- Home

- »

- Plastics, Polymers & Resins

- »

-

Structural Foam Market Size And Share Report, 2026-2033GVR Report cover

![Structural Foam Market (2026 - 2033)Report]()

Structural Foam Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material (Polypropylene (PP), Polyethylene (PE), Polyurethane (PU), Polystyrene (PS), Other Materials), By Application (Electrical & Electronics, Automotive), By Region, And Segment Forecasts

Market Size, 2025

$21.5BMarket Estimate, 2026

$22.6BMarket Forecast, 2033

$32.6BCAGR, 2026–2033

5.4%Structural Foam Market Summary

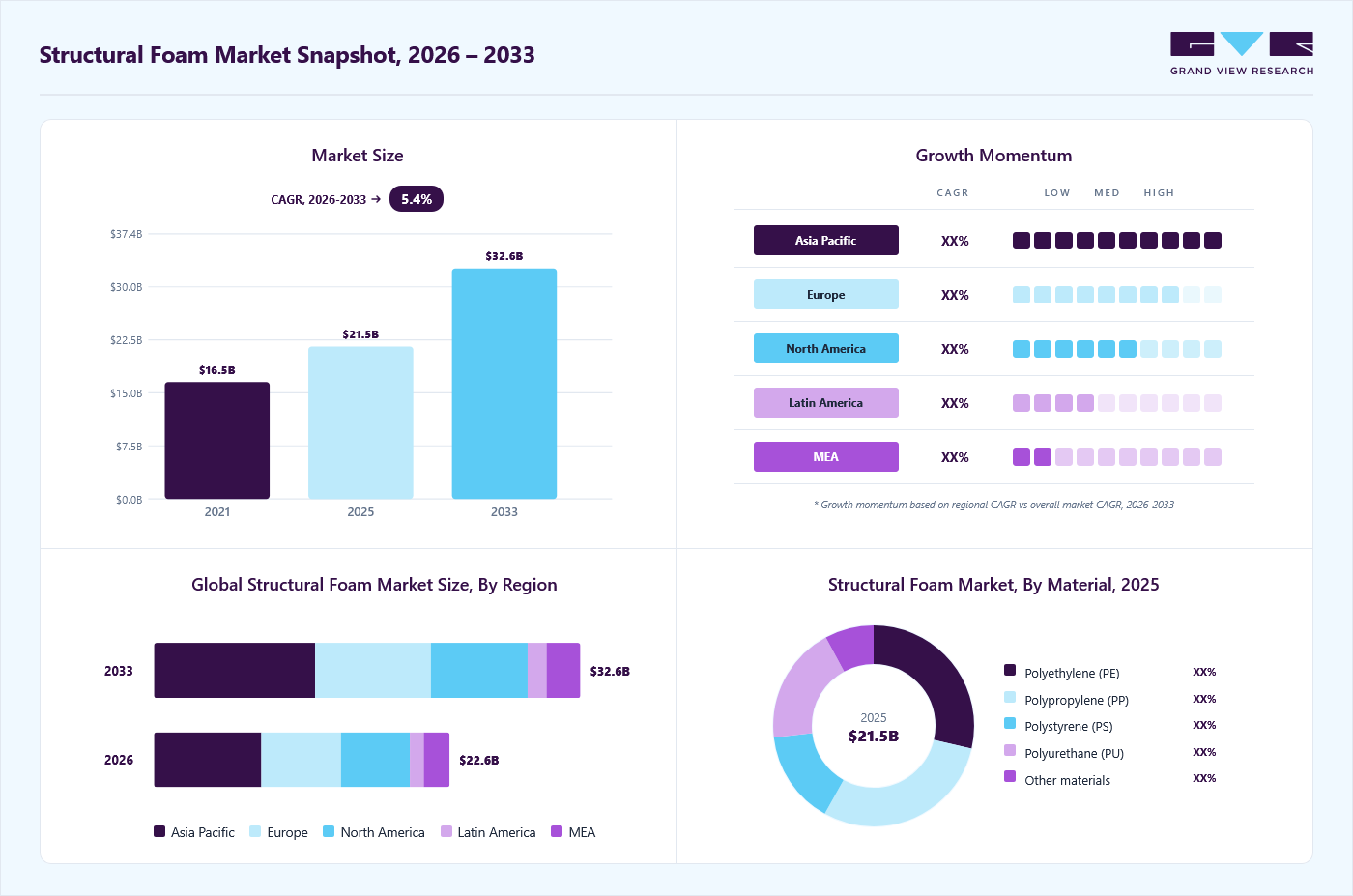

The global structural foam market size was valued at USD 21.5 billion in 2025 and is projected to grow from USD 22.6 billion in 2026 to USD 32.6 billion by 2033, at a CAGR of 5.4% from 2026 to 2033. The Asia Pacific held the largest share of 36.1% of the global market in 2025. The market is driven by increasing demand for lightweight and high-strength materials across automotive, construction, and industrial applications to improve fuel efficiency and reduce overall material usage.

Key Market Trends & Insights

- By material: Polypropylene segment held the largest market share of 29.4% in 2025.

- By application: Material handling segment held the largest market share of 33.3% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (36.1% revenue share, 2025)

- By country: China held the largest share in 2025

Market Size & Forecast

- Market size in 2025: USD 21.5 Billion

- Estimated market size in 2026: USD 22.6 Billion

- Projected market size by 2033: USD 32.6 Billion

- CAGR (2026-2033): 5.4%

It is also supported by growing emphasis on cost-effective manufacturing processes, design flexibility, and part consolidation, along with rising sustainability pressures encouraging material optimization and reduced emissions. Manufacturers are actively replacing traditional materials such as metal and solid plastics with structural foam to achieve weight reduction, improved fuel efficiency, and enhanced structural performance. This is particularly critical in the automotive sector, where stringent emission norms and the shift toward electric vehicles are accelerating the adoption of lightweight components.")

In addition, the need for cost-effective manufacturing and design flexibility is significantly contributing to market growth. Structural foam enables part consolidation, reduced tooling costs, and lower material consumption while maintaining durability and rigidity. Its ability to produce large, complex parts with minimal internal stress makes it highly suitable for applications such as pallets, enclosures, and housing components, thereby improving overall production efficiency.

Growing emphasis on sustainability and resource optimization is also positively influencing the industry outlook. Structural foam processes use less raw material compared to solid injection molding and generate lower waste, aligning with increasing environmental regulations and corporate sustainability targets. Industries are adopting these materials to reduce carbon footprint, optimize energy usage, and comply with evolving regulatory standards around plastics and emissions.

Moreover, expanding application industries, particularly construction and infrastructure development, are driving demand for durable and corrosion-resistant materials. Structural foam is widely used in outdoor furniture, building components, and industrial storage solutions due to its resistance to moisture, chemicals, and harsh environmental conditions. Rapid urbanization, coupled with rising investments in infrastructure and industrial equipment, continues to support steady growth in the market.

Market Concentration & Characteristics

A key characteristic of the structural foam industry is its innovation focused on material efficiency and process optimization rather than breakthrough technologies. Industry participants compete on the basis of lightweight performance, structural strength, durability, and cost efficiency. Technological advancements are largely centered around improved polymer blends, reinforcement techniques, and molding technologies that enable large, complex part production with reduced material usage and minimal warpage. Customization capabilities and application-specific design also play a critical role in differentiation across application sectors.

The structural foam industry is characterized by moderate innovation, with advancements focused on reinforced polymer formulations, lightweighting technologies, and improved molding processes that enable large, complex parts with reduced material usage. M&A activity remains steady, with players pursuing capacity expansions and regional acquisitions to strengthen market presence. Regulatory impact is significant, particularly due to evolving requirements around recyclability, emissions, and sustainable material usage, driving the adoption of eco-friendly foam solutions. The threat of substitutes, including metals, solid plastics, and advanced composites, remains moderate as these materials compete in high-strength and durability applications. End-user concentration is relatively high, with demand primarily driven by automotive, construction, and industrial sectors, making the market sensitive to cyclical trends in these industries.

Material Insights

The Polypropylene (PP) segment dominated the market in 2025, accounting for 29.4% supported by their favorable balance of strength, lightweight properties, and cost efficiency. These materials are widely used across automotive components, pallets, and industrial enclosures due to their excellent impact resistance, chemical stability, and ease of processing through structural foam molding. PP benefits from higher stiffness and thermal resistance, making it suitable for load-bearing applications, while PE offers superior toughness and durability for outdoor and heavy-duty uses. Their widespread availability and recyclability further strengthen their position in high-volume manufacturing applications.

The Polyethylene (PE) segment growth in the market is supported by its excellent toughness, impact resistance, and cost-effectiveness. The material is widely used across applications such as pallets, containers, outdoor furniture, and industrial components due to its superior durability, moisture resistance, and chemical stability. PE offers high flexibility and low-temperature performance, making it particularly suitable for heavy-duty and outdoor applications where resilience is critical. Its ease of processing, widespread availability, and recyclability further enhance its adoption in high-volume manufacturing and material handling applications.

Application Insights

The material handling segment dominated the market in 2025, accounting for 33.3% of total demand, driven by its extensive use in pallets, crates, containers, and bulk bins. The segment benefits from the material’s high strength-to-weight ratio, durability, and resistance to chemicals and moisture, making it ideal for logistics, warehousing, and industrial transport applications. The growth of global trade, e-commerce, and supply chain optimization has further strengthened demand for reusable and long-lasting material handling solutions.

The electrical & electronics segment is expected to grow at a CAGR of 5.6% from 2026 to 2033 in terms of revenue. The electrical & electronics segment is gaining traction due to increasing demand for durable, lightweight, and high-performance materials in electronic enclosures and components. Structural foam is widely used in switchgear housings, control panels, and electrical cabinets due to its excellent insulation properties, dimensional stability, and resistance to heat and chemicals. The growth is further supported by rising investments in industrial automation, expansion of power infrastructure, and increasing production of consumer electronics, which require reliable and cost-efficient protective solutions.

Regional Insights

Asia Pacific strucutural foam industry dominated the global market, accounting for 36.1% in 2025 of the total demand, driven by rapid industrialization, expanding construction activities, and strong growth in automotive and manufacturing sectors. The region benefits from cost-effective production, rising infrastructure investments, and increasing demand for lightweight, durable materials. In addition, the expansion of logistics and warehousing industries is supporting higher adoption of structural foam in material handling applications across key economies such as China, India, and Southeast Asia.

China strucutural foam industry is a key market within the Asia Pacific region, driven by its large-scale manufacturing base, rapid urbanization, and strong growth in construction and automotive sectors. The country’s expanding infrastructure projects and increasing demand for cost-effective, lightweight materials are accelerating the adoption of structural foam across applications such as building components, industrial equipment, and material handling. In addition, the growth of e-commerce, logistics, and warehousing industries is further supporting demand for durable pallets, containers, and storage solutions, reinforcing China’s position as a major growth engine in the regional market.

North America Structural Foam Market Trends

North America strucutural foam industry accounted for 23.4% of the global market, supported by advanced manufacturing capabilities and strong demand across automotive, construction, and material handling applications.

U.S. Structural Foam Market Trends

The U.S. strucutural foam industry plays a central role in regional growth, driven by high adoption of lightweight materials, well-established industrial infrastructure, and increasing focus on sustainable and efficient production processes. The presence of major manufacturers and continuous innovation in polymer technologies further support market expansion.

Europe Structural Foam Market Trends

Europe strucutural foam industry captured 26.9% of the global market for structural foam, characterized by stringent environmental regulations and a strong emphasis on sustainability and circular economy practices. The region is witnessing increasing adoption of recyclable and high-performance materials across automotive and construction sectors. Demand is further supported by technological advancements and the presence of established automotive manufacturers focusing on lightweight and energy-efficient solutions.

Key Structural Foam Company Insights

The competitive environment of the structural foam industry is moderately fragmented, characterized by the presence of global chemical manufacturers, specialized foam producers, and regional players. Key companies, such as Evonik Industries AG, SABIC, SEKISUI CHEMICAL CO., LTD., Carpenter Co., Tasuns Composite Technology Co., Ltd, among others, compete on the basis of material performance, cost efficiency, product customization, and manufacturing capabilities. Strategic expansions, partnerships, and investments in sustainable and recyclable materials further shape the competitive landscape.

-

In March 2026, Spur launched Hardex Performance Easy XPP, an extruded polypropylene structural foam core enabling faster, lower-temperature lamination with PP reinforcements and aluminum skins, improving strength, surface quality, and energy efficiency.

-

In February 2026, BASF introduced biomass balance grades of Autofroth polyurethane foam systems in North America, reducing carbon footprint by around 18-20% while maintaining performance and enabling easy adoption without process changes.

-

In January 2026, Covestro AG launched the CQ-Configurator, a digital tool for real-time design and sustainability assessment of polyurethane foams, helping optimize CO₂ footprint and sustainable material usage.

Key Structural Foam Companies:

The following key companies have been profiled for this study on the structural foam market.

- Evonik Industries AG

- SABIC

- SEKISUI CHEMICAL CO., LTD.

- Carpenter Co.

- Tasuns Composite Technology Co.,Ltd

- ALSTONE INDUSTRIES PVT. LTD.

- Covestro AG

- MEGAFLEX Schaumstoff GmbH

- Arnon Plastic Industries Co. Ltd

- BASF

- ARMACELL

Structural Foam Market Report Scope

Report Attribute

Details

Market size in 2025

USD 21.5 billion

Estimated market size in 2026

USD 22.6 billion

Projected market size by 2033

USD 32.6 billion

Growth rate

CAGR of 5.4% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million, Volume in Kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue & volume forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material, application, region

Regional Scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country Scope

U.S.; Canada; Mexico; Germany; France; UK; Italy; Spain; Russia; Denmark; Sweden; Norway; China; India; Japan; South Korea; Australia; Indonesia; Vietnam; Brazil; Argentina; Saudi Arabia; UAE; South Africa; Kuwait

Key companies profiled

Evonik Industries AG; SABIC; SEKISUI CHEMICAL CO., LTD.; Carpenter Co.; Tasuns Composite Technology Co.,Ltd; ALSTONE INDUSTRIES PVT. LTD.; Covestro AG; MEGAFLEX Schaumstoff GmbH; Arnon Plastic Industries Co. Ltd; BASF; ARMACELL

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail of customized purchase options to meet your exact research needs. Explore purchase options

Global Structural Foam Market Report Segmentation

This report forecasts revenue growth at the regional and country levels and provides an analysis on the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the structural foam market report based on material, application, and region:

-

Material Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Polypropylene (PP)

-

Polyethylene (PE)

-

Polyurethane (PU)

-

Polystyrene (PS)

-

Other materials

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Material Handling

-

Building & Construction

-

Automotive

-

Electrical & Electronics

-

Other applications

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

Russia

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

Indonesia

-

Vietnam

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

Kuwait

-

-

Frequently Asked Questions About This Report

Key factors that are driving the market growth include structural foam are considerably lighter than other solid plastics and exhibit better weight to strength ratio.

The global structural foam market size was estimated at USD 21.5 billion in 2025 and is expected to reach USD 22.6 billion in 2026.

The global structural foam market is expected to grow at a compound annual growth rate of 5.4% from 2026 to 2033 to reach USD 32.6 billion by 2033.

Asia Pacific dominated with a 36.1% revenue share in 2025.

The material handling segment led with a 33.3% revenue share in 2025, while the electrical & electronics segment is expected to grow at a CAGR of 5.6% from 2026 to 2033.

The polypropylene segment dominated the structural foam market with a share of 29.4% in 2025, supported by its favorable balance of strength, lightweight properties, and cost efficiency. These materials are widely used across automotive components, pallets, and industrial enclosures due to their excellent impact resistance, chemical stability, and ease of processing through structural foam molding.

Some key players operating in the structural foam market include Evonik Industries AG, SABIC, SEKISUI CHEMICAL CO., LTD., Carpenter Co., Tasuns Composite Technology Co., Ltd, ALSTONE INDUSTRIES PVT. LTD., Covestro AG, MEGAFLEX Schaumstoff GmbH, Arnon Plastic Industries Co. Ltd, BASF, and ARMACELL, among others.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.