- Home

- »

- Advanced Interior Materials

- »

-

Thermal Interface Materials Market Size Report, 2026-2033GVR Report cover

![Thermal Interface Materials Market (2026 - 2033)Report]()

Thermal Interface Materials Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Tapes & Films, Metal, Elastomeric Pads, Greases And Adhesives, Phase Change Materials), By Application (Telecom, Computers), By Region, And Segment Forecasts

Market Size, 2025

$4.6BMarket Estimate, 2026

$5.1BMarket Forecast, 2033

$11.2BCAGR, 2026–2033

12.0%Thermal Interface Materials Market Summary

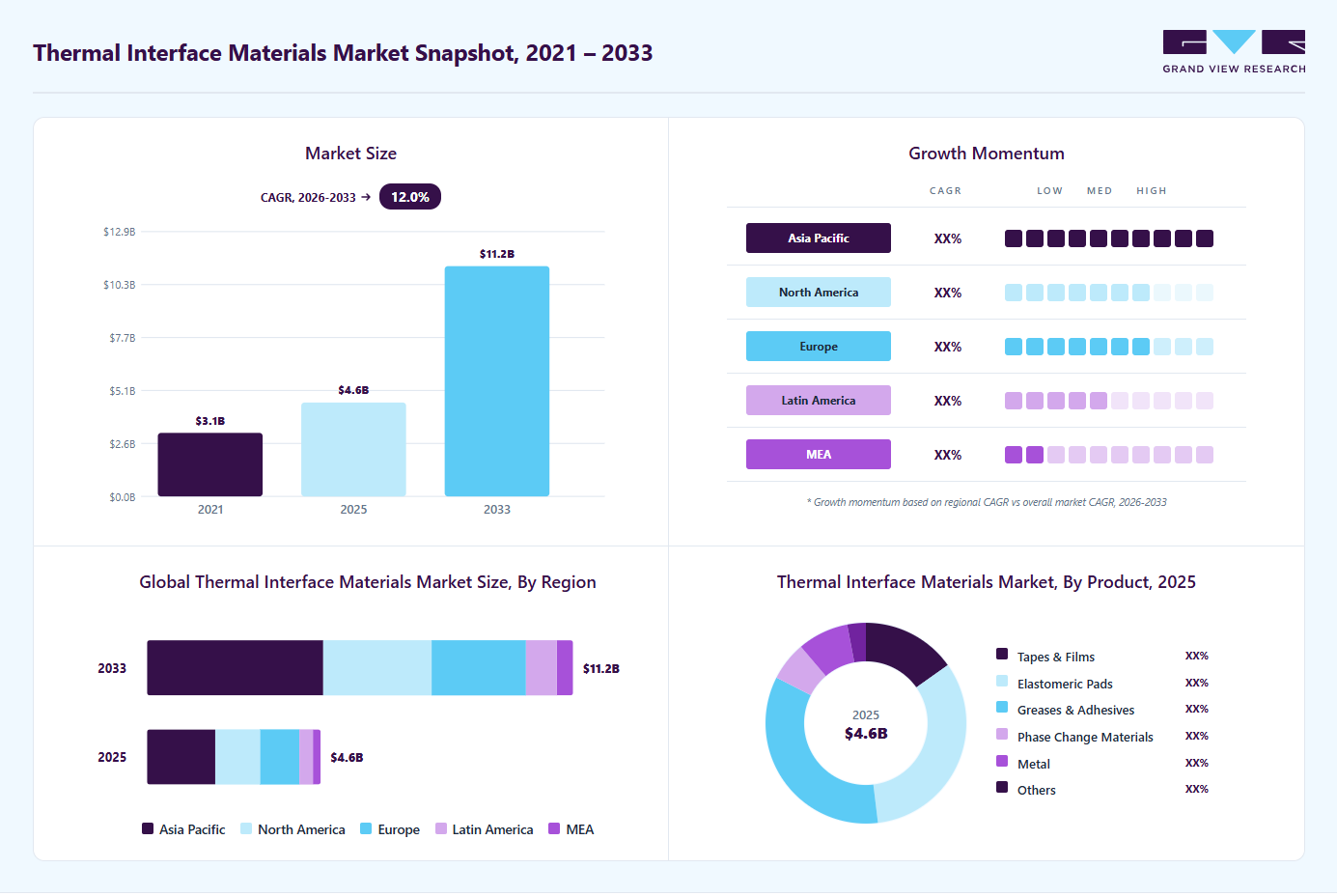

The global thermal interface materials market size was valued at USD 4.6 billion in 2025 and is projected to grow from USD 5.1 billion in 2026 to USD 11.2 billion by 2033, at a CAGR of 12.0% from 2026 to 2033. Asia Pacific held the largest revenue share of 39.3% of the global market in 2025. The increasing use of electronic consumer products, such as smartphones and laptops, the adoption of automation in industries in developing countries, and the rising disposable income of the middle-class population are expected to drive demand for thermal interface materials during the forecast period.

Key Market Trends & Insights

- By product: Thermal greases and adhesives segment held the largest market share of 34.4% in 2025.

- By application: Computers segment held the largest market share of 23.5% in 2025.

- By product: Phase change materials segment is expected to grow at the fastest CAGR of 12.4%

Regional Highlights

- Largest market: Asia Pacific (39.3% market share, 2025)

- Fastest-growing market: Asia Pacific (highest CAGR, 2026-2033)

- By Country: China is experiencing substantial growth and continues to be a global leader.

Market Size & Forecast

- Market size in 2025: USD 4.6 Billion

- Estimated market size in 2026: USD 5.1 Billion

- Projected market size by 2033: USD 11.2 Billion

- CAGR (2026–2033): 12.0%

Thermal interface materials are applied between two hard surfaces to conduct heat and are often used in situations where there is a greater demand for modern electronic devices. The commercial availability of various thermal interface materials in diverse forms, coupled with the growing applications in the electronic industry, is expected to drive demand over the coming years. The growing demand for automation in the manufacturing of pharmaceuticals and medical machinery is expected to drive the demand for thermal interface materials over the forecast period. Furthermore, the demand for pharmaceuticals and medical products is growing with the increasing incidences of illnesses and diseases among the population in developed as well as developing economies. This is likely to drive the demand for thermal interface materials across the globe.

The increased use of smartphones and other smart devices has led to an increased demand for thermal interface materials in developed countries such as the U.S. The need for fast-speed networks, higher bandwidth, and increased system performance due to the boom in the computer industry and increased IT activities is also expected to augment the growth of the market.

")

Thermal interface materials are widely utilized in consumer electronics for improving performance, sustainability, quality, functionality, and environmental properties. These materials help boost the overall lifespan of consumer electronics on account of their high protection & durability. Moreover, the growing need for thermal conductivity in high-end electronic products is anticipated to support the market over the forecast period.

The pandemic has changed consumer purchase behaviour which has led to increased use of consumer electronics such as tablets, phones, and video games. The demand for automation in applications such as the pharmaceutical and medical industries has also seen a rise due to increased demand for drugs and medical equipment during and post-pandemic.

The thermal interface is commonly known to provide efficient heat management solutions required for improving the system’s overall performance and lifespan. Various products of thermal interfaces available in the market include greases, thermal tapes, elastomeric pads, and solders. The materials selection criteria are based on mechanical factors, electrical insulation, quality, thermal resistance, performance, and material compatibility.

The product is anticipated to witness significant gains owing to its thermal conductivity nature which helps in strengthening the life and efficiency of the electronic device or the equipment where it finds its application. The product is usually made of conducting materials like silicone, metal oxides, or metals.

Market Dynamics

The increasing adoption of automation in the pharmaceutical and medical machinery sectors continues to be a major driver for the TIM market. The rising global demand for pharmaceuticals and medical equipment, fueled by the growing prevalence of chronic illnesses and lifestyle diseases, is accelerating the need for efficient heat management solutions. Thermal interface materials are critical in ensuring reliable performance and longevity of medical devices, particularly in high-precision applications.

The integration of advanced components, such as threaded inserts for plastics, wire screw thread inserts, blind rivets, and self-locking systems in medical devices like surgical lasers, MRI scanners, and pacemakers, underscores the importance of TIMs. In addition, the development of innovative solutions like self-locking elastomeric pads and advanced thermal tapes and films is anticipated to drive significant demand in medical electronics.

The continued price volatility in the oil market remains a significant restraint for industries dependent on crude oil and natural gas, including the thermal interface materials (TIM) sector. The impact of oil price volatility causes cost fluctuations and affects the overall supply chain, from sourcing raw materials to final product distribution. During periods of rising oil prices, manufacturers face increased production costs, which may lead to higher prices for end-users. Conversely, when oil prices decline significantly, there may be a risk of oversupply, leading to market instability. These market fluctuations create challenges for TIM companies in maintaining stable profit margins, particularly for new products entering competitive markets. Furthermore, the economic pressure exerted by volatile oil prices may deter investment in new manufacturing technologies and innovations critical to advancing TIM products.

Market Concentration & CharacteristicsThe thermal interface materials market is moderately consolidated, with a mix of large multinational players and specialized material manufacturers. Leading companies benefit from strong R&D capabilities, long-term relationships with electronics OEMs, and broad product portfolios. High entry barriers exist due to the need for advanced material science expertise and stringent quality requirements. However, niche players continue to enter the market with application-specific solutions, especially in emerging sectors such as EVs and 5G equipment. Strategic partnerships between TIM suppliers and semiconductor or automotive manufacturers are becoming more common.

The threat of substitutes in the thermal interface materials market is moderate, as alternative cooling solutions such as advanced heat sinks, liquid cooling, and vapor chambers are gaining popularity. However, these technologies generally complement rather than replace TIMs, as thermal interface materials remain essential for minimizing interfacial thermal resistance. Design-level thermal optimization and advanced packaging techniques may reduce the volume of TIMs used but do not eliminate the need for them. Cost and complexity of alternative solutions limit their widespread adoption in low- to mid-range applications. TIMs continue to offer a cost-effective and efficient solution for most electronic systems.

Product Insights

Thermal greases and adhesives segment led the market with a share of 34.4% in 2025, owing to the widespread usage in consumer products and the high thermal resistance of the product. The elastomeric pads are expected to have a significant revenue share based on their easy assembly as compared to greases. Also, with elastomeric pads, the handling mechanism is improved and possesses less chance of degrading interface resistance.

Phase change materials segment is anticipated to expand at the fastest CAGR of 12.4% during the forecast period. It is widely used in construction work, supported by the demand for cooler buildings. The material act as heat storage wherein the heat gets absorbed during summer and retained heat can be used in winter times to manage the temperature difference.

Elastomeric pads are expected to register a significant CAGR over the forecast period, owing to their easy handling and installation techniques used for thermal conductivity in electrical and electronic components. However, the limited application scope and the high unit cost of the products are expected to hamper the growth in the estimated time frame.

These interface materials are majorly used for applications in dispensable gels, gap-filling and insulating pads, adhesive tapes, and greases. These are selected based on their toughness, environmental & chemical resistance, hardness, tensile strength, and thermal conductivity. Moreover, compatibility with electronic and mechanical gadgets is considered.

Application Insights

The computers segment accounted for a significant share of 23.5% in 2025, due to increased utilization in office end-use. The affordable prices of desktops have revolutionized the demand and supply of products. The post-pandemic times did not dampen the market, rather with the increase in the number of people working from home, the upgradation, sales, and installation figures of the PC market have increased.

The telecom application segment for product utilization is expected to witness significant demand in the estimated time owing to the increasing preference for digital and cashless economy. The banks, e-commerce, utilities, and media rely on the telecom industry for their businesses, and it is seen as their lifeline. Thus, is likely to support the industry’s growth over the projected time.

The products are considered to address the challenge of higher thermal insulation, dissipation, and conductance in medical electronics and other industries. These are broadly classified into polymer matrix composites, metal matrix composites, and carbon composite products. Moreover, technical advancements in the product for providing better thermal management solutions are expected to augment the growth.

The material finds application in medical devices, industrial machinery, consumer durables, and automotive electronics. With the advanced cockpit functionality, the materials are also installed in aerospace components. The recent advancements in military and aerospace applications have led engineers to address the increased thermal management issues.

Regional Insights

North America thermal interface materials market is anticipated to grow significantly over the forecast period. The growth of North America's thermal interface materials market is primarily driven by the increasing demand for advanced electronic devices, including high-performance computing systems, consumer electronics, and electric vehicles. As these technologies evolve, efficient heat dissipation systems are critical. TIMs play a vital role in ensuring the thermal management of electronic components, preventing overheating, and improving the overall lifespan and performance of devices.

U.S. Thermal Interface Materials Market Trends

The thermal interface materials market in the U.S. is experiencing significant growth. The U.S. government's focus on renewable energy and sustainability has further supported the growth of the TIM market. The push for energy-efficient technologies and green building practices has led to greater investments in industries that require reliable thermal management, such as renewable energy storage systems, LED lighting, and industrial automation.

Asia Pacific Thermal Interface Materials Market Trends

Asia Pacific dominated the market with a share of over 39.3% in 2025 due to high demand owing to the presence of a large base of manufacturing zone. In addition to the manufacturing base, reductions in corporate tax, GST, rising household incomes, consumer health awareness, changing lifestyles, and government policies have the potential to propel industry growth in this region.

Thermal interface materials market in China is experiencing substantial growth. As China continues to be a global leader in the production of consumer electronics, including smartphones, computers, and wearable devices, the demand for efficient heat management solutions has surged. Thermal interface materials are essential in managing heat dissipation in electronic components such as processors and batteries, thus preventing overheating and ensuring optimal performance.

Europe Thermal Interface Materials Market Trends

The thermal interface materials market in Europe is experiencing notable growth. In Europe, the rise in consumer electronics, including smartphones, laptops, and gaming consoles, as well as the growing adoption of electric vehicles (EVs), has significantly contributed to the demand for advanced thermal management solutions. European manufacturers are also focusing on developing high-performance TIMs to meet the stringent regulatory standards for energy efficiency and sustainability, further propelling the market.

Thermal interface materials market in Germany plays a crucial role in the respective European market due to its strong automotive and industrial base. High adoption of electric vehicles and advanced manufacturing equipment drives demand for thermal management solutions. The country’s emphasis on engineering excellence and product reliability supports the use of high-performance TIMs. Growth in automation and Industry 4.0 technologies further boosts demand. Local OEMs collaborate closely with material suppliers for customized solutions. Germany remains a technologically advanced and stable market.

Latin America Thermal Interface Materials Market Trends

Latin America represents an emerging market for thermal interface materials, driven by gradual growth in electronics assembly and renewable energy projects. Increasing adoption of EVs and industrial automation is creating new demand opportunities. Brazil and Mexico are key countries contributing to regional growth. Limited local production leads to higher dependence on imports, shaping market dynamics. Infrastructure development and digital transformation initiatives support long-term growth. The market is expanding at a moderate pace.

Middle East & Africa Thermal Interface Materials Market Trends

The Middle East & Africa thermal interface materials market is growing due to investments in data centers, energy infrastructure, and smart city projects. Rising adoption of advanced electronics in industrial and defense applications supports demand. The region is increasingly focusing on renewable energy and grid modernization, which requires effective thermal management. Limited manufacturing base results in reliance on imported TIM products. Gulf countries are leading growth due to strong infrastructure investments. Overall, the market shows gradual but steady expansion.

Key Thermal Interface Materials Company Insights

Some of the key players operating in the market include 3M, Indium Corporation, Honeywell International Inc. and others:

-

3M is a diversified technology company known for its innovative products across various industries, including electronics, automotive, and healthcare. Among its extensive portfolio, 3M offers a range of thermal interface materials designed to enhance thermal management in electronic devices. These materials are crucial for dissipating heat generated by components such as CPUs, GPUs, and power transistors, thereby improving the reliability and performance of electronic systems.

-

Indium Corporation is a global manufacturer of advanced materials for electronics, semiconductors, and solar industries. Among its diverse product offerings, the company specializes in thermal interface materials, critical for enhancing thermal conductivity between heat-generating components and heat sinks or other cooling solutions.

Key Thermal Interface Materials Companies:

The following key companies have been profiled for this study on the thermal interface materials market.

- 3M

- Henkel

- Indium Corporation

- Fujipoly

- The Dow Chemical Company

- Honeywell International Inc.

- SIBELCO

- Shin-Etsu

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: The 3M Company; Dow Corning Company; Honeywell International Inc.; Parker Chomerics; Henkel AG & Co. KGaA

- Mature players focus on product diversification, partnerships with industry leaders, and expanding their presence in emerging markets.

- They emphasize on large-scale, long-term contracts with manufacturers, especially in high-growth sectors like EVs, telecommunications, and healthcare.

- The competitive edge for these players lies in their robust supply chains, advanced manufacturing capabilities, and the ability to cater to a wide range of customer needs.

- Their strong financial resources allow them to invest heavily in R&D, driving the development of next-generation TIM solutions.

- Despite their market dominance, mature players may face challenges related to product commoditization and pricing pressure, particularly from emerging players offering cost-effective alternatives. Moreover, their large-scale operations can sometimes result in slower adaptability to rapidly changing market dynamics and innovations, putting them at risk in more niche applications.

Emerging Players: Indium Corporation; Fuji Polymer Industries Co., Ltd.; AIM Specialty Materials; AOS Thermal Compounds, LLC

- Emerging players often differentiate themselves by focusing on specialized products or targeting specific regions with high growth potential, such as China, India, and Southeast Asia.

- They tend to operate with leaner structures, allowing for faster product development cycles and the ability to quickly adapt to customer demands.

- The primary competitive advantage for emerging players is their ability to offer cost-effective, tailored solutions that cater to the unique needs of specific industries.

- They focus on providing high-performance materials at competitive prices, capitalizing on regional demand and the increasing need for customized thermal management solutions.

- Emerging players often struggle with limited resources for large-scale production and R&D compared to their larger counterparts.

- Their relatively smaller market presence and limited financial backing can hinder their ability to scale quickly or penetrate highly competitive global markets.

Recent Developments

- In November 2024, Dow partnered with Carbice to offer advanced thermal interface materials for various industries, including mobility, industrial, consumer electronics, and semiconductors.

Thermal Interface Materials Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 4.6 billion

Estimated Market size in 2026

USD 5.1 billion

Projected Market size by 2033

USD 11.2 billion

Growth rate

CAGR of 12.0% from 2026 to 2033

Base year for estimation

2025

Actual estimates/Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD Million/Billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Regional Scope

North America, Europe, Asia Pacific, Central & South America, and Middle East & Africa

Country scope

U.S.; Canada; Mexico; France; Germany; UK; Italy; China; India; Japan; South Korea; Argentina; Brazil; UAE; Saudi Arabia

Segments covered

Product, application, and region

Key companies profiled

The 3M Company; Henkel; Indium Corporation; Fujipoly; The Dow Chemical Company; Honeywell International Inc.; SIBELCO; Shin-Etsu

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Thermal Interface Materials Market Report Segmentation

This report forecasts revenue growth at regional and country levels and provides an analysis of the industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global thermal interface materials market based on product, application, and region:

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Tapes And Films

-

Elastomeric Pads

-

Greases And Adhesives

-

Phase Change Materials

-

Metal

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Telecom

-

Computer

-

Medical Devices

-

Industrial Machinery

-

Consumer Durables

-

Automotive Electronics

-

Others

-

-

Regional Outlook (Revenue; USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Mexico

-

Canada

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Extension

Expanded regional analysis of the thermal interface materials market, including country-level demand trends, electronics and EV manufacturing activities, regulatory landscape, and adoption patterns across key end-use industries.

Enable identification of high-growth regional markets and demand hotspots. Support regional expansion strategies and understanding of region-specific industry trends and competitive dynamics.

Competitive Benchmarking

Benchmarking of key thermal interface material manufacturers based on product portfolio, production capacity, geographic presence, technology capabilities, pricing strategy, end-use focus, and strategic initiatives such as product launches, partnerships, and capacity expansions.

Enable comparison of competitive positioning and identification of differentiation opportunities, strategic gaps, and market leadership trends.

Opportunity Assessment

Evaluation of growth opportunities across product types, applications, and end-use industries in the thermal interface materials market, including EV batteries, consumer electronics, telecommunications, data centers, and renewable energy systems, along with emerging thermal management technology trends.

Identify high-growth applications and emerging demand areas. Support product development, market entry, and expansion strategies driven by increasing thermal management requirements across advanced electronic systems.

Frequently Asked Questions About This Report

Some key players operating in the precision guided munition market include Indium Corporation, Fujipoly, The Dow Chemical Company, 3M, Henkel, Honeywell International Inc., among others.

Asia Pacific dominated the global thermal interface materials market with the highest share of 39.3% in 2025. This is attributable to rising industrial base, automation, and manufacturing activities happening in emerging economies.

Key factors driving the thermal interface materials market growth include rising demand for high-performance and energy-efficient electrical & electronic gadgets, growth in application industries like telecom and computer segments, because of the affordable pricing, which has revolutionized the demand and supply in these segments.

The global thermal interface materials market was estimated at USD 4.6 billion in 2025 and is expected to reach USD 5.1 billion in 2026.

The global thermal interface materials market is expected to grow at a compound annual growth rate of 12.0% from 2026 to 2033 to reach USD 11.2 billion in 2033.

Asia Pacific is the fastest-growing region over the forecast period.

Thermal greases and adhesives segment led the market with a share of 34.4% in 2025, while phase change materials segment is expected to grow fastest.

Computers segment accounted for a significant share of 23.5% in 2025.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.