- Home

- »

- Plastics, Polymers & Resins

- »

-

Thermoplastic Polyester Elastomer Market Size Report, 2030GVR Report cover

![Thermoplastic Polyester Elastomer Market Size, Share & Trends Report]()

Thermoplastic Polyester Elastomer Market (2023 - 2030) Size, Share & Trends Analysis Report By Type (Injection Molding, Extrusion Molding), By End-use (Medical, Industrial), By Region, And Segment Forecasts

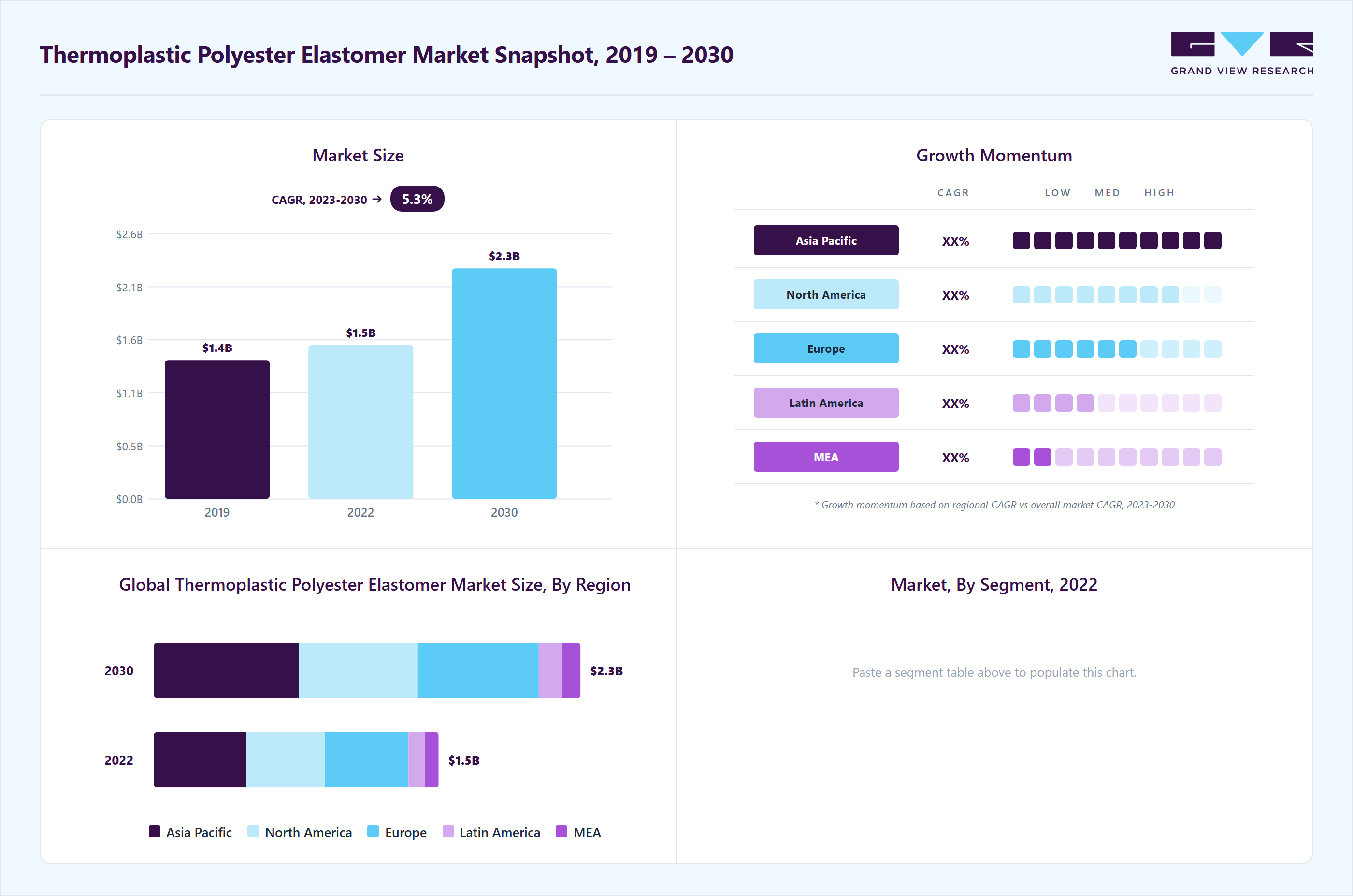

Market Size, 2022

$1.5BMarket Estimate, 2026

$1.6BMarket Forecast, 2030

$2.3BCAGR, 2023–2030

5.3%Market Size & Trends

The global thermoplastic polyester elastomer market size was estimated at USD 1.52 billion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 5.34% from 2023 to 2030. Increasing adoption of lightweight products in several end-use industries including automotive, medical, and consumer goods, among others is expected to boost the market growth over the forecast period. The growing demand for thermoplastic polyester elastomer (TPEE) in electronic devices, electronic housings, gadgets, and others is expected to contribute to the growth of the market. The increasing preferences for lightweight electronics and wearables are expected to propel the demand for TPEE in the coming years.

The market in the U.S. is predicted to experience significant growth in recent years, with several factors driving the market. Increasing demand for automotive components is predicted to be a primary driver of the global market throughout the forecast period. The surge in technological developments in TPEE production processes, along with consumer awareness of the health and environmental repercussions of plastics, are also predicted to boost the market growth.

The U.S. medical industry has witnessed significant growth in the thermoplastic polyester elastomer (TPEE) market. It is used in catheters, tubing, and seals owing to their several properties such as flexibility, lightweight, anti-fatigue, heat resistance, and others. The increasing use of TPEE in medical devices, instruments, and equipment is expected to boost production and development in the market.

Market Dynamics

The thermoplastic polyester elastomer market is being driven by increasing demand for lightweight, high-performance materials that combine flexibility, mechanical strength, and chemical resistance across automotive, electronics, healthcare, and industrial applications. Thermoplastic polyester elastomers (TPEEs) offer superior fatigue resistance, elasticity, dimensional stability, and processability, making them suitable for applications requiring long-term durability under dynamic operating conditions. Industries are increasingly adopting TPEEs as alternatives to conventional rubber and engineering plastics to improve product performance and manufacturing efficiency.

Automotive applications remain among the largest contributors to market growth. TPEEs are widely utilized in air ducts, CVJ boots, seals, hoses, cable jacketing, and vibration-control components because of their excellent heat resistance and mechanical durability. The growing transition toward electric vehicles is further accelerating demand for lightweight and high-temperature elastomer materials capable of supporting thermal management and electrical insulation requirements. Automotive manufacturers are also prioritizing recyclable thermoplastic materials to support sustainability objectives and improve processing efficiency.

The market faces competition from alternative thermoplastic elastomers and engineered polymers. Thermoplastic polyurethanes, thermoplastic vulcanizates, silicone elastomers, and polyamide elastomers continue to compete with TPEEs in automotive, electronics, and industrial applications. In certain cost-sensitive applications, manufacturers may select lower-cost substitute materials when premium elastomer performance characteristics are not essential, limiting broader TPEE penetration.

Type Insights

Based on type, the injection molding vehicle segment accounted for the largest revenue share of over 68.0% in 2022. Injection molding is one of the most common techniques for processing TPEE. Injection molding grade TPEE is utilized in a variety of applications, including automotive parts, electrical and electronic components, and consumer items. The injection molding technology for thermoplastic polyester elastomers (TPEEs) is expected to drive growth in the TPEE market.

The growing demand for high-performance materials in a variety of end-use sectors is likely to boost the demand for injection molding grade TPEE. Injection molding provides high precision and repeatability to the resin, making it an ideal material for several end-use applications.

The extrusion molding is expected to grow at a significant rate over the forecast period. Extrusion molding for thermoplastic polyester elastomers is an integral process that is expected to contribute to the TPEE market growth. Extrusion molding helps to manufacture objects such as tubes, hoses, profiles, and films. Extruded TPEE weather-stripping, seals, and gaskets are employed in the construction industry, particularly in energy-efficient and green building designs.

End-use Insights

Based on end-use, the automotive segment dominated the market and accounted for the largest revenue share of over 129% in 2022. Increasing plastics usage in automotive components, as well as concurrent increases in heavy-duty vehicle production, passenger car production, and increased demand for electric vehicles, are likely to fuel growth over the projection period.

The rising penetration of electrical vehicles across the globe owing to the biocompatibility offered by the product is expected to boost the consumption and manufacturing of TPEE in the automotive industry. TPEE are used in a variety of applications in the automotive industry, including the production of high-quality automotive instrument panels, seat backs, airbag deployment doors, air intake ducting, wheel covers, dashboard components, door liners and handles, pillar trim, and consumer goods components, among others. In addition, TPEE is increasingly used to replace vulcanized rubber and flexible polyvinyl chloride (PVC), with the goal of reducing vehicle weight for higher fuel efficiency and lower CO2 and NOx gas emissions, along with achieving greater recyclability for environmental sustainability.

Medical and healthcare expenditures have also risen significantly in recent years, demanding rapid production of lightweight and durable medical equipment and gadgets. The segment is expected to increase at an exponential rate, mainly in emerging economies such as India, Indonesia, Thailand, Argentina, and Mexico.

Regional Insights

The Asia Pacific region dominated the market and accounted for the largest revenue share of over 32.30% in 2022. The increasing manufacturing sector is expected to fuel the demand for TPEE compounds in the automotive, industrial machinery, packaging, and electrical and electronics industries. TPEEs are widely employed in automotive applications such as seals, gaskets, and interior components, contributing to the overall growth of the TPEE market in the region.

The continuously growing automotive manufacturing companies serve to fill the product gaps in the local market. China, Indonesia, India, and Bangladesh are expected to be the main factors driving the rise of the regional market. In addition, a robust electrical and electronics manufacturing base in China and South Korea is likely to influence the demand for thermoplastic polyester elastomer, thus driving market growth.

Europe is expected to grow at a significant CAGR in the coming years. The rise in the industrial sector in the region owing to the widening of the scope of machine parts and accessories is likely to boost TPEE consumption in the region.TPEEs possess superior strength, durability, and resistance to wear and tear, making them suitable for a wide range of industrial components and parts. The expansion of numerous industrial sectors, such as manufacturing, construction, and energy, has raised demand for materials such as TPEEs, particularly in emerging economies.

Key Companies & Market Share Insights

The market is highly competitive due to the presence of major industries across the region as these companies are comparatively concentrated and fiercely competitive along with acquisitions, mergers, and collaborations. For Instance, in June 2023, MM Polytrade Ltd announced the acquisition of acquisition of Celanese's business in thermoplastic copolyesters (TPC) and hotmelt polyesters manufactured in the Ferrara Donegani plant, as well as some assets present in the Forl compounding plant, through its existing subsidiary Taro Plast.

Key Thermoplastic Polyester Elastomer Companies:

- SABIC

- DuPont

- A. Schulman

- Teijin Plastics

- BASF SE

- Entec Polymers

- Covestro

- Celanese Corporation

- LG Chemicals

- Mitsubishi Engineering Plastics Corp.

- Arkema

- Chang Chun Group

- TOYOBO CO., LTD

- RadiciGroup

- Sunshine Plastics

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: SABIC, DuPont, BASF SE, Covestro

- Broad thermoplastic elastomer portfolios across automotive, electronics, industrial, consumer goods, and specialty engineering applications.

- Strong investment in lightweight materials, recyclable elastomer systems, and specialty polymer technologies.

- Integrated manufacturing capabilities and global distribution networks supporting large-scale industrial demand.

- Advanced polymer engineering expertise and strong technical development capabilities.

- Established global manufacturing footprint and diversified end-use penetration.

- Strong R&D infrastructure supporting specialty elastomer innovation and application development.

- High exposure to petrochemical feedstock and energy price volatility.

- Significant sustainability and regulatory compliance-related investment requirements.

- Dependence on automotive and industrial manufacturing cycles affects demand consistency.

Emerging Players: A. Schulman, Entec Polymers, Sunshine Plastics

- Focus on customized elastomer compounds, specialty distribution capabilities, and application-specific material solutions.

- Flexible manufacturing and customer-oriented product development strategies supporting regional demand.

- Expansion into niche automotive, industrial, and consumer goods applications requiring tailored elastomer formulations.

- Greater responsiveness to customized customer requirements and specialty applications.

- Strong flexibility in regional market servicing and product modification capabilities.

- Competitive positioning in niche and mid-volume elastomer markets.

- Smaller manufacturing scale and limited global supply infrastructure compared with multinational competitors.

- Lower economies of scale in raw material procurement and production operations.

- Higher dependence on regional market demand and selected customer segments.

Thermoplastic Polyester Elastomer Market Report Scope

Report Attribute

Details

Market size value in 2023

USD 1.59 billion

Revenue forecast in 2030

USD 2.28 billion

Growth rate

CAGR of 5.34% from 2023 to 2030

Base year for estimation

2022

Historical data

2018 - 2021

Forecast period

2023 - 2030

Report updated

October 2023

Quantitative units

Volume in kilotons, revenue in USD million/billion, and CAGR from 2023 to 2030

Report coverage

Volume forecast, revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, end-use, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Netherlands; China; India; Japan; South Korea; Australia; Malaysia; Singapore; Thailand; Vietnam; Brazil; Argentina; Saudi Arabia; UAE; South Africa

Key companies profiled

SABIC; DuPont; A. Schulman; Teijin Plastics; BASF SE; Entec Polymers; Covestro; Celanese Corporation; LG Chemicals; Mitsubishi Engineering Plastics Corp.; Arkema; Chang Chun Group; TOYOBO CO., LTD.; RadiciGroup; Sunshine Plastics.

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional, and segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Thermoplastic Polyester Elastomer Market Report Segmentation

This report forecasts volume and revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2030. For this study, Grand View Research has segmented the global thermoplastic polyester elastomer market report based on type, end-use, and region:

-

Type Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

-

Injection Molding Grade

-

Extrusion Molding Grade

-

Blow Molding Grade

-

-

End-use Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

-

Automotive

-

Electrical & Electronics

-

Industrial

-

Medical

-

Consumer Goods

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

The Netherlands

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

Malaysia

-

Singapore

-

Thailand

-

Vietnam

-

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Pricing Analysis

Delivered comprehensive pricing analysis for thermoplastic polyester elastomers across automotive, electronics, industrial, consumer goods, and specialty engineering applications. The study evaluated polyester feedstock pricing trends, compounding costs, additive pricing structures, regional manufacturing economics, logistics expenses, and specialty elastomer price variations influencing global TPEE market pricing dynamics.

Supported procurement optimization and pricing strategy development. Improved understanding of feedstock cost exposure and regional pricing trends across specialty elastomer categories. Assisted in supplier comparison, margin planning, and raw material risk assessment. Enabled better response to petrochemical price fluctuations and changing industrial demand conditions.

Competitive Benchmarking

Conducted detailed benchmarking analysis of key TPEE manufacturers based on product portfolio breadth, technology capabilities, production capacity, regional presence, sustainability initiatives, end-use penetration, and strategic developments. The assessment compared company positioning across automotive systems, industrial components, electrical insulation, consumer products, and specialty elastomer applications.

Supported competitive intelligence and strategic positioning analysis. Identified technology differentiation, operational strengths, and capability gaps among market participants. Improved understanding of specialty elastomer positioning and customer alignment across industrial sectors. Enabled informed sourcing, partnership, and expansion planning decisions.

Cross-Segmentation

Delivered cross-segment analysis across elastomer type, application, processing technology, end-use industry, and regional demand trends. The study evaluated interactions between automotive lightweighting, industrial automation systems, electrical components, consumer electronics, medical devices, and recyclable elastomer technologies utilizing thermoplastic polyester elastomers.

Improved understanding of high-growth application intersections and emerging revenue opportunities across elastomer markets. Supported product portfolio optimization and targeted commercialization planning. Enabled identification of premium-value application areas and evolving sustainability-driven demand patterns within the TPEE industry.

Frequently Asked Questions About This Report

The global thermoplastic polyester elastomer market size was estimated at USD 1.52 billion in 2022 and is expected to reach USD 1.59 billion in 2023.

The global thermoplastic polyester elastomer market is expected to grow at a compound annual growth rate of 5.34% from 2023 to 2030 to reach USD 2.28 billion by 2030.

The automotive segment dominated the thermoplastic polyester elastomer market with a share of 40.88% in 2022. This is attributable to the high usage of TPEE in seating & windows, passenger airbags, safety belt tensioners, and more.

Some of the key players operating in the thermoplastic polyester elastomer market include SABIC; DuPont; A. Schulman; Teijin Plastics; BASF SE; Entec Polymers; Covestro; Celanese Corporation; LG Chemicals; Mitsubishi Engineering Plastics Corp.; Arkema; Chang Chun Group; TOYOBO CO., LTD.; RadiciGroup; and Sunshine Plastics.

Key factors driving the thermoplastic polyester elastomer market growth include increasing adoption of TPEE for lightweight automobiles, wearable electronics, and expanding medical & healthcare facilities.

The Asia Pacific dominated the thermoplastic polyester elastomer market with a share of 32.35% in 2022. China and India are expected to have a significant market share in the region. The growing manufacturing sector in the region is expected to drive TPEE compound demand in industrial machinery, automotive, packaging, and electrical & electronics industries.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.