- Home

- »

- Advanced Interior Materials

- »

-

Advanced Ceramics Market Size, Share Report, 2026-2033GVR Report cover

![Advanced Ceramics Market (2026 - 2033)Report]()

Advanced Ceramics Market (2026 - 2033)

Size, Share & Trends Analysis Report, By Material (Alumina, Titanate, Zirconate, Ferrite, Aluminum Nitride, Silicon Carbide, Silicon Nitride), By Product (Monolithic, CMCs), By End Use, By Region, And Segment Forecasts

Market Size, 2025

$119.4BMarket Estimate, 2026

$124.1BMarket Forecast, 2033

$159.3BCAGR, 2026–2033

3.6%Advanced Ceramics Market Summary

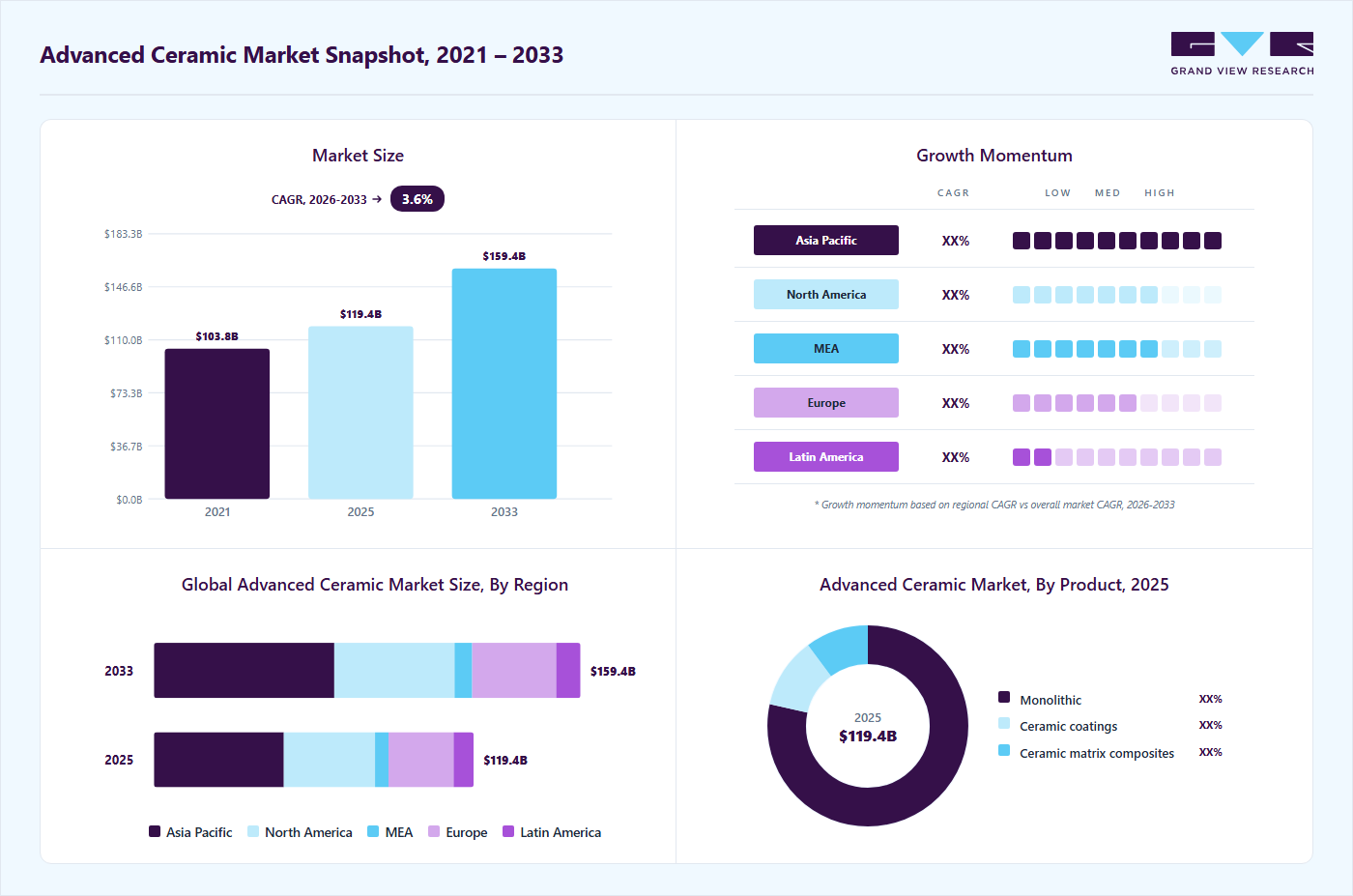

The global advanced ceramics market size was valued at USD 119.4 billion in 2025 and is projected to grow from USD 124.1 billion in 2026 to USD 159.3 billion by 2033, at a CAGR of 3.6% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 40.6% in 2025. Market growth is primarily driven by the increasing adoption of advanced ceramics across a wide range of applications, supported by rising demand from the medical and telecommunications industries.

Key Market Trends & Insights

- By material: Titanate segment is anticipated to register at the fastest CAGR of 4.2% from 2026 to 2033.

- By product: Monolithic segment led the market with the largest market revenue share of 78.0% in 2025.

- By end use: Electrical & electronics segment led the market with the largest revenue share of 56.7% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (40.6% revenue share, 2025)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 119.4 billion

- Estimated market size in 2026: USD 124.1 billion

- Projected market size by 2033: USD 159.3 billion

- CAGR (2026-2033): 3.6%

The superior mechanical, thermal, and electrical properties of advanced ceramics continue to expand their penetration into high-performance, technology-intensive end uses, thereby supporting sustained market expansion over the forecast horizon.Advanced ceramics, also referred to as technical ceramics, exhibit superior magnetic, optical, thermal, and electrical properties compared to conventional ceramics. These performance advantages enable end users to enhance product efficiency while simultaneously reducing production and energy costs. As a result, advanced ceramics have gained significant traction in high-performance, technology-driven applications. Asia Pacific is the largest regional market for advanced ceramics globally, with the highest consumption levels, supported by strong manufacturing activity, rapid industrialization, and expanding electronics, automotive, and healthcare sectors.

")

Advanced ceramics, also known as technical ceramics, offer enhanced magnetic, optical, thermal, and electrical properties compared to conventional ceramics, enabling improved performance across a wide range of applications. Their ability to increase product efficiency while lowering production and energy costs has driven strong adoption among end users. Asia Pacific dominates the global advanced ceramics industry in terms of consumption, supported by robust manufacturing activity, rapid industrialization, and growing demand from key end-use industries such as electronics, automotive, and healthcare.

Drivers, Opportunities & Restraints

The advanced ceramics market continues to be propelled by robust demand for high-performance materials across critical industries. In 2025, strong innovation in semiconductor and automotive components has driven market growth, with companies such as Kyocera showcasing advanced ceramic solutions for semiconductors, fine ceramics, and automotive applications at The Advanced Ceramics Show 2025 in Birmingham, UK, targeting next-generation sensors, actuators, and piezoelectric elements for automotive and electronics markets. Additionally, adoption in medical technology is expanding, with companies presenting advanced ceramics at compared 2025, where high-performance ceramic materials are being applied in diagnostics, surgical instruments, and implant components, illustrating their critical role in improving reliability and device performance. The increasing prevalence of ceramic materials in electronic substrates, thermal management systems, and EV components further drives demand as industries pursue weight reduction, efficiency, and enhanced thermal and electrical performance.

Significant opportunities emerge from innovation, collaboration, and expanded application domains. In 2025, the 2nd Semiconductor Ceramic Materials Technology Symposium, hosted by Shenyang Starlight Technical Ceramics, highlighted breakthroughs in high-performance carbide (SiC) materials for semiconductor and power-electronics applications, underscoring the strategic importance of ceramics in advanced electronics and EV power systems. Moreover, the ongoing China International Advanced Ceramics Expo 2025 provided a platform for companies worldwide to unveil new ceramic materials and manufacturing technologies for applications across communications, aerospace, and automotive sectors, reinforcing the role of ceramics in industrial innovation. The rising adoption of additive manufacturing and 3D printing tailored to ceramic powders and parts also presents opportunities to penetrate high-precision, customizable applications in the aerospace, medical, and energy sectors.

Despite these opportunities, the market faces persistent challenges. Advanced ceramics often require complex and energy-intensive manufacturing processes and specialized sintering technologies, which contribute to higher production costs and can impede scalability. Supply chain constraints for high-purity raw materials, including high-grade alumina, zirconia, and silicon carbide, continue to impact cost structures and delivery timelines. Although innovation in production and materials processing is ongoing, these factors remain constraints to broader adoption in lower-cost, high-volume markets.

Material Insights

The alumina segment led the market with the largest revenue share of 33.9% in 2025, owing to its wide-ranging applicability, cost-effectiveness, and favorable mechanical and thermal properties. High hardness, excellent wear resistance, electrical insulation, and thermal stability have established alumina as a preferred material across electrical & electronics, automotive, medical, and industrial applications. Its well-established manufacturing ecosystem and availability in various grades further support its dominant market position.

The titanate segment is expected to register at the fastest CAGR of 4.2% over the forecast period, driven by its expanding use in advanced electronic and energy-related applications. Titanate-based ceramics offer excellent dielectric, piezoelectric, and ferroelectric properties, making them highly suitable for capacitors, sensors, actuators, and energy storage systems. Rising demand for miniaturized electronic components, electric vehicles, and advanced communication infrastructure is accelerating the adoption of titanate ceramics, particularly in high-performance and precision-driven applications.

Product Insights

The monolithic ceramics segment led the market with the largest revenue share of 78.3% in 2025, driven by their extensive use in mature, high-volume applications. These ceramics offer excellent hardness, wear resistance, and chemical stability, making them suitable for electronic components, medical devices, cutting tools, and industrial machinery. Their relatively lower production costs and established manufacturing processes, compared with composites, continue to drive widespread adoption, reinforcing their leading position in revenue.

The ceramic matrix composites segment is expected to register at the fastest CAGR of 4.6% during the forecast period, driven by their superior strength-to-weight ratio, fracture toughness, and thermal stability compared to monolithic ceramics. CMCs are increasingly adopted in aerospace, defense, automotive, and energy applications where high-temperature performance and lightweight materials are critical. The growing demand for fuel-efficient aircraft, hypersonic vehicles, and advanced propulsion systems is accelerating the adoption of CMCs in high-value applications.

End Use Insights

The electrical & electronics segment led the market with the largest revenue share of 56.7% in 2025, driven by strong demand for high-performance substrates, insulators, and dielectric components. Advanced ceramics play a critical role in thermal management, electrical insulation, and the miniaturization of electronic devices. Continuous growth in consumer electronics, semiconductor manufacturing, telecommunications infrastructure, and power electronics, particularly for EVs and renewable energy systems, continues to underpin this segment’s revenue dominance.

The environmental segment is projected to witness at the fastest CAGR of 4.4% during the forecast period, supported by growing investments in emission control, water treatment, and sustainable industrial processes. Advanced ceramics are increasingly used in filtration membranes, catalytic substrates, and pollution control systems due to their chemical inertness, high-temperature resistance, and long operational life. Stricter environmental regulations and the global push toward sustainability are further accelerating demand for ceramic-based environmental solutions.

Regional Insights

The advanced ceramics market in North America is mature and technologically advanced, supported by strong demand from the aerospace, defense, electronics, healthcare, and energy sectors. The region also plays a significant role in the advanced ceramics market and the aerospace advanced ceramics market, driven by high-performance requirements in aircraft components, defense systems, and precision medical and electronic applications. The region benefits from a well-established manufacturing base, continuous R&D investments, and the presence of leading advanced ceramics producers and end users. Increasing adoption of advanced ceramics in electric vehicles, semiconductor manufacturing equipment, and medical devices, along with ongoing innovation in ceramic matrix composites and electronic ceramics, continues to support steady market growth across the region.

U.S. Advanced Ceramics Market Trends

The U.S. advanced ceramics market accounted for the largest share of revenue in North America in 2025, driven by high demand from the electrical & electronics, defense, aerospace, and medical industries. Growth is further supported by increasing production of electric vehicles, expansion of semiconductor fabrication facilities, and rising investments in advanced manufacturing technologies. Strong government and private-sector funding for defense and healthcare innovation, combined with the presence of major advanced ceramics manufacturers, underpins the country’s dominant position.

Europe Advanced Ceramics Market Trends

The advanced ceramics market in Europe is a key region, characterized by strong demand across automotive, industrial, medical, and renewable energy applications. Countries such as Germany, France, and the UK are at the forefront of ceramic innovation, supported by stringent environmental regulations, a strong focus on energy efficiency, and advanced engineering capabilities. The region’s emphasis on lightweight materials, electrification of mobility, and high-performance industrial components continues to drive adoption of advanced ceramics.

Asia Pacific Advanced Ceramics Market Trends

Asia Pacific dominates the global advanced ceramics market with the largest revenue share of 40.6% in 2025 and is anticipated to grow at the fastest CAGR of 4.2% during the forecast period, supported by rapid industrialization, large-scale electronics manufacturing, and expanding automotive and healthcare sectors.

The India advanced ceramics market and Japan advanced ceramics market are key growth engines within the region, alongside China and South Korea, benefiting from strong demand for electronic components, semiconductor substrates, and advanced materials for EVs and renewable energy systems. The presence of a robust manufacturing ecosystem, cost advantages, and growing investments in advanced material technologies further strengthen the region’s leadership position.

Latin America Advanced Ceramics Market Trends

The advanced ceramics market in Latin America is emerging, driven primarily by expanding industrial activity, automotive production, and the development of healthcare infrastructure. Countries such as Brazil and Mexico are witnessing increasing adoption of advanced ceramic components in manufacturing and energy-related applications. While market penetration remains lower than in developed regions, rising investments in industrial modernization and the gradual adoption of advanced materials are expected to support steady growth.

Middle East & Africa Advanced Ceramics Market Trends

The advanced ceramics market in the Middle East & Africa is at a nascent stage but is gradually gaining traction, supported by infrastructure development, energy diversification initiatives, and growing healthcare investments. Advanced ceramics are increasingly being adopted in industrial equipment, medical devices, and energy-related applications, particularly in Gulf countries. Government-led initiatives aimed at economic diversification and industrial development are expected to create long-term growth opportunities for advanced ceramics across the region.

Key Advanced Ceramics Company Insights

Some of the key players operating in the market include KYOCERA Corporation, CoorsTek Inc., and others

-

KYOCERA Corporation, established in 1959, is a leading global manufacturer of advanced ceramics and fine ceramic components, with a strong presence across the Asia Pacific, North America, and Europe. The company offers a broad portfolio of ceramic solutions for electronics, automotive, semiconductor, medical, and industrial applications, including substrates, packages, insulators, cutting tools, and structural ceramic components. KYOCERA is recognized for its continuous innovation in fine ceramics and for integrating material science expertise with high-precision manufacturing to support next-generation electronic and mobility applications.

-

CoorsTek Inc., founded in 1910, is a global leader in engineered ceramics, serving customers across North America, Europe, and Asia. The company provides a comprehensive range of advanced ceramic materials, including alumina, silicon carbide, silicon nitride, and zirconia, used in semiconductor manufacturing, aerospace, automotive, medical devices, and energy systems. CoorsTek is known for its vertically integrated manufacturing capabilities and material innovation, enabling high-performance ceramic components for demanding thermal, electrical, and wear-intensive environments.

-

CeramTec GmbH, established in 1903, is a prominent supplier of advanced ceramic solutions with a strong footprint in Europe, North America, and Asia. The company specializes in technical ceramics for applications in electronics, medical engineering, automotive systems, and industrial machinery. CeramTec’s product portfolio includes ceramic substrates, bio ceramics, wear-resistant components, and electronic ceramic parts. The company is widely recognized for its expertise in medical ceramics and its focus on precision engineering, quality, and long-term reliability in high-performance applications.

Key Advanced Ceramics Companies:

The following key companies have been profiled for this study on the advanced ceramics market

- 3M

- AGC Ceramics Co., Ltd.

- CeramTec GmbH

- CoorsTek Inc.

- Elan Technology

- KYOCERA Corporation

- Morgan Advanced Materials

- Murata Manufacturing Co., Ltd.

- Nishimura Advanced Ceramics Co., Ltd.

- Ortech Advanced Ceramics

- Saint-Gobain

Recent Development

-

In March 2025, KYOCERA Corporation announced the expansion of its fine ceramics manufacturing facility in Kagoshima, Japan, as disclosed through publicly available company communications. The expansion is intended to increase production capacity for advanced ceramic substrates and components used in semiconductor manufacturing, EV power electronics, and telecommunications infrastructure, in response to rising global demand.

-

In April 2025, CoorsTek Inc. publicly announced the launch of a new range of ceramic matrix composites (CMCs) designed for high-temperature aerospace and industrial energy applications. According to company disclosures, the newly introduced materials offer enhanced thermal resistance and mechanical durability, enabling improved performance and longer service life in extreme operating environments.

-

In June 2025, CeramTec GmbH announced the commercialization of a new advanced bioceramics platform, as reported in its official press releases. The development focuses on next-generation alumina- and zirconia-based ceramic materials for orthopedic and dental implants, aiming to improve biocompatibility, wear resistance, and long-term clinical performance.

Advanced Ceramics Market Report Scope

Report Attribute

Details

Market size in 2025

USD 119.4 billion

Estimated market size in 2026

USD 124.1 billion

Projected market size by 2033

USD 159.3 billion

Growth rate

CAGR of 3.6% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Material, product, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; China; India; Japan; Brazil; Argentina; Saudi Arabia; UAE; Egypt

Key companies profiled

3M; AGC Ceramics Co., Ltd.; CeramTec GmbH; CoorsTek Inc.; Elan Technology; KYOCERA Corporation; Morgan Advanced Materials; Murata Manufacturing Co., Ltd.; Nishimura Advanced Ceramics Co., Ltd.; Ortech Advanced Ceramics; Saint-Gobain

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Advanced Ceramics Market Report Segmentation

This report forecasts revenue growth at the country & regional levels and provides an analysis of the industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global advanced ceramics market report based on the material, product, end use, and region.

-

Material Outlook (Revenue, USD Million, 2021-2033)

-

Alumina

-

Titanate

-

Zirconate

-

Ferrite

-

Aluminum Nitride

-

Silicon Carbide

-

Silicon Nitride

-

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Monolithic

-

Ceramic Coatings

-

Ceramic Matrix Composites (CMCs)

-

Others

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Electric & Electronics

-

Automotive

-

Machinery

-

Environmental

-

Medical

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

-

Asia Pacific

-

China

-

India

-

Japan

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

Egypt

-

-

Frequently Asked Questions About This Report

The global advanced ceramics market size was estimated at USD 119.4 billion in 2025 and is expected to reach USD 124.1 billion in 2026.

Some of the key players operating in the advanced ceramics market are 3M; AGC Ceramics Co., Ltd.; CeramTec GmbH; CoorsTek Inc.; Elan Technology; KYOCERA Corporation; Morgan Advanced Materials; Murata Manufacturing Co., Ltd.; Nishimura Advanced Ceramics Co., Ltd.; Ortech Advanced Ceramics, among others.

The global advanced ceramics market is driven by growing demand for high-performance, lightweight, and durable materials across electronics, automotive, aerospace, and healthcare sectors. Rapid adoption in electric vehicles, semiconductors, and bioceramics for medical implants further boosts growth. Technological advancements like ceramic matrix composites and 3D printing also support market expansion.

The market in Asia Pacific dominated with a revenue share of 40.6% in 2025.

The alumina segment led the market with the largest revenue share of 33.9% in 2025, owing to its wide-ranging applicability, cost-effectiveness, and favorable mechanical and thermal properties.

The global advanced ceramics market is expected to grow at a compound annual growth rate of 3.6% from 2026 to 2033 to reach USD 159.3 billion by 2033.

Monolithic accounted for the largest market revenue share of over 78.0% in 2025.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.