients can receive these imaging procedures. Ultimately, ongoing technological improvements, particularly in advanced MRI and CT scanners, continue to encourage healthcare providers to embrace them to enhance patient results.

The UK spinal imaging market is expected to grow rapidly in the coming years due to the increasing prevalence of spinal disorders, growing awareness, and earlier detection, leading to a higher need for these services. The UK's well-established healthcare system and favorable reimbursement policies make it an optimistic market for spinal imaging solutions.

Asia Pacific Spinal Imaging Market Trends

The Asia Pacific spinal imaging market is anticipated to grow with the fastest CAGR of 4.5% over the forecast period. The demand for advanced imaging technologies is increasing due to the demand for spinal imaging services. In addition, positive government actions include funding a growing population, rising healthcare expenditures, and greater awareness of spinal health issues. Moreover, the ever-increasing middle class in the region is also resulting in improved availability of top-notch healthcare, such as specialized healthcare infrastructure, and advocating for preventive healthcare measures aids the market expansion.

Spinal imaging market in China held a substantial market share in 2025. The growing middle class and individuals with higher disposable income in the country have led to a rise in the availability of good-quality healthcare, including specialized spinal imaging services. Moreover, government efforts to enhance healthcare infrastructure and encourage preventive care are also contributing to the market's expansion.

Key Spinal Imaging Company Insights

Some of the key companies in the spinal imaging market include GE HealthCare, Koninklijke Philips N.V., Siemens Healthineers AG, Canon Medical Systems Corporation, and others. Most companies focus on R&D activities to develop technologically advanced products to gain a competitive edge. Companies are also adopting various strategies, such as mergers and acquisitions, joint ventures, and developing low-cost equipment, especially for developing economies.

-

GE Healthcare is a global technology company focusing on medical imaging, patient monitoring, and IT solutions. It provides extensive products and services for various medical fields, such as spinal imaging. Its spinal imaging solutions, including advanced MRI and CT systems, are designed to provide high-quality images and accurate diagnoses for conditions such as herniated discs, spinal stenosis, and fractures.

-

Koninklijke Philips N.V. is a multinational healthcare technology company that provides various medical imaging solutions, including spinal imaging. Philips is recognized for its innovation and dedication to patient care, offering advanced MRI and CT systems tailored for spinal imaging.

Key Spinal Imaging Companies:

The following key companies have been profiled for this study on the spinal imaging market

- GE HealthCare

- Koninklijke Philips N.V.

- Siemens Healthineers AG

- Canon Medical Systems Corporation

- Bruker

- Mediso Ltd.

- Shimadzu Corporation

- FUJIFILM

- Hitachi, Ltd.

- Toshiba Medical Systems, Inc.

Recent Developments

-

In February 2025, Esaote Group unveiled its new portfolio of imaging solutions at the European Congress of Radiology (ECR) in Vienna, featuring AI-integrated platforms across MRI and ultrasound. The company launched “e-SPADES,” an AI-powered MRI platform that reduces examination time by up to 60% while enhancing image quality. It introduced AI-enabled C-series systems, offering portability, clinical applications, and workflow optimization.

-

In March 2024, Siemens Healthineers introduced an automated, self-driving C-arm system for intraoperative imaging in surgery. This alleviates the pressure on technologists, who used to configure these settings by hand. Moreover, the automated procedure saves time by making accurate adjustments, ultimately cutting down imaging durations.

Spinal Imaging Market Report Scope

Report Attribute

Details

Market size in 2025

USD 54.4 billion

Estimated market size in 2026

USD 56.4 billion

Projected market size by 2033

USD 73.6 billion

Growth rate

CAGR 3.9% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, trends

Segments covered

Product, spinal region, application, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; China; Japan; India; Australia; South Korea; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key company profiled

GE HealthCare; Koninklijke Philips N.V.; Siemens Healthineers AG; Canon Medical Systems Corporation; Bruker; Mediso Ltd.; Shimadzu Corporation; FUJIFILM; Hitachi Ltd.; Toshiba Medical Systems, Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Spinal Imaging Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global spinal imaging market report based on product, spinal region, application, end-use, and region:

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

X-ray

-

CT

-

MRI

-

-

Spinal Region Outlook (Revenue, USD Million, 2021 - 2033)

-

Cervical

-

Thoracic

-

Lumbar

-

Sacral

-

Whole Spinal Imaging

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Trauma & Emergency

-

Degenerative & Pain-related Disorders

-

Deformity

-

Oncology & Infection

-

Post-operative Follow up

-

Others

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospitals

-

Diagnostic Imaging Centers

-

Speciality Clinics

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

North America dominated with a 53.3% revenue share in 2025.

Key factors driving the spinal imaging market growth include rising geriatric population, growing healthcare expenditure, the advent of advanced imaging technologies, and developing healthcare reimbursement policies related to spinal imaging.

The MRI segment led with a 46.7% revenue share in 2025.

The lumbar region segment led with a 45.4% revenue share in 2025.

The degenerative & pain-related disorders segment led with a 54.6% revenue share in 2025.

Hospital segment held the largest share (over 59.0%) in 2025.

The global spinal imaging market size was valued at USD 54.4 billion in 2025 and is estimated at USD 56.4 billion for 2026.

The global spinal imaging market is expected to grow at a CAGR of 3.9% from 2026 to 2033, reaching USD 73.6 billion by 2033.

Asia Pacific is the fastest-growing region over the forecast period.

Key players include GE HealthCare; Koninklijke Philips N.V.; Siemens Healthineers AG; Canon Medical Systems Corporation; Bruker; Mediso Ltd.; Shimadzu Corporation; FUJIFILM; Hitachi Ltd.; Toshiba Medical Systems, Inc.

About the Author(s)

Medical Imaging Research Team

Healthcare · Medical ImagingThis report was authored by the medical imaging research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical imaging segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.