- Home

- »

- Next Generation Technologies

- »

-

Active Electronic Components Market Size Report 2026-2033GVR Report cover

![Active Electronic Components Market (2026 - 2033)Report]()

Active Electronic Components Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product Type (Semiconductor, Vacuum Tubes, Display Devices), By End-use (Consumer Electronics, Networking & Telecommunication, Automotive), By Region, And Segment Forecasts

Market Size, 2025

$358.8BMarket Estimate, 2026

$380.9BMarket Forecast, 2033

$642.8BCAGR, 2026–2033

7.8%Active Electronic Components Market Summary

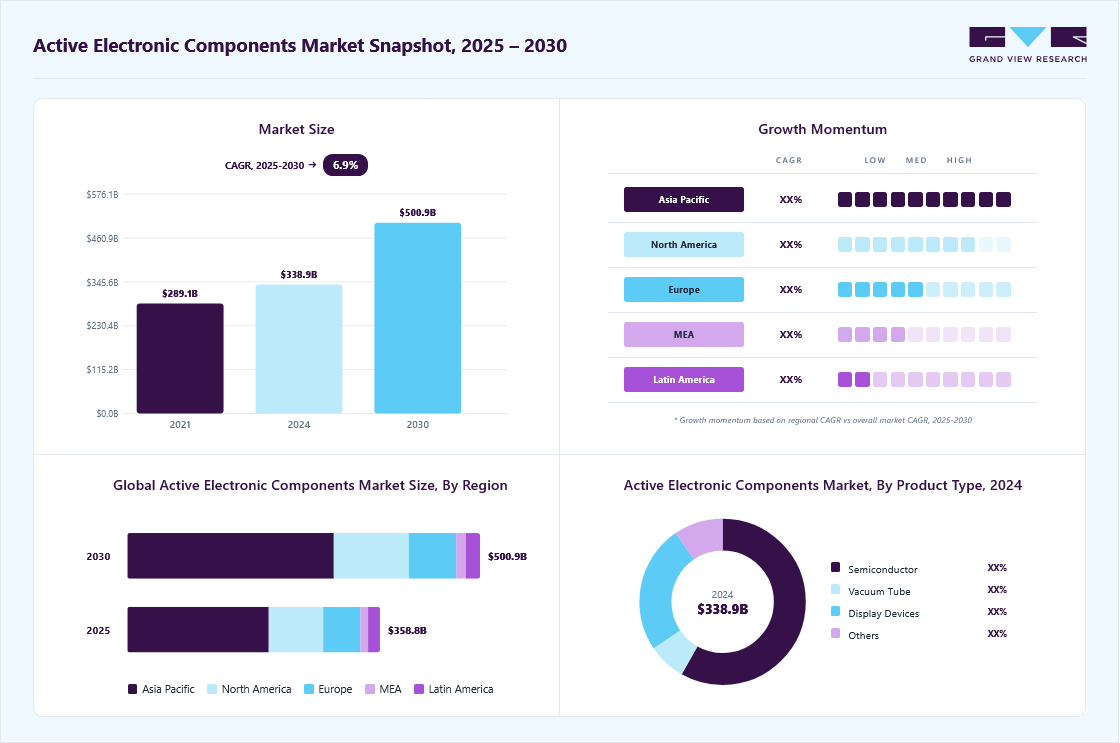

The global active electronic components market size was valued at USD 358.8 billion in 2025 and is projected to grow from USD 380.9 billion in 2026 to USD 642.8 billion by 2033, at a CAGR of 7.8% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 56.0% in 2025. The region's dominance is driven by its strong electronics manufacturing ecosystem, particularly across countries such as China, Japan, South Korea, and India, which serve as major production hubs for semiconductors, integrated circuits, transistors, diodes, and other active electronic components.

Key Market Trends & Insights

- By product type: Semiconductor segment held the largest market share of 58.4% in 2025.

- By end-use: Consumer electronics segment held the largest market share of 32.0% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (56.0% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 358.8 Billion

- Estimated market size in 2026: USD 380.9 Billion

- Projected market size by 2033: USD 642.8 Billion

- CAGR (2026-2033): 7.8%

Rising demand from consumer electronics, automotive electronics, industrial automation, telecommunications, and renewable energy sectors continues to support market growth. These components can act as AC circuits in electronic equipment, increasing power and voltage. All active components require an energy source, usually derived from a DC circuit. Increasing demand for active electronic components in numerous sectors and widespread usage of connected devices are some of the reasons driving this market growth.The increasing popularity of smartphones, laptops, and other wearable devices, as well as increased industrial automation, has raised the demand for active electronic components. The worldwide active electronic components market benefits from increased demand for active electronic components in the healthcare and automotive industries owing to the fast use of MEMS technology. One of the most significant advantages of active electronic components is the ability to manage tiny inputs of electricity to match a greater power output. The most active components are semiconductors, such as diodes, transistors, and integrated circuits.

")

The automotive industry is undergoing a transformation, and there is a rising market for electric vehicles, thus increasing global adoption of different autonomous vehicle technologies. Numerous vehicle applications use the above-mentioned technologies, including parking assistance, safety airbags, telematics, and navigation. Additionally, a considerable rise in consumer smartphone use is anticipated to fuel the booming electronic components market's expansion throughout the projected years. The market expansion is predicted to be further driven by the probable introduction of active electronic components to produce network and communication equipment for 5G infrastructure. As a result, it is anticipated that high demand for these systems will fuel market expansion throughout the projection period.

To attract more customers, automotive manufacturers worldwide are concentrating on integrating numerous electronics and technologies into their products. The growing popularity of premium and ultra-luxury automobiles significantly impacts the automotive active electronic components industry. In July 2022, NXP Semiconductors announced a collaboration agreement with Hon Hai Technology Group to create platforms for a new generation of smart connected automobiles. Hon Hai, an electronics manufacturer and technology solution provider, aims to leverage NXP's automotive technology portfolio and long-standing experience in safety and security to offer architectural innovation and platforms for electrification, connectivity, and safe autonomous driving which in turn will drive the demand of active electronic components in automotive industry.

Market Dynamics

The active electronic components market is witnessing significant growth driven by the increasing demand for advanced electronic devices and the rapid expansion of digital technologies across industries. Active electronic components, including semiconductors, integrated circuits (ICs), transistors, diodes, and power management devices, play a critical role in enabling signal amplification, switching, processing, and power control functions in electronic systems. Growing adoption of consumer electronics, electric vehicles (EVs), industrial automation, 5G infrastructure, data centers, and Internet of Things (IoT) applications is accelerating market expansion. Furthermore, continuous advancements in semiconductor technologies and increasing investments in electronics manufacturing are supporting long-term market growth.

The active electronic components market is primarily driven by the growing demand for smartphones, laptops, wearable devices, smart home products, and other connected electronic devices. Increasing integration of advanced semiconductor components in automotive electronics, industrial automation systems, telecommunications equipment, and renewable energy applications is further fueling market growth. The rapid deployment of 5G networks, expansion of data centers, and rising adoption of artificial intelligence (AI)-enabled devices are creating substantial demand for high-performance integrated circuits, processors, memory chips, and power semiconductor devices. Additionally, government initiatives supporting domestic semiconductor production and electronics manufacturing are contributing to market expansion.

Despite strong growth prospects, the active electronic components market faces challenges related to supply chain disruptions, semiconductor shortages, and rising manufacturing costs. The production of advanced electronic components requires substantial capital investment, sophisticated fabrication facilities, and access to critical raw materials. Geopolitical tensions, trade restrictions, and fluctuations in raw material prices can impact component availability and pricing. Additionally, the increasing complexity of semiconductor manufacturing processes and lengthy product development cycles may pose challenges for manufacturers and affect market growth.

The increasing adoption of electric vehicles, smart connected devices, and Industry 4.0 technologies presents significant growth opportunities for the active electronic components market. EVs require a large number of power semiconductors, sensors, microcontrollers, and battery management components to support vehicle electrification and advanced driver-assistance systems (ADAS). Similarly, the proliferation of IoT devices, smart factories, robotics, and intelligent infrastructure is driving demand for high-performance electronic components capable of enabling real-time data processing and connectivity. Furthermore, ongoing investments in next-generation semiconductor technologies, renewable energy systems, and advanced communication networks are expected to create new revenue opportunities for market participants over the forecast period.

Market Concentration & Characteristics

The active electronic components market is moderately concentrated, characterized by the presence of several global semiconductor manufacturers and electronic component suppliers competing on technological innovation, product performance, manufacturing scale, energy efficiency, and application-specific solutions. Major players such as Infineon Technologies AG, Advanced Micro Devices Inc., STMicroelectronics N.V., Microchip Technology, Inc. hold significant positions in the market. Other prominent participants include Analog Devices, Inc.; Broadcom Inc., NXP Semiconductors N.V., Intel Corporation, Monolithic Power Systems, Inc., Texas Instruments Incorporated, Qualcomm Inc.. Continuous investments in advanced semiconductor fabrication, power electronics, automotive-grade chips, AI accelerators, IoT-enabled components, and 5G communication technologies are intensifying competition and fostering innovation across the market.

Analyst Perspective

The active electronic components market is positioned as a fundamental enabler of modern electronic systems, driven by the growing demand for advanced semiconductors, intelligent devices, high-speed connectivity, and energy-efficient technologies across industries such as consumer electronics, automotive, networking & telecommunications, manufacturing, aerospace & defense, and healthcare. Active electronic components play a critical role in enabling data processing, signal amplification, power management, sensing, and communication functions within increasingly sophisticated electronic products and infrastructure.

The market is benefiting from continuous advancements in semiconductor technologies, artificial intelligence (AI) hardware, 5G communications, industrial automation, Internet of Things (IoT) ecosystems, and electric vehicle (EV) platforms. Increasing integration of processors, memory devices, power semiconductors, sensors, and display technologies is enhancing device performance, connectivity, and operational efficiency across end-use applications. Furthermore, ongoing investments in semiconductor fabrication capacity, next-generation chip architectures, advanced packaging technologies, and high-performance computing solutions are strengthening the market's growth outlook.

Product Type Insights

Based on product type, the semiconductor segment led the market with the largest revenue share of 58.4% in 2025, and is also anticipated to witness the fastest growth, growing at a CAGR of 8.3% during the forecast period. Integrated circuits (ICs), the sub-segment of semiconductor devices, dominated the overall market, gaining a market share of 56.9% in 2025, and is also to witness the fastest growth, growing at a CAGR of 9.2%. A semiconductor substance exists between the insulator and the conductor, which controls and regulates the current flow in electrical devices and equipment. As a result, it has become an essential component of electronic chips used in computing components and various electronic devices, such as solid-state storage.

An SMD (Surface Mount Device) electronic component made of multiple transistors, diodes, resistors, and capacitors in a tiny semiconductor chip are an Integrated Circuit (IC). ICs, or Integrated Circuit Electronic Components, are small and light, providing more significant outcomes while using less power. An Integrated Circuit (IC) is the integration or assimilation of several electronic components (primarily transistors) on a chip (or single device) constructed of a semiconductor material. ICs are extensively utilized in various applications such as televisions, mobile phones, laptops, audio players, routers, etc.

End-use Insights

Based end user, the consumer electronics segment led the market with the largest revenue share of 32.0% in 2025. It is expected to grow at the fastest CAGR of 8.8% throughout the forecast period. The expansion is primarily due to rising demand for semiconductor devices for various consumer electronics such as digital cameras, mobile phones, gaming devices, wearable devices, Set-Top Boxes (STB), and others. Moreover, networking equipment such as modems, routers, repeaters, and gateways are in great demand, especially in the office automation and home application segments. Active electronics components are predicted to increase over the forecast period due to increased demand for network devices and other IT equipment. In June 2022, Nokia Corporation, a Finland-based telecommunication, IT, and consumer electronics company, has launched a new Fiber-ToThe-Home (FTTH) kit to help service providers deliver fiber networks to rural regions in the U.S. The package contains all the equipment and licenses for the operator to set up a standard 1,000-home community. The package includes active equipment for the central office (OLT or the optical line terminal), a fiber termination device for the home (ONT or the optical network terminal), and Wi-Fi modules inside the house. Over a single port, the kits support GPON and XGS-PON.

The automotive segment is anticipated to grow at a considerable CAGR of 8.4% throughout the forecast period. Automotive manufacturers worldwide focus on integrating various electronics and technology to attract customers. The increasing popularity of premium and ultra-luxury vehicles has considerably influenced the automotive active electronic components industry. Vehicles' reliance on electronic components and safety systems has grown significantly in recent years, resulting in increased use of electronic components in vehicles. Electronic components are frequently used to increase the functioning and efficiency of powertrain systems. These components let an automobile's powertrain systems exchange messages and sensor signals while also managing their operations. In powertrain systems, turbine speed, transmission fluid temperature, and throttle position sensors are all used.

Regional Insights

The North America active electronic components market is anticipated to grow at a considerable CAGR of 7.4% throughout the forecast period. In North America, the adoption of connected cars is gaining significant traction, particularly in the U.S. Leading telecom service providers, such as Verizon Inc. and AT&T Inc., are investing aggressively in deploying the next-generation 5G network infrastructure to provide unified connectivity between vehicles and the network infrastructure. The outbreak of the COVID-19 pandemic may have delayed the industrial deployment of 5G in the U.S. However, the U.S. government is trying to overcome this delay by investing aggressively in rolling out highly efficient network infrastructure and building smart cities. As such, the installation of telecom equipment and other networking devices is expected to gain traction in line with the unabated rollout of 5G network infrastructure across North America, thereby driving the growth of the North America active electronic components market over the forecast period.

U.S. Active Electronic Components Market Trends

The U.S. active electronic components market is projected to experience steady growth, driven by advancements in technology and increasing demand across various sectors, including consumer electronics, automotive, telecommunications, and industrial applications. Additionally, the growth of the Internet of Things (IoT) and increasing reliance on renewable energy sources are further driving demand for active electronic components.

Asia Pacific Active Electronic Components Market Trends

Asia Pacific dominated the active electronic components market with the largest revenue share of 56.0% in 2025. The Asia Pacific dominates the global electronics sector and is mainly regarded as a manufacturing powerhouse for consumer electronics. Due to a variety of favorable factors, including relatively lower labor costs, the availability of a large pool of highly skilled workers, rising foreign direct investments, government initiatives supporting the production of electronic components, and preferential trading access to Europe and North America, Asia Pacific has emerged as the most prominent electronics manufacturing and exporting region. China, India, Vietnam, and Malaysia are among the leading Asia Pacific economies helping to drive the region's electronics sector growth. Over the projection period, these economies will likely strengthen their position in the semiconductor sector and grow their share of the worldwide market.

Key Active Electronic Components Company Insights

Some of the key players operating in the market include Intel Corporation and Qualcomm Inc., among others.

-

Intel Corporation is a prominent U.S. based multinational technology company headquartered in California. The company is one of the largest semiconductor chip manufacturers globally, specializing in designing, manufacturing, and selling a wide range of computer components and related products for both business and consumer markets. Intel Corporation offers a diverse range of active electronic components, including microprocessors such as the Core, Xeon, and Atom series, which are essential for personal computers, servers, and embedded systems. The company also produces chipsets that enhance processor functionality, along with memory products like its 3D NAND technology used in solid-state drives (SSDs).

Texas Instruments Incorporated and Renesas Electronics Corporation are some of the emerging market participants in the target market.

-

Microchip Technology, Inc., founded in 1989 and headquartered in Arizona, U.S. is a provider of microcontroller and analog semiconductor solutions. The company specializes in developing embedded control solutions for a variety of applications, including automotive, industrial, consumer electronics, and IoT devices. It offers an extensive portfolio of microcontrollers, which are designed for a range of functionalities, from simple applications to complex systems requiring high performance. Additionally, the company offers a comprehensive range of analog products, including operational amplifiers, voltage references, and power management solutions, which are essential for signal conditioning and power efficiency in electronic devices.

Key Active Electronic Components Companies

The following key companies have been profiled for this study on the active electronic components market.

- Infineon Technologies AG

- Advanced Micro Devices, Inc.

- STMicroelectronics N.V.

- Microchip Technology, Inc.

- Analog Devices, Inc.

- Broadcom Inc.

- NXP Semiconductors N.V.

- Intel Corporation

- Monolithic Power Systems, Inc.

- Texas Instruments Incorporated

- Qualcomm Inc.

- Renesas Electronics Corporation

- Semiconductor Components Industries, LLC

- Toshiba Corporation

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Intel Corporation, Infineon Technologies AG, STMicroelectronics N.V., NXP Semiconductors N.V., Texas Instruments Incorporated, Qualcomm Inc., Broadcom Inc., Renesas Electronics Corporation)

- Focus on expanding semiconductor and active component portfolios through advanced process technologies, power electronics innovation, automotive semiconductor development, AI-enabled chips, and strategic manufacturing investments. Emphasize long-term supply agreements, vertical integration, capacity expansion, and R&D to maintain technological leadership

- Strong global market presence, extensive manufacturing capabilities, diversified product portfolios, established customer relationships, advanced fabrication technologies, large-scale R&D investments, and strong positions across automotive, industrial, consumer electronics, and communications sectors.

- High capital expenditure requirements, exposure to semiconductor industry cyclicality, supply chain vulnerabilities, geopolitical risks, pricing pressures, and lengthy product development and qualification cycles.

Emerging Players (Advanced Micro Devices, Inc., Microchip Technology, Inc., Analog Devices, Inc., Monolithic Power Systems, Inc., Semiconductor Components Industries, LLC, Toshiba Corporation)

- Focus on specialized active electronic components including power semiconductors, discrete devices, optoelectronics, circuit protection solutions, and application-specific products. Invest in product innovation, strategic partnerships, regional expansion, and high-growth sectors such as electric vehicles, renewable energy, industrial automation, and IoT.

- Strong expertise in niche component categories, agile product development, specialized engineering capabilities, growing presence in high-growth applications, and ability to address specific customer requirements.

- Smaller market share relative to leading semiconductor manufacturers, limited manufacturing scale, lower bargaining power with large OEMs, dependence on specific product categories, and challenges in competing with larger players on R&D spending and global distribution reach.

Recent Developments

-

In September 2024, Intel Corporation launched its new Core Ultra 200V series mobile processors, offering significant advancements in AI, graphics, and energy efficiency for laptops. Featuring AI Acceleration and integrated GPU upgrades, the processors are designed to handle intensive computing tasks with reduced power consumption. These chips are targeted at a range of applications, from gaming to creative content production, enhancing both performance and battery life.

-

In September 2024, Qualcomm Inc. introduced new advancements for PC users with its Snapdragon X Plus, boosting performance in AI-powered features like Copilot. This processor enhances productivity, collaboration, and entertainment with AI acceleration and superior efficiency. Qualcomm is positioning itself as a leader in AI-driven computing solutions, aiming to optimize experiences in connected PCs while maintaining high energy efficiency and powerful processing capabilities.

Active Electronic Components Market Report Scope

Report Attribute

Details

Market size in 2025

USD 358.8 billion

Estimated market size in 2026

USD 380.9 billion

Projected market size by 2033

USD 642.8 billion

Growth rate

CAGR of 7.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product Type, End-use & Region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; U.K; France; China; Japan; India; Singapore, Malaysia, South Korea; Australia; Brazil; Saudi Arabia; South Africa; UAE;

Key companies profiled

Infineon Technologies AG; Advanced Micro Devices, Inc.; STMicroelectronics N.V.; Microchip Technology, Inc.; Analog Devices, Inc.; Broadcom Inc.; NXP Semiconductors N.V.; Intel Corporation; Monolithic Power Systems, Inc.; Texas Instruments Incorporated; Qualcomm Inc.; Renesas Electronics Corporation; Semiconductor Components Industries, LLC; Toshiba Corporation.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Active Electronic Components Market Report Segmentation

This report forecasts market revenue growths at global, regional, as well as at country levels. It offers an analysis of the qualitative and quantitative market trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global active electronic components market report based on product type, end-use, and region.

-

Product Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Semiconductor Devices

-

Diode

-

Transistors

-

Integrated Circuits (ICs)

-

Optoelectronics

-

-

Vacuum Tube

-

Display Devices

-

Others

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Consumer Electronics

-

Networking & Telecommunication

-

Automotive

-

Manufacturing

-

Aerospace & Defense

-

Healthcare

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia-Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

Mexico

-

-

Middle East & Africa

-

Research Methodology

The active electronic components market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each active electronic components segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Product Type

Revenue capture definition

Semiconductor

Revenue in this segment is generated through the design, fabrication, packaging, testing, and sale of semiconductor devices and components used across a wide range of electronic applications. These products include microprocessors, microcontrollers, memory devices, logic ICs, analog ICs, power semiconductors, sensors, and discrete components

Vacuum Tube

Revenue in this segment is generated through the manufacturing and sale of vacuum tubes used for amplification, switching, rectification, signal modulation, and power generation applications. These products include transmitting tubes, receiving tubes, microwave tubes, phototubes, cathode-ray tubes, and specialized vacuum electronic devices.

Display Devices

Revenue in this segment is generated through the manufacturing and sale of display technologies and display modules used for visual information presentation across consumer, commercial, industrial, and automotive applications. These products include liquid crystal displays (LCDs), light-emitting diode (LED) displays, organic light-emitting diode (OLED) displays, micro-LED displays, electronic paper displays, and related display panels and components

Others

The segment includes products such as thyristors (SCRs), triacs, diacs, optoelectronic devices (including laser diodes, photodiodes, and optocouplers), power modules, hybrid electronic circuits, and specialized RF and microwave devices

Segment - End User

Revenue capture definition

Consumer Electronics

Revenue in this segment is generated through the use and integration of active electronic components in consumer electronic devices designed for personal, household, entertainment, and communication applications. These components include semiconductors, integrated circuits, processors, memory devices, display drivers, power management ICs, sensors, and other active electronic devices that enable computing, connectivity, signal processing, display, and power control functions

Networking & Telecommunication

Revenue in this segment is generated through the use and integration of active electronic components in networking and telecommunications equipment that enable data transmission, signal processing, wireless connectivity, and communication infrastructure operations. These components include semiconductors, integrated circuits (ICs), processors, memory devices, RF components, power management devices, transistors, and optoelectronic components that support high-speed communication and network performance.

Automotive

Revenue in this segment is generated through the use and integration of active electronic components in automotive systems that enable vehicle control, electrification, connectivity, safety, and infotainment functions. These components include semiconductors, microcontrollers, integrated circuits (ICs), power devices, sensors, memory chips, processors, and display drivers that support vehicle performance, energy management, and advanced electronic functionalities.

Manufacturing

Revenue in this segment is generated through the use and integration of active electronic components in industrial and manufacturing equipment to enable automation, process control, monitoring, power management, and intelligent production operations. These components include semiconductors, integrated circuits (ICs), microcontrollers, power devices, sensors, processors, memory components, and communication modules that support efficient and reliable manufacturing processes.

Aerospace and Defence

Revenue in this segment is generated through the use and integration of active electronic components in aerospace and defense systems that support communication, navigation, surveillance, electronic warfare, flight control, and mission-critical operations. These components include semiconductors, integrated circuits (ICs), processors, memory devices, power electronics, RF and microwave components, sensors, optoelectronic devices, and specialized high-reliability electronic systems designed to operate in demanding environments.

Healthcare

Revenue in this segment is generated through the use and integration of active electronic components in medical and healthcare devices that enable diagnostics, monitoring, imaging, treatment, and patient care applications. These components include semiconductors, integrated circuits (ICs), microprocessors, sensors, memory devices, power management components, optoelectronic devices, and communication modules that support the operation and performance of advanced medical equipment.

Others

Revenue in this segment is generated through the use and integration of active electronic components in applications that fall outside the primary end-use industries of consumer electronics, networking & telecommunications, automotive, manufacturing, aerospace & defense, and healthcare. These components include semiconductors, integrated circuits (ICs), sensors, power devices, optoelectronic components, and other active electronic devices used for signal processing, control, connectivity, and power management functions.

Estimation Model

Layer Name

Key Question

Description

Addressable Electronics Manufacturing & End-Use Base Layer

Which industries require active electronic components?

Identify the global addressable base of industries and applications that utilize active electronic components, including consumer electronics, automotive, networking & telecommunications, manufacturing, aerospace & defense, healthcare, energy, and other industrial sectors. components.

Component Penetration Layer

Which devices and systems deploy active electronic components?

Apply component penetration rates across end-use applications based on the adoption of processors, memory chips, integrated circuits (ICs), power semiconductors, sensors, display modules, RF devices, and other active electronic components within electronic products and equipment.

Component Consumption Layer

How extensively are active electronic components utilized?

Estimate component consumption based on the average number and value of active electronic components integrated per device, equipment unit, vehicle, communication system, industrial machine, or healthcare device.

Revenue Generation Layer

How much revenue is generated?

Multiply the volume of active electronic components shipped across applications by their average selling prices (ASPs), considering revenues from semiconductors, display devices, vacuum tubes, and other active electronic components.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Competitive Landscape & Strategic Benchmarking

Conducted a comprehensive assessment of leading semiconductor manufacturers, active electronic component suppliers, integrated device manufacturers (IDMs), and power electronics providers. Evaluated competitive positioning, product portfolios, semiconductor technologies, manufacturing capabilities, end-market exposure, supply chain strategies, and recent strategic developments to benchmark performance across the active electronic components ecosystem.

Analyzed the impact of advanced semiconductor technologies, power electronics, 5G infrastructure, IoT connectivity, electric vehicle electronics, advanced packaging solutions, and next-generation display technologies on market evolution. Identified emerging growth pockets, whitespace opportunities, and high-potential application areas across major end markets.

End-Use Demand & Application Analysis

Assessed demand trends across key application sectors, including consumer electronics, automotive, networking & telecommunications, manufacturing, aerospace & defense, healthcare, and industrial automation. Evaluated component adoption patterns, technology requirements, purchasing trends, and growth drivers across major end-use industries.

Provides actionable insights into demand drivers, component consumption patterns, high-growth application areas, and emerging industry trends, supporting market-entry, expansion, and commercialization strategies.

Technology Innovation & Growth Opportunity Assessment

Analyzed the impact of advanced semiconductor technologies, power electronics, 5G infrastructure, IoT connectivity, electric vehicle electronics, advanced packaging solutions, and next-generation display technologies on market evolution. Identified emerging growth pockets, whitespace opportunities, and high-potential application areas across major end markets.

Supports strategic growth planning by identifying attractive investment areas, prioritizing technology development opportunities, evaluating future revenue streams, and understanding the structural trends shaping the long-term evolution of the active electronic components market.

Frequently Asked Questions About This Report

The global active electronic components market is expected to grow at a compound annual growth rate of 7.8% from 2026 to 2033 to reach USD 642.8 billion by 2033.

The semiconductor devices segment held the highest revenue share of over 58.4% in 2025 in the active electronic components market, and is estimated to expand further at the fastest CAGR from 2026 to 2033.

Some of the key players operating in the active electronic components market include Infineon Technologies AG; NXP Semiconductors NV; Texas Instruments Incorporated; Toshiba Corporation; STMicroelectronics; Semiconductor Components Industries, LLC; Intel Corporation; Maxim Integrated; Renesas Electronics Corporation; Broadcom Inc.; Qualcomm Inc.; Analog Devices, Inc.; Advanced Micro Devices; and Microchip Technology Inc.

The global active electronic components market size was valued at USD 358.8 billion in 2025 and is expected to reach USD 380.9 billion in 2026.

U.S. leads the North America market with revenue share of 74.0% in 2025, While Canada is the fastest growing country in the region.

China leads the Asia Pacific market with revenue share of 45.0% in 2025, While India is the fastest growing country in the region.

Germany leads the Europe market with revenue share of 32.6% in 2025, While France is the fastest growing country in the region.

The consumer electronics segment led the global market for active electronic components in 2025, accounting for the highest revenue share of 32.0%. The segment is expected to expand further at the fastest CAGR of 8.8% over the forecast period.

Asia Pacific held the highest revenue share of over 56.0% in 2025 in the active electronic components market and is estimated to exhibit the fastest CAGR in the market.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.