- Home

- »

- Pharmaceuticals

- »

-

Active Pharmaceutical Ingredients Market Report, 2026-2033GVR Report cover

![Active Pharmaceutical Ingredients Market (2026 - 2033)Report]()

Active Pharmaceutical Ingredients Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type Of Synthesis (Biotech, Synthetic), By Type Of Manufacturer (Captive, Merchant), By Type, By Application, By Type of Drug, By Region, And Segment Forecasts

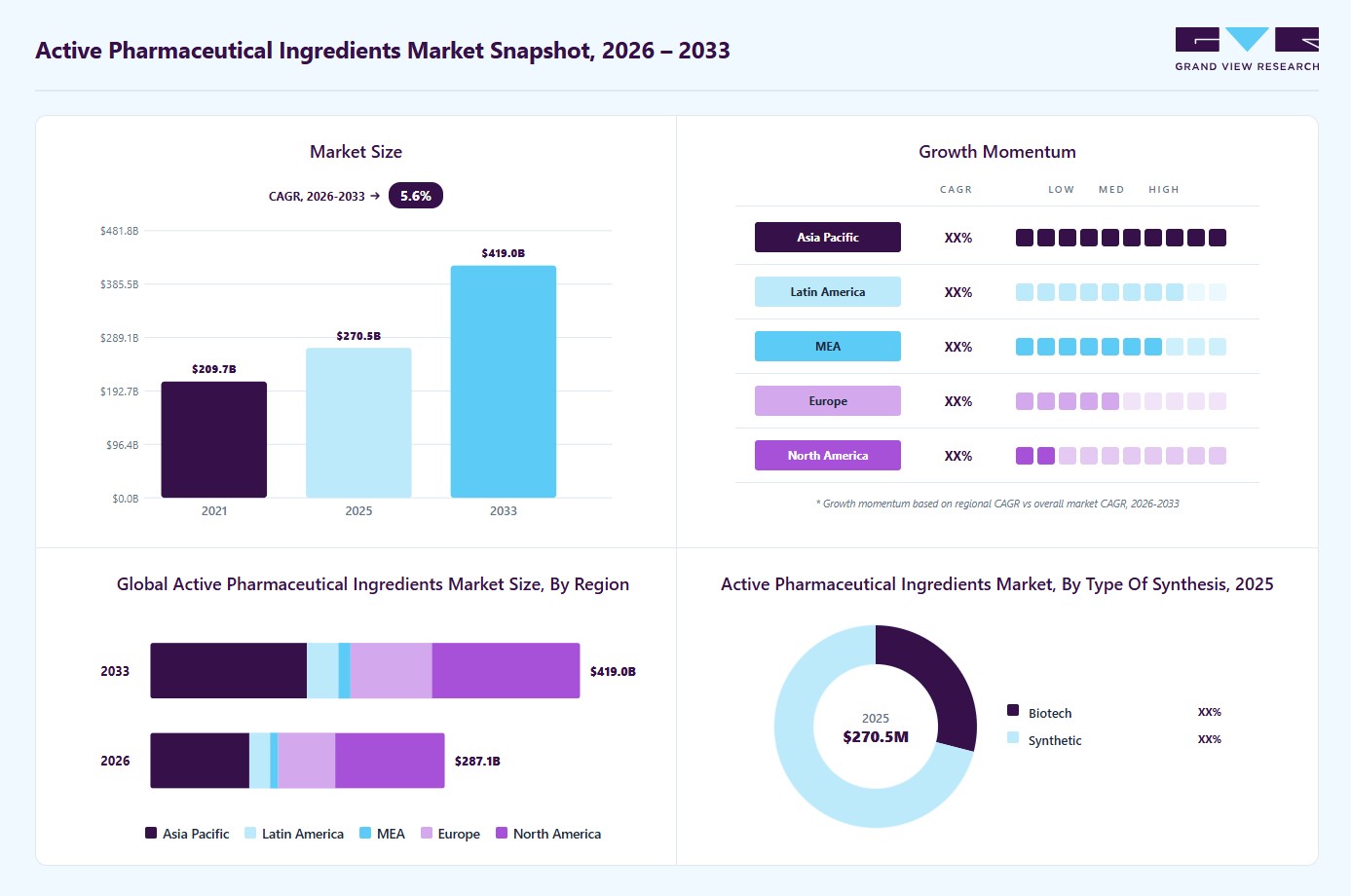

Market Size, 2025

$270.5BMarket Estimate, 2026

$287.1BMarket Forecast, 2033

$419.0BCAGR, 2026–2033

5.6%Active Pharmaceutical Ingredients Market Summary

The global active pharmaceutical ingredients market size was valued at USD 270.5 billion in 2025 and is projected to grow from USD 287.1 billion in 2026 to USD 419.0 billion by 2033, at a CAGR of 5.6% from 2026 to 2033. The market in North America dominated with a revenue share of 37.7% in 2025. The rising global demand for pharmaceuticals, especially in emerging markets, drives growth due to increasing chronic diseases like cancer, diabetes, and cardiovascular conditions.

Key Market Trends & Insights

- By type of synthesis: Synthetic segment held the largest market share of 70.9% in 2025.

- By type of manufacturer: Captive APIs segment held the largest market share of 50.6% in 2025.

- By type: Innovative APIs segment held the largest market share of 53.8% in 2025.

- By application: Cardiology segment held the largest market share of 20.9% in 2025.

- By type of drug: Prescription segment held the largest market share of 79.5% in 2025.

Regional Highlights

- Largest regional market: North America (37.7% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 270.5 Billion

- Estimated market size in 2026: USD 287.1 Billion

- Projected market size by 2033: USD 419.0 Billion

- CAGR (2026-2033): 5.6%

Advancements in biologics and biosimilars, along with innovative drug formulations, are further boosting the need for specialized APIs. Moreover, the shift toward generic medicines and the rise in contract manufacturing organizations (CMOs) are accelerating API production and distribution, driving the growth of the active pharmaceutical ingredients industry.The global geriatric population is increasing. According to the UN, in 2023, people aged 65 and above accounted for approximately 771 million of the population, and the number is expected to reach 994 million by 2030, and 1.6 billion by 2050. The number of older adults is showing the fastest growth in Africa, with a threefold increase estimated in people aged 60 and above, followed by Latin America, which is projected to reach 18.8 billion by 2050. Aging is considered the greatest risk factor for the development of diseases, including cardiovascular and neurological diseases. Thus, the rapidly growing global geriatric population is becoming a high-impact driver for the API market.

")

The increasing prevalence of infectious diseases and hospital-acquired infections is driving market growth. Additionally, the increasing prevalence of cardiovascular, genetic, and neurological disorders is expected to be a significant driver of market growth. Cardiovascular Diseases (CVDs) are the most prevalent causes of death globally. According to the WHO, cardiovascular diseases cause the deaths of 17.9 million people per day and are expected to cause approximately 25 million deaths by 2030. The increasing epidemiology of lifestyle, aided by the rising number of smokers globally, the growing incidence of obesity, and increasing dietary irregularities, is likely to propel market growth. A recent report by the United Nations (UN) in May 2023 suggests that there has been a 75% increase in the number of girls and 61% in the number of boys with obesity in Europe.

Outsourcing of APIs has become profitable over in-house production. However, this trend took a different turn during the COVID-19 pandemic. Companies are seeking to diversify their API suppliers and manufacturers across different locations, rather than outsourcing to a single manufacturer. Additionally, risk mitigation is achieved through dual sourcing to ensure a continuous supply. Hence, key companies aim to capitalize on this ongoing outsourcing trend with new acquisitions. For instance, in August 2023, EUROAPI announced its acquisition deal with BianoGMP to enhance its CDMO expertise in oligonucleotide manufacturing, a high-growth industry. This further demonstrates the company’s plans for vertical integration.

In addition, pharmaceutical companies are increasingly relying on partners with advanced, audit-ready capabilities as regulations place a greater emphasis on transparency in production and demanding quality-assurance standards, such as enhanced GMP compliance and serialization requirements. At the same time, the rapid expansion of precision medicine and targeted medicines is increasing the demand for highly specialized, small-batch API production. Growing investments in green chemistry and process intensification technologies are accelerating the move to more efficient and sustainable API synthesis. Furthermore, pharmaceutical developers are prioritizing supply chain resilience, accelerating the development of localized and near-shore CDMO collaborations to address geopolitical and logistical challenges. The rise in complicated small compounds, high-potency APIs, and banned drugs has increased the requirement for CDMOs with a specific understanding and containment facilities. These factors are shaping a more technology-enabled and strategically diversified active pharmaceutical ingredients CDMO market.

The growing demand for contamination-free and high-quality drug products is driving the growth of the sterile active pharmaceutical ingredients market, primarily due to an increase in the need for injectable therapies, biologics, and lyophilized pharmaceuticals, all of which require specialized sterile production techniques. Recent developments in sterile API production facilities, such as Akums Drugs and Pharmaceuticals' new lyophilized and injectable manufacturing site, set to open in 2025, and Piramal Pharma Solutions' USD 80 million expansion of sterile injectables in Kentucky, highlight the growing emphasis on aseptic processing and strict GMP compliance. Furthermore, the rising frequency of chronic and complex disorders emphasizes the need for safe and dependable injectable formulations. Global Contract Development and Manufacturing Organizations (CDMOs) are expanding their sterile manufacturing capacities to meet demand in both the clinical and commercial phases, ensuring that the sterile API market continues to grow strongly.

Market Dynamics

The rising demand for generic pharmaceuticals has been a major driver for the Active Pharmaceutical Ingredients (API) market, supported by increasing patent expirations, growing cost pressures, and expanding access to affordable medicines worldwide. Pharmaceutical manufacturers have significantly increased the production of generic drugs to meet the growing demand for low-cost treatment options, thereby accelerating the requirement for high-volume and cost-efficient API manufacturing across developed and emerging economies. In addition, governments and healthcare organizations have increasingly promoted generic drug adoption to reduce overall healthcare expenditures, further strengthening API consumption globally. For instance, in October 2025, the U.S. Food and Drug Administration (FDA) announced a pilot program to accelerate reviews of abbreviated new drug applications (ANDAs) manufactured in the United States. The FDA stated that more than 50% of pharmaceuticals used in the U.S. had been manufactured overseas, while only 9% of API manufacturers had been located domestically, compared with 22% in China and 44% in India.

Stringent regulatory requirements and compliance challenges have been a major restraint for the Active Pharmaceutical Ingredients (API) market, as manufacturers have faced increasing pressure to comply with strict quality, safety, and environmental standards imposed by global regulatory authorities. API producers have been required to invest significantly in facility modernization, quality control systems, and regulatory documentation processes, increasing overall operational costs and extending approval timelines. In addition, regulatory inspections and import restrictions have disrupted pharmaceutical supply chains and negatively affected production capacities for several manufacturers. For instance, in January 2024, the U.S. Food and Drug Administration (FDA) issued a warning letter to Sun Pharmaceutical Industries’ Halol facility in India for significant violations of current Good Manufacturing Practice (cGMP) regulations. The FDA identified deficiencies related to data integrity, inadequate equipment maintenance, and poor contamination control practices, highlighting the growing regulatory scrutiny and compliance burden faced by API and pharmaceutical manufacturers globally.

The growing expansion of biopharmaceuticals and specialty drug manufacturing has created significant growth opportunities for the Active Pharmaceutical Ingredients (API) market, driven by rising demand for targeted therapies, biologics, and advanced treatment solutions worldwide. Pharmaceutical and biotechnology companies have increasingly invested in high-potency APIs (HPAPIs), peptide APIs, and biologic drug production to address the growing prevalence of cancer, autoimmune disorders, and rare diseases. In addition, advancements in biotechnology and personalized medicine have accelerated the need for specialized API manufacturing capabilities across global healthcare markets. For instance, in March 2024, Eli Lilly announced plans to invest USD 5.3 billion in a new manufacturing facility in Indiana, increasing the company’s total investment in the site to USD 9 billion to support active pharmaceutical ingredient production for obesity and diabetes medicines. The investment highlighted the rising industry focus on expanding advanced API manufacturing capacity for next-generation therapeutics.

Market Concentration & Characteristics

The market for Active Pharmaceutical Ingredients (API) is rapidly changing, driven by advances in synthetic biology, biocatalysis, and continuous processing that are transforming API discovery and manufacture. The growing need for complex compounds, such as highly powerful active pharmaceutical ingredients (HPAPIs), nucleic acid medicines, and tailored cancer treatments, is driving investment in new process technologies and containment methods. AI-driven design and automation are also accelerating development plans and improving molecular accuracy.

M&A activity in the active pharmaceutical Ingredients market is medium, driven by strategic consolidation, capability enhancement, and the advancement of operational efficiency. Many pharmaceutical companies and contract manufacturers are seeking acquisitions to expand their product lines, increase manufacturing capacity, and gain expertise in high-growth sectors, such as biologics, highly potent active pharmaceutical ingredients (HPAPIs), and complex generics. Nonetheless, mergers and acquisitions are slowed due to regulatory scrutiny, high valuation premiums, and the technical difficulties associated with merging API manufacturing plants.

Regulation has a significant impact on the active pharmaceutical ingredients industry, as it influences production standards, quality requirements, and global trade dynamics. The FDA, EMA, and national health agencies enforce stringent standards for quality control, documentation, traceability, and compliance with Good Manufacturing Practices (GMP) throughout the API lifecycle. While these requirements are critical to ensuring patient safety, they also provide significant operational and financial challenges for manufacturers. The increase in regulatory audits and the push toward international standard harmonization, such as ICH Q7 and Q11, require significant investment in modern facilities, digital quality-management systems, and continuous monitoring technological advancements.

The growth of product offerings in the Active Pharmaceutical Ingredients market is relatively limited due to the specialized requirements of API development, lengthy regulatory processes, and large capital investments. In contrast to consumer-oriented markets, the API product range evolves gradually, as novel compounds must go through extensive research, testing, and approval before they can enter commercial manufacturing. Instead of producing new goods on a regular basis, many manufacturers focus on improving existing APIs or increasing process efficiency.

The API market is growing moderately across geographies, driven by increased demand for diverse supply chains, low-cost manufacturing, and proximity to key pharmaceutical centers. The Asia-Pacific area, particularly India, China, and South Korea, continues to attract investments due to its strong industrial capabilities and expanding innovation environment. Concurrently, geopolitical risks and regulatory pressures are driving corporations in North America and Europe to regionalize production and reduce their reliance on single-source Asian suppliers. Emerging markets in Latin America, the Middle East, and Eastern Europe are becoming more attractive for capacity growth, thanks to improved regulatory conditions and government incentives.

Type of Synthesis Insights

The synthetic segment captured the largest revenue share of 70.99% in 2025. The primary driver behind the synthetic API market is the strong demand for generic drugs, which significantly contributes to revenue for companies involved in synthetic and chemical API manufacturing. This creates substantial opportunities for Contract Development and Manufacturing Organizations (CDMOs) operating in this segment. The appeal of the synthetic API market is further heightened for CDMOs due to the growing trend of outsourcing, as companies seek to enhance profitability by lowering production costs. In October 2023, Cambrex announced the completion of its USD 38 million small molecule API manufacturing facility, effectively doubling the size of its operations and improving its capacity to attract new customers to meet their changing requirements.

The biotech API segment is projected to experience the fastest growth during the forecast period, driven by increasing investments in the biopharmaceutical and biotechnology sectors. These investments facilitate the development of new molecules that can effectively treat diseases like cancer. Major players are placing significant emphasis on biotech APIs due to their potential to generate high revenue and achieve profitability. For instance, in May 2023, the OLON Group announced its entry into the Antibody Drug Conjugate (ADC) API market with a new facility in Italy, investing approximately €22 million (USD 23.13 million) in production that meets a containment level of OEB6.

Type of Manufacturer Insights

The captive APIs segment led the active pharmaceutical ingredients industry, accounting for the largest share of 50.58% in 2025. An increasing number of companies are investing in overcoming challenges and developing new chemical methods for in-house API production. This approach helps lower costs and minimize the risk of contamination. Advances in protein synthesis and artificial intelligence are expected to enhance development by providing greater control over the manufacturing process. Moreover, recent initiatives by major players show a strong inclination toward in-house production rather than outsourcing. For instance, in August 2025, AbbVie announced a USD 195 million investment to improve its API manufacturing plant in North Chicago, with the goal of increasing domestic API production capabilities and supporting the company's portfolio of neurology, immunology, and oncology medicines. Initiatives like these from significant industry stakeholders are expected to drive growth in this sector.

The Merchant APIs segment is expected to experience the fastest growth during the forecast period. A notable trend in the pharmaceutical sector is the growing use of contract manufacturing and outsourcing for the development of API molecules. Given the high costs associated with captive production of APIs, many companies are turning to outsourcing as a means to reduce expenses. Merchant APIs offer a solution by eliminating the need for significant investments in costly equipment and advanced infrastructure. In the post-pandemic landscape, leading companies are enhancing their capacities to strengthen their market positions. For instance, in May 2023, MilliporeSigma announced a $69 million expansion of its facility in the U.S., which will double its manufacturing capacity for Highly Potent Active Pharmaceutical Ingredients (HPAPIs). This facility will focus on the development and commercial manufacturing of Antibody Drug Conjugates (ADCs).

Type Insights

The innovative APIs segment held the largest share of the overall API market, accounting for 53.82% of revenue in 2025. This growth can be attributed to increased funding and favorable regulations for research and development facilities. A number of novel products are currently in the pipeline due to extensive research in this area, with many expected to launch in the near future. Moreover, growing support from regulatory agencies for the approval of new drugs is anticipated to enhance market growth further, reflecting a heightened focus by governments on healthcare and the pharmaceutical sector.

The generic APIs segment is expected to experience the fastest growth during the forecast period. The expiration of patents for various branded molecules presents significant opportunities for the growth of generic API drugs. Following the pandemic, the pharmaceutical industry is approaching a patent cliff by 2030, with nearly 200 molecules scheduled to lose exclusivity and over 100 biosimilars currently in development as of 2023. This trend creates a favorable environment for generic API manufacturers, as the demand for these APIs is projected to increase significantly by the end of the decade. This includes more than 60 molecules within the oncology segment that are associated with complex, high-revenue-generating APIs.

Application Insights

The cardiology segment led the API industry, with a revenue share of 20.91% in 2025, driven by the increasing global prevalence of cardio vascular diseases (CVDs). As per the CDC, heart disease is the leading cause of death in the U.S. for men, women, and people across most racial and ethnic groups. In 2024, cardiovascular disease continues to pose a severe public health burden, with one person dying from it every 34 seconds. Cardiovascular disease represents a significant public health challenge, prompting substantial research into APIs within this field. Notable APIs include Simvastatin, a cholesterol-lowering medication from the statin class used to treat dyslipidemia, and Rosuvastatin calcium, another API utilized for cardiovascular conditions by AstraZeneca.

The oncology segment is projected to experience the fastest CAGR during the forecast period, driven primarily by the rising global prevalence of cancer. According to the American Cancer Society, an estimated 2,001,140 new cancer cases are expected in the U.S. in 2024. Collaborative efforts among pharmaceutical companies, research institutions, and regulatory bodies play a crucial role in accelerating drug development, ensuring patient safety, and promoting innovation. For instance, in March 2023, Pfizer Inc. and Seagen Inc. announced a definitive merger agreement under which Pfizer plans to acquire Seagen, a leading biotechnology company focused on groundbreaking cancer therapies. This strategic transaction involves a cash payment of USD 229 per Seagen share, culminating in an enterprise value of USD 43 billion. Therefore, the increasing incidence of strategic alliances among market players is boosting the growth of the oncology active pharmaceutical ingredients market.

Type of Drug Insights

The prescription segment led the active pharmaceutical ingredients industry, with a substantial share of 79.48% in 2025. Physicians' recommendations significantly influence the demand for prescription drugs. The use of certain prescription medications, such as Proton Pump Inhibitors (PPIs) for managing heartburn, has leveled off due to various side effects. In contrast, the prescription rates for Histamine-2 Receptor Antagonists (H2RAs) have also been affected. The oncology segment continues to rely heavily on prescription drugs, as cancer treatment predominantly involves chemotherapy, targeted therapies, immunotherapy, and hormonal therapies. Additionally, the use of biologics is on the rise. The effectiveness of new targeted therapies has led to a rapid increase in prescriptions for these treatments, and major companies are actively introducing innovative targeted therapies to the market.

The OTC segment is projected to grow rapidly during the forecast period. These products are readily available to consumers and are susceptible to fluctuations in consumer demand. A growing trend suggests a shift away from antacids for heartburn, with an increasing emphasis on gut health through the use of probiotics. This shift fosters greater opportunities for preventive health products, including supplements, nutraceuticals, and probiotics, while dampening the growth of traditional offerings.

Regional Insights

The active pharmaceutical ingredients market in North America accounted for a 37.66% share in 2025, driven by the increasing prevalence of cardiovascular, genetic, and other chronic diseases, as well as growing research in the field of drug development. The presence of key players such as AbbVie Inc.; Curia; Pfizer Inc. (Pfizer Center One); Viatris Inc.; and Fresenius Kabi AG is positively influencing growth. Furthermore, there is an increasing number of innovators and Contract Development and Manufacturing Organizations (CDMOs) in the area, which improves the ability to develop and commercialize active pharmaceutical ingredients (APIs). For instance, in 2025, ESTEVE acquired CDMO Regis Technologies, increasing its presence and infrastructure in North America for small-molecule API development and manufacture. The above-mentioned drivers are driving the market growth.

U.S. Active Pharmaceutical Ingredients Market Trends

Strong pharmaceutical manufacturing capabilities and increasing demand for both generic and innovative APIs drive the growth of the U.S. active pharmaceutical ingredients industry. The U.S. market benefited from advancements in biotechnology, particularly in the production of monoclonal antibodies, recombinant proteins, and vaccines. Additionally, the rise of chronic diseases, including cancer, cardiovascular conditions, and diabetes, further increased API demand. The U.S. maintained its leadership in the region through a combination of cutting-edge API production, regulatory support, and an expanding biopharmaceutical sector.

Europe Active Pharmaceutical Ingredients Market Trends

The API market in Europe is experiencing significant growth, driven by increasing demand for high-quality APIs across pharmaceutical applications, including both innovative and generic drugs. The region's robust regulatory framework, which emphasizes stringent production standards, has significantly contributed to the market's growth. Furthermore, the rise in chronic diseases such as cardiovascular and oncology-related conditions is fueling API demand. Europe’s leadership in biotechnology has boosted the production of biotech APIs, including monoclonal antibodies, therapeutic enzymes, and vaccines. The growing focus on biosimilars and outsourcing to contract manufacturing organizations (CMOs) is further accelerating market growth.

The UK active pharmaceutical ingredients market is likely to show significant growth due to improvements in healthcare infrastructure and increasing demand for innovative and generic APIs. The rise in chronic diseases, including cardiovascular and oncology-related conditions, is driving API consumption. Nonetheless, advancements in biotechnology and the production of biologics, along with supportive government policies, are further contributing to the market's expansion. The growing focus on biosimilars and contract manufacturing organizations (CMOs) is also expected to boost the market growth.

The active pharmaceutical ingredients market in Germany is experiencing significant growth, driven by strong pharmaceutical manufacturing capabilities and a robust regulatory framework. The increasing demand for both generic and innovative APIs, coupled with advancements in biotechnology, is propelling market expansion. The rise in chronic diseases and the growing focus on biosimilars are further enhancing the market's prospects.

Asia Pacific Active Pharmaceutical Ingredients Market Trends

The active pharmaceutical ingredients industry in the Asia Pacific is anticipated to witness the fastest CAGR of 6.77% over the forecast period, due to sharp growth as the majority of API production occurs in countries present in the region with a high API export rate.China is the largest producer of APIs, manufacturing over 1,600 varieties of chemical APIs. Moreover, several key global players are establishing their operations in the region. Rising investments and initiatives to support and expand manufacturing facilities are further driving the market growth. Aurobindo Pharma opened a new Penicillin-G (Pen-G) facility in Kakinada from April to June 2024, sponsored by the national PLI scheme, with an annual production capacity of 15,000 tons, with the goal of increasing self-sufficiency and decreasing reliance on imports. This expansion in capacity, together with rising investments and good export opportunities, is expected to drive the regional market growth.

The China active pharmaceutical ingredients market is growing at a lucrative rate, driven by the expanding pharmaceutical industry and increasing domestic demand for both generic and innovative APIs. The government's support for healthcare reforms and investments in biotechnology are facilitating this growth. The rising prevalence of chronic diseases and an increasing focus on quality standards in API manufacturing are further propelling the market's expansion, positioning China as a key player in the global API landscape.

The active pharmaceutical ingredients market in India is expected to grow steadily over the forecast period, driven by strong domestic production capabilities, increased export potential, and government efforts to improve pharmaceutical self-sufficiency. India is one of the world's largest producers of generic pharmaceuticals, driving demand for high-quality APIs in a variety of therapeutic areas such as cardiology, anti-infectives, central nervous system, and oncology. Furthermore, increasing investments in modernizing manufacturing facilities, the implementation of continuous processing technologies, and a greater emphasis on high-potency and specialty APIs are all driving market growth. The country's Production-Linked Incentive (PLI) initiatives and particular API parks continue to attract national and international investment, boosting supply-chain resilience. For instance, in 2024, Granules India announced a significant expansion of its API production capacity in Andhra Pradesh to meet the increased global demand for paracetamol and other key pharmaceutical ingredients.

Latin America Active Pharmaceutical Ingredients Market Trends

The API industry in Latin America is experiencing significant progress, driven by rising healthcare investments and increasing demand for both generic and innovative APIs. The growing prevalence of chronic diseases and supportive regulatory environments is enhancing market growth, positioning the region as a developing hub for pharmaceutical production and development. Improvements in industrial infrastructure, along with a surge in clinical research activities, are creating new opportunities for both local and foreign businesses. Furthermore, strategic alliances and technological transfers are enhancing the region's capabilities in the synthesis of complex compounds. The use of modern production methods and quality standards improves the competitiveness of indigenous producers.

The Brazil Active pharmaceutical ingredients market is expected to grow over the forecast period. The Brazilian government has been keen on launching initiatives to improve healthcare infrastructure and increase access to diagnostic services, particularly in rural areas. Furthermore, there the both global and local players. The market still faces challenges such as the need for more accurate and reliable diagnostic tests, the high cost of treatment, and the lack of access to healthcare services in some regions. In addition, increased expenditures on cutting-edge manufacturing facilities, process innovations, and adherence to global regulatory standards are enhancing production efficiency and reliability. Nonetheless, the market faces challenges, including high treatment costs, disparities in healthcare access across countries, and a growing demand for more complex and reliable diagnostic and therapeutic solutions, all of which continue to impact market dynamics and expansion.

Middle East and Africa Active Pharmaceutical Ingredients Market Trends

The active pharmaceutical ingredients industry in the Middle East and Africa is experiencing growth driven by rising healthcare investments and an increasing focus on improving healthcare infrastructure. The demand for both generic and innovative APIs is on the rise due to the growing prevalence of chronic diseases in the region. Moreover, supportive regulatory frameworks and collaborations with global pharmaceutical companies are enhancing the market's potential, making MEA a significant player in the global API landscape as it seeks to boost local production capabilities.

The Saudi Arabia active pharmaceutical ingredients market is driven by significant government initiatives aimed at enhancing the local pharmaceutical industry. Investments in healthcare infrastructure and a focus on reducing dependence on imports are fostering a favorable environment for API production. The increasing prevalence of chronic diseases and the demand for both generic and innovative APIs are further contributing to market expansion, positioning Saudi Arabia as a key player in the MEA API landscape.

Key Active Pharmaceutical Ingredients Company Insights

The competitive scenario in the API market is characterized by the presence of several key players, including large multinational pharmaceutical companies and specialized API manufacturers. These companies are focusing on innovation, quality assurance, and regulatory compliance to gain a competitive edge. Collaborations, mergers, and acquisitions are common strategies to enhance market share and expand product portfolios. In addition, the rise of biotechnology firms is intensifying competition, particularly in the biotech API segment.

Regional players are also emerging, leveraging cost advantages and localized production to compete effectively. Overall, the market is dynamic, with ongoing advancements and shifting player strategies shaping the competitive landscape. The presence of pipeline products in the API market is expected to launch in the coming years and is anticipated to drive market growth. A blockbuster drug patent expiration, increasing outsourcing activities due to high manufacturing costs, and stringent regulations on the production of APIs are expected to maintain the competitive rivalry at a high level during the forecast period. Some of the key players in the global active pharmaceutical ingredients market include:

-

In May 2025, the two firms merged under the name Cohance to develop a more powerful and integrated CDMO/API company that combines Suven's commercial manufacturing capabilities with Cohance's specialist platforms, including antibody-drug conjugates and complex chemistry.

-

In January 2025, AGC Pharma Chemicals announced plans to significantly improve its high-potency API (HPAPI) capabilities at its Barcelona facility, investing more than $110 million in containment systems, R&D laboratories, QC laboratories, and the establishment of a new manufacturing plant capable of producing OEB5-level HPAPI, fueling the growth of the high-potency active pharmaceutical ingredients market.

-

In May 2024, Eli Lilly made a significant investment in its Lebanon, Indiana, manufacturing site, increasing its total investment to USD 9 billion. This expansion aims to increase the production of active pharmaceutical ingredients (APIs) for tirzepatide, the active ingredient in their drugs Zepbound and Mounjaro, which are used to treat obesity and type 2 diabetes.

-

In April 2023, Eli Lilly announced an additional USD 1.6 billion investment in two new manufacturing plants in Indiana, raising its total commitment to USD 3.7 billion. This investment supports the production of its cancer drug, Jaypirca, and aims to enhance capacity for treating obesity, Alzheimer's disease, and autoimmune diseases. Over the past three years, Lilly has invested USD 6.4 billion in U.S. manufacturing expansion.

-

In January 2023, Sterling Pharma Solutions completed its acquisition of an active pharmaceutical ingredient (API) manufacturing facility in Ringaskiddy, Ireland, from Novartis, initially announced in March 2022. The facility enhances Sterling's API manufacturing capacity and includes an ongoing supply agreement with Novartis for APIs used in cardiovascular, immunology, and oncology applications. The site features multiple production buildings and extensive capabilities for handling potent APIs. This acquisition aligns with Sterling's growth strategy, expanding its workforce to 1,300 employees across five global facilities.

Key Active Pharmaceutical Ingredients Companies:

The following are the leading companies in the active pharmaceutical ingredients market. These companies collectively hold the largest Market share and dictate industry trends.

- Dr. Reddy’s Laboratories Ltd.

- Sun Pharmaceutical Industries Ltd.

- Teva Pharmaceutical Industries Ltd.

- Cipla Inc.

- AbbVie Inc.

- Aurobindo Pharma

- Sandoz International GmbH (Novartis AG)

- Viatris Inc.

- Fresenius Kabi AG

- STADA Arzneimittel AG

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Teva Pharmaceutical Industries Ltd

- Mature API manufacturers focus on expanding global manufacturing capacity, strengthening backward integration, securing regulatory approvals, and maintaining long-term pharmaceutical partnerships.

- They also invest in complex APIs, high-potency APIs, and process innovation to sustain market leadership and improve operational efficiency globally.

- Mature players maintain competitive advantage through diversified API portfolios, strong global distribution networks, vertically integrated operations, and established regulatory compliance capabilities.

- Their large-scale manufacturing infrastructure, financial strength, and long-standing pharmaceutical partnerships help sustain dominant positioning within the highly competitive global API market.

- Mature API manufacturers face challenges including high operational expenses, strict environmental and regulatory compliance requirements, and pricing pressure from generic pharmaceutical markets.

- Large organizational structures may also reduce flexibility, increase production costs, and slow responses to rapidly evolving market and supply chain conditions.

Emerging Players: Aurobindo Pharma

- Emerging API manufacturers prioritize cost-efficient production, expansion into regulated markets, and increasing exports of specialty and generic APIs.

- They also emphasize strategic collaborations, process optimization, and capacity expansion initiatives to strengthen competitiveness and accelerate growth across global pharmaceutical markets.

- Emerging players gain competitive advantage through lower manufacturing costs, operational flexibility, and rapid expansion into high-growth therapeutic segments.

- Their ability to quickly scale production, optimize manufacturing processes, and strengthen penetration in regulated pharmaceutical markets supports increasing competitiveness within the global API industry.

- Emerging API manufacturers often face limitations including lower brand recognition, dependence on export-driven revenues, and comparatively smaller research and development capabilities.

- They may also experience difficulties in scaling complex API manufacturing, obtaining global regulatory approvals, and competing against financially stronger multinational pharmaceutical companies.

Active Pharmaceutical Ingredients Market Report Scope

Report Attribute

Details

Market size in 2025

USD 270.5 billion

Estimated market size in 2026

USD 287.1 billion

Projected market size by 2033

USD 419.0 billion

Growth rate

CAGR of 5.6% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2023

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type of synthesis, type of manufacturer, type, application, type of drug, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; UK; Germany; Spain; France; Italy; Russia; Hungary; Russia; Poland; Hungary; Sweden; Switzerland; Portugal; Greece; Japan; China; India; South Korea; Australia; Thailand; Vietnam; Indonesia; Malaysia; Taiwan; Philippines; Brazil; Mexico; Colombia; Peru; Chile; South Africa; Saudi Arabia; UAE; Kuwait; Egypt; Israel; Belarus; Algeria; Jordan; Iran

Key companies profiled

Dr. Reddy’s Laboratories Ltd.; Sun Pharmaceutical Industries Ltd.; Teva Pharmaceutical Industries Ltd.; Cipla Inc.; AbbVie Inc.; Aurobindo Pharma; Sandoz International GmbH (Novartis AG); Viatris Inc.; Fresenius Kabi AG; STADA Arzneimittel AG

Customization scope

Free report customization (equivalent to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Global Active Pharmaceutical Ingredients Market Report Segmentation

This report forecasts revenue growth and provides an analysis on the latest trends in each of the sub-segments from 2021 to 2033. For this report, Grand View Research has segmented the active pharmaceutical ingredients market report based on type of synthesis, type of manufacturer, type, application, type of drug, and region:

-

Type of Synthesis Outlook (Revenue, USD Million, 2021 - 2033)

-

Biotech

-

Biotech APIs, By Type

-

Generic APIs

-

Innovative APIs

-

-

Biotech APIs, By Product

-

Monoclonal Antibodies

-

Hormones

-

Cytokines

-

Recombinant Proteins

-

Therapeutic Enzymes

-

Vaccines

-

Blood Factors

-

-

-

Synthetic

-

Synthetic APIs, By Type

-

Generic APIs

-

Innovative APIs

-

-

-

-

Type of Manufacturer Outlook (Revenue, USD Million, 2021 - 2033)

-

Captive APIs

-

Merchant APIs

-

Merchant APIs, By Type of Synthesis

-

Generic APIs

-

Innovative APIs

-

-

Merchant APIs, By Type

-

Biotech

-

Synthetic

-

-

-

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Generic APIs

-

Innovative APIs

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Cardiology

-

Oncology

-

CNS and Neurology

-

Orthopedic

-

Endocrinology

-

Pulmonology

-

Gastroenterology

-

Nephrology

-

Ophthalmology

-

Others

-

-

Type of Drugs Outlook (Revenue, USD Million, 2021 - 2033)

-

Prescription

-

OTC

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

-

Europe

-

UK

-

Germany

-

Spain

-

France

-

Italy

-

Russia

-

Hungary

-

Russia

-

Poland

-

Hungary

-

Sweden

-

Switzerland

-

Portugal

-

Greece

-

Rest of Europe

-

-

Asia Pacific

-

Japan

-

China

-

India

-

South Korea

-

Australia

-

Thailand

-

Vietnam

-

Indonesia

-

Malaysia

-

Taiwan

-

Philippines

-

Rest of APAC

-

-

Latin America

-

Brazil

-

Mexico

-

Colombia

-

Peru

-

Chile

-

Rest of LATAM

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

Egypt

-

Israel

-

Belarus

-

Algeria

-

Jordan

-

Iran

-

Rest of MEA

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Generic API Supply Chain & Sourcing Assessment (U.S. & Europe)

Conducted a targeted assessment of generic API sourcing trends across the U.S., Germany, France, Italy, Spain, and the UK. The study evaluated supplier concentration, import dependency, regulatory compliance risks, pricing benchmarks, and API manufacturing capabilities for cardiovascular, oncology, and anti-infective therapeutic categories.

Helped the client identify reliable API sourcing regions, optimize procurement strategy, reduce supply chain risks, and strengthen long-term partnerships with compliant API manufacturers across regulated pharmaceutical markets.

High-Potency API (HPAPI) Manufacturing Benchmarking Study

Delivered a comprehensive benchmarking analysis of HPAPI manufacturers focusing on oncology and specialty pharmaceutical applications. The assessment covered containment technologies, manufacturing scalability, regulatory certifications, production capacities, and investment trends across leading global API manufacturing companies and emerging contract development organizations.

Enabled the client to evaluate expansion opportunities in specialty APIs, identify strategic manufacturing partners, benchmark competitive positioning, and prioritize investments in high-growth oncology and advanced therapeutic API segments.

API Manufacturing Expansion Feasibility Study for Asia-Pacific

Conducted a country-level feasibility assessment for API manufacturing expansion across India, China, Singapore, and South Korea. The study analyzed labor costs, regulatory frameworks, infrastructure readiness, environmental compliance requirements, raw material availability, and export competitiveness for pharmaceutical API production facilities.

Supported strategic investment planning by identifying cost-efficient manufacturing hubs, improving regional supply chain resilience, reducing dependency on single-country sourcing, and strengthening long-term API production and export capabilities across global pharmaceutical markets.

Frequently Asked Questions About This Report

The global active pharmaceutical ingredients market size was valued at USD 270.5 billion in 2025 and is estimated at USD 287.1 billion for 2026.

Key players in the global API market are Merck & Co., Inc.; AbbVie Inc.; Teva Pharmaceutical Industries Ltd.; Viatris Inc.; Cipla Inc.; Boehringer Ingelheim International GmbH; Merck & Co., Inc.; Sun Pharmaceutical Industries Ltd.; Bristol-Myers Squibb Company; Albemarle Corporation and Aurobindo Pharma.

Asia Pacific is the fastest-growing region over the forecast period.

The synthetic segment led with a 70.9% revenue share in 2025, while the biotech API segment is the fastest-growing.

The captive APIs segment led with a 50.6% revenue share in 2025, while the merchant APIs segment is the fastest-growing.

The innovative APIs segment led with a 53.8% revenue share in 2025, while the generic APIs segment is the fastest-growing.

Cardiology segment held the largest share (over 20.0%) in 2025, while the oncology segment is the fastest-growing.

The global active pharmaceutical ingredients market is expected to grow at a CAGR of 5.6% from 2026 to 2033, reaching USD 419.0 billion by 2033.

North America dominated with a 37.7% revenue share in 2025.

The active pharmaceutical ingredients market growth can be attributed to the advancements in active pharmaceutical ingredient (API) manufacturing and the rising prevalence of chronic diseases, such as cardiovascular diseases and cancer. Favorable government policies for API production along with changes in geopolitical situations are boosting the market growth.

About the Author(s)

Pharmaceuticals Research Team

Healthcare · PharmaceuticalsThis report was authored by the pharmaceuticals research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the pharmaceuticals segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.