- Home

- »

- Animal Health

- »

-

Veterinary Services Market Size & Share Report, 2026-2033GVR Report cover

![Veterinary Services Market (2026 - 2033)Report]()

Veterinary Services Market (2026 - 2033)

Size, Share & Trends Analysis Report by Animal (Companion Animals, Production Animals), by Service (Medical Services, Non-Medical Services), by Region, And Segment Forecasts

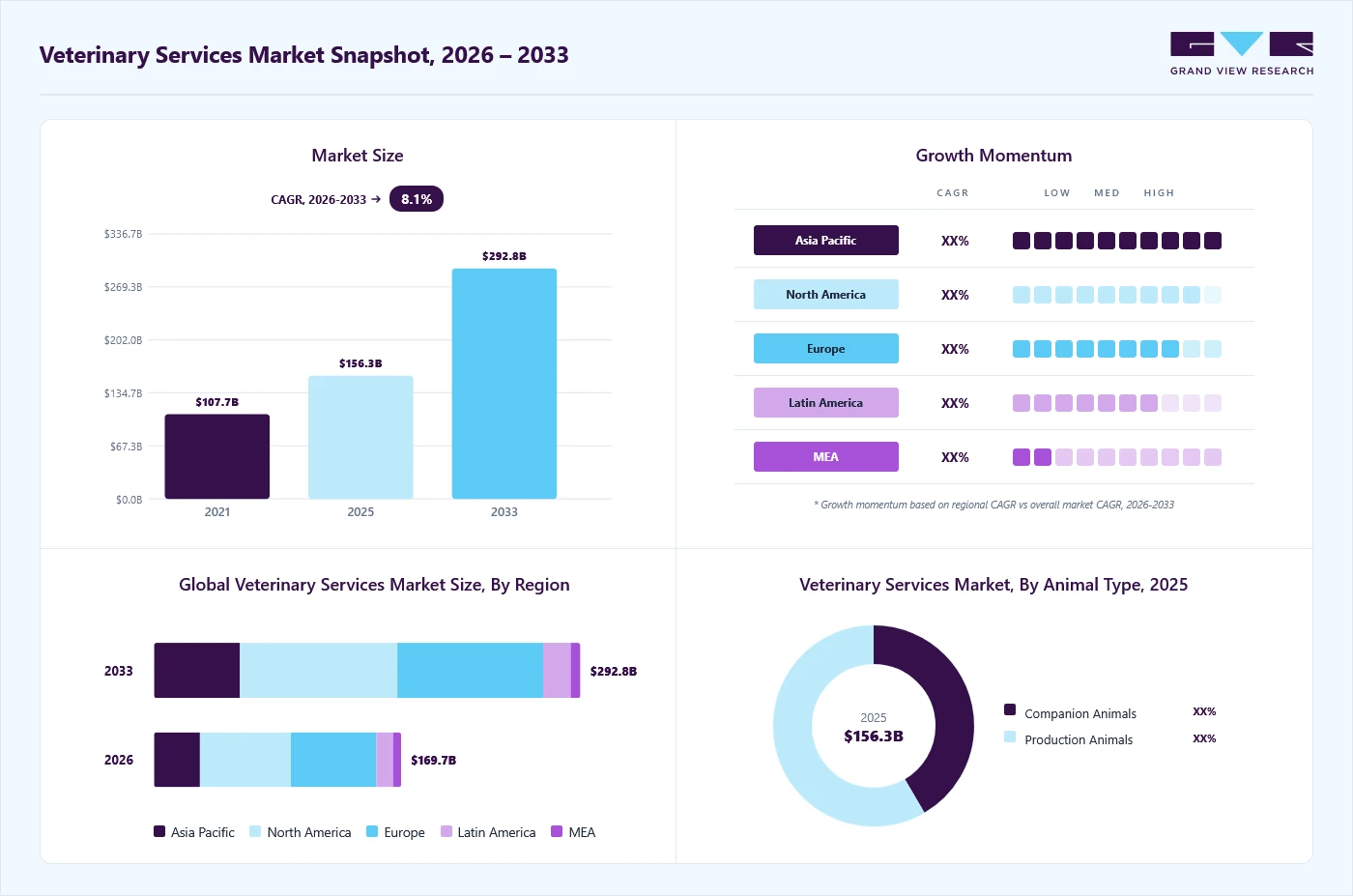

Market Size, 2025

$156.3BMarket Estimate, 2026

$169.7BMarket Forecast, 2033

$292.8BCAGR, 2026–2033

8.1%Veterinary Services Market Summary

The global veterinary services market size was valued at USD 156.3 billion in 2025 and is projected to grow from USD 169.7 billion in 2026 to USD 292.8 billion by 2033, at a CAGR of 8.1% from 2026 to 2033. The North America held the largest share of 36.8% of the global market in 2025. The industry is advancing, driven by rising pet ownership and spending on animal healthcare, rising prevalence of chronic and infectious diseases in pets and livestock, and advancements in diagnostics and treatment technologies.

Key Market Trends & Insights

- By animal: Production animals segment held the largest market share of 58.5% in 2025.

- By service: Medical services segment held the largest market share of 70.4% in 2025.

Regional Highlights

- Largest regional market: North America (36.8% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest share in 2025

Market Size & Forecast

- Market size in 2025: USD 156.3 Billion

- Estimated market size in 2026: USD 169.7 Billion

- Projected market size by 2033: USD 292.8 Billion

- CAGR (2026-2033): 8.1%

Growing demand for preventive care, wellness services, and specialized veterinary expertise is accelerating market growth. For instance, in September 2025, SignalPET introduced SignalPET 360°, a comprehensive radiology solution designed to streamline veterinary diagnostics. The platform integrates AI-powered immediate triage, a complete AI Report modeled after radiologist reports, and 24/7 access to board-certified radiologists, all in one system. By merging AI technology with radiologist expertise, the platform enables clinics to work more efficiently, make more confident decisions, and provide better patient care.")

The veterinary services market is witnessing strong growth, driven by the rapid rise in pet ownership and the increasing focus on preventive healthcare. In 2024, 66% of U.S. households (86.9 million homes) owned a pet, with dogs and cats making up the majority. This surge in pet adoption has driven demand for routine veterinary checkups, diagnostics, and preventive services, as pet owners increasingly view animals as family members. Spending reflects this trend-pet-related expenditures reached USD 150.6 billion in 2024, up from USD 147.0 billion in 2023, with diagnostics gaining a growing share. For example, IDEXX's 2024 survey revealed that 73% of Millennials and 71% of Gen Z pet parents support annual wellness diagnostics, underscoring a generational shift toward proactive health management.

Generation

% of Dog Parents

% Owning Dogs <2 Years Old

% Supporting Annual Diagnostics

Gen Z (≤27 yrs)

24%

48%

71%

Millennials (28-43 yrs)

33%

37%

73%

Gen X (44-59 yrs)

28%

27%

63%

Baby Boomers (60-78 yrs)

15%

15%

57%

Source: IDEXX’s U.S. Pet Owner survey fielded in June 2024

The market is further supported by increasing pet lifespans and the growing healthcare needs of senior animals. IDEXX reported that the average lifespan of dogs rose from 11.6 years in 2010 to 13.4 years in 2024, while cats now live up to 14.4 years on average. With age, diagnostic demand rises significantly-per-patient diagnostic revenue grows from USD 50 in puppies and kittens to USD 170 in geriatric pets, reaching as high as USD 395 in wellness-focused practices. This trend highlights diagnostics' central role in managing chronic and age-related conditions such as kidney disease, cancer, and orthopedic disorders, fueling steady revenue growth for veterinary providers.

Another key driver is expanding pet insurance, which lowers financial barriers to diagnostics. In January 2026, Progressive Insurance launched pet insurance for cats and dogs, offering accident, illness, and optional wellness coverage. It has been available across most U.S. states, with plans averaging USD 47 monthly, helping manage unexpected veterinary expenses. Similarly, the North American Pet Health Insurance Association (NAPHIA) reported that pet insurance premiums surpassed USD 4.27 billion in 2023, reflecting rising demand for comprehensive coverage. Insurance-driven affordability increases uptake of advanced diagnostic tools and strengthens early disease detection and preventive care adoption. In addition to companion animals, equine insurance plans also expand diagnostic coverage for conditions such as lameness and metabolic issues, broadening opportunities within the market.

Market Concentration & Characteristics

The veterinary services market is moderate - highly fragmented with pockets of consolidation, as large corporate groups expand their footprint through acquisitions, while independent clinics and regional practices still hold significant market share. Major players such as Mars Inc. (VCA, Banfield, BluePearl) and CVS Group in the UK have built extensive networks of veterinary hospitals and specialty centers, leveraging scale to invest in advanced diagnostics, technology, and workforce training. However, independent and mid-sized practices continue to dominate rural and local markets, especially in developing regions, sustaining a diverse competitive landscape. This balance between corporate consolidation and independent presence underscores a market structure in which industry concentration is growing but remains far from monopolistic.

The degree of innovation in the veterinary services industry is high, driven by rapid advancements in diagnostics, therapeutics, and digital health solutions, transforming animal care. Precision medicine and advanced technologies, such as 3D printing for custom implants and surgical guides (launched by VCA Animal Hospitals in October 2024), enable more accurate and minimally invasive treatments. Similarly, companies like Zomedica are expanding access to advanced point-of-care diagnostic tools, such as Truforma and VETGuardian, thereby improving clinical efficiency and enabling early disease detection. The adoption of AI-powered telemedicine platforms, wearable monitoring devices, and genetic testing for companion animals is also expanding, aligning with the rising trend of pet humanization. For instance, in April 2026, Napollo Software launched VeterinaryMarketing.ai, an AI-driven platform offering specialized digital marketing for veterinary practices, enhancing patient acquisition through SEO, ads, and social media, addressing growing competition among over 33,000 U.S. clinics.

The level of M&A activity is robust, as companies pursue consolidation, geographic expansion, and access to advanced technologies. Large corporate and private equity firms actively acquire veterinary chains, specialty practices, and pet service providers to strengthen market positioning. For instance, in November 2025, Nestlé Purina PetCare partnered with Ease to expand access to veterinary behavioral support, enabling clinics to connect with board-certified behaviorists, addressing rising pet anxiety issues and improving specialized care availability nationwide. Similarly, in the U.S., Harbour Group’s 2025 acquisition of Senproco and Groomer’s Choice highlights growing interest in complementary non-medical services such as grooming. These deals reflect the industry’s trend toward consolidation, integrated service offerings, and cross-border expansion, driving growth and competitiveness across both companion and production animal segments.

Regulations significantly affect the market, shaping standards for animal health, food safety, and service delivery. Governments and international bodies enforce strict frameworks to control zoonotic diseases, enhance biosecurity, and improve animal welfare, directly influencing demand for veterinary diagnostics, preventive care, and workforce expansion. For instance, in February 2025, India's Union Animal Husbandry and Dairying Ministry, in collaboration with WOAH, launched a public-private partnership initiative to strengthen veterinary services through FMD-free zones, vaccine platform development, and NABL-accredited district labs. Similarly, in Brazil, Ibama mandated Petrobras to establish a veterinary center in Amapá as a condition for offshore drilling approval, reflecting how environmental and animal welfare regulations drive investment in veterinary infrastructure. Such policies safeguard public health and create opportunities for innovation and service expansion within the sector.

The threat of product substitutes in the veterinary services market is moderate, as alternatives such as over-the-counter (OTC) pet medications, telemedicine apps, and nutraceuticals can partially replace traditional in-clinic services. Pet owners increasingly turn to digital health platforms and home diagnostic kits for basic consultations or preventive care, reducing dependency on routine veterinary visits. For instance, the rise of AI-driven telehealth apps like Pawly and Fuzzy Pet Health allows owners to access remote consultations, while advanced nutraceuticals and functional foods by companies like Royal Canin and Hill’s Pet Nutrition support preventive health without clinical intervention. However, complex procedures such as surgeries, advanced diagnostics, and regulatory requirements for livestock health cannot be substituted, keeping veterinary services essential and limiting the overall threat of substitution.

End-user concentration in the market is moderate to high, driven by the dominance of companion animal owners and livestock producers, who collectively account for the bulk of service demand. Companion animal services are concentrated among urban pet owners, where rising pet humanization and higher disposable incomes drive uptake of advanced care, diagnostics, and wellness services. For instance, in April 2026, CodaPet expanded in-home pet euthanasia services in the U.S. by adding a licensed veterinarian, enhancing access to compassionate, end-of-life care that allows pets to pass peacefully in familiar home environments. On the production side, livestock veterinary services remain concentrated among large-scale cattle, poultry, and swine producers, particularly in regions such as Brazil and the U.S., where high protein demand necessitates continuous veterinary oversight. This concentration amplifies the bargaining power of large clients while pushing service providers to scale offerings, adopt innovation, and tailor solutions to meet high-volume livestock producers and increasingly health-conscious pet owners.

Animal Insights

The production animals segment accounted for the largest share of 58.5% in 2025 due to the essential role of veterinary services in ensuring the health, productivity, and biosecurity of livestock such as cattle, poultry, swine, sheep, goats, and aquaculture. Rising global demand for animal protein, coupled with the FAO’s projection that food demand will increase by 70% by 2050, has intensified the need for veterinary interventions to secure high-quality and safe animal-derived products. Preventive care, disease surveillance, and advanced diagnostic services are becoming increasingly important as governments and producers work to mitigate zoonotic disease risks and ensure food safety.

Furthermore, strong institutional support is accelerating the segment’s dominance. For instance, in February 2026, India’s Union Budget 2026 prioritized animal husbandry through expanded veterinary infrastructure, mobile services, LFPO support, strengthening the dairy value chain, and increased funding for vaccination and disease control programs. Such initiatives boost veterinary service demand by expanding infrastructure, increasing preventive care adoption, strengthening rural outreach, creating employment opportunities, and accelerating growth in livestock healthcare, diagnostics, and disease management services.

The companion animals segment is projected to be the fastest-growing in the veterinary services market, due to the sharp increase in global pet ownership and the rising focus on pet health, nutrition, and preventive care. In addition, growing urbanization, smaller household sizes, and the emotional value placed on pets have fueled the trend of pet humanization, where owners treat pets as family members and invest in advanced veterinary treatments, diagnostics, and wellness services. In addition, expanding pet insurance, the availability of specialized services such as oncology, dentistry, and orthopedics, and the rising demand for non-medical services like grooming, daycare, and boarding are driving segment growth. Pet owners' increasing willingness to spend on medical and lifestyle care is positioning the companion animal segment as the key driver of long-term expansion in the global market.

Service Insights

Medical services accounted for the largest share of 70.4% in the market in 2025 due to the rising prevalence of zoonotic diseases and the extensive measures taken worldwide to manage and control outbreaks. Growing pet ownership and heightened awareness of animal health have increased demand for diagnostics, surgeries, and preventive care. Moreover, expanding access to veterinary medical services in developing countries drives higher utilization of core treatments, vaccinations, and emergency interventions. For instance, in January 2025, Schwarzman Animal Medical Center

completed a USD125M expansion, adding advanced specialty facilities, emergency services, and increased capacity, strengthening its position as a leading veterinary teaching hospital. Such expansion highlight enhances advanced veterinary care access, increases specialty service capacity, drives demand for high-end treatments, supports clinical research, and sets benchmarks for infrastructure development in the veterinary services market.

The non-medical services segment is the fastest-growing in the veterinary services industry due to rising demand for pet-focused services such as boarding, grooming, sitting, travel, and funeral care, driven by increasing pet humanization and owner spending. On the livestock side, services such as artificial insemination (AI) are expanding rapidly, with strong government support to improve breeding efficiency and productivity. In addition, major industry players are undertaking strategic initiatives, such as acquisitions, partnerships, and service expansions, to capture this growing demand, further accelerating the segment’s growth trajectory. For instance, in January 2025, Harbour Group, backed by Abacus Finance, acquired Senproco and its distribution arm Groomer's Choice, manufacturers of professional pet grooming products, including shampoos, conditioners, grooming tools, and pet accessories. With well-known brands like Bark2Basics, Green Groom, and Bather Box, Senproco serves thousands of groomers across the U.S., and Harbour Group aims to accelerate its growth through strategic and operational support. This acquisition strengthens the non-medical pet care segment, particularly grooming, which is increasingly integrated into veterinary practices to meet rising demand from pet owners for holistic care.

Regional Insights

North America veterinary services industry held the largest revenue share of 36.8% in 2025, driven by rising pet ownership, expanding service offerings, and strategic investments from industry players. For instance, in January 2026, Human Animal Bond Research Institute partnered with Trupanion to advance research and awareness of the human-animal bond, supporting pet insurance access and highlighting the benefits of service animals for health and well-being. Such a partnership boosts pet insurance adoption, expands awareness of veterinary care benefits, supports service animal demand, and drives growth in pet healthcare and wellness services.

Government-supported initiatives and animal welfare organizations across the U.S. and Canada also contribute to this momentum by implementing programs that enhance access to veterinary services. Expanding new veterinary education programs, including non-traditional accredited training, is expected to reduce shortages and broaden service adoption. While North America continues to dominate the market, the Asia Pacific is projected to be the fastest-growing region, fueled by the rapid rise in pet ownership and livestock populations in developed and emerging economies.

U.S. Veterinary Services Market Trends

The U.S. veterinary services industry is witnessing strong growth, fueled by rising pet ownership, higher spending on pet healthcare, and the growing expansion of veterinary care companies. For instance, in March 2026, Bond Vet surpassed one million pet visits across its clinics, reflecting rapid growth and its mission to expand accessible, convenient, and high-quality veterinary care for pet owners. This strategic milestone highlights rising veterinary demand, supports clinic expansion, increases service accessibility, and strengthens the growth of organized veterinary care networks.

The Canada veterinary services industryis advancing due to increasing government investments and modernization of programs. For instance, in February 2026, initiatives in Northern Ontario strengthen livestock care and agri-food productivity by boosting veterinary services. Similarly, in March 2026, New Brunswick’s shift toward privatization is fostering private sector expansion and innovation. In addition, competitive intensity is increasing as private clinics, corporate chains, and technology-enabled providers compete on accessibility, pricing, and service quality, while addressing veterinarian shortages and rising demand for companion and livestock healthcare services nationwide.

Europe Veterinary Services Market Trends

The veterinary services industry in Europe is expanding rapidly, driven by rising pet humanization, growing demand for advanced treatments, and strong innovation in companion animal healthcare. For instance, in February 2025, Ireland-based TriviumVet advanced first-to-market therapies for chronic conditions in pets, including feline hypertrophic cardiomyopathy (HCM), canine neuropathic pain, gastric ulcers, and chronic kidney disease. These breakthroughs address long-standing gaps in veterinary care, enabling earlier intervention and improving treatment outcomes for veterinarians across Europe.

Such innovations are raising the standard of care, particularly in specialty and chronic disease management, while also boosting the adoption of advanced veterinary pharmaceuticals in the region. As European pet owners increasingly seek high-quality, human-like healthcare for animals, the market is witnessing stronger demand for specialized diagnostic and digital care services. For instance, in April 2025, Rover Group, Inc. expanded in Europe by acquiring Gudog and entering Denmark and Ireland, strengthening its marketplace presence and accelerating growth in digital pet care services.

The UK veterinary services industry is evolving with rising demand for advanced diagnostic and monitoring technologies, driven by strong industry partnerships and innovation. For instance, in September 2025, Zomedica partnered with Pioneer Veterinary Products to distribute its Truforma diagnostic platform and later VETGuardian remote monitoring technology across the UK. This collaboration expands access to innovative tools for small animal and equine care, enhancing diagnostic precision, practice efficiency, and patient outcomes. Similarly, in March 2026, Fi expanded into the UK and EU, launching AI-powered smart collars with GPS and health monitoring. Such an initiative boosts pet wearable adoption, intensifies competition, and accelerates growth in digital pet healthcare markets.

The veterinary services industry in Germany is advancing due to rising cross-border collaborations and innovation through AI-based diagnostics and research. For instance, in March 2026, at the InDeVet Summit, Indo-German collaboration for veterinary education highlighted AI-driven diagnostics, research, and institutional partnerships, fostering innovation, food safety, and One Health solutions through combined technological expertise and large-scale field data. Moreover, Germany’s stringent regulatory framework, aligned with EU animal health, data protection, and clinical standards, ensures high-quality veterinary services, encouraging the adoption of advanced technologies.

Asia Pacific Veterinary Services Market Trends

The veterinary services industry in the Asia Pacific is expected to be the fastest growing region over the forecast period, driven by the region's dependence on agriculture, rising livestock populations, and growing awareness of disease prevention. Increasing cases of zoonotic diseases drive demand for advanced veterinary care, while expanding companion animal ownership boosts the need for pet healthcare services. In Japan, the number of veterinarians focusing on small animals continues to rise, strengthening the companion services segment. Meanwhile, rapid population growth in India fuels demand for meat and milk, accelerating livestock rearing and creating higher demand for veterinary expertise in animal health and productivity.

The India veterinary services industry is expanding rapidly, driven by government initiatives, rising livestock demand, and a booming companion animal sector. For instance, in February 2025, the Union Animal Husbandry and Dairying Ministry, in collaboration with the World Organization for Animal Health (WOAH), conducted a workshop to strengthen veterinary services through public-private partnerships (PPPs). The initiative emphasizes disease control, Foot-and-Mouth Disease (FMD)-free zones, advanced vaccine platforms, workforce training, and district-level NABL-accredited laboratories, which will significantly improve diagnostic capacity, disease management, and private sector participation.

At the same time, India’s growing pet ownership is fueling demand for advanced companion animal healthcare, attracting global and domestic players. For instance, in February 2026, a national conference in Chennai, organized by the Indian Society for Veterinary Medicine and Madras Veterinary College, highlighted AI-driven diagnostics, precision veterinary care, and integration of IoT technologies across India’s animal healthcare ecosystem. Such an initiative accelerates the adoption of AI and digital tools, boosting efficiency, innovation, and demand for advanced veterinary diagnostics and tech-enabled services nationwide.

Latin America Veterinary Services Market Trends

The veterinary services industry in Latin America is experiencing robust growth, driven by the region's large livestock population, rising companion animal ownership, and increasing focus on sustainable animal health practices. Countries like Brazil, with the world's second-largest cattle population, invest heavily in pasture rehabilitation and livestock productivity. For instance, in July 2025, Sumitomo Corporation of America partnered with Grupo Papalotla to scale hybrid pasture seed adoption through its Brazilian subsidiary, Tropical Seeds do Brasil. These innovations improve forage quality, reduce greenhouse gas emissions, and enhance animal productivity, creating new opportunities for veterinary services tied to preventive health, nutrition, and disease management.

At the same time, the companion animal sector in markets such as Argentina and Chile is expanding rapidly, fueled by urbanization and a cultural shift toward treating pets as family. This trend boosts demand for advanced veterinary care, diagnostics, and specialty treatments. The combination of large-scale livestock initiatives and growing pet healthcare adoption positions Latin America as a dynamic market, with veterinary services playing a pivotal role in both agricultural sustainability and companion animal well-being.

The Brazil veterinary services industry is expanding rapidly, driven by the country’s large livestock population and rising investments in animal health infrastructure. For instance, in February 2025, MSD Animal Health partnered with Union Agener Animal Health to co-distribute LACTOTROPIN in Brazil, a biotechnology solution that boosts dairy cow productivity while lowering emissions per liter of milk. Similarly, in April 2025, Petrobras established a veterinary center in Oiapoque, Amapá, as part of its environmental licensing, strengthening capacity for wildlife care in sensitive ecosystems. These examples highlight how agribusiness and environmental initiatives fuel demand for advanced veterinary solutions, positioning Brazil as a key growth hub in Latin America's animal health sector.

Middle East & Africa Veterinary Services Market Trends

The veterinary services industry in the Middle East & Africa is expanding due to increasing livestock production, growing awareness of zoonotic diseases, and rising demand for companion animal care. In South Africa, veterinary services are being strengthened by initiatives to improve surveillance and control of foot-and-mouth disease (FMD), supporting livestock exports and food security. Meanwhile, in markets like the UAE, pet ownership is surging, leading to higher demand for advanced veterinary clinics, grooming, and preventive care services. These trends highlight how both livestock health management and companion animal care are shaping the growth trajectory of the market across the region.

The South Africa veterinary services industry is expanding, driven by rising companion animal ownership, government focus on livestock health, and the integration of advanced clinical standards. For instance, in July 2025, the University of Pretoria’s Onderstepoort Veterinary Academic Hospital, in partnership with Royal Canin, launched Gauteng’s first gold-status Cat-Friendly Clinic, setting international benchmarks in feline care, research, and veterinary education. On the livestock side, state initiatives targeting foot-and-mouth disease (FMD) control and improved biosecurity are strengthening the export competitiveness of South African cattle and sheep. In addition, the enhancement of service accessibility, transparency, and rising digital adoption fuels the country’s growth. For instance, in March 2026, SAVET launched a digital platform in South Africa, offering a verified, centralized database of veterinary clinics, enabling easy access to emergency, specialized, and location-based pet healthcare services nationwide.

The veterinary services industry in Saudi Arabia is expanding rapidly, driven by rising livestock populations, growing pet ownership, and government initiatives under Vision 2030. The Kingdom is home to more than 7.5 million livestock in the Northern Borders region alone, with sheep, goats, camels, and cattle forming the backbone of its food security strategy. This has led to significant investments in animal health infrastructure. For instance, in July 2025, Saudi Arabia began constructing its first National Excellence Center for Animal Research and Disease Control in Arar, with a SAR 29.6 million investment. The facility will span over 17,000 square meters and include veterinary laboratories, barns, refrigeration, and support infrastructure to strengthen diagnostics, disease prevention, and scientific research. Strategically located in the livestock-rich Northern Borders region-home to more than 7.5 million animals-the center will enhance veterinary services, food security, sustainability, and biosecurity, aligning with Vision 2030 goals. The new research hub will modernize veterinary infrastructure, enabling early detection and control of livestock diseases. This strengthens local veterinary capacity, reduces zoonotic risks, and positions Saudi Arabia as a regional leader in animal health innovation.

Key Veterinary Services Company Insights

The market is competitive and largely fragmented, with a significant number of veterinary service providers ranging from small to large. These companies are constantly involved in implementing strategic initiatives, such as collaborations, mergers and acquisitions, and service and regional expansions.

Key Veterinary Services Companies:

The following key companies have been profiled for this study on the veterinary services market.

- CVS Group Plc

- Mars Incorporated

- National Veterinary Associates

- Pets at Home Group PLC

- Greencross Vets

- Fetch! Pet Care

- IVC Evidensia

- A Place for Rover, Inc.

- PetSmart LLC

- Airpets International

Recent Developments

-

In February 2026, GekkoVet and Royal Canin launched AI-driven clinical decision tools in Mexico, enhancing diagnostics, treatment accuracy, and workflow efficiency for veterinary professionals. Such an initiative accelerates AI adoption, improves clinical outcomes, boosts efficiency, and drives demand for tech-enabled veterinary services across Latin America.

-

In December 2025, PetPlusU expanded into China, leveraging AI, IoT, and data analytics to deliver digital pet healthcare solutions, supporting clinics and enhancing personalized care in a rapidly growing pet economy. Such an initiative drives digital transformation, enhances preventive care, and increases demand for AI-based veterinary solutions, strengthening tech-driven service ecosystems in China.

-

In September 2025, SignalPET introduced SignalPET 360°, a comprehensive radiology solution designed to streamline veterinary diagnostics. The platform integrates AI-powered immediate triage, a Complete AI Report modeled after radiologist reports, and 24/7 access to board-certified radiologists, all in one system.

-

In May 2025, Vetanco, a global animal health company, partnered with Saudi Arabia’s Arasco via its veterinary division Al-Emar International, granting Al-Emar exclusive distribution rights for Vetanco’s portfolio in Saudi Arabia.

-

In March 2025, Pet Madness Inc. launched the world's first AI-driven pet ecosystem, integrating software, hardware, and partnerships to connect pet owners, veterinarians, brands, and service providers.

Veterinary Services Market Report Scope

Report Attribute

Details

Market size in 2025

USD 156.3 billion

Estimated market size in 2026

USD 169.7 billion

Projected market size by 2033

USD 292.8 billion

Growth rate

CAGR of 8.1% from 2026 to 2033

Historical Period

2021 - 2024

Actual data

2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Animal, service, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East and Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; Japan; China; India; Australia; South Korea; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait; Qatar; Oman

Key companies profiled

CVS Group Plc; Mars Incorporated; National Veterinary Associates; Pets at Home Group PLC; Greencross Vets; Fetch! Pet Care; IVC Evidensia; A Place for Rover, Inc.; PetSmart LLC; Airpets International

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Veterinary Services Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global veterinary services market report based on animal, service, and region.

-

Animal Outlook (Revenue, USD Million, 2021 - 2033)

-

Companion Animals

-

Dogs

-

Cats

-

Horses

-

Others

-

-

Production Animals

-

Cattle

-

Poultry

-

Swine

-

Others

-

-

-

Service Outlook (Revenue, USD Million, 2021 - 2033)

-

Medical Services

-

Diagnosis

-

In-Vitro Diagnosis

-

In-Vivo Diagnosis

-

-

Preventative Care

-

Treatment

-

Consultation

-

Surgery

-

Others

-

-

-

Non-Medical Services

-

Pet Services

-

Livestock Services

-

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

India

-

China

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

Qatar

-

Oman

-

-

Frequently Asked Questions About This Report

Some key players operating in the global veterinary services market include CVS Group Plc; Mars Incorporated; National Veterinary Associates; Pets at Home Group PLC; Greencross Vets; Fetch! Pet Care; IVC Evidensia; A Place for Rover, Inc.; PetSmart LLC; Airpets International, among others.

Some of the key factors propelling the market growth includes, increasing animal welfare activities, rising need to enhance food security, increasing pet populations, growing awareness about animal health coupled with growing timely diagnosis & treatments, and increasing expenditure on animal healthcare services.

Asia Pacific is the fastest-growing region over the forecast period.

The production animals segment led with a 58.5% revenue share in 2025, while the companion animals segment is the fastest-growing.

The medical services segment led with a 70.4% revenue share in 2025, while the non-medical services segment is the fastest-growing.

North America veterinary services market held the largest revenue share of 36.8% in 2025, driven by rising pet ownership, expanding service offerings, and strategic investments from industry players. In addition numerous measures undertaken by government & animal welfare organizations inclined towards improving veterinary services are further supporting the substantial share.

The global veterinary services market size was estimated at USD 156.3 billion in 2025 and is expected to reach USD 169.7 billion in 2026.

The global veterinary services market is expected to grow at a compound annual growth rate (CAGR) of 8.1% from 2026 to 2033 to reach USD 292.8 billion by 2033.

About the Author(s)

Animal Health Research Team

Healthcare · Animal HealthThis report was authored by the animal health research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the animal health segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.