- Home

- »

- Next Generation Technologies

- »

-

Telecom Managed Services Market Size Report, 2026-2033GVR Report cover

![Telecom Managed Services Market (2026 - 2033)Report]()

Telecom Managed Services Market (2026 - 2033)

Size, Share & Trends Analysis Report By Service Type (Managed Data Center Services, Managed Security Services), By Deployment (On-premise, Cloud), By Enterprise Size, By Region, And Segment Forecasts

Market Size, 2025

$28.6BMarket Estimate, 2026

$32.3BMarket Forecast, 2033

$89.9BCAGR, 2026–2033

15.8%Telecom Managed Services Market Summary

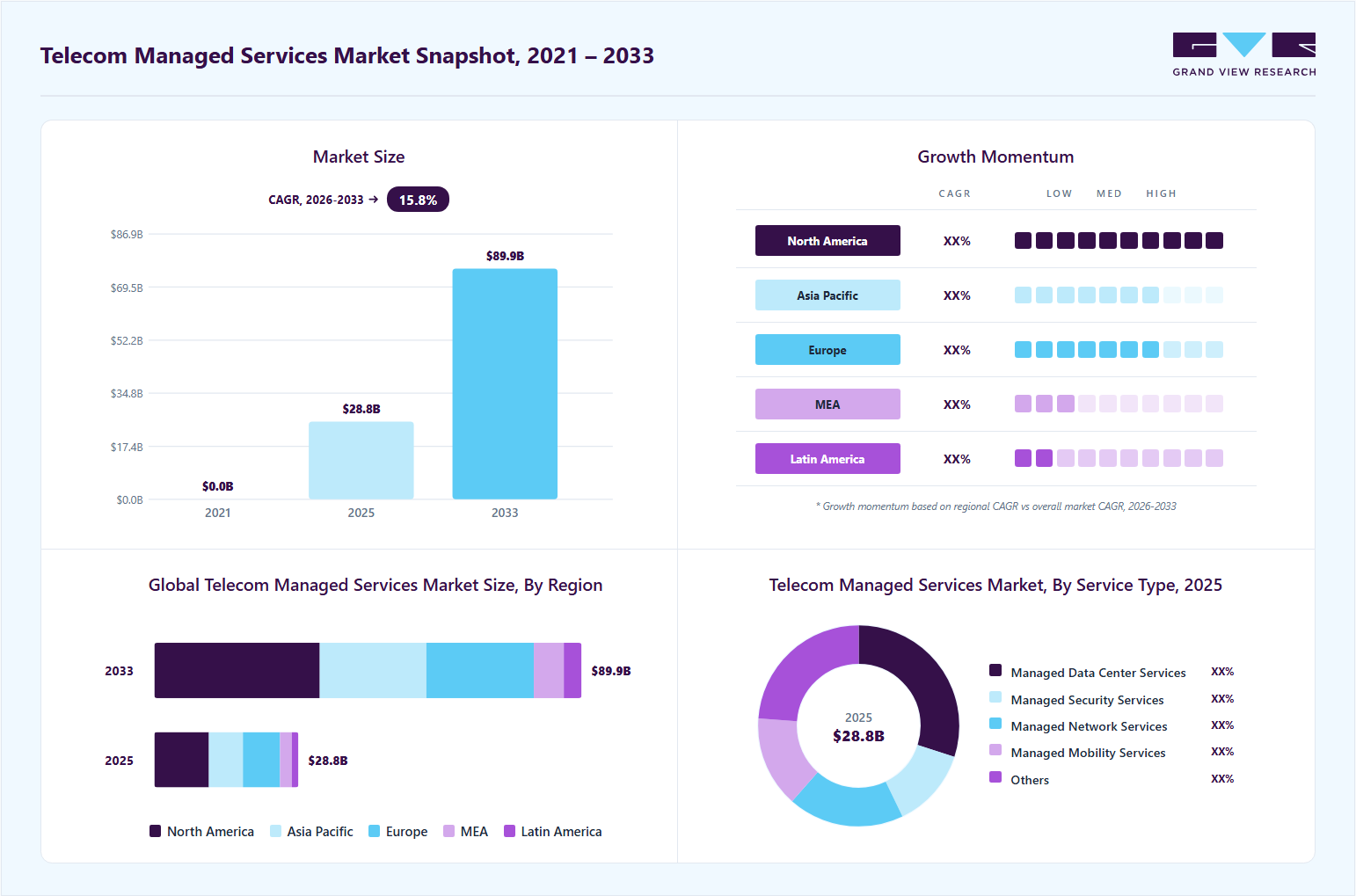

The global telecom managed services market size was valued at USD 28.6 billion in 2025 and is projected to grow from USD 32.3 billion in 2026 to USD 89.9 billion by 2033, at a CAGR of 15.8% from 2026 to 2033. The North America dominated the global market with a revenue share of 38.0% in 2025. The ability of telecom managed services to improve efficiency and cost-effectiveness and to cater to the industry's evolving needs of the industry, is contributing to the market growth.

Key Market Trends & Insights

- By service type: The managed data center services segment led the market with the largest revenue share of 30.0% in 2025.

- By deployment: The cloud segment accounted for the largest market revenue share in 2025.

- By enterprise size: The large enterprises segment accounted for the largest market revenue share in 2025.

Regional Highlights

- Largest regional market: North America (38.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By Country: The U.S. accounted for the largest market revenue share in North America in 2025.

Market Size & Forecast

- Market size in 2025: USD 28.6 billion

- Estimated market size in 2026: USD 32.3 billion

- Projected market size by 2033: USD 89.9 billion

- CAGR (2026-2033): 15.8%

These services encompass a wide range of solutions, including network management, security, cloud computing, and customer support, all designed to ensure seamless, uninterrupted communication for businesses and individuals. The integration of advanced technologies, such as AI-driven automation, has further accelerated this growth, enhancing service quality while reducing operational complexities.")

Telecom companies are increasingly adopting AI-based innovations discreetly, supporting a steady upward trajectory in telecom managed services and enabling enhanced connectivity and improved customer satisfaction without compromising data privacy or security. The expansion of 5G technology is further driving the evolution of managed services to address the growing need for ultra-fast, reliable connectivity. At the same time, the integration of edge computing is enabling data processing closer to the network edge, significantly reducing latency and unlocking new opportunities for IoT applications. Security remains a critical priority, prompting the deployment of advanced cybersecurity solutions within managed services to mitigate evolving cyber threats effectively.

A rise in the usage of cloud computing is anticipated to have a profound impact on the market growth. Cloud computing offers significant advantages to telecom providers, enabling them to optimize resources, scale operations efficiently, and offer a diverse range of services. By leveraging cloud-based solutions, telecom companies can streamline network management processes, improve service delivery, and reduce downtime. In addition, cloud computing enables rapid deployment of new services and applications, accelerating time-to-market and enhancing the overall customer experience. As the demand for cloud-based services continues to surge, managed telecom services are poised to play a pivotal role in assisting businesses in navigating the complexities of cloud adoption, ensuring seamless integration, robust security, and reliable performance.

Cost minimization in managing enterprise infrastructure is expected to play a significant role in driving the market growth. Businesses seeking to optimize operations and reduce expenses are increasingly relying on managed service providers to address complex telecom infrastructure requirements. Outsourcing network management, security, and support to specialized providers enables enterprises to benefit from economies of scale and access advanced technologies without incurring substantial capital investments. Flexible pricing models further enhance the appeal of managed telecom services, enabling organizations to pay only for the services they use and thereby avoid unnecessary costs.

Market Dynamics

The rapid deployment of 5G networks is driving the growth of the telecom managed services industry. Telecom operators are facing increasing pressure to deliver high-speed, low-latency connectivity while managing highly complex, capital-intensive infrastructure. The transition from legacy networks to advanced 5G architectures involves dense network deployments, spectrum management, and continuous performance optimization, which can be challenging to handle internally.

Managed service providers play a critical role in addressing these challenges by offering end-to-end support across network planning, deployment, monitoring, and optimization. Their expertise and specialized tools enable telecom companies to accelerate 5G rollouts while maintaining service quality and operational efficiency. By outsourcing these functions, operators can reduce operational burdens and redirect their focus to strategic initiatives such as innovation, customer experience enhancement, and new service development, ensuring scalable, seamless performance in evolving 5G ecosystems.

The loss of operational control and increased dependence on third-party managed service providers are restraining the market's growth. Telecom companies often express concerns regarding reduced visibility into critical network operations when these functions are outsourced. This limited control can affect decision-making agility, particularly in situations that require rapid responses to network disruptions or performance issues.

In addition, the risk of vendor lock-in, where telecom operators become heavily reliant on a single service provider, also restrains the growth of the market. Transitioning to an alternative vendor can be complex, time-consuming, and costly due to integration challenges and contractual obligations. Such dependency reduces operational flexibility and may hinder the ability of telecom companies to quickly adapt to evolving market demands, technological advancements, or strategic shifts.

The rapid proliferation of Internet of Things (IoT) devices and the expansion of connected ecosystems across industries such as smart cities, manufacturing, healthcare, and consumer applications present an opportunity for the market. The increasing number of connected devices generates vast amounts of data, requiring advanced network management, continuous monitoring, and efficient data processing. Telecom operators are increasingly relying on managed service providers to handle the complexity of these large-scale, distributed networks, ensuring seamless connectivity, low latency, and real-time data insights. This growing reliance on specialized expertise enhances network performance and operational efficiency, enabling telecom companies to unlock new revenue streams through value-added services, long-term contracts, and innovative IoT-driven business models.

Market Concentration & Characterstics

The telecom managed services industry is moderately fragmented, with the presence of several global telecom equipment providers, network service companies, IT service providers, and regional managed service vendors competing across different service segments and geographies. Large players such as Cisco Systems, Huawei Technologies, Ericsson, Nokia, AT&T, and Verizon dominate the market through extensive service portfolios, global delivery capabilities, and long-term partnerships with telecom operators and enterprises. However, the market also includes numerous emerging and niche providers specializing in cloud-managed services, cybersecurity, OSS/BSS solutions, network analytics, and AI-driven automation.

Market fragmentation is further supported by the rapid evolution of technologies such as 5G, edge computing, IoT, and cloud-native networks, which create opportunities for specialized vendors to offer innovative, customized solutions. Regional service providers and emerging companies continue to gain traction by delivering cost-effective, flexible, and industry-specific managed services tailored to enterprise requirements. At the same time, strategic partnerships, mergers, acquisitions, and integrated service offerings among larger players are gradually increasing market consolidation in certain high-value segments of the telecom managed services ecosystem.

Service Type Insights

The managed data center services segment led the market with the largest revenue share of 30.0% in 2025. Increasing adoption of edge data centers, driven by the proliferation of IoT devices and the need for low-latency applications, is contributing to the growth of the segment. Edge data centers enable data processing closer to the source, reducing network congestion and improving overall performance. In addition, the growing focus on sustainability and energy efficiency in data center operations is also contributing to the growth of the segment. Telecom providers are exploring innovative technologies and green practices to minimize energy consumption and carbon footprint, aligning with global environmental goals.

The managed mobility services segment is expected to grow at the fastest CAGR during the forecast period. The growth of the segment is attributed to its capability to enable employees to access enterprise data from any smart device, regardless of location. These services facilitate seamless connectivity by providing configuration, deployment, and smart device management for both in-office and remote workers. Managed mobility services encompass IT and process management services that enable businesses to procure, deploy, and support smartphones, tablets, and other field-force devices. The main goal of managed mobility services is to securely and efficiently connect mobile out-of-office workers to databases, servers, management, and other employees.

Deployment Insights

The cloud segment accounted for the largest market revenue share in 2025 and is projected to grow at the fastest CAGR during the forecast period. The increasing demand for flexible and scalable communication solutions drives the segment growth. Businesses across industries are transitioning their operations to the cloud, making reliable, efficient telecom services essential. Managed service providers in the telecom sector are leveraging this trend by offering comprehensive solutions that include cloud-based voice, data, and messaging services. The integration of advanced technologies, such as AI-driven automation and analytics, is further enhancing service quality and improving customer experience. Cloud telecom managed services are expected to grow rapidly as organizations continue to prioritize cost-effective, secure, and innovative solutions to meet their evolving communication requirements in a rapidly changing digital landscape.

The on-premise segment is expected to grow at a significant CAGR during the forecast period.While cloud-based solutions have gained popularity, on-premises managed services continue to serve organizations that prioritize data control, compliance requirements, or unique networking setups. These services offer businesses the ability to have their telecom infrastructure and services managed within their own premises, providing a higher level of customization and security. On-premise telecom managed service providers discreetly tailor solutions to meet the specific demands of their clients, ensuring seamless integration with existing systems and facilitating efficient communication.

Enterprise Size Insights

The large enterprises segment accounted for the largest market revenue share in 2025. The need to manage highly complex, large-scale network infrastructure efficiently is driving the adoption of telecom managed services among large enterprises. These organizations operate across multiple geographies, requiring seamless connectivity, high network uptime, and consistent service quality. Managed service providers enable centralized network management, advanced monitoring, and proactive maintenance, helping large enterprises ensure operational continuity. In addition, the integration of technologies such as 5G, cloud, and AI-driven analytics further increases infrastructure complexity, making outsourcing a strategic necessity.

The small & medium enterprise segment is projected to grow at the fastest CAGR of 16.3% over the forecast period. The need for cost-effective and scalable communication solutions is fueling the growth of the telecom managed services among small and medium enterprises (SMEs). SMEs often face budget, technical expertise, and in-house IT capabilities constraints, making it challenging to manage telecom infrastructure independently. Managed service providers offer flexible, subscription-based models that allow SMEs to access advanced telecom technologies without significant upfront investments. This enables them to focus on core business activities while ensuring reliable connectivity and network security.

Regional Insights

North America dominated the global telecom managed services market with the largest revenue share of 38.0% in 2025. The market in the region is characterized by high maturity, advanced network infrastructure, and early adoption of emerging technologies such as 5G, cloud computing, and AI-driven network automation. Strong demand for network optimization, cybersecurity, and operational efficiency has been observed across telecom operators and enterprises.

U.S. Telecom Managed Services Market Trends

The telecom managed services market in the U.S. accounted for the largest market revenue share in North America in 2025, due to the extensive 5G deployment and a highly competitive telecom landscape. Telecom operators are increasingly outsourcing network operations, maintenance, and service assurance to improve efficiency and reduce operational costs.

Europe Telecom Managed Services Market Trends

The telecom managed services market in Europe was identified as a lucrative region in 2025. The market in the region is driven by strong regulatory frameworks, increasing focus on data privacy, and widespread adoption of digital technologies. Telecom operators across the region are prioritizing cost optimization and network modernization, leading to increased outsourcing of non-core functions.

The UK telecom managed services market is expected to grow rapidly in the coming years, driven by ongoing investments in 5G infrastructure and digital transformation initiatives across industries. Telecom operators are increasingly leveraging managed services to enhance network resilience, improve service quality, and meet evolving customer expectations.

The telecom managed services market in Germany held a substantial market share in Europe in 2025. The country's growth is driven by its strong industrial base and the increasing adoption of Industry 4.0 technologies. Telecom managed services are being widely adopted to support advanced manufacturing processes, IoT integration, and real-time data communication. Operators and enterprises are focusing on network reliability, low latency, and secure connectivity, which is accelerating the demand for specialized managed services.

Asia Pacific Telecom Managed Services Market Trends

The telecom managed services market in the Asia Pacific is anticipated to grow at the fastest CAGR of 16.6% during the forecast period. The region is experiencing rapid growth driven by expanding telecom infrastructure, rising mobile penetration, and accelerating digital transformation across emerging economies. Telecom operators are increasingly outsourcing network management functions to address rising operational complexity and cost pressures.

The India telecom managed services market is expected to grow at a rapid CAGR during the forecast period, fueled by widespread 4G and 5G expansion, increasing internet penetration, and a rapidly digitizing economy. Telecom operators are leveraging managed services to improve network efficiency, reduce costs, and manage large-scale subscriber bases.

The telecom managed services market in China held a substantial market share in the Asia Pacific in 2025. The growth in the country is driven by extensive 5G deployment, large-scale industrial digitization, and strong government support for technology advancement. Telecom operators are increasingly adopting managed services to handle complex network environments and ensure high-performance connectivity.

Key Telecom Managed Services Company Insights

Some of the key companies in the telecom managed services industry include Cisco Systems Inc., Huawei Technologies Co., Ltd., Telefonaktiebolaget LM Ericsson, Acuity Technologies, Verizon Communications Inc., and others. Organizations are focusing on increasing customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies.

-

Cisco Systems Inc. is a networking, cybersecurity, and collaboration technology company that powers the internet's infrastructure with products such as switches, routers, wireless access points, and firewalls. Cisco has evolved from its core Internetworking Operating System (IOS) roots to AI-native solutions in secure networking, observability, cloud, and unified communications, serving sectors from telecom and finance to healthcare and manufacturing via segments including Networking, Security, and Collaboration. Cisco's Managed Service Provider Networks deliver end-to-end 4G/5G orchestration via telco cloud platforms, combining segment routing, Cisco Virtualized Infrastructure Manager (OpenStack), and packet core apps for operators seeking lower opex and faster go-to-market without owning full stacks.

-

Telefonaktiebolaget LM Ericsson is a telecommunications equipment and services provider offering hardware, software, and managed solutions for 5G, IoT, and cloud-native networks to operators serving over 1 billion subscribers worldwide. It provides managed services covering networks (4G/5G RAN/core), IT (apps/data centers), and design/optimization, with an AI-driven Ericsson Operations Engine for automation, user-experience focus, and opex savings of up to 25% through predictive maintenance and zero-touch provisioning.

Key Telecom Managed Services Companies:

The following key companies have been profiled for this study on the telecom managed services market.

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Telefonaktiebolaget LM Ericsson

- Acuity Technologies

- Verizon Communications Inc.

- AT&T Inc

- NTT DATA

- Comarch SA

- Nokia

- Fujitsu Ltd.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Cisco Systems, Inc.; Huawei Technologies Co., Ltd.; Telefonaktiebolaget LM Ericsson

- Mature players focus on delivering large-scale, end-to-end telecom managed services across network planning, deployment, operations, and optimization.

- Their strategies emphasize long-term managed services contracts, integrated service portfolios (network, IT, cloud, and security), and outcome-based service delivery models.

- Strong domain expertise across telecom infrastructure, including 5G, fiber, cloud, and network virtualization technologies.

- Established global presence with deep relationships with telecom operators and large enterprises.

- Ability to deliver end-to-end managed services combining hardware, software, and lifecycle support.

- Large organizational structures can reduce agility and slow innovation cycles compared to smaller players.

- High service costs and complex engagement models may limit adoption among small and mid-sized enterprises.

- Dependence on legacy systems and existing infrastructure can create integration challenges with newer technologies.

Emerging Players: Acuity Technologies; Comarch SA

- Emerging players focus on niche and specialized telecom managed services such as OSS/BSS, network analytics, cloud-native solutions, and managed security services.

- Higher agility and faster innovation cycles compared to large incumbents.

- Cost-effective service models and flexible pricing structures attract small and medium enterprises.

- Strong capabilities in cloud-native architectures, automation tools, and digital platforms.

- Limited global presence and smaller scale restrict their ability to handle large, multi-country telecom contracts.

- Lower brand recognition compared to established players may impact customer trust and acquisition.

Recent Developments

-

In August 2025, Vodafone Idea (Vi) partnered with IBM to modernize its IT and managed services environment using AI, automation, and a unified DevOps model, aiming the improve service reliability and customer experience. The partnership will form an AI Innovation Hub, where teams from Vi and IBM Consulting will co-create AI solutions, digital accelerators, and automation tools that can be embedded into development and operations workflows.

-

In April 2025, U Mobile selected EdgePoint Infrastructure as a preferred partner to accelerate in-building 5G coverage across Malaysia as it rolls out its second 5G network, with both sides signing an MoU to tailor site-specific solutions, improve performance, and keep deployment cost-effective and fast. The collaboration aims to expand indoor coverage in key locations while also enabling lower latency, faster speeds, and future applications such as AI, smart cities, and autonomous systems.

Telecom Managed Services Market Report Scope

Report Attribute

Details

Market size in 2025

USD 28.6 billion

Estimated Market size in 2026

USD 32.3 billion

Projected Market size by 2033

USD 89.9 billion

Growth rate

CAGR of 15.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion. and CAGR from 2026 to 2033

Report deployment

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Service type, deployment, enterprise size, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

Cisco Systems, Inc.; Huawei Technologies Co., Ltd.; Telefonaktiebolaget LM Ericsson; Acuity Technologies; Verizon Communications Inc.; AT&T Inc; NTT DATA; Comarch SA; Nokia; Fujitsu Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Telecom Managed Services Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global telecom managed services market report based on service type, deployment, enterprise size, and region.

-

Service Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Managed Data Center Services

-

Managed Security Services

-

Managed Network Services

-

Managed Mobility Services

-

Others

-

-

Deployment Outlook (Revenue, USD Million, 2021 - 2033)

-

On-premise

-

Cloud

-

-

Enterprise Size Outlook (Revenue, USD Million, 2021 - 2033)

-

Large Enterprises

-

Small & Medium Enterprises

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Telecom Managed Services Market Opportunity Assessment

Country/region-wise market sizing and forecasts

Analysis of demand, adoption trends, and regulatory landscape

Identification of high-growth regions and investment hotspots

Identified region-specific growth opportunities

Supported expansion and go-to-market strategy

Enabled informed regional investment decisions

Cross-Segmentation Analysis for the Telecom Managed Services Market

Criss-cross market analysis by service type, deployment, and enterprise size

Demand and adoption assessment across key segments

Segment attractiveness and growth potential benchmarking

Identified high-potential market segments

Supported targeted product positioning and marketing strategy

Improved customer and segment prioritization

Competitive Benchmarking and Strategic Positioning in the Telecom Managed Services Market

Benchmarking of key competitors across products, pricing, partnerships, and innovation

Comparative assessment of market share, capabilities, and strategies

Analysis of competitive strengths, gaps, and differentiation areas

Identified competitive white spaces and growth gaps

Supported strategic positioning and differentiation

Enabled data-driven competitive strategy development

Frequently Asked Questions About This Report

Some of the key players in the telecom managed services market include Cisco Systems, Inc., Huawei Technologies Co., Ltd., Telefonaktiebolaget LM Ericsson, Acuity Technologies., Verizon Communications Inc., AT&T Inc., NTT DATA, Comarch SA., Nokia, and Fujitsu Limited.

The rapid deployment and adoption of 5G networks fuel the demand for telecom managed services. 5G technology requires specialized expertise to optimize network performance, handle increased data traffic, and support new use cases like IoT and augmented reality.

The global telecom managed services market size was valued at USD 28.6 billion in 2025 and is expected to reach USD 32.3 billion in 2026.

North America dominated the global telecom managed services market with the largest revenue share of 38.0% in 2025.

Asia Pacific is the fastest-growing regional market during the forecast period.

The managed data center services segment led the market with the largest revenue share of 30.0% in 2025.

The cloud segment accounted for the largest market revenue share in 2025.

The large enterprises segment accounted for the largest market revenue share in 2025.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.