- Home

- »

- HVAC & Construction

- »

-

Submarine Cables Market Size & Share Report, 2026-2033GVR Report cover

![Submarine Cables Market Size, Share & Trends Report]()

Submarine Cables Market (2026 - 2033) Size, Share & Trends Analysis Report By Application (Submarine Power Cables, Submarine Communication Cables), By Voltage (Medium Voltage, High Voltage), By End-use, By Component, By Offerings, By Region, And Segment Forecasts

Market Size, 2025

$33.8BMarket Estimate, 2026

$35.8BMarket Forecast, 2033

$50.6BCAGR, 2026–2033

5.0%Submarine Cables Market Summary

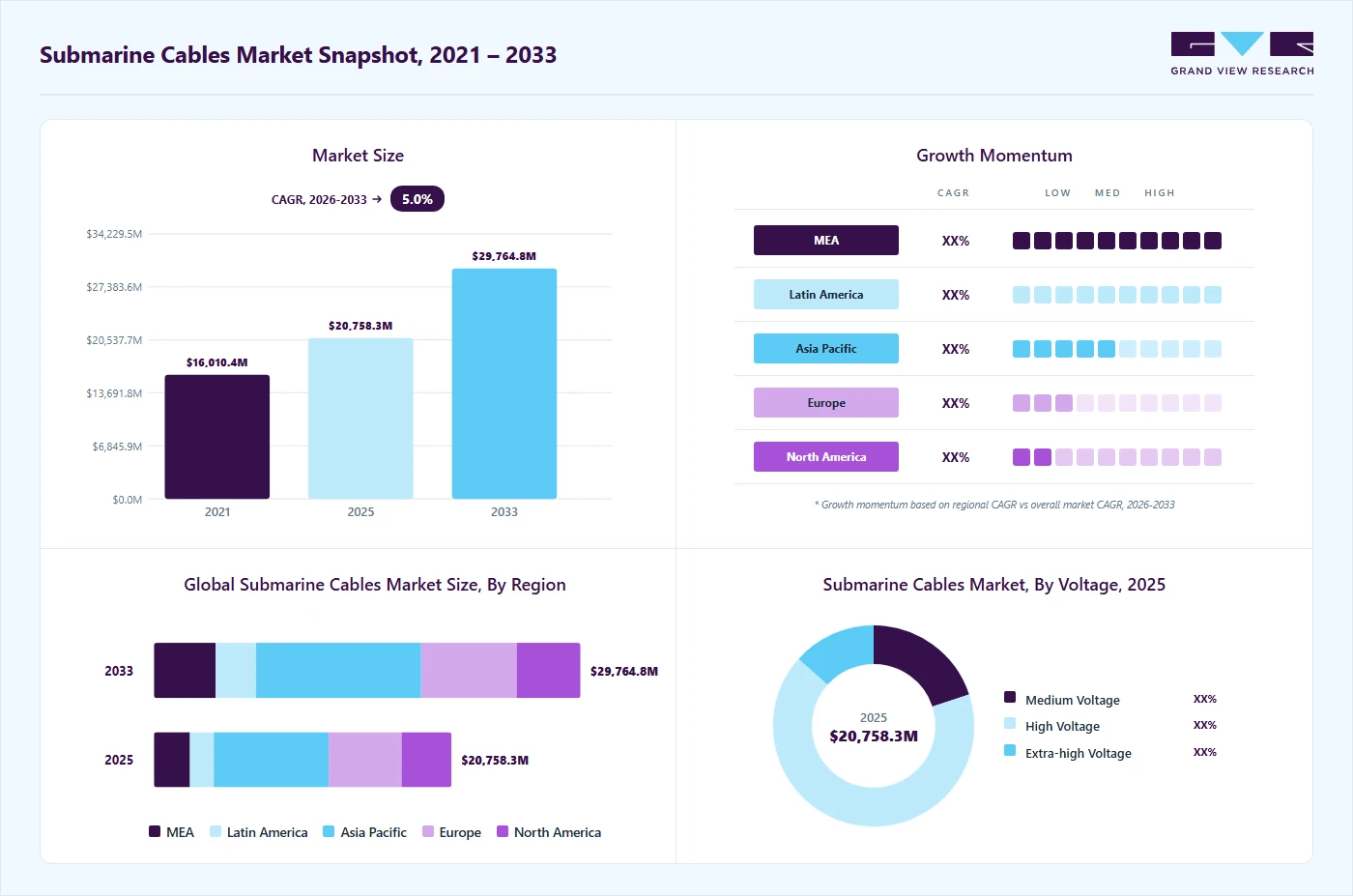

The global submarine cables market size was valued at USD 33.8 billion in 2025 and is projected to grow from USD 35.8 billion in 2026 to USD 50.6 billion by 2033, at a CAGR of 5.0% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 38.7% in 2025. The major factors driving the market are increasing investments in offshore wind farms, increasing data traffic, and investments by OTT providers to satisfy the requirements.

Key Market Trends & Insights

- By voltage: High voltage segment held the largest market share of 66.6% in 2025.

- By application: Submarine power cables segment held the largest market share of 61.5% in 2025.

- By component: Dry plant products segment held the largest market share in 2025.

- By end use: Offshore wind power generation segment held the largest market share in 2025.

- By offerings: Installation & commissioning segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (38.7% revenue share, 2025)

- By country: The China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 33.8 Billion

- Estimated market size in 2026: USD 35.8 Billion

- Projected market size by 2033: USD 50.6 Billion

- CAGR (2026-2033): 5.0%

Submarine cables are widely used for power and communication applications. The communication cables have observed a surge in demand due to increased data traffic. Regions such as Europe, the Middle East, Asia Pacific, and Latin America have noted rising investments in submarine communication cables. Companies such as Google, Facebook, Amazon, and Microsoft are the primary influencers of the submarine cables. Google owns 10,433 miles of submarine cables internationally and 63,605 miles in consortium with Facebook, Amazon, and Microsoft. Facebook owns 57,709 miles of submarine cables, Amazon owns 18,987 miles, and Microsoft owns 4,104 miles. Amazon’s cables run from the U.S. to the Asia Pacific region, connecting Singapore, Japan, California, and Oregon.")

Growing demand has led the manufacturers to actively participate in the Installation & Commissioning, upgrades, and maintenance of the submarine cables. For instance, in January 2024, NEC Corporation announced the successful completion of a submarine cable system connecting Kochi and the Lakshadweep Islands in India. Spanning approximately 1,870 kilometers, the system offers an initial capacity of 2x100 Gbps, expandable up to 1,600 GBPS per fiber pair. This project, executed under the Government of India’s ‘Digital India’ Mission, aims to enhance digital connectivity and socio-economic development in the region.

Market Dynamics

The submarine cable industry is being driven by the rapid increase in global internet traffic, cloud computing adoption, video streaming, social media usage, and international enterprise connectivity. The growing demand for low-latency, high-bandwidth communication across continents is prompting telecom operators, hyperscale cloud companies, and governments to invest heavily in advanced submarine fiber-optic cable systems.

The expansion of hyperscale data centers, 5G infrastructure, AI workloads, and cross-border digital services is further accelerating the deployment of new subsea cable routes across the Transatlantic, Transpacific, Indian Ocean, and Americas regions. In addition, rising internet penetration and digital transformation initiatives across emerging economies are significantly driving market growth.

Despite strong growth potential, the global market faces several challenges, including high deployment costs, complex maintenance, and operational risks.Establishing submarine cable networks requires substantial investment in cable manufacturing, marine surveys, installation ships, landing stations, and networkintegration infrastructure. Maintenance and repair operations are expensive and time-consuming, particularly in deep-sea environments and remote ocean regions.

Furthermore, submarine cables are vulnerable to damage from fishing activities, ship anchors, earthquakes, underwater landslides, and adverse marine conditions, leading to major connectivity disruptions. In addition, geopolitical tensions, regulatory approvals, and international permitting requirements continue to create deployment and operational challenges for market participants.

The growing expansion of AI-driven applications, hyperscale cloud infrastructure, and international digital connectivity projects is creating significant opportunities in the submarine cable industry. Increasing investments by major technology companies and telecom providers in high-capacity next-generation fiber-optic systems are enabling faster, more reliable global data transmission.

Emerging economies across Asia, Africa, the Middle East, and Latin America are witnessing rising demand for broadband connectivity and for modernizing digital infrastructure, which is encouraging the development of new subsea cable routes. Moreover, advancements in optical transmission technologies, space-division multiplexing, and energy-efficient cable systems are expected to improve network performance, scalability, and operational efficiency, supporting long-term market expansion.

Market Concentration & Characteristics

The submarine cable industry is moderately consolidated, with competition dominated by a limited number of globally established manufacturers and marine installation specialists, alongside several regional and niche technology providers.

The market is led by major companies such as SubCom, ASN (Alcatel Submarine Networks), NEC Corporation, Prysmian Group, Nexans, and HMN Technologies. These companies hold strong competitive positions due to their advanced manufacturing capabilities, specialized cable-laying fleets, long-standing relationships with telecom operators and hyperscale cloud providers, and proven expertise in executing large-scale transoceanic projects.

Although the market includes regional suppliers and engineering firms offering repeater technologies, branching units, and maintenance services, the high capital requirements, stringent technical standards, complex regulatory approvals, and limited availability of specialized installation vessels create substantial barriers to entry. As a result, a relatively small group of companies accounts for a significant share of global submarine cable deployments.

Application Insights

The submarine power cable segment led the market with the largest revenue share of 61.7% in 2025. Increased demand for inter-country and island connections, along with new capacity expansions in the offshore wind industry, are driving the submarine cable industry. Furthermore, the growing number of offshore wind farms and the electrification of offshore oil and gas networks have driven research and development, further increasing the demand for submarine power cables. The application of submarine power cables is rapidly expanding within the broader global market, driven by the global shift towards renewable energy and cross-border electricity interconnections. These high-voltage cables are critical for transmitting power from offshore wind farms and linking national power grids across seas. As countries invest heavily in decarbonization and energy security, the demand for reliable, long-distance power transmission solutions is rising. This trend is encouraging manufacturers to scale up production capacity and invest in advanced technologies for deep-sea and high-voltage cable systems.

The submarine communication cables segment is expected to grow at the fastest CAGR over the forecast period. There has been a rapid increase in urbanization and economic activities, which will drive the growth in infrastructure and construction segments in both developing and developed countries. The demand from sectors such as the commercial, telecom, energy, and power industries is driving infrastructure expansion and upgradation, which is anticipated to drive demand for the submarine cable industry. Also, the rising focus on joining offshore renewable energy generation to meet future renewable energy targets and increase energy security, providing energy access to remote landmasses, and interlinking national grids to economize energy use has driven the market expansion across the globe.

Voltage Insights

The high voltage segment accounted for the largest market revenue share in 2025. High-voltage cables ranging above 33kV are widely used for the transmission and distribution of power. Thus, the increasing demand for the HVDC submarine power cables and rising investments in offshore wind power generation is the primary factors driving the high voltage cables segment in the global market. In addition, high voltage cables reduce the transmission losses and thus allow efficient power transmission. The HVDC power system is evolving at high speed and permitting the transfer of electricity from the high-capacity high-power sources to the mainland. Several companies and development centers support the growth of HVDC power systems, including DESERTEC, the North Seas Countries Offshore Grid Initiative, and CIGRE.

The medium voltage cables segment is anticipated to exhibit at the fastest CAGR over the forecast period. The growth is attributable to the utilization of MV cables in the offshore oil & gas infrastructure for power transmission. The demand from overseas oil & gas operations has been increasing, thus driving the MV market. The growth is driven by the expansion of offshore renewable energy projects, particularly wind farms and tidal energy systems. These cables play a crucial role in transmitting power between offshore platforms and onshore grids or between different sections of offshore infrastructure. In addition, increased investment in inter-island and coastal connectivity is driving their adoption. The trend toward grid modernization and energy decentralization further supports sustained growth in this segment.

End-use Insights

The offshore wind power generation segment accounted for the largest market revenue share in 2025. Increasing investments in offshore wind power generation and usage of submarine power cables for long-distance power transmissions from these plants are the primary factors in driving the market growth. For instance, in June 2024, The Global Wind Energy Council (GWEC) reports that 2023 marked a significant year for offshore wind energy, with 10.8 GW of new capacity installed, a 24% increase from the previous year globally, bringing the total to 75.2 GW. This growth is attributed to favorable policy developments and increased collaboration between governments and industry stakeholders. GWEC forecasts an addition of 410 GW of offshore wind capacity over the next decade, aligning with global targets to install 380 GW by 2030.

The inter-country & island connection segment is anticipated to exhibit at the fastest CAGR over the forecast period. The growing need for inter-country and island connectivity is a key driver of the market growth, as nations seek to improve communication infrastructure and ensure reliable power transmission. Remote islands and geographically dispersed countries rely on submarine cables to bridge gaps in internet and electricity access, supporting economic development and digital inclusion. Regional integration initiatives and cross-border energy projects are further accelerating investments in both telecom and power submarine cable systems. This demand is pushing governments and private players to prioritize long-term, high-capacity cable installations across oceans and seas.

Component Insight

The dry plant products segment accounted for the largest market revenue share in 2025. The growth is driven by the increasing adoption of dry plant products such as power feeding equipment, monitoring systems, and transmission terminals in submarine communication cables. These components enhance network reliability, simplify maintenance, and reduce overall operational costs by enabling better onshore cable management. As demand for high-speed, low-latency global data transmission grows, dry plant technologies are becoming essential for supporting advanced cable systems. Their integration ensures seamless signal transmission and efficient management, making them a critical investment for operators expanding international communication networks.

The wet plant products segment is expected to expand at the fastest CAGR over the forecast period. Wet plant products, such as optical repeaters, branching units, and undersea fiber-optic cables, are crucial drivers of market growth. These components are directly deployed on the seabed and are vital for signal amplification, routing, and long-distance transmission. With increasing global demand for high-capacity, transoceanic connectivity, the need for robust, high-performance wet plant systems is growing. Advancements in wet plant technologies are enabling longer cable spans, higher data throughput, and improved fault tolerance, making them indispensable to the expansion of modern submarine communication infrastructure.

Application Insights

The Installation & Commissioning segment accounted for the largest market revenue share in 2025. Installation & Commissioning (I&C) offerings are driving the market by enabling faster deployment, ensuring technical reliability, and supporting complex system upgrades. As global data demand grows, I&C services provide end-to-end solutions from marine surveys to final system testing, crucial for timely and secure cable installations. Their role in large-scale connectivity projects and compliance assurance makes them vital to both new builds and modernization efforts. This specialized support is essential as more high-capacity systems are deployed across increasingly challenging environments.

The upgrade segment is expected to grow at the fastest CAGR over the forecast period. In the submarine communication cable market, upgrade offerings primarily focus on enhancing existing cable systems with advanced technologies such as coherent optical transmission and higher-capacity repeaters. These upgrades significantly extend the lifespan and data throughput of older systems without the need for full replacements, offering cost efficiency and faster deployment. Demand is driven by skyrocketing global data traffic and cloud services, pushing operators to maximize existing infrastructure. Vendors such as Ciena, Infinera, and Nokia are leading this space, offering scalable solutions that boost performance while minimizing operational disruptions.

Regional Insights

Asia Pacific dominated the global submarine cables market with the largest revenue share of 38.7% in 2025, driven by surging internet demand, fueled by rapid digitalization, mobile usage, and cloud adoption across emerging economies. Increasing investments from hyper-scalers like Google, Meta, and AWS are also accelerating infrastructure expansion to support data-intensive applications. In addition, the region's strategic position as a global data transit hub between the U.S., Europe, and Africa enhances its importance. Government initiatives promoting digital connectivity and public-private partnerships further support new cable projects.

China Submarine Cables Market Trends

China accounted for over 50.0% market share of the Asia Pacific submarine cables market in 2025, driven by rapidly increasing internet traffic, strong cloud computing adoption, and expanding hyperscale data center infrastructure. Rising demand for high-speed international connectivity to support AI applications, 5G deployment, video streaming, and digital commerce is accelerating investments in advanced submarine cable networks. The country’s growing role in global digital trade and cross-border data transmission is further strengthening demand for new subsea cable routes connecting Asia with North America, Europe, and other regional markets. In addition, government initiatives focused on digital infrastructure development, smart city expansion, and technological self-reliance are supporting long-term growth in the submarine communication cable market.

North America Submarine Cables Market Trends

The submarine cables market in North America is anticipated to grow at a significant CAGR during the forecast period. The region is experiencing rapid growth in submarine cable expansion driven by rising demand for high-speed, low-latency data transmission for cloud services, streaming platforms, and AI workloads. Strategic routes now connect the U.S. to Latin America, Europe, and the Asia-Pacific with increased capacity and redundancy. Regulatory support and public-private partnerships are accelerating deployment. In addition, emerging cable landing stations along the U.S. coasts are boosting regional digital infrastructure and economic activity.

The submarine cables market in the U.S. is accelerating as demand for high-capacity data transmission surges, fueled by the expansion of AI, cloud services, and global internet usage in this region. Key tech players such as Google, Meta, Amazon, and Microsoft are heavily investing in new transoceanic cable systems to strengthen international data connectivity and reduce latency. These cables are critical infrastructure for supporting data centers, content delivery networks, and emerging digital services. The U.S. is also becoming a key hub for intercontinental data traffic, reinforcing its role in the global digital economy.

Europe Submarine Cable Market Trends

The submarine cable market in Europe is driven by its geopolitical focus on digital autonomy and reducing reliance on non-EU data routes. Unlike North America’s transpacific focus, Europe is expanding connectivity with Africa, the Middle East, and Asia via the Mediterranean. Initiatives like the EU’s Global Gateway are funding infrastructure to enhance international digital links. Coastal nations such as France, Spain, and Greece are emerging as key landing points due to their geographic and political stability. Europe is also emphasizing green data transmission, integrating cable projects with renewable energy goals.

Key Submarine Cables Company Insights

The key players that dominated the global submarine cable industry include Alcatel-Lucent, TE SubCom, and NEC Corporation. The other small and mid-size submarine cable providers focus on smaller projects in various regions. Many submarine cable suppliers are also involved in offshore oil and gas projects, undersea electrical cables, and other marine infrastructure projects across the globe.

Further, the leading players are also focusing on strategic acquisitions and collaborations with regional players to expand their channel reach in untapped markets. For instance, in April 2023, Nexans acquired Reka Cables, a Finnish cable manufacturer. The combined business aimed to provide safe and high-quality cables to Nordic customers and beyond through this acquisition.

-

NEC Corporation is a prominent global player in the submarine cable industry, having deployed over 400,000 kilometers of undersea cables worldwide. The company offers end-to-end solutions, from cable manufacturing to marine installations and long-term maintenance, making it a preferred partner for global connectivity projects. NEC has been instrumental in major international cable systems like the Asia Direct Cable (ADC) and the India-Lakshadweep project, enhancing digital infrastructure across Asia. Its cables are engineered to withstand extreme oceanic conditions, supporting robust data transmission across continents. As global demand for high-speed, high-capacity networks rises, NEC continues to expand its presence in key markets, facilitating digital transformation and economic growth.

-

Microsoft Corporation is a global technology provider specializing in software, cloud services, and digital infrastructure. To support its expansive cloud offerings, including Azure and Microsoft 365, Microsoft has invested heavily in submarine cable systems to enhance global data connectivity. Notably, Microsoft co-developed the MAREA cable with Meta and Telxius-a 6,600 km transatlantic system connecting Virginia, USA, to Bilbao, Spain, designed to deliver ultra-high capacity and low-latency connectivity across the Atlantic. Additionally, Microsoft participates in the Amitié cable consortium, linking the U.S. to the UK and France, further strengthening its transatlantic infrastructure. These investments ensure faster, more reliable access to Microsoft's cloud services worldwide.

Key Submarine Cables Companies:

The following key companies have been profiled for this study on the submarine cables market.

-

ALE International,

-

SubCom, LLC

-

NEC Corporation

-

Prysmian S.p.A

-

Nexans

-

Google LLC

-

Amazon.com, Inc.

-

Microsoft

-

NKT A/S

-

ZTT

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: SubCom; NEC Corporation; Prysmian S.p.A.; Nexans; Microsoft

- Strengthen submarine cable capabilities through strategic partnerships, consortium participation, and investments in advanced subsea connectivity solutions.

- Invest in high-capacity fiber optic cables, repeaters, branching units, and specialized cable-laying vessels to support long-distance, low-latency international data transmission.

- Extensive global presence, strong relationships with telecom operators, hyperscale cloud providers, and government agencies

- Ability to design and deploy high-capacity, long-distance submarine cable systems with reliable low-latency connectivity strengthens competitive differentiation.

- Dependence on complex manufacturing facilities, specialized installation vessels, and established supply chains can slow the adoption of next-generation submarine cable technologies.

- Large organizational structures and lengthy project execution cycles may reduce operational agility and delay the deployment of innovative subsea connectivity solutions.

Emerging Players: ALE International; ZTT

- Develop specialized and cost-effective submarine cable solutions for niche applications such as regional connectivity, offshore energy projects, and island network deployments.

- Emphasize agility, customization, and rapid project execution to address evolving requirements for high-capacity, low-latency international data transmission

- Faster development cycles enable rapid adoption of advanced submarine cable technologies, including high-capacity fiber pairs, open cable architectures, and enhanced repeater systems.

- Flexible and customer-focused approaches help differentiate solutions in niche segments such as regional connectivity projects, offshore energy networks, and customized subsea infrastructure deployments.

- Limited financial resources and a smaller market presence can restrict participation in large-scale submarine cable projects and global infrastructure expansion.

- Lower brand recognition and a narrower customer base may hinder market penetration

Recent Developments

-

In January 2025, Microsoft filed plans for three subsea cables-Tuskar, SOBR1, and SOBR2 connecting Ireland to Wales to boost data center connectivity. These cables will connect key sites in Ireland and the UK, enhancing the speed and reliability of cloud services. This move supports Microsoft’s expanding data center footprint in Dublin and new developments in Wales. The project aligns with Microsoft’s global strategy to improve digital infrastructure and cloud performance. These filings highlight Microsoft’s commitment to strengthening trans-Irish Sea connectivity.

-

In November 2025, Google revealed Dhivaru, a subsea cable system spanning the Trans-Indian Ocean and linking the Maldives, Christmas Island, and Oman under the Australia Connect program. The initiative incorporates connectivity hubs in the Maldives and Christmas Island that offer cable switching to enable automatic traffic rerouting, content caching to minimize latency, and colocation facilities for regional carriers.

Submarine Cable Market Report Scope

Report Attribute

Details

Market size in 2025

USD 33.8 billion

Estimated market size in 2026

USD 35.8 billion

Projected market size by 2033

USD 50.6 billion

Growth rate

CAGR of 5.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Application, voltage, end-use, component, applications, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; India; Japan; Australia; South Korea; Brazil; UAE; South Africa; KSA

Key companies profiled

ALE International; SubCom, LLC; NEC Corporation; Prysmian S.p.A; Nexans; Google LLC; Amazon.com, Inc.; Microsoft; NKT A/S; ZTT.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Submarine Cables Market Report Segmentation

This report forecasts revenue growth at global, regional & country levels and provides an analysis of the industry trends in each of the sub-segments from 2026 to 2033. For this study, Grand View Research has segmented the global submarine cables market report based on the application, voltage, end use, offerings, component, and region:

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Submarine Power Cables

-

Submarine Communication Cables

-

-

Submarine Power Cables Voltage Outlook (Revenue, USD Billion, 2021 - 2033)

-

Medium Voltage

-

High Voltage

-

Extra High Voltage

-

-

Submarine Power Cables End-use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Offshore Wind Power Generation

-

Array Cables

-

Export Cables

-

-

Inter country & island connection

-

Offshore Oil & Gas

-

-

Submarine Communication Cables Applications Outlook (Revenue, USD Billion, 2021 - 2033)

-

Installation & Commissioning

-

Upgrade

-

Maintenance

-

-

Submarine Communication Cables Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Dry Plant Products

-

Wet Plant Products

-

-

Submarine Power Cables Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Submarine Cable Market Growth Strategy for Network Operators, Cloud Providers, and Infrastructure Developers

Conducted a comprehensive assessment of current and projected demand for submarine cable systems across international telecommunications networks

Benchmarked leading submarine cable manufacturers, system integrators, and installation providers based on technology capabilities, project execution models, and commercial pricing structures.

Identified high-growth application areas and strategic investment priorities across global subsea connectivity corridors.

Submarine Cable Market Entry and Expansion Strategy for Cable Manufacturers, Equipment Suppliers, and Technology Providers

Analyzed regional deployment trends across Asia-Pacific, North America, Europe, the Middle East, Africa, and Latin America, with a focus on new intercontinental and regional cable projects.

Assessed customer procurement criteria, preferred contracting models, and technical specifications for submarine cable systems and related equipment.

Supported product positioning, pricing strategies, and channel partnership development to strengthen competitive advantage.

Submarine Cable Investment Opportunity Assessment for Telecom Operators, Institutional Investors, and Government Agencies

Evaluated investment trends in submarine cable infrastructure, including consortium-led projects, privately funded hyperscale routes, and national connectivity programs.

Reviewed regulatory frameworks, permitting requirements, and geopolitical considerations affecting route selection and project execution.

Supported due diligence, strategic planning, and partnership evaluation for large-scale subsea infrastructure projects

Frequently Asked Questions About This Report

The global submarine cables market size was valued at USD 33.8 billion in 2025 and is estimated at USD 35.8 billion for 2026.

The global submarine cables market is expected to grow at a CAGR of 5.0% from 2026 to 2033, reaching USD 50.6 billion.

Key factors include increasing investments in offshore wind farms, increasing data traffic, and investments by OTT providers to satisfy the requirements. Submarine cables are widely used for power and communication applications.

Submarine power cables led with a 61.5% revenue share in 2025, while submarine communication cables is the fastest-growing application.

The high voltage segment held the largest share (over 66.0%) in 2025, while medium voltage cables is the fastest-growing segment.

Offshore wind power generation held the largest revenue share in 2025, while inter-country & island connection is the fastest-growing segment.

The dry plant products held the largest share in 2025, while wet plant products is the fastest-growing component.

Installation & commissioning led market in 2025, while upgrade is the fastest-growing segment.

Key players include ALE International; SubCom, LLC; NEC Corporation; Prysmian S.p.A; Nexans; Google LLC; Amazon.com, Inc.; Microsoft; NKT A/S; ZTT.

Asia Pacific dominated with a 38.7% revenue share in 2025.

About the Author(s)

HVAC & Construction Research Team

Technology · HVAC & ConstructionThis report was authored by the hvac & construction research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the hvac & construction segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.