- Home

- »

- Plastics, Polymers & Resins

- »

-

Polylactic Acid Market Size And Share Report, 2026-2033GVR Report cover

![Polylactic Acid Market (2026 - 2033)Report]()

Polylactic Acid Market (2026 - 2033)

Size, Share & Trends Analysis Report By Raw Materials (Corn starch, Sugarcane, Cassava), By Application (Rigid Thermoform, Film & Sheets, Bottles), By End Use (Packaging, Agriculture, Electronics, Textile), By Region, And Segment Forecasts

Market Size, 2025

$1.9BMarket Estimate, 2026

$2.3BMarket Forecast, 2033

$5.2BCAGR, 2026–2033

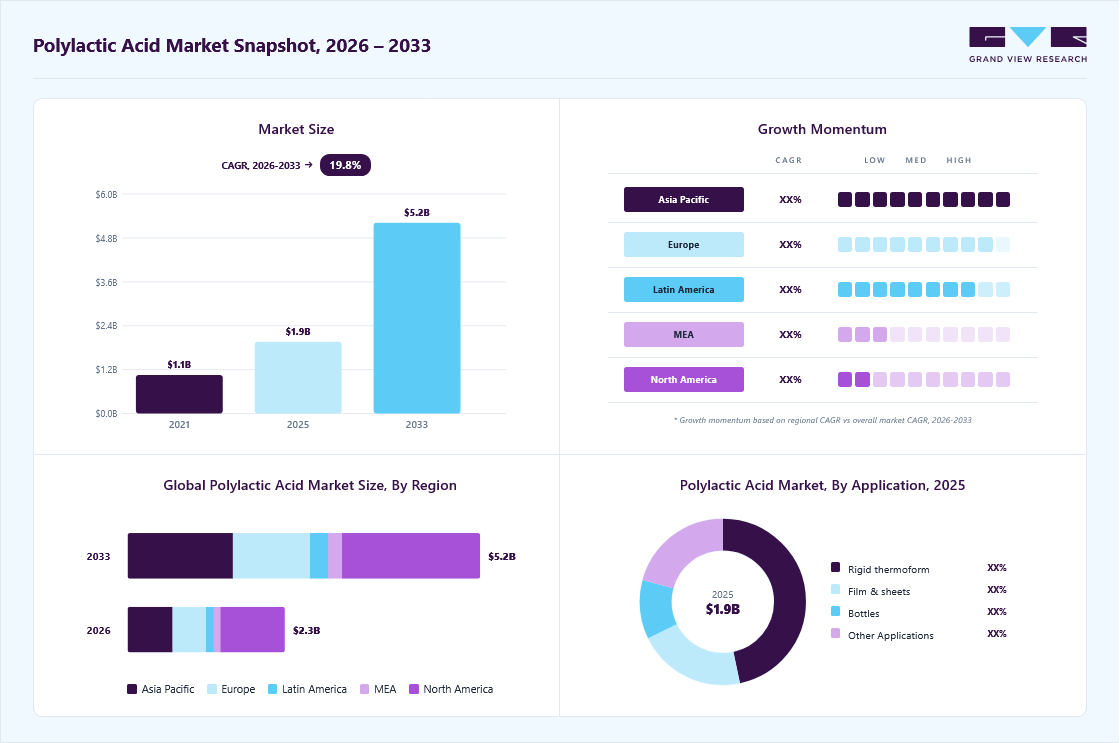

19.8%Polylactic Acid Market Summary

The global polylactic acid market size was valued at USD 1.9 billion in 2025 and is projected to grow from USD 2.3 billion in 2026 to USD 5.2 billion by 2033, at a CAGR of 19.8% from 2026 to 2033. The market in North America dominated with a revenue share of 41.3% in 2025. The rapid expansion of industrial composting infrastructure in North America and Europe is supporting the adoption of polylactic acid (PLA) in food packaging and foodservice ware.

Key Market Trends & Insights

- By raw materials: Corn starch segment held the largest market share of 62.7% in 2025.

- By application: Rigid thermoform segment held the largest market share of 46.6% in 2025.

- By end use: Packaging segment held the largest market share of 36.6% in 2025.

Regional Highlights

- Largest regional market: North America (41.3% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 1.9 Billion

- Estimated market size in 2026: USD 2.3 Billion

- Projected market size by 2033: USD 5.2 Billion

- CAGR (2026-2033): 19.8%

Improved end-of-life processing enhances regulatory acceptance and strengthens buyer confidence in certified compostable solutions. The PLA market is evolving toward higher-performance and diversified applications. The development of heat-resistant PLA grades and impact-modified blends is expanding their use beyond traditional packaging into automotive, textile, and engineering plastics segments. PLA’s share in 3D printing filaments and medical device components has grown significantly as suppliers improve mechanical and thermal properties through advanced polymerization and material science. Overall, major manufacturers are increasing capacity and broadening PLA portfolios to capture demand across end use industries.")

Drivers, Opportunities & Restraints

Demand for sustainable, bio-based polymers is the primary market growth driver. Regulatory measures, including bans on single-use plastics in over 80 countries, are shifting procurement toward renewable and compostable materials. Consumer goods, food service, and pharmaceutical sectors are increasingly specifying PLA to meet corporate environmental goals and reduce lifecycle emissions. Adoption of packaging, flexible films, and consumer products is rising as businesses align with sustainability mandates and circular-economy principles.

Emerging high-value applications offer significant opportunities for PLA producers. The material’s biodegradability and biocompatibility position it well for growth in medical devices, tissue scaffolds, and drug delivery systems. PLA fibers are gaining traction in textile markets due to their lower carbon footprint compared to conventional fibers, and additive manufacturing segments continue to expand, driven by PLA demand for 3D printing. These adjacent applications support diversification beyond bulk packaging and can drive margin expansion for industry participants.

High production costs relative to traditional petroleum-based polymers remain a key restraint. PLA manufacturing relies on energy-intensive fermentation and polymerization, and feedstock prices for corn, sugarcane, or other biomass can fluctuate significantly. These factors result in unit costs that are materially higher than those of commodity plastics, limiting PLA adoption in price-sensitive applications, especially in developing regions. Cost competitiveness with conventional and alternative bioplastics continues to constrain market penetration.

Market Concentration & Characteristics

The market growth stage is exponential and is expected to accelerate in the coming years. The market exhibits slight consolidation, with key players dominating the industry landscape. Major companies such as NatureWorks LLC, TotalEnergies Corbion PLA S.A., BASF SE, Futerro SA, Toray Industries, Inc., Mitsubishi Chemical Corporation, COFCO Biotechnology (COFCO Biochemical), Zhejiang Hisun Biomaterials Co., Ltd., Evonik Industries AG, Unitika Ltd., and others play a significant role in shaping the market dynamics. These leading players often drive innovation in the market, introducing new products, technologies, and product types to meet the industry's evolving demands.

Innovation in the market is gaining momentum with advanced PLA grades and production technologies driving performance improvements. Manufacturers are launching high-heat PLA capable of withstanding temperatures above 110°C, opening applications in hot-fill packaging and durable goods. Reinforced PLA filaments for 3D printing and impact-modified formulations with up to 40% greater toughness are expanding their utility in industrial and consumer segments. Chemical recycling-compatible PLA and enhanced fiber variants are also emerging, supporting lifecycle value and broadening applicability across sectors.

PLA is being replaced by both conventional and bio-based polymers across key end uses. In packaging, PET and PE remain entrenched due to their lower costs and established supply chains, challenging PLA’s price competitiveness. Bio-based alternatives such as bio-PET and PBS are gaining traction where biodegradability or higher performance is prioritized. In textiles, recycled polyester and bio-polyethylene terephthalate blends compete with PLA fibers on cost and mechanical properties. These substitutes constrain PLA adoption where performance or economics outweigh sustainability benefits.

Raw Material Insights

Corn starch accounted for the largest share of raw materials, at 62.7% in 2025. and is expected to grow at a 19.9% CAGR from 2026 to 2033. It serves as a primary source of carbohydrates, which are enzymatically converted to glucose and then fermented into lactic acid, the essential monomer for PLA polymer production. The extensive use of corn starch is influenced by its abundant availability, established wet-milling processes, cost-effectiveness, and high fermentation efficiency.

Sugarcane is expected to grow at the fastest CAGR owing to its direct availability of fermentable sucrose. Furthermore, sugarcane boasts strong sustainability credentials due to its high crop yield per hectare and advantageous carbon footprint, which aligns with increasing regulatory demands and brand commitments to low-carbon, bio-based materials. The growing cultivation and processing infrastructure in major producing countries like Brazil, India, and Thailand further enhances supply reliability. As PLA manufacturers seek feedstock diversification and enhanced lifecycle performance, sugarcane is expected to capture market share at the fastest rate among other raw material sources.

Application Insights

Rigid thermoform dominated the market across end-use segments in terms of revenue, accounting for 46.6% market share in 2025, and is forecast to grow at a 19.5% CAGR from 2026 to 2033. PLA-based rigid thermoform is commonly used for environmentally friendly food and retail packaging, such as trays, clamshells, and containers, due to its superior clarity, rigidity, and biodegradability. Its expansion is fueled by rising demand for sustainable packaging options and regulatory pressures to reduce the use of traditional plastics in single-use applications.

The bottles segment of the PLA market is experiencing rapid growth, driven by rising demand for compostable, bio-based containers for beverages and personal care products. Advances in PLA’s barrier and thermal properties are facilitating its wider use in liquid packaging, thereby supporting its growth.

End Use Insights

Packaging dominated the market across end-use segments in terms of revenue, accounting for 36.6% market share in 2025, and is forecast to grow at a 19.9% CAGR from 2026 to 2033. The rapid adoption of PLA is driven by shifting regulatory mandates and corporate sustainability initiatives. Governments in Europe, North America, and parts of Asia are enforcing stringent restrictions on single-use plastics, compelling major brands and retail conglomerates to replace conventional PET and polystyrene with compostable PLA alternatives in food and beverage packaging. Consumers increasingly expect environmentally responsible packaging, driving the procurement of PLA films, rigid containers, and trays that align with waste-reduction and recycling targets. This trend elevates PLA as a strategic material for sustainable packaging portfolios.

The textile segment is expected to expand at a robust 20.4% CAGR over the forecast period. In textiles, a unique driver for PLA growth is rising demand for bio-based fibers that support low-impact fashion and performance apparel. Sustainability standards and textile certifications are increasingly linked to bio-based content, prompting manufacturers to integrate PLA blends in activewear, non-woven hygiene products, and home textiles. This alignment with sustainability criteria is broadening PLA’s footprint beyond packaging into value-added textile applications.

Regional Insights

The North American polylactic acid market held the largest revenue share of 41.3% in 2025. The region is expected to grow at a CAGR of 19.0% over the forecast period. PLA market growth is driven by strong adoption in sustainable packaging, advanced manufacturing, and institutional procurement policies. Corporate sustainability standards among major food, beverage, and consumer goods companies are increasing demand for PLA films, containers, and serviceware. The region also benefits from robust 3D printing growth and established medical applications that elevate PLA volumes. Furthermore, well-developed composting and recycling infrastructure enhances end-of-life management, supporting broader PLA integration in commercial supply chains.

U.S. Polylactic Acid Market Trends

The polylactic acid market in the U.S. is a central driver for the global market due to its mature bio-based chemicals industry and strong regulatory support. PLA adoption surges as major fast-moving consumer goods and retail brands transition to certified compostable materials to meet federal and state sustainability pledges. FDA approvals for food contact and medical use further stimulate demand in healthcare and packaging segments. Substantial private investment in PLA production capacity and R&D reinforces domestic supply and innovation.

Europe Polylactic Acid Market Trends

The polylactic acid market in Europe is growing significantly, and regulatory pressure is the primary driver. Stringent EU directives on single-use plastics and circular-economy targets require the adoption of biodegradable alternatives across packaging, retail, and consumer product segments. High consumer environmental awareness is accelerating demand for PLA in foodservice ware and certified compostable applications. Extensive waste collection and industrial composting infrastructure further support material acceptance among converters and brand owners seeking compliance and sustainability certifications.

Asia Pacific Polylactic Acid Market Trends

The polylactic acid market in the Asia Pacific is expanding rapidly, driven by large-scale manufacturing and supportive government policies for biodegradable polymers. China and India lead in packaging and agricultural applications, supported by cost-efficient feedstocks and expanded production capacity. National initiatives to reduce plastic waste and incentives for adopting bio-based materials strengthen regional demand. The textile industry’s shift toward eco-friendly fibers also drives growth in PLA consumption across the industrial and consumer sectors.

Key Polylactic Acid Company Insights

The industry is highly competitive, with several key players dominating the landscape. Major companies include NatureWorks LLC, TotalEnergies Corbion PLA S.A., BASF SE, Futerro SA, Toray Industries, Inc., Mitsubishi Chemical Corporation, COFCO Biotechnology (COFCO Biochemical), Zhejiang Hisun Biomaterials Co., Ltd., Evonik Industries AG, and Unitika Ltd. The polylactic acid industry is characterized by a competitive landscape with several key players driving innovation and market growth. Major companies in this sector are investing heavily in research and development to enhance the performance, cost-effectiveness, and sustainability of their products.

Key Polylactic Acid Companies:

The following key companies have been profiled for this study on the polylactic acid market.

- NatureWorks LLC

- TotalEnergies Corbion PLA S.A.

- BASF SE

- Futerro SA

- Toray Industries, Inc.

- Mitsubishi Chemical Corporation

- COFCO Biotechnology (COFCO Biochemical)

- Zhejiang Hisun Biomaterials Co., Ltd.

- Evonik Industries AG

- Unitika Ltd.

Recent Developments

-

In April 2025, TotalEnergies Corbion formed a strategic partnership with USEON to develop and commercialize EPLA molded products. The collaboration targets high-performance PLA foam applications and aims to speed commercialization through joint technology development and global go-to-market efforts.

-

In August 2024, TotalEnergies Corbion appointed Nagase & Co., Ltd. as its distributor for Luminy PLA in Japan, expanding local market access for compostable packaging grades and strengthening supply to converters and brand owners focused on low-carbon materials.

Polylactic Acid Market Report Scope

Report Attribute

Details

Market size in 2025

USD 1.9 billion

Estimated market size in 2026

USD 2.3 billion

Projected market size by 2033

USD 5.2 billion

Growth rate

CAGR of 19.8% from 2026 to 2033

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Report Segmentation

Raw material, application, end use, region

Regional scope

North America; Europe; Asia Pacific; CSA; MEA

Country Scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Netherlands; Turkey; China; India; Japan; Indonesia; Malaysia; Philippines; Brazil

Key companies profiled

NatureWorks LLC; TotalEnergies Corbion PLA S.A.; BASF SE; Futerro SA; Toray Industries, Inc.; Mitsubishi Chemical Corporation; COFCO Biotechnology (COFCO Biochemical); Zhejiang Hisun Biomaterials Co., Ltd.; Evonik Industries AG; Unitika Ltd.

Customization scope

Free report customization (equivalent to up to 8 analyst working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Polylactic Acid Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends across sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global polylactic acid market report based on raw material, application, end use, and region:

-

Raw Material Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Corn starch

-

Sugarcane

-

Cassava

-

Other Raw Materials

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Rigid thermoform

-

Film & sheets

-

Bottles

-

Other Applications

-

-

End Use Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Packaging

-

Agriculture

-

Automotive & Transport

-

Electronics

-

Textile

-

Other End Uses

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Netherlands

-

Turkey

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Indonesia

-

Malaysia

-

Philippines

-

-

Central & South America

-

Brazil

-

-

Middle East & Africa

-

Frequently Asked Questions About This Report

North America dominated with a 41.3% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The corn starch segment led with a 62.7% revenue share in 2025, while sugarcane is the fastest-growing materials.

The rigid thermoform segment led with a 46.6% revenue share in 2025.

The global polylactic acid (PLA) market size was valued at USD 1.9 billion in 2025 and is estimated at USD 2.3 billion for 2026.

The global polylactic acid market is expected to grow at a CAGR of 19.8% from 2026 to 2033, reaching USD 5.2 billion by 2033.

Key players include NatureWorks LLC; TotalEnergies Corbion PLA S.A.; BASF SE; Futerro SA; Toray Industries, Inc.; Mitsubishi Chemical Corporation; COFCO Biotechnology (COFCO Biochemical); Zhejiang Hisun Biomaterials Co., Ltd.; Evonik Industries AG; Unitika Ltd.

The rapid expansion of industrial composting infrastructure in North America and Europe is supporting the adoption of polylactic acid (PLA) in food packaging and foodservice ware. Improved end-of-life processing enhances regulatory acceptance and strengthens buyer confidence in certified compostable solutions.

Packaging dominated the market across the end-use segmentation in terms of revenue, accounting for a 36.6% market share in 2025, and is forecast to grow at a 19.9% CAGR from 2026 to 2033.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.