- Home

- »

- Plastics, Polymers & Resins

- »

-

Agricultural Films Market Size, Share, Industry Report, 2033GVR Report cover

![Agricultural Films Market Size, Share & Trends Report]()

Agricultural Films Market (2026 - 2033) Size, Share & Trends Analysis Report By Product (Conventional Plastics, Biodegradable Plastics), By Application (Green House, Mulching, Silage), By Region (North America, Europe, Asia Pacific), And Segment Forecasts

- Report ID: 978-1-68038-144-3

- Number of Report Pages: 100

- Format: PDF

- Historical Range: 2021 - 2024

- Forecast Period: 2026 - 2033

- Industry: Bulk Chemicals

- Report Summary

- Table of Contents

- Segmentation

- Methodology

- Download FREE Sample

-

Download Sample Report

Download Sample Report

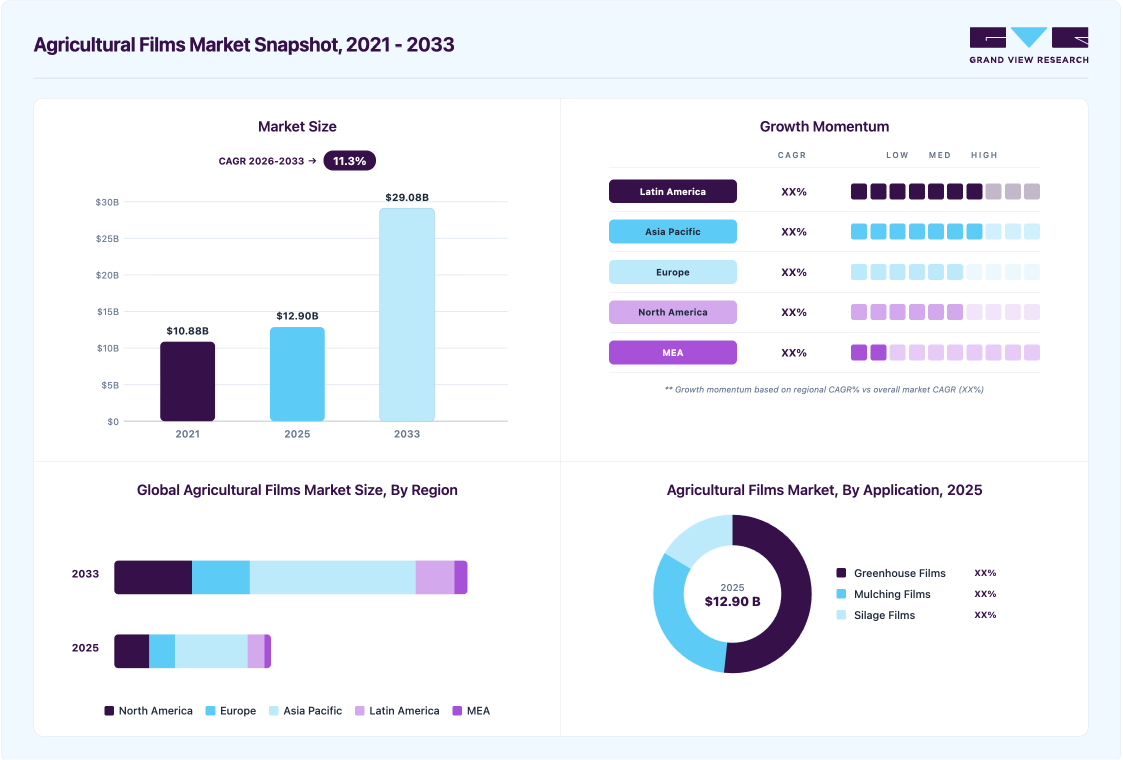

Market Size, 2025$12.9BMarket Estimate, 2026$13.8BMarket Forecast, 2033$29.1BCAGR, 2026 - 203311.3%Agricultural Films Market Summary

The global agricultural films market size was valued at USD 12.90 billion in 2025 and is projected to reach USD 29.08 billion by 2033, growing at a CAGR of 11.3% from 2026 to 2033. Agricultural output, demand for modern agricultural practices, and sustainable farming are expected to drive the agricultural films market in the forecast period.

Key Market Trends & Insights

- Asia Pacific dominated the Agricultural Films Market with the largest revenue share of 46.23% in 2025.

- The Agricultural Films Market in China is expected to grow at a substantial CAGR of 11.9% from 2026 to 2033.

- By product, the biodegradable plastics segment is expected to grow at the fastest CAGR of 15.5% from 2026 to 2033 in terms of revenue.

- By application, the Greenhouse Films segment is expected to grow at the fastest CAGR of 11.8% from 2026 to 2033 in terms of revenue.

Market Size & Forecast

- 2025 Market Size: USD 12.90 Billion

- 2033 Projected Market Size: USD 29.08 Billion

- CAGR (2026-2033): 11.3%

- Asia Pacific: Largest market in 2025

Agricultural film products are used to protect crops in greenhouses and help plants withstand extreme climates. Agricultural films are used in various farming techniques to improve crop quality, regulate soil temperature, control weed growth, and boost crop yields. Other uses of these products include storing corn, silage, and hay. Thus, farmers require agricultural films for their cultivation needs. Agricultural films are proven solutions for soil protection, greenhouse yields, and precision farming. The elastic films safeguard the plants in both indoor and outdoor environments. The durability and efficiency of agricultural films improve production. In extreme climates and regions with excess rainfall, it lessens the impact of hail.")

The growing demand for food has led to increased use of plastic films in the agricultural sector. These films are used in low tunnels, irrigation systems, mulching, and silage. Agricultural films enhance crop yield, leading to better harvests and higher yields. Therefore, they are utilized in contemporary agriculture to supplement crop production. Unlike the norm, film manufacturing industries focus on producing nano greenhouse films for agricultural use at affordable prices. These films are ideal for remote regions because they do not require electricity.

Market Dynamics

As the global population continues to grow, the demand for food is increasing rapidly. This, coupled with rising per capita income, is driving a shift toward better quality and higher quantity food production. People now expect fresher, healthier, and more diverse food options, which has put significant pressure on the agricultural sector to improve crop yield and quality. To meet this growing demand, farmers are turning to innovative farming techniques, including the use of agricultural films. Agricultural films are used in several mulching applications, such as to cover soil, helping to retain moisture, control weeds, and regulate soil temperature, all of which contribute to higher crop productivity. As a result, the global mulch films market is expected to experience substantial growth as more farmers adopt these products to increase efficiency and output in food production.

Moreover, the shift toward intensive agricultural practices is driven by the need to produce more food on the same amount of land, or even less land in some regions. Agricultural films help in optimizing these conditions by improving water usage efficiency and reducing the reliance on chemical pesticides and herbicides. This technology has become crucial, especially in regions facing water scarcity or harsh climates, where maintaining soil quality and moisture levels is vital for successful crop production. The growing emphasis on sustainability in agriculture is also pushing the demand for biodegradable agricultural films, which provide the same benefits while reducing plastic waste. Overall, these factors are contributing to the growing importance of agricultural films in modern farming, helping farmers meet the rising food demands of a growing global population.

High installation costs are restraining the growth of the global agricultural films market, especially for small and medium-sized farmers. While mulch films offer several benefits, including improved crop yields, better moisture retention, and weed control, the initial investment required for purchasing and installing these films can be substantial. This includes the cost of agricultural films and the additional expenses of labor and equipment needed for proper installation. For many farmers, especially in developing regions, these upfront costs can be prohibitive, limiting the adoption of agricultural films despite their long-term benefits. As a result, the high initial investment acts as a barrier to market growth.

Market Concentration & Characteristics

The agricultural films industry demonstrates a moderate to high level of innovation, spurred by ongoing breakthroughs in material science, multilayer film designs, and functional additives that improve durability, light management, and environmental impact. The innovation is particularly notable in the realm of biodegradable and specialty films, where producers aim to enhance field longevity and controlled degradation. The industry also experiences a moderate frequency of mergers and acquisitions, as major polymer producers and film manufacturers seek to expand capacity, increase geographical presence, and diversify their portfolios, while smaller companies are often acquired to gain access to proprietary technologies and bio-based formulations.

Regulatory frameworks governing plastic use and waste management significantly impact the agricultural films market, particularly in areas that impose restrictions on single-use plastics. These regulations are driving the transition to biodegradable, compostable, and recyclable film options, while also increasing compliance costs for traditional plastic products. Alternatives, including organic mulching materials, paper-based coverings, and woven fabrics, pose a limited yet expanding competitive challenge; however, their reduced durability and variable performance often hinder wide-scale adoption compared to plastic films.

The end user base in the agricultural films market is quite fragmented, highlighting the extensive and varied group of farmers, including both smallholders and large commercial growers. Although the volume of individual usage tends to be low, demand is consolidated through cooperatives, distributors, and agribusinesses, which have moderate bargaining power. On the other hand, greenhouse operators and large-scale horticulture farms constitute more concentrated end-user groups, typically forming long-term supply relationships and preferring high-performance, value-added film products.

Product Insights

Conventional Plastics accounted for the largest market share in 2025, at 73.54%. Conventional plastics are the primary material category in the agricultural films sector, driven by their affordability, ease of processing, and proven performance. Low-Density Polyethylene (LDPE) and Linear Low-Density Polyethylene (LLDPE) are commonly used for their flexibility, durability, and outstanding film-forming capabilities, making them ideal for applications such as mulching and greenhouse coverings. High-Density Polyethylene (HDPE) is favored in applications that demand greater strength, rigidity, and chemical resistance. Ethyl Vinyl Acetate (EVA) and Ethyl Butyl Acrylate (EBA) are added to improve clarity, elasticity, and thermal efficiency, especially in greenhouse films. The use of reclaimed materials is on the rise to lower raw material expenses and promote circular economy practices, while other standard polymers cater to specific performance needs.

Biodegradable plastics are expected to register the fastest CAGR of 15.5% during the forecast period. Biodegradable plastics are driven by heightened environmental regulations, concerns about soil health, and a desire to minimize plastic waste buildup on agricultural lands. These materials are designed to break down in specific agricultural environments, eliminating the need to remove and dispose of film after use, reducing labor costs and enhancing operational efficiency for farmers. The increasing use of these films is especially noticeable in mulching applications, where biodegradable options provide similar agronomic benefits to traditional plastics while promoting sustainable farming practices.

Application Insights

The Greenhouse Films segment accounted for the largest market revenue share of 51.70% in 2025. Greenhouse films play a crucial and rapidly growing role in the agricultural films market, driven by the growing use of protected cultivation techniques to improve crop production, resource efficiency, and year-round productivity. These films are designed to ensure optimal light transmission, thermal insulation, and microclimate regulation, enabling farmers to counter climatic fluctuations and extend growing seasons across various regions.

Mulching is projected to grow at a significant 11.0% CAGR over the forecast period. Mulching films are a fundamental segment of the agricultural films market due to their role in enhancing crop yields and farm input efficiency. These films are commonly used to control weed growth, retain soil moisture, manage soil temperature, and reduce nutrient loss, thereby increasing yields and improving crop quality. Additionally, mulching films facilitate earlier planting and more consistent plant growth, especially in high-value crops such as vegetables, fruits, and row crops. The rising adoption of these films is driven by the need to optimize water use, reduce reliance on chemical herbicides, and promote sustainability in agriculture.

Regional Insights

North America agricultural films accounted for a global market share of 22.31% in 2025. The rising popularity of greenhouse farming, the need to conserve water resources, and the growing interest in organic agriculture are driving the agricultural film market. Furthermore, regional market growth is anticipated to be positive due to agricultural films' biodegradability, UV resistance, and increased durability.

U.S. Agricultural Films Market Trends

The U.S. agricultural films market is expected to grow rapidly in the coming years due to population growth, and the country is a major agricultural exporter. Shifts in farming practices from traditional to modern techniques underpin the demand for mulching films in the U.S. Additionally, as environmental concerns continue to dominate, biodegradable agricultural products will witness significant growth in the forecast period.

Asia Pacific Agricultural Films Market Trends

Asia Pacific agricultural films dominated the global market in 2025, with a 46.23% revenue share, driven by high populations in countries such as China and India. There is a significant increase in food demand. Ideal weather conditions support perennial farming, and with the help of agricultural films, soil quality can be controlled. Furthermore, the increasing use of greenhouse technology and focus on sustainability objectives drive market expansion with a leading position in the global market. It also capitalizes on the growing use of advanced farming techniques, which increases demand for agricultural films.

Agricultural films market in China dominated the market with a share of 44.15% in 2025 due to farmers adopt protective agrarian methods to improve the output and quality of crops. Protected cultivation covers nearly 3.3 million hectares of crop area in China.

Europe Agricultural Films Market Trends

Europe agricultural films market is anticipated to witness significant growth due to the rising use of modern farming practices and technologies, the desire for better crop yield and quality, and increased awareness of sustainable agriculture are fueling the demand for agricultural films. In addition, the anticipated growth of the agricultural film market in the area is expected to be driven by increased government support and efforts to promote sustainable farming practices and reduce carbon emissions.

The UK agricultural films market growth is anticipated to be higher in the coming years as agricultural films such as mulches and silage wraps maximize productivity on existing farmlands. The UK has a flourishing greenhouse industry driven by demand for out-of-season produce and protection against unpredictable weather.

Key Agricultural Films Company Insights

Key companies are adopting a range of organic and inorganic growth strategies, such as new product development, mergers & acquisitions, and joint ventures, to maintain and expand their market share.

Key Agricultural Films Companies:

The following key companies have been profiled for this study on the agricultural films market.

- Dow Inc.

- Ab Rani Plast Oy

- ARMANDO ÁLVAREZ, S.A.

- Berry Global Inc.

- Kuraray Co. Ltd

- Coveris

- RKW Group

- Trioplast Industrier AB (Trioworld Industrier AB)

- Exxon Mobil Corporation

- Groupe Barbier

- Novamont S.p.A.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature player: Dow Inc.; Berry Global Inc.; Kuraray Co. Ltd.; Coveris; RKW Group; Trioplast Industrier AB; Exxon Mobil Corporation; Groupe Barbier - Focus on the expansion of multilayer agricultural film production and sustainable film technologies.

- Invest in recyclable, biodegradable, and UV-resistant agricultural film solutions.

- Strengthen global distribution networks and partnerships with agricultural distributors and farming cooperatives.

- Strong manufacturing scale and integrated raw material supply capabilities.

- Broad product portfolios with advanced film technologies for greenhouse, mulch, and silage applications.

- Established a global customer base and high R&D investment capacity.

- Exposure to fluctuations in petrochemical feedstock prices.

- High operational and sustainability compliance costs.

- Dependence on seasonal agricultural demand and climatic conditions.

Emerging Players: Ab Rani Plast Oy; ARMANDO ÁLVAREZ, S.A.; Novamont S.p.A. - Focus on niche agricultural film applications and sustainable bio-based film development.

- Expand regional distribution capabilities and customer-specific product customization.

- Strengthen presence in biodegradable and environmentally friendly agricultural film segments.

- Higher operational flexibility and faster innovation in specialty agricultural films.

- Strong focus on sustainable and biodegradable material technologies.

- Ability to cater to region-specific farming and crop protection requirements.

- Limited global manufacturing and distribution scale compared to multinational leaders.

- Narrower product portfolios and lower bargaining power in raw material procurement.

- Comparatively lower financial and R&D resources for large-scale expansion initiatives.

Agricultural Films Market Report Scope

Report Attribute

Details

Market size value in 2026

USD 13.76 billion

Revenue forecast in 2033

USD 29.08 billion

Growth rate

CAGR of 11.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Russia; Denmark; Sweden; Norway; China; Japan; India; South Korea; Australia; Indonesia; Vietnam; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

Dow Inc.; Ab Rani Plast Oy; ARMANDO ÁLVAREZ, S.A.; Berry Global Inc.; Kuraray Co. Ltd; Coveris; RKW Group; Trioplast Industrier AB (Trioworld Industrier AB); Exxon Mobil Corporation; Groupe Barbier; Novamont S.p.A.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Agricultural Films Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends across sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global agricultural film market report based on product, application, and region.

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Conventional Plastics

-

Low-Density Polyethylene (LDPE)

-

Linear Low-Density Polyethylene (LLDPE)

-

High-Density Polyethylene (HDPE)

-

Ethyl Vinyl Acetate/Ethyl Butyl Acrylate (EVA/EBA)

-

Reclaims

-

Others

-

-

Biodegradable Plastics

-

Starch-based Plastics

-

Polylactic Acid (PLA)

-

Polyhydroxyalkanoates (PHA)

-

Others

-

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Greenhouse Films

-

Classic Greenhouse

-

Macro Tunnel/Walking Tunnel

-

Low Tunnel

-

-

Mulching Films

-

Transparent or Clear Mulches

-

Black Mulches

-

Other Mulches

-

-

Silage Films

-

Silage Stretch Wrap

-

Silage Sheet

-

Silage Bag

-

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Russia

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

Indonesia

-

Vietnam

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Cross-Segmentation

The agricultural films market was thoroughly examined in terms of greenhouse films, mulch films, and silage films, which included various sub-segments such as traditional greenhouse, macro tunnel/walking tunnel, low tunnel, clear mulches, black mulches, silage stretch wrap, silage sheets, and silage bags. The analysis also explored demand patterns based on film characteristics, types of crops, farming methods, suitability for different climates, durability needs, UV resistance, oxygen barrier effectiveness, and use in protected cultivation, commercial agriculture, and livestock feed preservation.

Recognize crucial overlaps between fast-expanding industries and opportunities for tailored applications. Assist in targeted product development and strategies for enhancing the portfolio. Aid in identifying preferred crops and agricultural uses across various regional markets.

Competitive Benchmarking

An evaluation of top agricultural film producers concerning their product range, production capacity, commitment to sustainability, geographic reach, technological prowess, pricing strategies, and key strategic advancements. A comparative analysis of operational advantages and emphasis on innovation among global and regional market players.

Recognize competitive positioning opportunities and compare performance with industry leaders. Assist in developing differentiation strategies, evaluating partnerships, and planning for expansion. Facilitate strategic decision-making regarding product positioning and market entry.

Pricing Analysis

Analysis of pricing trends for agricultural films by material types, applications, and regions, which includes an examination of resin price variations, raw material expenses, multilayer film costs, premiums for biodegradable films, and supply and demand factors. The evaluation also investigated past price changes and the future pricing forecast in major agricultural areas.

Enhance the optimization of pricing strategies and procurement planning. Increase awareness of cost factors, regional pricing competitiveness, and areas experiencing margin pressure. Facilitate improved forecasting and commercial planning for agricultural film applications.

Frequently Asked Questions About This Report

Key factors that are driving the market growth include rising high-quality crop requirement for optimum agricultural productivity and declining arable land.

The global agricultural films market size was estimated at USD 12.90 billion in 2025 and is expected to reach USD 13.76 billion in 2026.

The global agricultural films market is expected to grow at a compound annual growth rate of 11.3% from 2026 to 2033 to reach USD 29.08 billion by 2033.

The Conventional Plastics segment dominated the agricultural films market, accounting for 73.98% in 2025. Conventional plastics are the primary material category in the agricultural films sector, driven by their affordability, ease of processing, and proven performance.

Some key players operating in the agricultural films market include Dow Inc., Ab Rani Plast Oy, ARMANDO ÁLVAREZ, S.A., Berry Global Inc., Kuraray Co. Ltd, and Coveris, among others.

About the authors:

Author: GVR Plastics, Polymers & Resins Research Team | Last Updated:

Share this report with your colleague or friend.

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.