- Home

- »

- Next Generation Technologies

- »

-

5G Systems Integration Market Size Report, 2026-2033GVR Report cover

![5G System Integration Market (2026 - 2033)Report]()

5G System Integration Market (2026 - 2033)

Size, Share & Trends Analysis Report By Services (Consulting, Infrastructure Integration, Application Integration), By Vertical (Manufacturing, Energy & Utility, Media & Entertainment), By Application, By Region, And Segment Forecasts

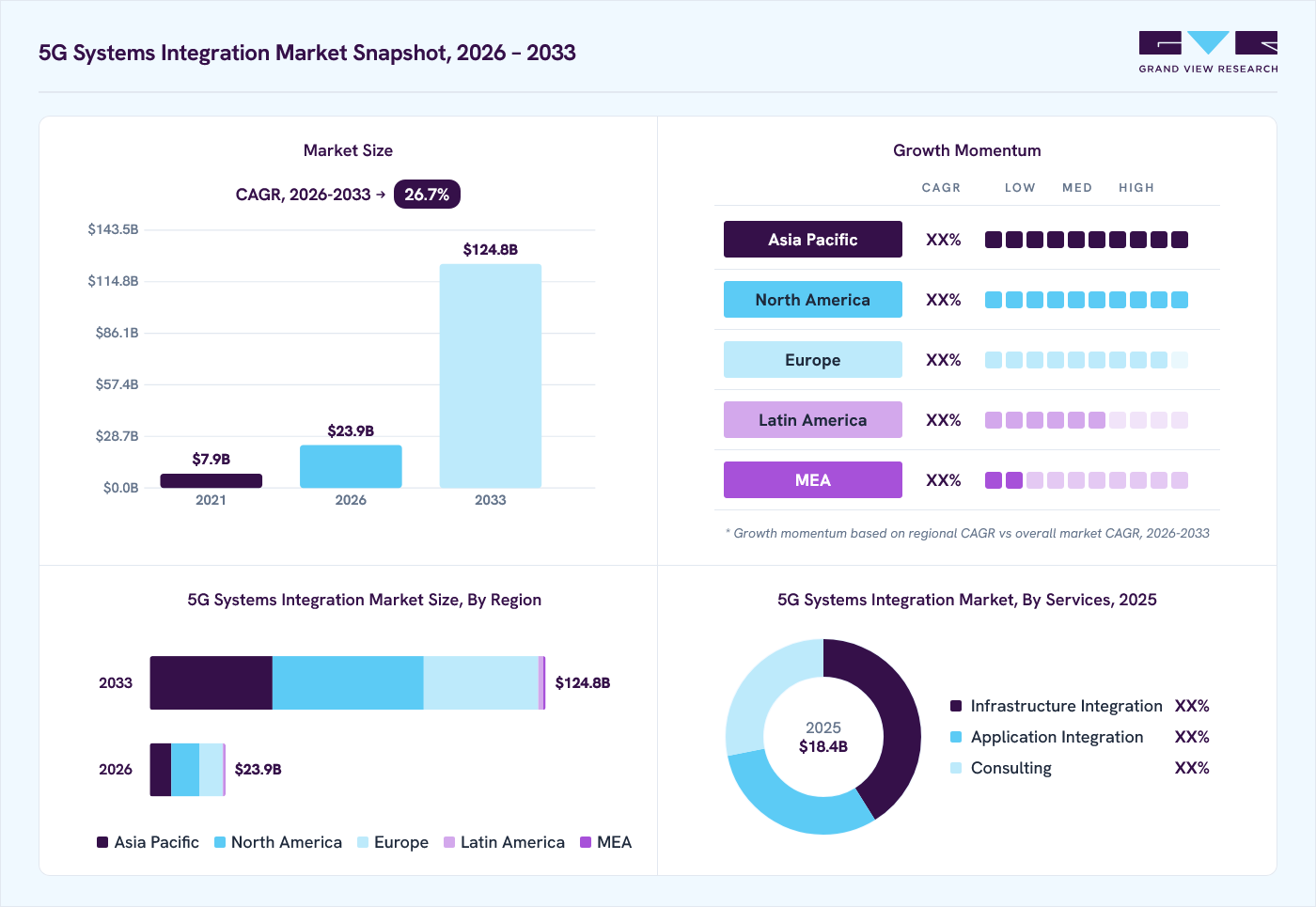

Market Size, 2025

$18.4BMarket Estimate, 2026

$23.9BMarket Forecast, 2033

$124.8BCAGR, 2026–2033

26.7%5G System Integration Market Summary

The global 5G system integration market size was valued at USD 18.4 billion in 2025 and is projected to grow from USD 23.9 billion in 2026 to USD 124.8 billion by 2033, at a CAGR of 26.7% from 2026 to 2033. North America dominated the market, accounting for a revenue share of 36.7% in 2025. The increasing penetration of 5G networks globally is one of the major factors attributed to the growing demand for 5G system integration services.

Key Market Trends & Insights

- By service: Infrastructure Integration segment dominated the market, with a revenue share of 41.1% in 2025.

- By vertical: IT & Telecom segment held the largest market share of 26.3% in 2025.

- By application: Home and Office Broadband segment led the market with the largest revenue share of 23.4% in 2025.

Regional Highlights

- Largest regional market: North America (36.7% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in North America market in 2025.

Market Size & Forecast

- Market size in 2025: USD 18.4 Billion

- Estimated market size in 2026: USD 23.9 Billion

- Projected market size by 2033: USD 124.8 Billion

- CAGR (2026-2033): 26.7%

The growing penetration of 5G-supporting devices, including tablets, laptops, smartphones, routers, smart home devices, and many others, is expected to fuel the growth of the market. In addition, the market is also driven by the growing need for low-latency and high-reliable connectivity to support industrial internet of things (IIoT) applications such as industrial sensors, industrial cameras, and collaborative robots.")

Major global manufacturers are seeking opportunities to speed up their operations by embracing modern digital technologies to empower the fourth industrial revolution (Industry 4.0). Technologies such as big data analytics, industrial wireless cameras, the Internet of Things (IoT), and collaborative robots are enabling manufacturing facilities to take a giant leap toward smart and data-driven flexible operations.

Several manufacturers have developed and implemented these aforementioned technologies to compete in a highly competitive environment. Manufacturers need to integrate them with next-generation networks to provide unified communication with these 5G technologies, which also helps reduce the overall operational downtime and costs through delivering continuous connectivity and remote monitoring. Thus, the robust deployment of the industrial internet of things (IIoT), along with the increasing demand for 5G services to deliver unified connectivity, is expected to bolster the demand for 5G system integration services during the forecast period.

With the evolution of fifth-generation mobile network services, various enterprises globally are aggressively focusing on integrating their legacy network infrastructure with the new upcoming 5G technologies. These companies are integrating their existing on-premise applications and cloud networks with modern 5G technologies to work seamlessly over a centralized network. This integration process allows enterprises to access high bandwidth capacity with low latency for their operations, thereby increasing the total operational efficiency by reducing the overall response time to customers. Therefore, a significant rise in demand for fast broadband to reduce overall response time is expected to drive the market for 5G system integration from 2025 to 2033.

The growing popularity of Network Function Visualization (NFV) and Software-Defined Networking (SDN) across enterprises is also expected to be one of the major factors driving the market for 5G system integration. NFV allows enterprises to deploy several virtual machines and firewalls to achieve an efficient economy of scale. On the other hand, SDN provides a smart network architecture that aims to reduce hardware constraints on the company premises. SDN allows these companies to manage the use of their network efficiently through an Application Program Interface (API). Thus, the rapid adoption of NFV and SDN technologies to minimize overall network infrastructure costs is anticipated to further surge the market growth. However, a rapidly increasing large chunk of datasets over the cloud, coupled with increasing demand for cloud-based application integration, creates a major security concern among consumers, which may hinder the 5G system integration industry growth in the future.

Market Dynamics

The 5G systems integration market is witnessing strong growth driven by the rapid deployment of 5G networks, increasing enterprise digital transformation initiatives, and rising demand for seamless integration of network infrastructure, cloud platforms, edge computing, IoT ecosystems, and operational support systems. The market is benefiting from growing investments in private 5G networks, network virtualization, Open RAN architectures, and the convergence of 5G with artificial intelligence (AI), industrial automation, and Industry 4.0 applications. However, integration complexity across multi-vendor environments, high implementation costs, and cybersecurity concerns continue to restrain market growth. In addition, emerging opportunities associated with smart cities, autonomous vehicles, connected healthcare, and mission-critical industrial applications are expected to accelerate market expansion. Continued investments by telecom operators, enterprises, and governments in next-generation connectivity infrastructure are expected to support the long-term growth of the 5G systems integration market.

The increasing deployment of 5G networks across developed and developing economies is a major driver of the 5G systems integration market. Telecom operators and enterprises are investing heavily in 5G infrastructure to support high-speed connectivity, ultra-low latency communication, and massive device connectivity. As organizations adopt advanced technologies such as the Internet of Things (IoT), artificial intelligence (AI), edge computing, cloud computing, and industrial automation, the need for seamless integration of diverse systems and platforms is growing significantly. 5G systems integration services enable organizations to connect network infrastructure, applications, devices, and operational systems efficiently, ensuring optimized performance and enhanced user experiences. The growing adoption of private 5G networks across manufacturing, logistics, healthcare, energy, and transportation sectors is further accelerating demand for integration services. This increasing focus on digital transformation and next-generation connectivity continues to support market growth.

The expansion of Industry 4.0 initiatives and smart infrastructure projects is further strengthening demand for 5G systems integration solutions. Enterprises require specialized integration services to manage complex multi-vendor environments, virtualized network architectures, cloud-native platforms, and edge computing ecosystems. Governments worldwide are investing in smart city programs, intelligent transportation systems, and digital public infrastructure that rely on robust 5G connectivity. In addition, the growing need for real-time data processing, remote monitoring, predictive maintenance, and mission-critical communications is driving organizations to deploy integrated 5G-enabled solutions. As businesses increasingly seek to improve operational efficiency, automate processes, and enhance connectivity, demand for 5G systems integration services is expected to grow steadily throughout the forecast period.

The high cost associated with deploying and integrating 5G infrastructure remains a significant restraint for the 5G systems integration market. Implementing 5G-enabled solutions often requires substantial investments in network equipment, software platforms, edge computing infrastructure, cloud services, and cybersecurity systems. Organizations must also upgrade legacy IT and operational technology (OT) environments to ensure compatibility with new 5G architectures. These capital-intensive requirements can limit adoption, particularly among small and medium-sized enterprises (SMEs) and organizations operating in cost-sensitive markets. Additionally, the need for specialized expertise to design, deploy, and manage complex 5G ecosystems increases implementation expenses and project timelines, creating challenges for widespread market adoption.

The complexity of integrating multiple technologies, platforms, and vendors further constrains market growth. Many enterprises operate heterogeneous environments consisting of legacy systems, cloud platforms, IoT devices, and third-party applications that must function seamlessly within a 5G network. Ensuring interoperability, network reliability, data security, and regulatory compliance across these diverse systems can be challenging. Furthermore, concerns related to cybersecurity vulnerabilities, data privacy, and network management complexity increase operational risks for organizations adopting 5G solutions. The shortage of skilled professionals with expertise in 5G architecture, network virtualization, cloud integration, and cybersecurity further complicates deployment efforts. These factors collectively act as barriers to the rapid adoption of 5G systems integration solutions and may restrain market growth during the forecast period.

The increasing adoption of private 5G networks across industrial and enterprise environments presents a significant growth opportunity for the 5G systems integration market. Organizations in manufacturing, logistics, energy, mining, healthcare, and transportation are deploying private 5G networks to enable secure, reliable, and high-performance connectivity for mission-critical operations. These networks support a wide range of advanced applications, including industrial automation, autonomous vehicles, robotics, predictive maintenance, augmented reality (AR), virtual reality (VR), and real-time asset monitoring. As enterprises seek to improve operational efficiency, reduce downtime, and enhance productivity, demand for comprehensive systems integration services that connect 5G infrastructure with cloud platforms, IoT devices, edge computing systems, and enterprise applications is increasing rapidly. This trend is creating substantial opportunities for system integrators, network providers, and technology vendor.

Analyst Perspective

The 5G Systems Integration Market is driven by the rapid deployment of 5G networks, increasing enterprise digital transformation initiatives, and growing demand for seamless integration of cloud, edge computing, IoT, and network infrastructure. Companies are focusing on enhancing network performance, enabling private 5G deployments, supporting Industry 4.0 applications, and developing industry-specific connectivity solutions. Rising adoption of 5G-enabled technologies across manufacturing, healthcare, transportation, energy, smart cities, and telecom sectors continues to strengthen market demand. Furthermore, increasing investments in network virtualization, Open RAN architectures, edge computing, and intelligent automation are accelerating the need for advanced 5G systems integration services globally.

Services Insights

Based on service, the Infrastructure Integration segment led the market with the largest revenue share of 41.1% in 2025. This is attributed to the surging demand for the integration of traditional network infrastructure with next-generation network infrastructure. Thus, integration of legacy infrastructure enables users to access the same hardware with enhanced features, thereby reducing the additional costs of hardware. In addition, the infrastructure system integration services consist of network integration, building management, and data center infrastructure management (DCIM).

The consulting segment is expected to grow at a moderate CAGR over the forecast period. With the rapidly increasing demand for 5G technologies, such as network equipment, business enterprises initially approach system integrators to build upgraded network architecture for their organizations. This architecture helps business enterprises to boost overall operational output in less time. Moreover, spiraling demand for multi-vendor cloud-based applications across enterprises is expected to augment the need for application integration services over the forecast period.

Vertical Insights

Based on vertical, the IT & Telecom segment led the market with the largest revenue share of 26.3% in 2025. This is attributed to surging demand for 5G integration services across various IT and telecom companies to support new radio (NR) waves. A healthy rise in demand for integrating enterprise network infrastructure and data center network hardware is anticipated to witness significant growth in demand for 5G system integration services in the IT and telecom segment. Moreover, 5G network services are expected to witness significant adoption across enterprises over the forecast period due to an increased focus on providing uniform connectivity during a virtual meeting to reduce the overall travel time of a specialist or consultant. Therefore, demand for 5G system integration services is estimated to witness a substantial rise in integrating an entire enterprise network to make it compatible with the next-generation network.

The manufacturing segment is expected to witness the fastest CAGR over the forecast period. This is owing to the growing requirement for system integration services to integrate the entire manufacturing facility with 5G carriers supporting the network. As digitalization is becoming popular in the manufacturing sector, production lines are being continuously automated to improve overall production efficiency. This has triggered the need for seamless wireless communication between industrial robots, actuators, sensors, and other devices mounted in manufacturing facilities, thereby driving the segment’s growth.

Application Insights

Based on frequency band, the Home and Office Broadband segment led the market with the largest revenue share of 23.4% in 2025. This is attributed to the growing need for 5G system integration services to deliver enhanced Mobile Broadband (eMBB) connectivity to consumers and enterprises. Moreover, a remarkable increase in IoT devices across rapidly developing smart cities worldwide is expected to surge the demand for 5G system integration services to make these devices compatible with next-generation network services. This factor is anticipated to further boost the growth of the smart city application segment from 2025 to 2033.

The industrial sensors segment is expected to witness the fastest CAGR over the forecast period. The segment’s growth is driven by the rapid adoption of smart manufacturing, Industry 4.0 initiatives, and real-time process automation. Industrial environments increasingly rely on 5G-enabled sensor networks to support low-latency, ultra-reliable machine-to-machine (M2M) communication, predictive maintenance, and real-time data analytics. System integrators play a critical role in bridging legacy industrial equipment with advanced 5G infrastructure, ensuring seamless connectivity and interoperability. This segment is expected to witness robust growth as companies seek to optimize operational efficiency, reduce downtime, and enable autonomous decision-making on the factory floor.

Regional Insights

North America dominated the global 5G systems integration market with the largest revenue share of 36.7% in 2025. This is attributed to the presence of large IT and telecom players, such as IBM Corporation; Microsoft Corporation; and Cisco Systems, Inc. Moreover, rising investments in deploying 5G infrastructure by key market players, such as AT&T Inc. and Verizon Communications Inc., are expected to create a robust need to integrate overall infrastructure and applications across various verticals, such as IT and telecom, energy & utilities, and healthcare, to support 5G NR frequency bands. This factor is anticipated to boost the overall growth of the regional market.

U.S. 5G System Integration Market Trends

The 5G systems integration market in the U.S. held the largest share in the North America region in 2025, driven by a mature ICT ecosystem and aggressive investments from major telecom and cloud companies. The demand is particularly strong in defense, healthcare, and smart manufacturing, where low-latency and high-reliability networks are critical. Integration projects are also expanding in rural connectivity and infrastructure modernization, supported by federal programs.

Europe 5G System Integration Market Trends

The 5G system integration market in Europe is expected to register a moderate CAGR from 2025 to 2033. Europe’s 5G system integration market is driven by a pan-regional focus on digital sovereignty, industrial automation, and green connectivity solutions. The European Union’s funding initiatives and policy frameworks, such as the Digital Europe Programme, are encouraging the integration of 5G into cross-border infrastructure. System integrators are increasingly targeting energy, logistics, and automotive sectors with customized 5G deployment models.

The UK 5G system integration market held a substantial share in 2024. The UK is emerging as a strategic hub for 5G system integration, backed by national-level policies and innovation funding for telecom infrastructure. Enterprises in sectors such as logistics, healthcare, and creative industries are adopting 5G to boost productivity and digital capability. The country’s focus on open RAN and vendor diversification is also influencing the integration ecosystem.

The 5G system integration market in Germany is expected to grow at the fastest CAGR from 2025 to 2033. Germany’s industrial strength makes it a key market for 5G system integration, especially within manufacturing, automotive, and logistics sectors. The government’s support for private 5G networks in industrial parks is boosting demand for end-to-end integration services.

Asia Pacific 5G System Integration Market Trends

The 5G system integration market in Asia Pacific is expected to witness the fastest CAGR of 28.6% during the forecast period. Prominent telecom operators such as China Mobile Limited, China Telecom Corporation Limited, KT Corporation, and SK Telecom Co., Ltd. are making significant investments in rolling out fifth-generation networks in China, Japan, and South Korea. Most of these investments are envisioned to focus on implementing next-generation infrastructure for various industry verticals, including transportation, energy and utility, healthcare, media and entertainment, and manufacturing. Thus, rapidly growing investments in installing 5G infrastructure across the above-mentioned countries are expected to create a significant opportunity for system integrators in the market in the forthcoming years. Furthermore, a rapid increase in the number of small and medium IT companies in emerging countries, such as China and India, is estimated to propel regional market growth.

India 5G system integration market is expected to grow at the fastest growth rate during the forecast period. India’s market growth is driven by the commercial rollout of 5G networks and strong government support through initiatives such as Digital India and Make in India. Enterprises across manufacturing, logistics, and healthcare are engaging with integrators to modernize operations with private 5G networks. The demand for cloud-based services, combined with a growing ecosystem of tech startups, is accelerating 5G-driven enterprise digitalization.

The 5G system integration market in China held a substantial share in 2024, driven by state-backed investments and a national strategic focus on digital infrastructure. Major Chinese technology firms are driving large-scale deployments across sectors such as automotive, energy, and smart manufacturing. The integration of 5G with AI and edge computing is a key priority for enabling real-time, data-driven operations.

Key 5G System Integration Companies Insights

Key players operating in the 5G system integration market are undertaking various initiatives to strengthen their presence and increase the reach of their products and services. Strategies such as expansion activities and partnerships are key in propelling the market growth.

Key 5G System Integration Companies:

The following are the leading companies in the 5g system integration market.

-

Accenture Inc.

-

Cisco Systems, Inc.

-

Huawei Technologies Co., Ltd.

-

Infosys Limited

-

Tata Consultancy Services Limited

-

IBM Corporation

-

Hewlett Packard Enterprise Development LP

-

Wipro Limited

-

Samsung Electronics Co., Ltd.

-

Telefonaktiebolaget LM Ericsson

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Accenture, IBM, Cisco Systems, Inc.; Huawei Technologies Co., Ltd.)

- These players focus on large-scale 5G deployment projects through strategic partnerships with telecom operators, cloud providers, equipment vendors, and enterprise customers.

- Their strategies include expanding private 5G offerings, strengthening industry-specific solutions, investing in Open RAN and edge computing capabilities, and pursuing acquisitions to enhance their systems integration portfolios.

- These companies possess extensive global delivery capabilities, strong technical expertise, established customer relationships, broad service portfolios, and significant experience in managing complex digital transformation projects.

- Their ability to provide end-to-end consulting, infrastructure integration, application integration, and managed services positions them as preferred partners for large enterprises and telecom operators.

- Despite their strong market presence, these companies often face challenges related to lengthy implementation cycles, high service costs, and operational complexity associated with large-scale projects.

- They also face increasing competition from specialized 5G integrators, cloud-native solution providers, and regional technology firms offering more flexible and cost-effective solutions.

Emerging Players (Wipro Limited; HPC)

- These players are focusing on niche 5G integration opportunities such as private networks, Open RAN deployments, edge computing, industrial IoT, and cloud-native network architectures.

- These companies offer greater flexibility, faster deployment capabilities, specialized expertise, and innovative technology solutions tailored to specific industry requirements.

- While these players have established strong positions in selected markets and technology domains, they often face limitations in global reach, financial resources, large-scale project execution capabilities, and brand recognition.

Recent Developments

-

In March 2025, Lockheed Martin, Verizon Communications Inc., and Nokia Corporation announced the integration of Nokia Corporation’s advanced, military-grade 5G solutions into Lockheed Martin’s 5G.MIL Hybrid Base Station. This collaboration enhances the ability to merge commercial 5G connectivity with military communication systems, enabling faster, more decisive information delivery to support national defense operations.

-

In October 2024, NEC Corporation, a prominent integrator of IT and network technologies, partnered with Cisco Systems, Inc. to launch a private 5G network solution for enterprise customers. The offering combines Cisco Systems, Inc.’s 5G Standalone (SA) Core and Cloud Control Center with NEC Corporation’s validated radio network and systems integration expertise, delivering a market-ready, end-to-end 5G architecture.

5G System Integration Market Report Scope

Report Attribute

Details

Market size in 2025

USD 18.4 billion

Estimated market size in 2026

USD 23.9 billion

Projected market size by 2033

USD 124.8 billion

Growth rate

CAGR of 26.7% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Services, vertical, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; China; Japan; India; Australia; South Korea; Brazil; Mexico; KSA; UAE; South Africa

Key companies profiled

Accenture Inc.; Cisco Systems, Inc.; Huawei Technologies Co., Ltd.; Infosys Limited; Tata Consultancy Services Limited; IBM Corporation; Hewlett Packard Enterprise Development LP; Wipro Limited; Samsung Electronics Co., Ltd.; and Telefonaktiebolaget LM Ericsson

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global 5G System Integration Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global 5G system integration market report based on services, vertical, application, and region.

-

Services Outlook (Revenue, USD Million, 2021 - 2033)

-

Consulting

-

Infrastructure Integration

-

Application Integration

-

-

Vertical Outlook (Revenue, USD Million, 2021 - 2033)

-

Manufacturing

-

Energy & Utility

-

Media & Entertainment

-

IT & Telecom

-

Transportation & Logistics

-

BFSI

-

Healthcare

-

Retail

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Smart City

-

Collaborate Robot /Cloud Robot

-

Industrial Sensors

-

Logistics & Inventory Monitoring

-

Wireless Industry Camera

-

Drone

-

Home and Office Broadband

-

Vehicle-to-everything (V2X)

-

Gaming and Mobile Media

-

Remote Patient & Diagnosis Management

-

Intelligent Power Distribution Systems

-

P2P Transfers /mCommerce

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Russia

-

Italy

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Research Methodology

The 5G system integration market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each 5G system integration segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment- Service

Revenue Capture Definition

Consulting

This segment captures revenue generated from advisory, planning, assessment, and strategy services related to 5G deployment and transformation initiatives. Services include network readiness assessment, use-case identification, architecture design, technology roadmapping, spectrum planning, cybersecurity consulting, regulatory compliance support, and business case development. Revenue is derived from helping enterprises and telecom operators define, optimize, and implement 5G adoption strategies.

Infrastructure Integration

This segment includes revenue generated from integrating 5G network infrastructure components, including radio access networks (RAN), core networks, edge computing platforms, cloud environments, private 5G networks, network virtualization solutions, Open RAN architectures, and supporting hardware. Revenue also includes deployment, configuration, testing, optimization, and interoperability services required to establish seamless 5G connectivity across enterprise and operator environments.

Application Integration

This segment captures revenue associated with integrating 5G-enabled applications, enterprise software, IoT platforms, operational technology (OT) systems, analytics platforms, AI solutions, and cloud services. Revenue includes customization, deployment, interoperability management, data integration, workflow automation, and performance optimization services that enable organizations to leverage 5G capabilities for business operations and digital transformation initiatives.

Segment- Vertical

Revenue Capture Definition

Manufacturing

Revenue generated from integrating 5G solutions within manufacturing facilities to support industrial automation, robotics, predictive maintenance, digital twins, asset tracking, machine-to-machine communication, and smart factory operations.

Energy & Utility

Revenue derived from 5G integration services supporting smart grids, intelligent power distribution, remote asset monitoring, predictive maintenance, renewable energy management, utility automation, and real-time operational control systems.

Media & Entertainment

This segment includes revenue from integrating 5G-enabled solutions for content creation, live broadcasting, immersive media experiences, AR/VR applications, cloud gaming, video streaming, and remote production workflows.

IT & Telecom

Revenue generated from deployment and integration of public and private 5G networks, network virtualization, cloud-native infrastructure, edge computing platforms, OSS/BSS modernization, and telecom network transformation initiatives.

Transportation & Logistics

This segment captures revenue from integrating 5G-enabled fleet management systems, autonomous transportation solutions, connected logistics networks, warehouse automation, real-time asset tracking, and intelligent transportation systems.

BFSI

Revenue derived from integrating secure 5G-enabled platforms that support digital banking, mobile payments, real-time transactions, fraud detection, customer engagement solutions, branch automation, and financial technology applications.

Healthcare

This segment includes revenue generated from 5G integration for telemedicine, remote patient monitoring, connected medical devices, digital healthcare platforms, robotic-assisted procedures, and real-time clinical data management systems.

Retail

Revenue generated from integrating 5G-enabled smart retail solutions, including automated checkout systems, inventory management, customer analytics, in-store automation, personalized shopping experiences, and omnichannel commerce platforms.

Others

This segment includes revenue from 5G systems integration across government, education, defense, public safety, agriculture, mining, hospitality, and other end-use industries not covered under the above categories.

Segment- Application

Revenue Capture Definition

Smart City

Revenue generated from integrating 5G infrastructure and applications that support intelligent traffic management, public safety systems, smart lighting, environmental monitoring, connected public services, and urban digital infrastructure.

Collaborative Robot (Cobot) / Cloud Robot

This segment captures revenue from integrating 5G-enabled robotic systems that utilize real-time communication, cloud processing, remote control, machine learning, and automation technologies across industrial and commercial environments.

Industrial Sensors

Revenue derived from integrating 5G-connected sensors used for equipment monitoring, predictive maintenance, process optimization, asset tracking, environmental monitoring, and industrial automation applications.

Logistics & Inventory Monitoring

This segment includes revenue generated from 5G-enabled tracking, warehouse management, inventory visibility, supply chain monitoring, automated material handling, and logistics optimization solutions.

Wireless Industrial Camera

Revenue captured from integrating high-definition wireless industrial cameras utilizing 5G connectivity for real-time monitoring, quality inspection, security surveillance, remote operations, and machine vision applications.

Drone

Revenue generated from integrating 5G-enabled drone systems used for inspection, surveillance, mapping, monitoring, delivery services, infrastructure assessment, agriculture, and industrial operations requiring real-time data transmission.

Home and Office Broadband

This segment includes revenue from integrating fixed wireless access (FWA) and 5G broadband solutions that provide high-speed internet connectivity for residential, commercial, and enterprise environments.

Vehicle-to-Everything (V2X)

Revenue derived from integrating 5G-enabled communication systems that facilitate real-time interaction between vehicles, infrastructure, pedestrians, and networks to support connected and autonomous mobility applications.

Gaming and Mobile Media

This segment captures revenue from integrating 5G platforms that enable cloud gaming, immersive entertainment, video streaming, AR/VR experiences, esports, and high-bandwidth mobile media services.

Remote Patient & Diagnosis Management

Revenue generated from integrating 5G-powered healthcare applications that support telehealth, remote diagnostics, connected medical devices, patient monitoring, emergency response, and virtual healthcare delivery.

Intelligent Power Distribution Systems

This segment includes revenue from integrating 5G-enabled smart grid technologies, distribution automation systems, real-time energy monitoring platforms, and advanced utility management solutions.

P2P Transfers / mCommerce

Revenue derived from integrating secure 5G-enabled platforms supporting peer-to-peer payments, mobile commerce, digital wallets, instant financial transactions, and mobile banking services.

Others

This segment captures revenue from additional 5G-enabled applications such as public safety communications, smart agriculture, connected mining, education technology, defense communications, and emerging enterprise use cases.

Estimation Model

Layer Name

Key Question

Description

Enterprise Connectivity & Digital Transformation Demand Layer

Who requires 5G-enabled connectivity and digital transformation solutions?

Establish the total potential demand base by identifying enterprises, telecom operators, governments, industrial facilities, healthcare providers, logistics companies, utilities, financial institutions, retailers, and smart city operators seeking enhanced connectivity, automation, real-time communication, and digital transformation capabilities enabled by 5G technology.

Addressable Market Layer

Who can realistically be served by 5G systems integration providers?

Refine the total demand ecosystem into the realistically serviceable market by considering factors such as 5G network availability, spectrum allocation, enterprise IT readiness, cloud infrastructure maturity, regulatory compliance requirements, cybersecurity standards, technology compatibility, and investment capacity. This layer identifies organizations capable of deploying and benefiting from integrated 5G solutions.

5G Systems Integration Adoption & Utilization Layer

Who is actively deploying 5G-integrated solutions and generating integration demand?

Estimate annual demand generation by analyzing enterprise adoption of private and public 5G networks, IoT deployments, edge computing infrastructure, industrial automation systems, smart city projects, connected healthcare platforms, intelligent transportation systems, and cloud-native applications. Demand is measured through integration projects, connected devices, network deployments, application implementations, and operational usage of 5G-enabled services.

Revenue Layer

How is revenue generated from 5G systems integration deployments?

Converts 5G adoption demand into market revenue through consulting services, infrastructure integration, application integration, deployment services, system customization, network optimization, managed services, maintenance, and support contracts. Revenue is generated from integrating 5G infrastructure with enterprise systems, cloud platforms, IoT ecosystems, edge computing environments, and industry-specific applications across various end-use sectors.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Entity-wise Value Chain Structure Analysis (% Share)

Delivered detailed value chain assessment of the 5G systems integration ecosystem, including Consulting Providers, Network Equipment Vendors, Cloud & Edge Infrastructure Providers, System Integrators, Telecom Operators, Managed Service Providers, and Enterprise End Users.

Evaluated the flow of value creation from network planning and consulting through infrastructure deployment, application integration, network management, and end-user enablement.

Assessed revenue contribution and margin distribution across each value chain participant.

Enabled identification of the highest value-generating segments within the 5G systems integration ecosystem.

Supported strategic investment, partnership, and market-entry decisions.

Improved understanding of industry structure, stakeholder dependencies, and revenue distribution.

Analysis of the Role of Private 5G Networks in the 5G Systems Integration Industry

Delivered comprehensive analysis of the growing role of private 5G networks across enterprise and industrial environments.

Assessed the impact of private 5G deployments on manufacturing automation, logistics optimization, smart utilities, connected healthcare, campus networks, and mission-critical communications.

Evaluated the competitive positioning of private 5G networks relative to Wi-Fi 6/6E, LTE private networks, and other enterprise connectivity technologies in terms of latency, reliability, security, scalability, and operational efficiency.

Enabled understanding of key technology trends driving enterprise 5G adoption.

Supported strategic planning related to private network deployment opportunities.

Identified high-growth application areas and emerging enterprise use cases.

Competitive Benchmarking & Strategic Landscape Analysis

Delivered benchmarking of major system integrators, telecom infrastructure providers, cloud service providers, and private 5G solution vendors based on service capabilities, industry expertise, geographic presence, technology partnerships, deployment experience, and innovation initiatives.

Analyzed strategic collaborations, acquisitions, product launches, private 5G deployments, Open RAN initiatives, and cloud-edge integration developments.

Assessed competitive positioning across key end-use industries and regional markets.

Supported competitive intelligence and strategic decision-making.

Enabled identification of market gaps, differentiation opportunities, and expansion strategies.

Provided visibility into evolving competitive dynamics and future growth opportunities within the 5G systems integration market.

Frequently Asked Questions About This Report

The global 5G system integration market size was estimated at USD 18.4 billion in 2025 and is expected to reach USD 23.9 billion in 2026.

The North America dominated the market in 2025 and accounted for the largest share of 36.7% in the global 5G system integration market

The home and office segment dominated the market in 2025 and accounted for the largest share of 23.4%. This is attributed to the growing need for 5G system integration services to deliver enhanced Mobile Broadband (eMBB) connectivity to consumers and enterprises.

Asia Pacific is the fastest-growing region over the forecast period.

The global 5G system integration market is expected to grow at a compound annual growth rate of 26.7% from 2026 to 2033 to reach USD 124.8 billion by 2033.

The infrastructure integration segment dominated the market in 2025 and accounted for the largest share of 41.1%. This is attributed to the surging demand for the integration of traditional network infrastructure with next-generation network infrastructure.

The IT and telecom segment dominated the market in 2025. This is attributed to surging demand for 5G integration services across various IT and telecom companies to support new radio (NR) waves.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.