- Home

- »

- Next Generation Technologies

- »

-

Wires And Cables Market Size, Share, Industry Report, 2033GVR Report cover

![Wires And Cables Market Size, Share & Trends Report]()

Wires And Cables Market (2026 - 2033) Size, Share & Trends Analysis Report By Voltage (Low, Medium, High, Extra-High), By Installation (Overhead, Underground), By End Use (Aerospace & Defense, Building & Construction, Oil & Gas), By Region, And Segment Forecasts

Market Size, 2025

$230.9BMarket Estimate, 2026

$240.4BMarket Forecast, 2033

$313.1BCAGR, 2026–2033

3.8%Wires And Cables Market Summary

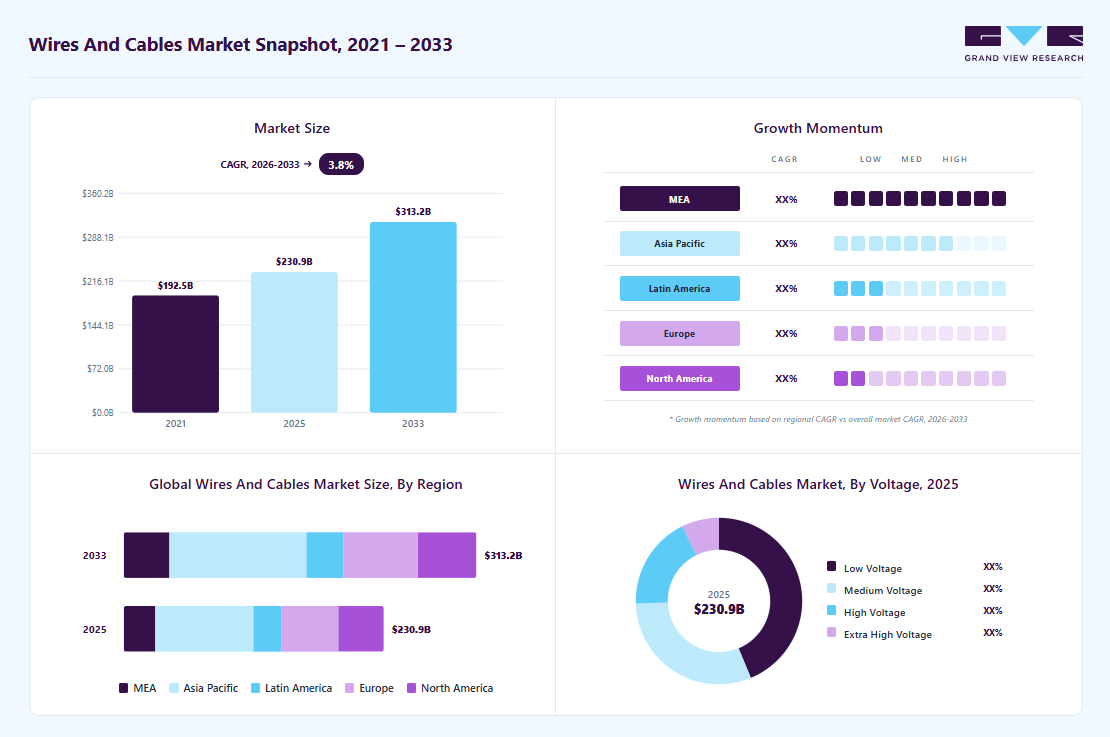

The global Wires And Cables market size was valued at USD 230.9 billion in 2025 and is projected to grow from USD 240.4 billion in 2026 to USD 313.1 billion by 2033, at a CAGR of 3.8% from 2026 to 2033. Asia Pacific dominated the global Wires And Cables market with the largest revenue share of 37.8% in 2025. The market is expanding due to increased investments in power cable infrastructure and grid modernization, the expansion of fiber-optic networks for telecommunications and data center connectivity, and the rising deployment of renewable energy cables and smart grid infrastructure.

Key Market Trends & Insights

- By voltage: Low voltage (LV) segment led the market with the largest revenue share of 43.75% in 2025.

- By installation: Overhead segment led the market with the largest revenue share of 63.62% in 2025.

- By end use: Automotive segment is expected to grow at the fastest CAGR of 4.7% from 2026 to 2033.

Regional Highlights

- Largest regional market: Asia Pacific (37.8% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 230.9 Billion

- Estimated market size in 2026: USD 240.4 Billion

- Projected market size by 2033: USD 313.1 Billion

- CAGR (2026-2033): 3.8%

Additional drivers include increasing demand for electric vehicle wiring and automotive electrification, expanding use of low-, medium-, and high-voltage cables across construction and industrial sectors, and rising adoption of underground and submarine cable systems for reliable power transmission.

The wires and cables industry is witnessing strong momentum driven by the rapid expansion of renewable energy and power infrastructure. Increasing investments in solar and wind power projects are accelerating demand in the power cable market and the broader electrical wire and cable industry. Governments are prioritizing smart grid infrastructure and grid modernization to improve electricity transmission efficiency. This development is driving significant deployment of high voltage cable, medium voltage cable, and extra high voltage cable systems for large-scale power transmission. As renewable energy capacity continues to expand, the global wire and cable market size and forecast indicate rising demand for advanced transmission cables.

")

The increasing demand for digital infrastructure is creating significant growth opportunities in the global wire and cable industry. Rising adoption of cloud computing, artificial intelligence, and digital services is accelerating investments in data center cable infrastructure and high-capacity communication networks. Large-scale data centers require advanced fiber optic cables and structured cabling systems to support high-speed data transmission and reliable connectivity. Increasing internet penetration and enterprise digitalization are further driving fiber optic network expansion across telecommunications infrastructure. As digital transformation continues globally, this trend is strengthening the growth outlook of the wire and cable industry analysis and supporting long-term market growth.

The growing demand for large-scale infrastructure development is emerging as a major growth catalyst for the global wire and cable industry. Increasing investments in roads, railways, metro networks, and airports are significantly driving the need for advanced electrical wire and cable market solutions. Governments are focusing on improving transportation connectivity and logistics infrastructure, which requires extensive deployment of power cables, low voltage cables, and communication cables across infrastructure projects. Rapid urbanization and smart city initiatives are further accelerating the installation of building wires and underground cables in modern construction projects. As global infrastructure investments continue to expand, the wire and cable market growth is expected to strengthen with rising demand for reliable and high-performance cable systems.

Voltage Insights

The low voltage segment led the market with the largest revenue share of 43.75% in 2025. Increasing urbanization demands reliable power distribution in dense areas, where low voltage wires and cables provide essential mechanical protection through steel wire armour (SWA) and aluminium wire armour (AWA) for direct burial installations. For instance, in December 2025, ABB introduced Kabeldon NXT, a cable distribution cabinet designed for utility low voltage systems with a 29% reduced carbon manufacturing footprint. The cabinet uses low-carbon steel made with 100% renewable energy and 75% recycled materials, reducing CO2 emissions by 78 kg during production.

The extra high voltage segment is expected to grow at the fastest CAGR during the forecast period, owing to the increasing demand for long-distance power transmission and large-scale grid interconnection projects. The power cable market is expanding as utilities deploy extra high voltage cables to support renewable energy integration and cross-regional electricity transmission. Technological advancements in insulation materials and high-temperature superconductors are improving efficiency, reliability, and predictive maintenance capabilities in modern transmission networks. For instance, in July 2025, Nexans and RTE collaborated to recycle aluminum from power cables used in France’s electricity transmission network. The recycled aluminum is reused to manufacture new cables for high and extra-high voltage lines, supporting sustainable infrastructure development and strengthening the market growth.

Installation Insights

The overhead segment accounted for the largest market revenue share in 2025, driven by the growing growth of the power transmission and distribution infrastructure across global utility networks. Overhead installation techniques remain the most widely adopted due to their cost-effectiveness, ease of deployment, and suitability for long-distance electricity transmission. Utilities and energy providers continue to deploy overhead power cables and transmission lines to support expanding electricity demand and grid connectivity. For instance, in November 2025, Sumcab launched tough ground and overground cables designed to support direct underground trench installation in various soil conditions. These cables offer high durability, resisting rodent damage, water exposure, low temperatures, crushing, and abrasion, with impact resistance of up to 35 joules.

The underground segment is projected to grow at the fastest CAGR during the forecast period, driven by the increasing demand for reliable power distribution across the global wire and cable market. The deployment of underground cables is rising as utilities focus on reducing transmission losses, improving grid reliability, and lowering long-term maintenance costs in dense urban environments. Rapid urbanization and expanding smart grid infrastructure are further accelerating the adoption of underground power cable installations across the electrical wire and cable industry. In addition, the expansion of data center cable infrastructure and fiber optic network expansion is increasing demand for secure underground cabling systems. For instance, in August 2025, ABB introduced advanced electrical solutions designed to improve scalability and installation efficiency, supporting growing digital infrastructure and strengthening market growth globally.

End Use Insights

The energy and power segments accounted for the largest market revenue share in 2025. The growing demand for efficient electricity transmission and distribution is significantly driving expansion in the global wire and cable market. Utilities are increasingly upgrading aging grid infrastructure by shifting from conventional transmission lines to high voltage cable and extra high voltage cable systems to reduce transmission losses and improve power efficiency. Rising investments in renewable energy projects and smart grid infrastructure are further accelerating the deployment of advanced power cables across the electrical wire and cable industry. For instance, in December 2024, NKT collaborated with ABB Distribution Solutions to provide electrical infrastructure for expanding its high-voltage submarine power cable factory in Karlskrona, Sweden. The expansion will enable the facility to produce sufficient cables to connect offshore wind farms with a combined capacity of 20 GW, supporting the market growth and global renewable energy integration.

The automotive segment is projected to grow at the fastest CAGR over the forecast period, rising demand driven by the increasing adoption of electric vehicles (EVs) and hybrid vehicles across the global automotive industry. The transition toward vehicle electrification is accelerating the deployment of advanced electric vehicle wiring, high-performance power cables, and automotive wiring harness systems for battery packs, powertrains, and charging infrastructure. Growing investments in EV charging networks and smart mobility infrastructure are further strengthening demand across the electrical wire and cable industry. In addition, lightweight and high-efficiency cable technologies are being developed to improve vehicle performance and energy efficiency. For instance, in March 2025, BMW Group Plant Debrecen in Hungary advanced assembly line operations for the Neue Klasse architecture, incorporating modularization and a zonal wiring harness that uses 600 fewer meters of wiring and weighs 30% less than previous generations.

Regional Insights

The wires and cables market in North America is primarily driven by rising investments in power transmission and smart grid infrastructure to modernize aging electricity networks. The increasing deployment of fiber-optic cables and data center cable infrastructure to support cloud computing, artificial intelligence, and high-speed connectivity is further accelerating wire and cable market growth in the region. In addition, the expansion of renewable energy projects and electric vehicle charging infrastructure is strengthening demand across the power cable market and the broader electrical wire and cable industry.

Asia Pacific Wires And Cables Market Trends

Asia Pacific dominated the global wires and cables market with the largest revenue share of 37.85% in 2025 and is projected to grow at a significant CAGR during the forecast period, owing to rapid industrialization and large-scale infrastructure development across emerging economies in the region. The market growth is driven by increasing investments in power transmission infrastructure, underground cable installations, and smart grid infrastructure to support rising electricity demand and urban expansion. In addition, the expansion of data center cable infrastructure and fiber-optic networks, driven by digital transformation and telecom network upgrades, is further accelerating market growth across the region.

The wires and cables market in China accounted for the largest market revenue share in the Asia Pacific in 2025, driven by expanding power transmission infrastructure and renewable energy integration across the country. The increasing deployment of underground, high-voltage, and smart grid infrastructure to support rising electricity demand is further strengthening the power cable market. In addition, rapid fiber-optic network expansion and the development of data center cable infrastructure, driven by digitalization and 5G deployment, are accelerating overall wire and cable market growth.

Europe Wires And Cables Market Trends

The wires and cables market in Europe is driven by the increasing adoption of renewable energy infrastructure and smart grid modernization, as well as stringent energy efficiency regulations. The region is witnessing rising demand from the automotive sector, particularly due to the rapid expansion of electric vehicle wiring and EV production. In addition, investments in data center cable infrastructure, fiber-optic network expansion, and upgrades to aging power transmission networks across countries such as Germany, France, and the UK are accelerating wire and cable market growth.

Key Wires And Cables Company Insights

Some key companies in the wires and cables industry are American Wire Group, Nexans,KEI Industries Ltd., Sumitomo Electric Industries, Ltd.

-

KEI Industries manufactures a range of electrical wires and cables, including EHV up to 400 kV, medium voltage, low voltage power cables, control and instrumentation cables, rubber cables, house wiring, and stainless steel wires. Operations extend to domestic retail, institutional, and export segments, serving power utilities, infrastructure, railways, refineries, petrochemicals, mining, cement, and steel sectors. KEI also provides end-to-end EPC services for turnkey power transmission and distribution projects, encompassing engineering, procurement, construction, and commissioning.

-

Sumitomo Electric Industries operations comprise product development, manufacturing of electric wires and cables, optical fiber cables, automotive wiring harnesses, compound semiconductors, cutting tools, and anti-vibration rubber components. Operates across five primary business segments: automotive, info communications, electronics, environment & energy, and industrial materials & others. Business activities support energy infrastructure, telecommunications networks, automotive production, and advanced materials applications globally.

Key Wires And Cables Companies:

The following key companies have been profiled for this study on the wires and cables market.

- American Wire Group

- Amphenol TPC.

- Belden Inc.

- Encore Wire Corporation

- Finolex Cables.

- Fujikura Ltd.

- Furukawa Electric Co., Ltd.

- KEI Industries Limited.

- LEONI AG

- LS Cable & System Ltd.

- Nexans

- NKT A/S

- Prysmian S.p. A

- Sumitomo Electric Industries Ltd.

- Southwire Company, LLC

Recent Developments

-

In January 2026, RR Kabel launched a new range of future-ready wires designed to address the increasing electrical load and safety requirements in modern homes. The company introduced advanced products such as Superex Green HR+FR and Firex LS0H-EBXL, offering improved heat resistance and enhanced fire safety. These wires feature advanced insulation technologies that help withstand higher temperatures and reduce smoke emission during fire incidents. The launch reflects the company’s focus on providing safer and more reliable wiring solutions for residential infrastructure.

-

In December 2025, LS Cable & System India launched 400 kV EHV cables and HTLS overhead conductor solutions, which complement its comprehensive cable-system portfolio which includes joints, terminations and related materials enabling end-to-end supply from engineering through implementation.

-

In July 2025, Sumitomo Electric Industries, Ltd. began installing a 525 kV XLPE high-voltage DC wires and cable system. The contract from transmission operator Amprion covers roughly 300 km of HVDC cables linking the converter stations in Petkum (Emden) and Osterath near Düsseldorf, representing a project value of more than EUR 500 million.

-

In June 2025, Sumitomo Electric Industries started installing a high-voltage underground cable system in Germany called the Corridor A-Nord project. They are taking care of everything from designing and making the cables to delivering, installing, connecting, testing, and maintaining nearly 300 kilometers of cable.

-

In April 2024, Encore Wire entered a definitive merger agreement with Prysmian, under which Prysmian acquired all outstanding shares of Encore Wire common stock. Encore Wire manufactures copper and aluminum electrical wire and cables for power generation and distribution at its vertically integrated Texas campus. The transaction expands Prysmian's North American operations and product portfolio while maintaining Encore Wire's McKinney facility.

Wires And Cables Market Report Scope

Report Attribute

Details

Market size in 2025

USD 230.9 billion

Estimated market size in 2026

USD 240.46 billion

Projected market size by 2033

USD 313.19 billion

Growth rate

CAGR of 3.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Voltage, installation, end use, regional

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

American Wire Group; Amphenol TPC.; Belden Inc.; Encore Wire Corporation; Finolex Cables.; Fujikura Ltd.; Furukawa Electric Co., Ltd.; KEI Industries Limited.; LEONI AG; LS Cable & System Ltd.; Nexans; NKT A/S; Prysmian S.p. A; Sumitomo Electric Industries, Ltd.; Southwire Company, LLC

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Wires And Cables Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global wires and cables market report based on voltage, installation, end use, and region.

-

Voltage Outlook (Revenue, USD Billion, 2021 - 2033)

-

Low Voltage (LV)

-

Medium Voltage (MV)

-

High Voltage (HV)

-

Extra-High Voltage (EHV)

-

-

Installation Outlook (Revenue, USD Billion, 2021 - 2033)

-

Overhead

-

Underground

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Aerospace and Defense

-

Building & Construction

-

Oil and Gas

-

Energy and Power

-

IT & Telecommunication

-

Automotive

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The global wires and cables market was estimated at USD 230.9 billion in 2025 and is expected to reach USD 240.4 billion in 2026.

The global wires and cables market is expected to witness a compound annual growth rate of 3.8% from 2026 to 2033, reaching USD 313.1 billion by 2033.

The Asia Pacific dominated the wires and cables market with a share of over 37.8% in 2025.

Key players operating in the wires & cables market are American Wire Group; Belden Inc.; Encore Wire Corporation; Fujikura Ltd.; KEI Industries Limited; LS Cable & System Ltd.; Nexans; NKT A/S, Prysmian S.p. A; Sumitomo Electric Industries Ltd.

Key factors that are driving the wires & cables market growth include the implementation of smart grid technology has met the increasing need for grid interconnections, thus resulting in rising investments in the new underground and submarine cables.

The low voltage segment accounted for the largest revenue share of over 43% in the wires & cables market in 2025, owing to the high usage of low voltage cables in building wires, LAN cables, appliance wires, distribution networks, and others.

Energy and power held the largest revenue share in 2025, while automotive is the fastest-growing area.

The overhead segment held the largest share in 2025, and underground is the fastest-growing market.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.