- Home

- »

- Plastics, Polymers & Resins

- »

-

3D Printing Plastics Market Size & Share Report, 2026-2033GVR Report cover

![3D Printing Plastics Market (2026 - 2033)Report]()

3D Printing Plastics Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (Photopolymers, ABS & ASA, Polyamide/Nylon), By Form (Filament, Ink, Powder), By End Use (Automotive, Medical, Aerospace & Defense, Consumer Goods), By Region, And Segment Forecasts

Market Size, 2025

$1.5BMarket Estimate, 2026

$1.8BMarket Forecast, 2033

$9.6BCAGR, 2026–2033

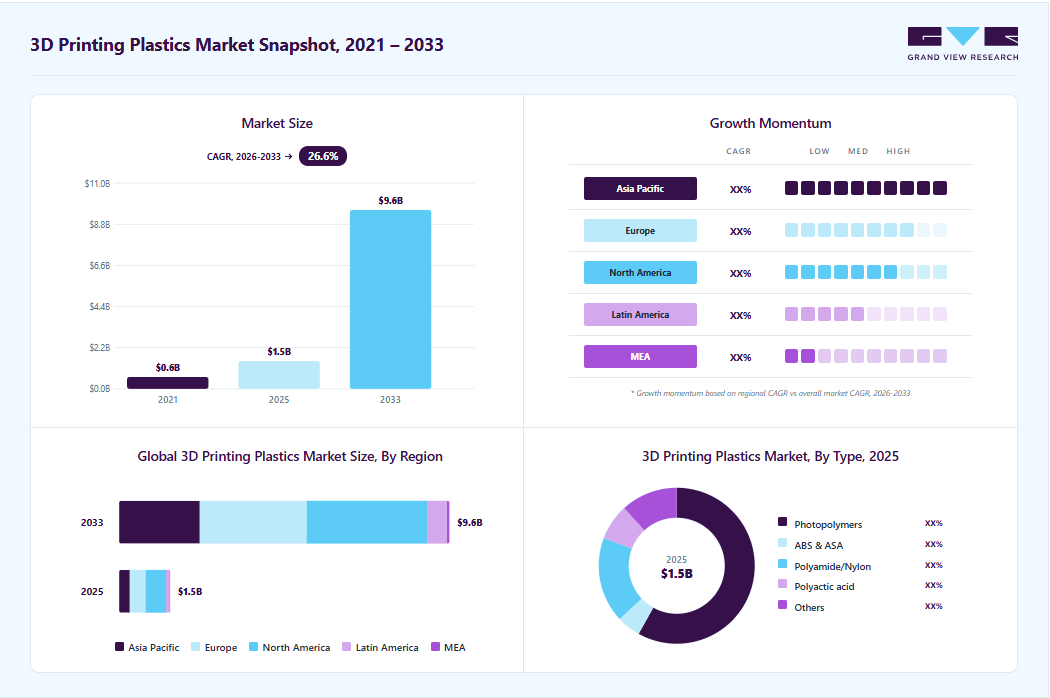

26.6%3D Printing Plastics Market Summary

The global 3d printing plastics market size was valued at USD 1.5 billion in 2025 and is projected to grow from USD 1.8 billion in 2026 to USD 9.6 billion by 2033, at a CAGR of 26.6% from 2026 to 2033. The market in North America dominated with a revenue share of 39.9% in 2025. The growing demand for customized and personalized products drives innovation in the 3D printing industry, leading to an increased need for 3D printing plastics.

Key Market Trends & Insights

- By type: Photopolymers segment held the largest market share of 58.1% in 2025.

- By form: Filament segment held the largest market share of 71.8% in 2025.

- By end use: Medical segment held the largest market share of 49.8% in 2025.

Regional Highlights

- Largest regional market: North America (39.9% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 1.5 Billion

- Estimated market size in 2026: USD 1.8 Billion

- Projected market size by 2033: USD 9.6 Billion

- CAGR (2026-2033): 26.6%

A major trend in the 3D printing plastics market is the rising adoption of sustainable materials such as bio-based polylactic acid (PLA) and recycled PETG (rPETG), which support circular manufacturing goals. PLA remains the dominant bio-based polymer, derived from renewable feedstocks such as corn and sugarcane, and is widely preferred for its lower carbon footprint and ease of processing. At the same time, demand for rPETG is increasing as manufacturers focus on reducing virgin polymer use and improving material recovery rates. These materials are widely used in prototyping, functional mechanical parts, consumer goods, and medical applications, strengthening sustainability across the additive manufacturing value chain.")

Key drivers in the 3D Printing Plastics Market include rising adoption across automotive, aerospace & defense, and healthcare industries for functional prototyping and end-use components. Growing electric and hybrid vehicle production, supported by sustainability regulations, is increasing demand for lightweight and durable printed plastic parts. Automation in automotive manufacturing is further supporting material consumption. Rapid industrialization and expanding commercial vehicle production are also contributing to market growth. In aerospace & defense, higher defense spending and robust demand in civil aviation are driving demand for advanced lightweight components. Healthcare applications such as dental aligners, custom implants, and ergonomic tools are expanding due to increasing demand for product customization and faster production cycles.

Technological advancements are accelerating the development of high-performance 3D printing plastics with improved strength, thermal stability, flame resistance, and lightweight properties. Manufacturers are focusing on engineering-grade polymers to support demanding industrial applications. Increasing adoption of additive manufacturing is reducing material waste, tooling requirements, and production lead times, particularly for low-volume and complex parts. Automation and digital workflow integration are improving manufacturing precision and operational efficiency. Sustainability initiatives are also encouraging the use of recycled and bio-based printing materials. Smart manufacturing trends and advancements in material engineering are further expanding the application scope of 3D printing plastics across industrial and consumer sectors.

Market Dynamics

The growing adoption of lightweight materials in the automotive and aerospace industries is a major driver of the 3D Printing Plastics Market. Manufacturers increasingly use 3D printing plastics to reduce component weight, improve fuel efficiency, and enhance design flexibility. In the automotive sector, rising production of electric and hybrid vehicles, supported by government sustainability regulations, is increasing demand for advanced printable polymers for interior parts, battery housings, and prototyping applications. Expanding automation in automotive manufacturing is further accelerating the adoption of additive manufacturing technologies. Rapid industrialization and growth in commercial vehicle production for logistics and supply chain operations are also supporting market expansion.

The aerospace and defense sector is emerging as a key growth area for 3D-printed plastics, driven by rising investments in advanced manufacturing technologies. Rising global defense budgets are driving demand for lightweight, high-performance plastic components for unmanned aerial vehicles, aircraft interiors, and defense equipment. At the same time, the recovery of the civil aviation industry is increasing aircraft production rates and new aircraft orders, creating strong demand for additive manufacturing materials. Aerospace manufacturers are increasingly adopting 3D-printed plastics to reduce material waste, shorten production cycles, and enable complex part geometries, improving operational efficiency.

High-emission and toxic plastics play a key role as a restraint in the 3D Printing Plastics Market due to increasing environmental and workplace safety concerns. Materials such as ABS release high levels of volatile organic compounds and ultrafine particles during the printing process, including styrene and ethylbenzene, which are associated with respiratory and health risks. Polycarbonate-based filaments also face scrutiny because of BPA-related toxicity concerns under high-temperature processing conditions. Regulatory pressure on industrial emissions and indoor air quality standards is increasing compliance costs for manufacturers. Standard PLA and PETG remain comparatively safer alternatives, but performance limitations restrict their adoption in high-temperature and engineering-grade applications.

Market Concentration & Characteristics

The market is in the medium-growth stage, with growth accelerating. The market is fragmented, with key players dominating the industry landscape. Major companies such as 3D Systems Corporation, Arkema Inc., Envisiontec Inc., Stratasys Ltd., SABIC, Materialse nv, HP INC., Eos GmbH Electro Optical Systems, PolyOne Corporation, Royal DSM N.V., and others play a significant role in shaping market dynamics. These leading players often drive innovation by introducing new products, technologies, and materials to meet the industry's evolving demands.

The market for 3D printing plastics is marked by significant innovation and an increasing frequency of mergers and acquisitions, driven by ongoing developments in high-performance polymers, recyclable materials, bio-based filaments, and industrial-grade additive manufacturing technologies. Industry players are investing heavily in research and development, forming strategic partnerships, pursuing acquisitions, and engaging in initiatives to broaden their technology capabilities in order to enhance their material offerings, improve production efficiencies, and widen their footprint in sectors such as aerospace, automotive, healthcare, and industrial manufacturing.

Regulatory measures concerning sustainability, emissions reduction, recyclability, and material safety are progressively impacting product development and manufacturing practices in the 3D printing plastics sector. Simultaneously, the market contends with competition from traditional manufacturing techniques like injection molding and CNC machining, as well as alternative additive manufacturing materials such as metals and ceramics. The end-user market remains somewhat concentrated, with key sectors including aerospace, healthcare, automotive, and industrial, which represent a substantial portion of demand driven by the growing need for lightweight components, tailored products, and rapid prototyping techniques.

Type Insights

The photopolymers segment led the 3D printing plastics market by type in revenue terms, holding a 58.1% share in 2025. It is expected to expand at a CAGR of 25.8% from 2026 to 2033. Growth is supported by the rapid expansion of the healthcare and dental segment. Demand is increasing for applications such as dental aligners, crowns, surgical guides, hearing aids, and biocompatible implants, where high precision and customization are critical. Market growth is also driven by rising adoption in the automotive sector, where photopolymer materials are widely used for rapid prototyping, design verification, assembly testing, and the production of lightweight components. Increasing focus on faster product development cycles and cost-efficient manufacturing is further supporting demand across industrial applications.

The Polyamide/Nylon segment is expected to expand at a CAGR of 31.4% during the forecast period. Growth is supported by rising demand for high-performance polymers in electric vehicle components and advanced electrical systems. The growing use of polyamide materials in battery housings, under-the-hood parts, and thermal management systems is driving market expansion. High-performance PA grades offer strong heat resistance, dimensional stability, and long service life under continuous thermal stress. In addition, growing adoption of PA6 and PA66 in electrical connectors, switches, circuit breaker housings, and consumer electronics is strengthening demand. Their superior insulation properties, mechanical strength, and compatibility with precision 3D printing processes are improving application potential across industrial and electronics sectors.

Form Insights

The filament segment led the 3D printing plastics market by form in revenue terms, holding a 71.8% share in 2025. It is expected to expand at a CAGR of 27.3% from 2026 to 2033. Growth is supported by rising demand from the healthcare and dental sectors, where filament-based materials are increasingly used for anatomical models, surgical planning tools, dental prototypes, and customized medical devices. Market expansion is further driven by strong adoption of desktop and industrial FDM printing systems, driven by lower material costs, ease of processing, and wide material availability. Increasing use in prototyping, educational applications, and low-volume manufacturing is also supporting segment growth across key end-use industries.

End Use Insights

The medical segment dominated the market by end use, contributing 49.8% of total revenue in 2025, and is projected to expand at a CAGR of 29.2% from 2026 to 2033. Growth is supported by the increasing use of 3D printing plastics in diagnostic imaging systems and surgical equipment, where high precision, biocompatibility, and sterilization resistance are critical. Materials such as ABS, polycarbonate, and medical-grade photopolymers are gaining adoption in MRI components, surgical guides, and customized medical tools. In addition, rising demand for patient-specific dental applications is accelerating material consumption across dental laboratories. Customized aligners, dentures, crowns, and implants produced through additive manufacturing are replacing conventional standardized solutions. This trend is strengthening demand for advanced 3D printing plastics across healthcare and dental manufacturing applications.

The aerospace & defense segment is expected to record a robust CAGR of 26.3% during the forecast period. Growth is driven by increasing adoption across aerospace, defense, and space applications. Commercial aviation remains a key consumer, with rising use of 3D printed plastics in engine brackets, cabin interiors, and lightweight structural components. Defense and space programs also support demand through applications in UAVs, propulsion systems, satellites, and missile structures. In addition, the technology enables topology optimization, helping manufacturers reduce component weight and improve fuel efficiency and operational performance. Rapid prototyping and faster production cycles further accelerate adoption. Cost advantages from reduced tooling and economical low-volume production also strengthen market growth.

Regional Insights & Trends

The North America 3D printing plastics industry is growing as the rising trend toward on-demand manufacturing and rapid prototyping is a key driver for the regional market. Companies in industries like aerospace, automotive, and healthcare are increasingly adopting 3D printing to reduce lead times, minimize material waste, and produce high-performance plastic parts with intricate designs. This is supported by the region’s strong ecosystem of 3D printing service providers and material manufacturers, which offer a wide range of specialized plastics, including Nylon, ABS, and PEEK. North America's focus on technological innovation, combined with government support for advanced manufacturing, is further boosting the demand for 3D printing plastics in various industrial applications.

U.S. 3D Printing Plastics Market Trends

The 3D printing plastics industry in the U.S. is being driven by the strong adoption of 3D printing in the healthcare and aerospace industries, where precision and customization are critical. Medical applications, including the production of patient-specific implants, prosthetics, and surgical tools, are rapidly expanding, with biocompatible, durable plastics such as PLA and PEEK playing a central role. In aerospace, 3D printing is being used to create lightweight, heat-resistant components that reduce fuel consumption and enhance performance. The U.S. government’s focus on maintaining technological leadership, along with the presence of leading 3D printing companies in the country, further amplifies the market's expansion.

Asia Pacific 3D Printing Plastics Market Trends

The 3D printing plastics industry in the Asia Pacific is expected to witness the fastest growth of 29.5% over the forecast period, driven by rapid industrialization and the increasing adoption of advanced manufacturing technologies in countries such as China, India, and Japan. Governments across the region are heavily investing in 3D printing technology as part of broader initiatives to modernize manufacturing and strengthen local industries. This growth is further supported by the rising demand for 3D printed products in sectors such as electronics, automotive, and healthcare, where high-performance plastic materials are used to create lightweight, complex components. Besides, the expansion of small and medium enterprises (SMEs) utilizing 3D printing technology for customized production is accelerating market growth across the region.

The China 3D printing plastics industry is being driven by the country's rapid advancements in manufacturing technologies and its ambition to become a global leader in 3D printing. The Chinese government is actively promoting 3D printing as part of its "Made in China 2025" initiative, which aims to upgrade the country's manufacturing capabilities. This has led to a surge in demand for 3D printing plastics in sectors such as electronics, consumer goods, and construction, where manufacturers are using 3D printing to create high-quality, complex products more efficiently. The availability of low-cost raw materials and strong local supply chains further support the widespread adoption of 3D printing plastics in China.

Europe 3D Printing Plastics Market Trends

The 3D printing plastics industry in Europe is growing due to the growing emphasis on sustainability and the circular economy. European manufacturers are increasingly adopting eco-friendly materials such as biodegradable and recycled plastics in their 3D printing processes to meet stringent environmental regulations. Sectors like automotive and aerospace are also leveraging 3D printing to produce lightweight components that help reduce emissions and enhance fuel efficiency. Additionally, Europe’s strong focus on research and development in advanced materials, combined with the region’s robust industrial base, is fostering innovation in 3D printing plastics, further driving market growth.

Key 3D Printing Plastics Company Insights

The 3D printing plastics industry is highly competitive, with several key players dominating the landscape. Major companies in the market include 3D Systems Corporation, Arkema Inc., Envisiontec Inc., Stratasys Ltd., SABIC, Materialse nv, HP INC., Eos GmbH Electro Optical Systems, PolyOne Corporation, Royal DSM N.V. The 3D printing plastics industry is characterized by a competitive landscape with several key players driving innovation and market growth. Major companies in this sector are investing heavily in research and development to enhance the performance, cost-effectiveness, and sustainability of their products.

Key 3D Printing Plastics Companies:

The following key companies have been profiled for this study on the 3D printing plastics market.

- 3D Systems Corporation

- Arkema Inc.

- Envisiontec Inc.

- Stratasys Ltd.

- SABIC

- Materialse nv

- HP INC.

- Eos GmbH Electro Optical Systems

- PolyOne Corporation

- Royal DSM N.V.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature players: Stratasys Ltd.; 3D Systems Corporation; EOS GmbH; Electro Optical Systems; HP Inc.; SABIC; Arkema Inc.; Royal DSM N.V.

• Focus on large-scale industrial adoption, vertically integrated manufacturing ecosystems, and continuous investments in advanced polymer and printer technologies.

• Strong global distribution networks, diversified product portfolios, and long-standing relationships with aerospace, automotive, and healthcare manufacturers enable sustained market leadership.

• High operational costs, complex manufacturing structures, and slower adaptability to rapidly evolving niche application requirements may limit flexibility in emerging segments.

Emerging players: Materialise NV; governTEC Inc.; PolyOne Corporation

• Primarily emphasize niche application development, customized material solutions, and strategic collaborations to strengthen market penetration.

• Greater flexibility in innovation, specialization in targeted end-use applications, and faster adaptation to evolving additive manufacturing requirements support their competitive positioning.

• Limited global reach, lower capital investment capacity, and comparatively narrower product portfolios restrict their ability to compete with established multinational players at scale.

Recent Developments

-

In July 2025, AMETEK announced the purchase of FARO Technologies to enhance its offerings in 3D metrology and additive manufacturing solutions. This acquisition broadened AMETEK's expertise in industrial 3D measurement, digital reality, and advanced manufacturing technologies applicable in automotive, aerospace, and industrial sectors.

-

In May 2025, Stratasys obtained essential assets and operations from Forward AM GmbH and established “Mass Additive Manufacturing GmbH” to broaden its industrial 3D printing materials and polymer additive manufacturing sector. This acquisition strengthened Stratasys’ standing in high-performance 3D printing plastics and large-scale additive manufacturing solutions.

3D Printing Plastics Market Report Scope

Report Attribute

Details

Market size in 2025

USD 1.5 billion

Estimated market size in 2026

USD 1.8 billion

Projected market size by 2033

USD 9.6 billion

Growth rate

CAGR of 26.6% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, volume in Tons, and CAGR from 2026 to 2033

Report coverage

Revenue & volume forecast, competitive landscape, growth factors, and trends

Segments covered

Type, form, end use, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country Scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; China; India; Japan; South Korea; Brazil; Argentina; South Africa; Saudi Arabia

Key companies profiled

3D Systems Corporation; Arkema Inc.; Envisiontec Inc.; Stratasys Ltd.; SABIC; Materialse nv; HP INC.; Eos GmbH Electro Optical Systems; PolyOne Corporation; Royal DSM N.V.

Customization scope

Free report customization (equivalent to up to 8 analyst working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global 3D Printing Plastics Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends across sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global 3D printing plastics market report based on type, form, end use, and region:

-

Type Outlook (Volume, Tons; Revenue, USD Billion, 2021 - 2033)

-

Photopolymers

-

ABS & ASA

-

Polyamide/Nylon

-

Polylactic acid

-

Others

-

-

Form Outlook (Volume, Tons; Revenue, USD Billion, 2021 - 2033)

-

Filament

-

Ink

-

Powder

-

-

End Use Outlook (Volume, Tons; Revenue, USD Billion, 2021 - 2033)

-

Automotive

-

Medical

-

Aerospace & Defense

-

Consumer Goods

-

-

Regional Outlook (Volume, Tons; Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Competitive Benchmarking

Evaluation of top manufacturers in 3D printing plastics by examining their product offerings, innovation in materials, technological expertise, geographic reach, production capacity, strategic collaborations, and the industries they serve. A comparative analysis of market standing, pricing strategies, research and development efforts, and sustainability initiatives among major players.

Identify competitive positioning gaps and benchmark against industry leaders. Support differentiation strategies, product portfolio optimization, and partnership evaluation. Enable informed strategic decision-making for expansion and technology investments.

Pricing Analysis

Analysis of pricing trends for 3D printing plastics across different material types, technologies, and geographic regions, with a focus on changes in raw material costs, pricing for premium materials, margin structures, and price differences based on applications. Examination of past pricing trends and future price expectations under various supply and demand scenarios.

Support pricing strategy development and margin optimization. Improve visibility into cost drivers, regional pricing competitiveness, and procurement planning. Enable better forecasting and customer pricing alignment across application segments.

Trade Assessment

Examination of global trade patterns for 3D printing plastics, encompassing trends in imports and exports, major manufacturing and consumption nations, tariff frameworks, trade regulations, supply chain dependencies, and regional sourcing trends. Evaluation of changing trade movements and localization tendencies within the supply chains of additive manufacturing.

Identify favorable sourcing regions and strategic trade corridors. Support supply chain diversification and regional manufacturing strategies. Enable risk assessment related to trade barriers, import dependency, and geopolitical disruptions.

Frequently Asked Questions About This Report

The global 3d printing plastics market size was valued at USD 1.5 billion in 2025 and is estimated at USD 1.8 billion for 2026.

The global 3d printing plastics market is expected to grow at a CAGR of 26.6% from 2026 to 2033, reaching USD 9.6 billion by 2033.

North America dominated with a 39.9% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Key players include 3D Systems Corporation; Arkema Inc.; Envisiontec Inc.; Stratasys Ltd.; SABIC; Materialse nv; HP INC.; Eos GmbH Electro Optical Systems; PolyOne Corporation; Royal DSM N.V.

The growing demand for customized and personalized products drives innovation in the 3D printing industry, leading to an increased need for 3D printing plastics.

The photopolymers segment led with a 58.1% revenue share in 2025, while the Polyamide/Nylon segment is the fastest-growing.

The filament segment led with a 71.8% revenue share in 2025.

The medical segment led with a 49.8% revenue share in 2025, while the aerospace & defense segment is the fastest-growing.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.