- Home

- »

- Medical Devices

- »

-

Aesthetic Injectable Market Size & Share Report, 2026-2033GVR Report cover

![Aesthetic Injectable Market (2026 - 2033)Report]()

Aesthetic Injectable Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Collagen & PMMA Microspheres, Hyaluronic Acid, PLLA), By Application (Wrinkle Correction, Lip Augmentation), By End-use (MedSpas, Aesthetic Surgery Centers), By Region, And Segment Forecasts

Market Size, 2025

$11.1BMarket Estimate, 2026

$12.3BMarket Forecast, 2033

$24.1BCAGR, 2026–2033

10.0%Aesthetic Injectable Market Summary

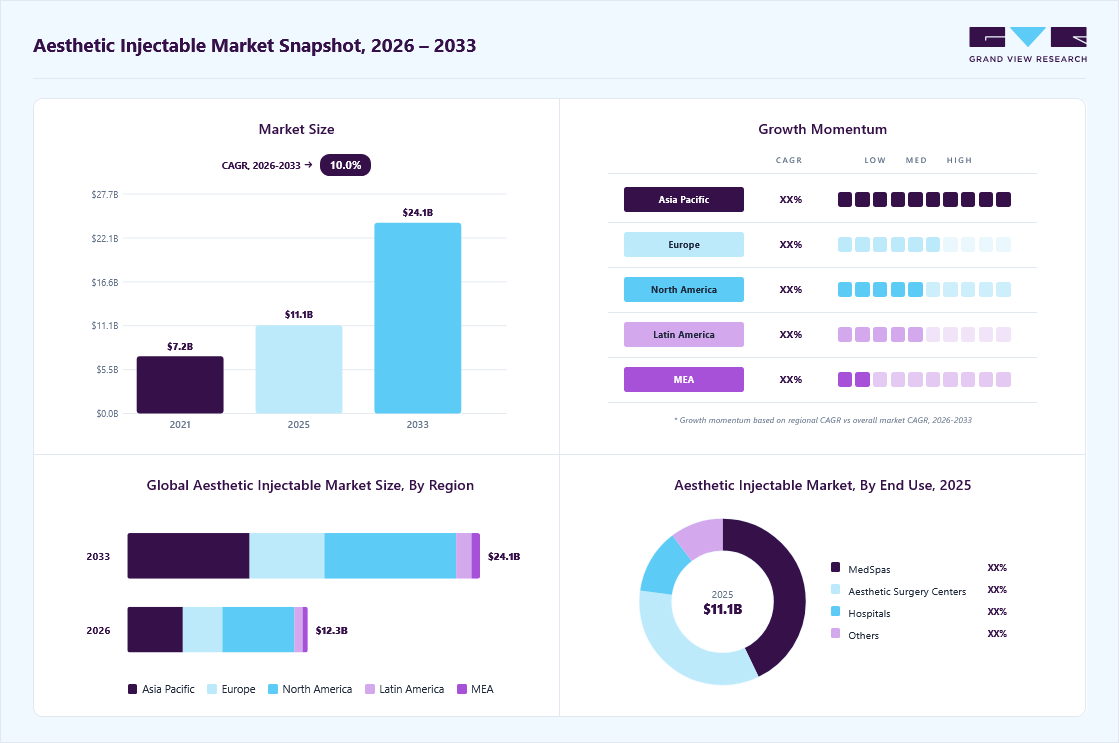

The global aesthetic injectable market size was valued at USD 11.1 billion in 2025 and is projected to grow from USD 12.3 billion in 2026 to USD 24.1 billion by 2033, at a CAGR of 10.0% from 2026 to 2033. The market in North America dominated with a revenue share of 40.1% in 2025. The rising demand for minimally invasive aesthetic procedures is significantly driving the growth of the aesthetic injectables industry.

Key Market Trends & Insights

- By product: Botulinum toxin (botox) segment held the largest market share of 44.5% in 2025.

- By end use: MedSpas segment held the largest market share of 42.8% in 2025.

- By application: Wrinkle correction segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (40.1% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 11.1 Billion

- Estimated market size in 2026: USD 12.3 Billion

- Projected market size by 2033: USD 24.1 Billion

- CAGR (2026-2033): 10.0%

Consumers are increasingly seeking subtle, non-surgical enhancements with minimal downtime, boosting the adoption of products such as botulinum toxins, dermal fillers, and biostimulatory injectables. These treatments effectively address concerns such as wrinkles, volume loss, and skin quality, delivering natural-looking results from immediate to gradual effects. This shift has expanded the consumer base to include both corrective and preventive users. In June 2024, an article published in the European Journal of Plastic Surgery analyzed 511 websites across Germany, Austria, and Switzerland, highlighting the strong presence and demand for non-surgical aesthetic procedures, reinforcing their growing role in modern clinical practice.")

The social acceptance of injectable treatments has also expanded the customer base beyond traditional segments. Younger consumers view dermal fillers as a proactive approach to aging, while older individuals appreciate the restoration of youthful features without going under the knife. With influencers and professionals normalizing these treatments, demand continues to grow in both urban and emerging markets. Patients value the ability to personalize results progressively and affordably. The rise of curated aesthetic journeys, guided by skilled practitioners, reinforces confidence in these procedures. In January 2024, Allergan Aesthetics revealed that its Allē loyalty rewards program achieved a 92% satisfaction rate in a consumer survey. Serving over six million members, Allē offers benefits such as cost savings, points on non-Allē treatments, and exclusive rewards for loyal users, making it a trusted resource for consumers and providers alike.

The following table highlights the rising volume and distribution of non-surgical aesthetic procedures across these regions, emphasizing injectables and facial rejuvenation as leading growth segments.

Non-Surgical Procedures by Category and Country:

Category

U.S.

Mexico

Japan

Germany

Total Non-Surgical Procedures

4,165,645

560,865

1,251,600

677,313

Injectables

3,183,878

421,893

787,600

610,885

Facial Rejuvenation

627,772

70,083

286,800

53,565

Other (Hair, Fat, Tattoo Removal)

353,995

68,889

177,200

12,863

The expanding aging population is another major driver of the aesthetic injectables market, as individuals increasingly seek non-surgical solutions to address visible signs of aging. Aesthetic injectables, including botulinum toxins, dermal fillers, and biostimulatory agents, help reduce wrinkles, restore facial volume, and improve skin quality through minimally invasive procedures. Their ability to deliver natural-looking results with limited downtime makes them highly appealing to older adults. For instance, in the U.S., the population aged 65 and above is projected to grow significantly by 2060, supporting sustained demand for such treatments.

Furthermore, signs of aging, including wrinkles and sagging of the skin due to low facial elasticity, and dark spots start appearing between 25 & 30 years of age and become more prominent from 30 to 65 years of age. Thus, the presence of a large population susceptible to various signs of aging boosts the demand for aesthetic injectables globally. Simultaneously, awareness and training initiatives are gaining importance amid the booming demand for non-surgical aesthetic procedures, which surged 57.8% globally between 2018 and 2022, reaching 18.8 million procedures. In the U.S. alone, over 4.5 million soft-tissue filler and neuromodulator procedures were performed in 2022, reflecting a 13-24% year-over-year growth.

As procedures become more complex, the importance of standardized training and certification has grown substantially. Companies such as Sinclair Pharma have introduced structured educational programs since March 2022, focusing on advanced injection techniques, facial anatomy, and complication management. These initiatives aim to reduce variability in outcomes, improve safety profiles, and ensure adherence to best practices. Enhanced practitioner expertise is critical in delivering high-quality results, particularly in the context of the “undetectable” aesthetics trend, where precision and subtlety are paramount.

Market Concentration & Characteristics:

The aesthetic injectables market is moderately concentrated, with leading companies such as AbbVie (Allergan Aesthetics), Galderma, Merz Pharma, Medytox, Inc., and Sinclair Pharma holding significant shares of the market. These players offer a wide range of injectable solutions, including botulinum toxin (neuromodulators) and dermal fillers, which are widely used for wrinkle reduction, facial contouring, volume restoration, and lip enhancement. Their strong product portfolios, established brand presence, and continuous innovation enable improved treatment outcomes, including natural-looking results, enhanced collagen stimulation, and longer-lasting effects.

The aesthetic injectable industry is witnessing significant innovation and technological advancements, particularly in cross-linking technologies and biodegradable compositions. A major milestone in market evolution occurred in March 2026, when Allergan Aesthetics introduced the concept of the “undetectable era” at the Aesthetic & Anti-Aging Medicine World Congress (AMWC) 2026. This paradigm shift reflects a growing preference for subtle, natural-looking enhancements rather than dramatic transformations. Data presented at the event, based on global consumer insights, indicated that over 70-80% of patients prefer results that are not visibly noticeable. The company’s JUVÉDERM portfolio exemplifies this trend by offering versatile HA injectables that support personalized, discreet outcomes aligned with individual facial anatomy and aging patterns.

Partnerships and collaborations play a crucial role in the aesthetic injectable market, enabling companies to accelerate research, enhance product development, and expand clinical adoption of regenerative skincare solutions. For instance, in August 2024, Alma announced a collaboration with Prollenium to exclusively distribute Revanesse dermal fillers and SoftFil cannulas in the UK. Alma will provide comprehensive training and support through Harley Academy and Alma Studios. This partnership aims to combine advanced injectables with energy-based technologies to enhance patient outcomes and clinic success.

Regulatory oversight plays a critical role in shaping the market by ensuring product safety, quality, and clinical validity before commercialization. Authorities such as the U.S. Food and Drug Administration and the Medicines and Healthcare products Regulatory Agency classify many exosome-based products as biological or medicinal products, requiring rigorous clinical evidence, manufacturing controls, and approval pathways. For instance, in March 2026, Galderma announced that the U.S. FDA approved Restylane Contour for the correction of temple hollowing in adults aged 21 and older. The approval expands its existing indications beyond cheek augmentation and midface contour deficiencies, enabling treatment of age-related volume loss in the temple area.

In the aesthetic injectable market, substitutes include a range of non-invasive and minimally invasive treatments that deliver comparable cosmetic outcomes without relying on synthetic or biologically derived injectables. Procedures such as platelet-rich plasma (PRP) therapy are widely used as natural substitutes, promoting collagen regeneration and tissue repair using the patient’s own biological material. In addition, energy-based devices such as laser treatments and radiofrequency systems are effective alternatives that stimulate collagen production, improve skin firmness, and reduce wrinkles. Microneedling, often combined with growth factors or serums, is another commonly adopted approach to enhance skin texture, elasticity, and overall rejuvenation. Chemical peels and advanced dermocosmetic formulations further act as substitutes by addressing pigmentation, fine lines, and dull skin through controlled exfoliation and active ingredient penetration.

Regional expansion in the aesthetic injectable industry is gaining momentum across North America, Europe, and Asia Pacific, driven by rising demand for regenerative, minimally invasive aesthetic treatments and improving access to advanced dermatology services. Companies are actively expanding their global footprint through strategic partnerships, distributor networks, and targeted product launches to strengthen commercialization. For instance, in February 2026, Galderma announced the expansion of its Restylane portfolio in Japan with the launch of Restylane Defyne and Restylane Refyne, the first OBT-based hyaluronic acid injectables in the country. The launch increases the portfolio to four products, enabling clinicians to address a broader range of facial wrinkles, folds, and contouring needs.

Product Insights

The botulinum toxin (Botox) segment dominated the market in 2025, accounting for the largest global share of 44.5%. The growth is driven by its proven efficacy in reducing dynamic facial wrinkles and fine lines through temporary muscle relaxation. Derived from Clostridium botulinum, the neurotoxin inhibits acetylcholine release at the neuromuscular junction, resulting in localized muscle paralysis and a smoother skin appearance. Another major factor supporting the segment’s expansion is the rising consumer focus on facial aesthetics, skin quality, and anti-aging solutions. According to a March 2026 global survey by Allergan Aesthetics, approximately 74% of respondents expressed intent to improve skin quality within the next 12 months, while 63% identified addressing signs of aging, such as wrinkles and loss of elasticity, as primary concerns. This growing aesthetic awareness, combined with rising disposable income and greater access to dermatology clinics and medical spas, has significantly boosted demand for botulinum toxin-based treatments.

The PN/PDRN segment is expected to grow at the fastest CAGR of 16.9% over the forecast period. PN/PDRN consists of natural DNA fragments, typically derived from salmon, known for their excellent biocompatibility with human tissue. These molecules stimulate fibroblast activity, promote collagen and elastin production, and trigger cellular-level tissue repair. Unlike hyaluronic acid injectables that primarily offer volumizing effects, polynucleotides regenerate and revitalize the skin, targeting fine lines, wrinkles, scars, and stretch marks while improving skin tone and hydration. Clinical evidence strongly supports their efficacy. A recent trial involving 20 women showed visible improvement in skin texture and reduced wrinkles within 6 weeks, with no side effects. Another 20-week study demonstrated reduced stretch mark width and volume after PN injections, highlighting their regenerative capacity. Their low downtime and natural outcomes make them particularly attractive to both patients and practitioners.

Application Insights

The wrinkle correction segment dominated the aesthetic injectable market, accounting for the largest revenue share in 2025. Factors such as repeated facial expressions, long-term sun exposure, environmental stress, lifestyle habits like smoking, and gravity weaken the skin structure, making it less able to bounce back. As a result, the skin begins to fold and crease, especially in areas like the face, where movement and sun exposure are highest. The rising global demand for wrinkle correction injectables reflects several societal and demographic trends. An aging population increasingly seeks non-surgical aesthetic solutions that can delay or diminish visible signs of aging without the recovery time or risk associated with surgical procedures. With populations over age 60 expanding worldwide, the prevalence of wrinkles and sagging skin has become a central driver of consumer demand for minimally invasive interventions. According to the WHO data published in October 2025, by 2030, 1 in the 6 people will be aged 60 years or over, where its share will increase from 1 billion in 2020 to 1.4 billion. This highlights the rising need for aesthetic injectable solutions among this age group for the wrinkle correction.

The lip augmentation segment is expected to grow at the fastest CAGR over the forecast period. Lip augmentation utilizes aesthetic injectables to enhance the fullness, shape, and definition of the lips. This procedure appeals to those aiming for a more balanced facial appearance by achieving plumper, well-contoured lips. As a minimally invasive alternative to surgery, aesthetic injectable lip augmentation has gained significant popularity due to its quick, visible results. Clinicians often combine this treatment with other aesthetic injectables for overall facial rejuvenation. In August 2024, the Journal of Cutaneous and Aesthetic Surgery published a scoping review highlighting recent advancements in both injectable and surgical methods for lip augmentation. The review found that dermal filler injections remain the predominant approach due to their minimally invasive nature and immediate results, though their effects tend to be temporary.

End-use Insights

The medspas segment accounted for the largest revenue share of the aesthetic injectable industry in 2025, and is expected to grow at the fastest CAGR over the forecast period. Medspas, which blend medical expertise with a spa-like environment, have become popular destinations for clients seeking facial rejuvenation treatments. PLLA injectables are particularly favored in these settings due to their ability to stimulate collagen production, providing natural-looking, long-lasting results. According to the American Med Spa Association's 2024 report, the number of medical spas in the U.S. grew from 8,899 in 2022 to 10,488 in 2023, marking a 15.2% increase over two years. The average annual revenue per medspa also rose from USD 1,307,587 in 2023 to USD 1,398,833 in 2024, underscoring the sector's robust financial performance. Several factors, including advancements in aesthetic treatments, a growing consumer base, and increasing acceptance of non-surgical procedures, support this growth trajectory.

The aesthetic surgery centers segment is anticipated to grow at the second-fastest CAGR over the forecast period. Aesthetic surgery centers serve as primary access points for aesthetic injectable treatments, providing patients with a safe, specialized environment, skilled medical professionals, and advanced injection techniques. Rising disposable incomes, medical tourism, and increasing acceptance of cosmetic procedures among both men and women have further boosted procedure volumes in aesthetic surgery centers. Many centers now offer personalized treatment plans that use advanced imaging technologies and injection protocols, thereby improving patient satisfaction and outcomes. Furthermore, aesthetic centers serve as strategic distribution channels for aesthetic injectable manufacturers, accelerating product adoption and market penetration.

Regional Insights

The North America aesthetic Injectable market accounted for the largest global revenue share of 40.1% in 2025. Aesthetic surgery centers serve as primary access points for aesthetic injectable treatments, providing patients with a safe, specialized environment, skilled medical professionals, and advanced injection techniques. Rising disposable incomes, medical tourism, and increasing acceptance of cosmetic procedures among both men and women have further boosted procedure volumes in aesthetic surgery centers. Many centers now offer personalized treatment plans that use advanced imaging technologies and injection protocols, thereby improving patient satisfaction and outcomes. Furthermore, aesthetic centers serve as strategic distribution channels for aesthetic injectable manufacturers, accelerating product adoption and market penetration.

U.S. Aesthetic Injectable Market Trends

The U.S. aesthetic Injectable industry is experiencing steady growth, driven by continuous product innovation and regulatory approvals. For instance, Hugel received FDA approval for its botulinum toxin Letybo (letibotulinumtoxinA) for the treatment of moderate-to-severe glabellar lines. Supported by Phase III clinical trials involving over 1,000 patients, this approval strengthens competition within the neurotoxin segment and expands treatment options for both providers and patients. Distribution of aesthetic injectables in the U.S. follows a structured approach. Injectable products are primarily available through dermatology clinics, plastic surgeons, and licensed practitioners, while certain adjunctive or topical aesthetic products are increasingly accessible via online platforms. This reflects regulatory controls that restrict injectable procedures to trained professionals while enabling broader consumer access to supportive skincare solutions.

Europe Aesthetic Injectable Market Trends

The Europe aesthetic injectable industry is being reshaped by shifting consumer preferences toward authenticity and skin vitality. Rising interest in trends like “clean beauty” and “natural aesthetics” reflects a decline in demand for overfilled or highly contoured appearances. Instead, patients are prioritizing gradual collagen stimulation, improved skin texture, and long-term anti-aging benefits. This aligns well with the mechanism of PLLA and PDRN injectables, which enhance endogenous collagen production and tissue repair. A key driver of this transition is education-led adoption. Programs such as Galderma’s NEXT initiative and the Galderma Aesthetic Injector Network (GAIN) are equipping practitioners with advanced knowledge in facial assessment, regenerative techniques, and patient-centric treatment planning. In 2024, thousands of European clinicians participated in structured training programs focusing on minimally invasive procedures and combination therapies. This has accelerated the integration of injectables into holistic, multimodal treatment protocols that include microneedling, radiofrequency, and laser-based technologies.

The UK aesthetic injectable market is steadily growing. The growth is driven by evolving treatment preferences, technological innovation, and increasing regulatory intervention. A major trend shaping the market is the shift toward regenerative aesthetics, where injectables stimulate natural biological processes rather than simply adding volume. By 2025-2026, treatments such as polynucleotide (PDRN) injections have gained visibility in clinical practice, with leading London clinics promoting their ability to enhance hydration, elasticity, and collagen production through cellular repair. Similarly, biostimulatory products like Sculptra continue to support long-term tissue regeneration, reflecting a broader move toward subtle, natural-looking outcomes.

The aesthetic injectable market in Spain is experiencing significant growth, driven by increasing demand for minimally invasive and regenerative aesthetic treatments. Major urban centers such as Madrid, Barcelona, and Valencia are at the forefront of this transition, with clinics increasingly incorporating advanced injectables into comprehensive anti-aging protocols. Recent product launches further demonstrate Spain’s growing importance in the injectable market. In June 2024, Daewoong Pharmaceutical, through its partner Evolus, introduced its botulinum toxin product under the brand Nuceiva in Spain, expanding its footprint across key European markets. Additionally, in December 2024, Galderma launched Relfydess in Spain, generating significant interest due to its potential for faster onset, longer duration, and improved precision.

Asia Pacific Aesthetic Injectable Market Trends

The Asia Pacific aesthetic injectable industry is gaining traction and is expected to grow at the fastest CAGR of 11.9% during the forecast period. Growing awareness of aesthetic medicine, coupled with rising demand for natural-looking results with limited downtime, has contributed to wider acceptance of aesthetic injectables as an alternative or complement to traditional cosmetic procedures. Alongside this shift, the expansion of digital platforms, medical tourism, and e-commerce channels has accelerated the availability and visibility of these injectables and related treatment protocols across the Asia-Pacific region. International and regional companies are actively offering aesthetic injectable formulations that range from hyaluronic acid and vitamin-based solutions to advanced injectables enriched with polynucleotides, peptides, and growth-stimulating complexes. These products are entering the market primarily through partnerships with dermatology and aesthetic clinics, well-established distributor networks, and structured practitioner training and certification programs, enabling wider clinical adoption across key countries.

China’s aesthetic injectable market is experiencing rapid expansion as minimally invasive beauty treatments become mainstream and technological innovation accelerates the adoption of injectable products. The growth is majorly driven by an aging population and a culture that increasingly embraces aesthetic treatments for youthfulness and appearance enhancement. At the same time, younger demographics, social media influence, and urbanization are boosting acceptance of aesthetic procedures, particularly among millennials and Gen Z consumers who seek subtle, natural results. In addition, the shift from traditional beauty treatments to injectables emphasizes safety, long-term outcomes, and collagen induction, reflecting an evolution in the product mix that aligns with more sophisticated consumer expectations.

The aesthetic injectable market in South Korea is largely driven by shifting consumer preferences toward natural-looking, regenerative outcomes and increasing adoption of non-invasive procedures. A key structural driver is the country’s rapidly aging population. According to a January 2026 report by JoongAng Ilbo, individuals aged 65 and above now account for over 21% of the total population, reflecting South Korea’s transition into a super-aged society. This demographic trend is significantly influencing demand for treatments that enhance skin quality, restore structural integrity, and support long-term tissue regeneration rather than delivering temporary volumization.

Latin America Aesthetic Injectable Market Trends

The Latin America region is an emerging market for aesthetic injectables and is expected to grow at the significant rate due to strong beauty consciousness, growing disposable income, and increasing acceptance of minimally invasive cosmetic procedures. Countries such as Brazil, Mexico, Colombia, and Argentina are key contributors, with consumers increasingly favoring collagen stimulators and regenerative fillers that enhance skin quality and stimulate natural tissue renewal rather than providing volume alone. This shift reflects a broader preference for subtle, natural-looking, and longer-lasting aesthetic outcomes. The region benefits from an expanding network of dermatology clinics, aesthetic centers, and medical spas, particularly in major urban hubs. Brazil stands out as a regional leader due to its high procedural volume, advanced practitioner expertise, and strong medical tourism ecosystem. Demand is being further driven by patients seeking procedures with minimal downtime, preventative anti-aging benefits, and gradual improvement in skin firmness, texture, and elasticity, key advantages associated with biostimulatory and regenerative injectable treatments.

The Brazil aesthetic injectable market is growing. The growth is supported by rising consumer awareness of non-surgical options, increasing disposable incomes, and a preference for treatments with minimal downtime and natural-looking results. For instance, in October 2023, Brazilian economic data showed that rising household disposable income was supporting broader economic activity, with authorities noting that increased consumer spending was an important contributor to growth amid evolving macro conditions in the country. This improvement in disposable income was cited as a factor boosting consumption and overall demand within Brazil’s economy. Such developments suggest an expanding base of consumer purchasing power that can positively influence sectors such as aesthetic injectable treatments.

Middle East & Africa Aesthetic Injectable Market Trends

The Middle East and Africa (MEA) aesthetic injectable industry is growing steadily, driven by rising aesthetic awareness, rising disposable incomes in urban centers, and an expanding network of specialized dermatology clinics and medical spas. Urban consumers in major cities are increasingly opting for minimally invasive solutions with natural-looking results, often influenced by social media and evolving beauty standards that emphasize subtle enhancement over surgical intervention. This has led to broader acceptance of injectables that not only restore volume but also enhance skin quality and promote rejuvenation.

The aesthetic injectable market in Saudi Arabia is experiencing notable growth supported by a combination of economic, demographic, and cultural factors. Rising disposable incomes, particularly among the urban middle- and high-income population, have increased the affordability of elective cosmetic procedures such as dermal fillers, botulinum toxin injections, and biostimulatory treatments. At the same time, a relatively young population with strong exposure to global beauty trends through social media is becoming more proactive about enhancing appearance and adopting preventive aesthetics, driving higher demand for minimally invasive procedures.

Key Aesthetic Injectable Company Insights

The aesthetic injectable market is highly competitive, with several key players. The major players are focusing on expanding their geographical footprint, forming strategic partnerships to enhance product accessibility and clinical adoption, and advancing regenerative skincare and hair restoration solutions through innovative aesthetic technologies.

Key Aesthetic Injectable Companies:

The following key companies have been profiled for this study on the aesthetic injectable market.

- AbbVie Inc

- Galderma

- Merz GmbH and Co. KGaA

- Sinclair

- Medytox

- Prollenium Medical Technologies

- Tiger Aesthetics Medical (Suneva Medical, Inc.)

- HUGEL, Inc.

- Ipsen Pharma

- Teoxane

Recent Developments

-

In April 2026, Merz Aesthetics announced that the U.S. FDA approved Radiesse for the treatment of wrinkles in the décolleté area, marking a significant expansion of its aesthetic indications. The calcium hydroxylapatite (CaHA)-based biostimulator stimulates collagen and elastin production, helping improve skin quality and firmness in the chest area.

-

In May 2025, Teoxane expanded its presence in the U.S. market by launching its dermocosmetics line directly to consumers online. Previously accessible only through aesthetic professionals, this move allows broader consumer access to Teoxane’s advanced skincare products featuring patented Resilient Hyaluronic Acid technology, marking a strategic shift beyond their established dermal filler offerings.

-

In October 2024, Tiger Aesthetics Medical, LLC expanded its regenerative aesthetics portfolio by acquiring BellaFill, a biostimulatory dermal filler, from Suneva Medical, Inc. This acquisition strengthened Tiger Aesthetics’ presence in the dermal fillers market by adding BellaFill’s well-established, long-lasting filler to its product lineup.

-

In March 2023, Allergan Aesthetics, a subsidiary of AbbVie, partnered with IFundWomen, a funding marketplace for women-owned businesses, to celebrate International Women’s Day. As part of this collaboration, they launched a grant program to support female entrepreneurs in their business ventures.

Aesthetic Injectable Market Report Scope

Report Attribute

Details

Market size in 2025

USD 11.1 billion

Estimated market size in 2026

USD 12.3 billion

Projected market size by 2033

USD 24.1 billion

Growth rate

CAGR of 10.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, end-use,region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway: Russia; Japan; China India; Australia; Thailand; South Korea; Singapore; Malaysia; Taiwan; Vietnam; Philippines; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

AbbVie Inc.; Galderma; Merz GmbH and Co. KGaA; Sinclair; Medytox; Prollenium Medical Technologies; Tiger Aesthetics Medical (Suneva Medical, Inc.); HUGEL, Inc.; Ipsen Pharma; Teoxane

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to the country, regional, and segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Aesthetic Injectable Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. Forthis study, Grand View Research has segmented the global aesthetic injectable market report based on product, application, end-use, and region:

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Collagen and PMMA Microspheres

-

Hyaluronic Acid

-

Monophasic

-

Biphasic

-

-

Calcium Hydroxylapatite (CaHA)

-

PLLA

-

PCL

-

PN/PDRN

-

Botulinum Toxin (Botox)

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Wrinkle Correction

-

Lip Augmentation

-

Facial Contouring

-

Scar Treatment

-

Volume Loss Restoration

-

Others

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

MedSpas

-

Aesthetic Surgery Centers

-

Hospitals

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Norway

-

Denmark

-

Sweden

-

Russia

-

-

Asia Pacific

-

China

-

Japan

-

South Korea

-

Thailand

-

Australia

-

Singapore

-

Malaysia

-

Taiwan

-

India

-

Vietnam

-

Philippines

-

-

Latin America

-

Brazil

-

Argentina

-

-

MEA

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

Key factors that are driving the aesthetic injectable market growth include the shifting beauty standards and a growing aging population contribute to market expansion, availability of a wide range of injectable products, coupled with innovative marketing strategies by key players, stimulate market growth.

North America dominated the aesthetic injectable market with a share of 40.1% in 2025. This is attributable to the growing population aged between 25 and 65 years, a demographic showing high concern related to skin aging, including skin laxity, wrinkles, and dark spots.

Asia Pacific is the fastest-growing region over the forecast period.

Botulinum toxin (botox) segment led with a 44.5% revenue share in 2025, while PN/PDRN is the fastest-growing product.

The wrinkle correction segment held the largest revenue share in 2025, while lip augmentation is the fastest-growing application.

MedSpas segment led with a 42.8% revenue share in 2025, and is the fastest-growing end use.

The global aesthetic injectable market size was valued at USD 11.1 billion in 2025 and is estimated at USD 12.3 billion for 2026.

The global aesthetic injectable market is expected to grow at a CAGR of 10.0% from 2026 to 2033, reaching USD 24.1 billion by 2033.

Key players include AbbVie Inc.; Galderma; Merz GmbH and Co. KGaA; Sinclair; Medytox; Prollenium Medical Technologies; Tiger Aesthetics Medical (Suneva Medical, Inc.); HUGEL, Inc.; Ipsen Pharma; Teoxane.

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.