- Home

- »

- Next Generation Technologies

- »

-

AI Code Assistants Market Size, Share, Industry Report 2033GVR Report cover

![AI Code Assistants Market Size, Share & Trends Report]()

AI Code Assistants Market (2026 - 2033) Size, Share & Trends Analysis Report By Component (Software, Service), By Deployment Mode (Cloud-based, On-premises), By Application (Code Debugging, Documentation Generation), By End-user, By Region, And Segment Forecasts

Market Size, 2025

$8.5BMarket Estimate, 2026

$10.3BMarket Forecast, 2033

$42.8BCAGR, 2026–2033

22.5%AI Code Assistants Market Summary

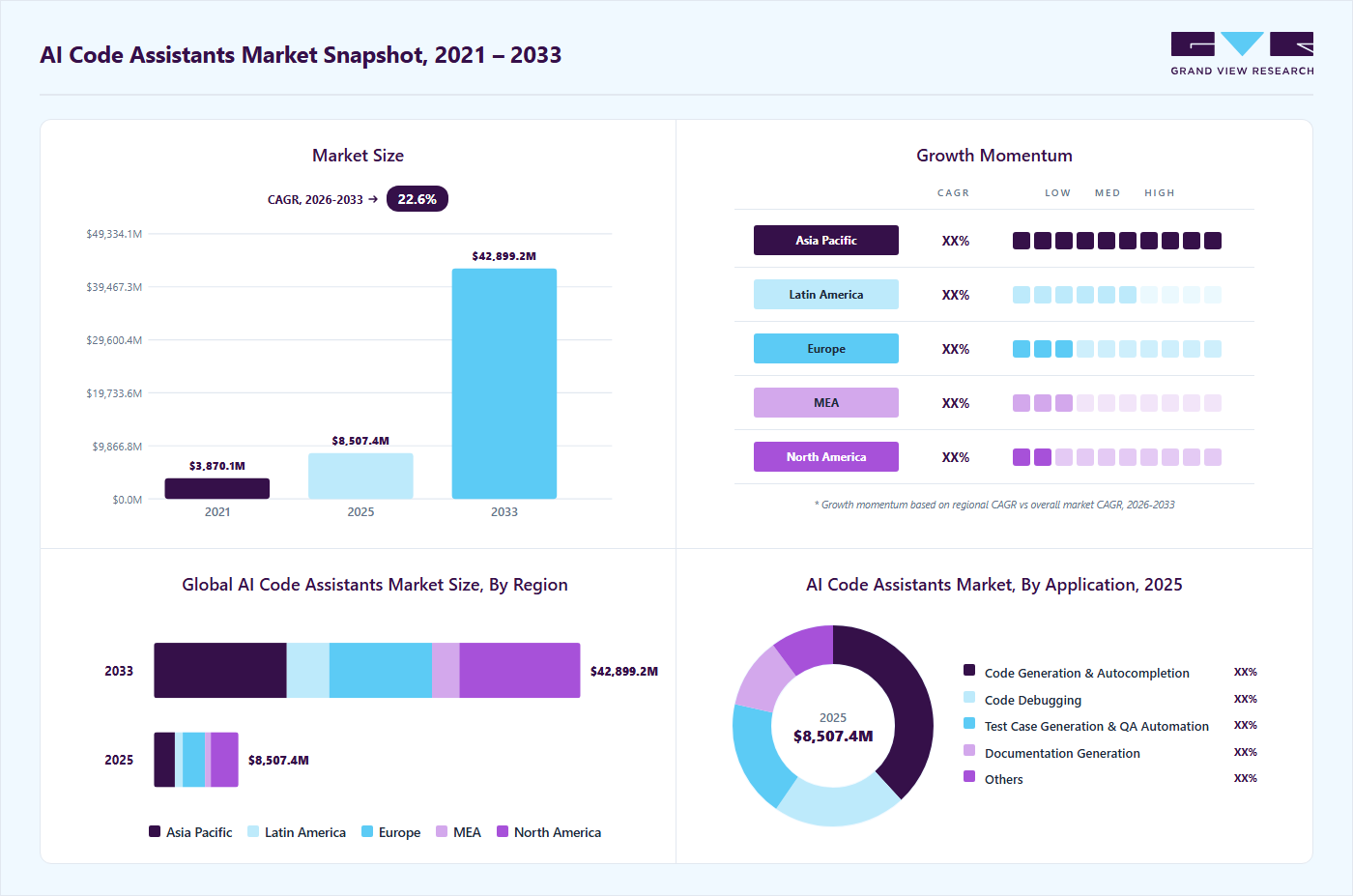

The global AI code assistants market size was valued at USD 8.5 billion in 2025 and is projected to grow from USD 10.3 billion in 2026 to USD 42.8 billion by 2033, at a CAGR of 22.5% from 2026 to 2033. North America dominated the global AI code assistants market with the largest revenue share of 32.7% in 2025. AI code assistants are increasingly replacing traditional coding support tools by delivering contextual, real-time recommendations directly within development environments, driving the market growth.

Key Market Trends & Insights

- By component: the software segment led the market with the largest revenue share of 78.7% in 2025.

- By deployment mode: the cloud-based segment held the dominant market position with the leading revenue share of 74.1% in 2025.

- By application: the code generation & autocompletion segment accounted for the largest revenue share in 2025.

Regional Highlights

- Largest regional market: North America (32.7% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 8.5 Billion

- Estimated market size in 2026: USD 10.3 Billion

- Projected market size by 2033: USD 42.8 Billion

- CAGR (2026-2033): 22.5%

AI code assistants are accelerating software development by automating routine programming tasks and reducing manual coding effort. They support multiple stages of development, including code generation, debugging, and documentation, enabling developers to complete tasks more efficiently. Research indicates that developers experience productivity improvements through faster implementation and structured guidance during coding processes. These tools also reduce dependency on traditional knowledge sources by providing contextual suggestions directly within development environments. This shift is driving widespread integration of AI assistants into daily developer workflows across industries.

The expansion of AI assistants across the full software development lifecycle is strengthening their adoption across organizations for testing, code validation, and documentation, supporting continuous integration and development pipelines. It shows that AI-driven systems enhance both learning and implementation processes by offering real-time insights and structured coding assistance. At the same time, enterprises are increasingly implementing AI into engineering practices to improve output volume and streamline workflows. This broader functional coverage is transforming AI code assistants into essential components of modern software engineering environments.

")

Additionally, the rising demand for secure, governed AI use is further shaping the adoption of AI coding assistants in enterprise environments. Government and cybersecurity agencies emphasize the importance of controlled deployment to mitigate risks associated with code quality, vulnerabilities, and data exposure. While AI improves productivity, it introduces variability in output and requires human oversight for validation. Additionally, the influence of AI on developer skill formation and long-term expertise is gaining attention in research environments. These factors are encouraging organizations to adopt structured frameworks for integrating AI into development workflows.

Component Insights

The software segment led the AI code assistants market, accounting for 78.7% of the global revenue share in 2025. AI code assistants delivered as software are gaining strong traction due to their direct impact on developer productivity and workflow efficiency. These tools are increasingly implanted into daily workflows, transforming from optional utilities into core software infrastructure within organizations. The ability of software-based assistants to enable users to perform tasks beyond their existing technical capabilities is further expanding their adoption across both technical and non-technical roles.

The service segment is expected to grow significantly during the forecast period. The services segment is expanding due to increasing enterprise demand for implementation, integration, and customization of AI-driven development tools. The complexity of deploying AI across the software development lifecycle has increased the need for consulting, training, and managed services to ensure effective utilization. Enterprises are also focusing on optimizing performance, monitoring outputs, and maintaining compliance, which drives continuous service engagement.

Deployment Mode Insights

The cloud-based segment accounted for the largest revenue share of 74.1% in 2025. Cloud-based deployment is driving adoption by enabling scalable access to advanced models without the need for local infrastructure. Organizations benefit from seamless integration with development environments, DevOps pipelines, and collaborative workflows, improving operational efficiency. Centralized cloud platforms support continuous updates and model improvements, ensuring consistent performance and feature enhancement across users. The availability of API-based access allows enterprises to embed AI capabilities directly into internal tools and applications, expanding usage across teams.

The on-premises segment is expected to grow significantly over the forecast period due to rising concerns about data security, intellectual property protection, and regulatory compliance. Organizations handling sensitive codebases prefer localized environments to maintain full control over data access, processing, and storage. This deployment model enables customization of models and workflows to meet specific enterprise requirements without external dependency. As enterprises move from pilot adoption to structured implementation, on-premises solutions are increasingly adopted to ensure controlled and secure integration of AI into development environments.

End-user Insights

The large enterprises segment accounted for the largest revenue share of the AI code assistants market in 2025, driven by the need to improve developer productivity across large, distributed engineering teams. These organizations integrate AI tools into existing DevOps and software delivery pipelines to accelerate development cycles and enhance operational efficiency. Enterprise environments generate significant volumes of code, making automation essential to reduce repetitive tasks and improve output consistency. The availability of scalable licensing models and centralized deployment enables organizations to standardize AI usage across teams and projects.

The SME segment is expected to grow significantly during the forecast period. The growth is driven by the availability of cloud-based solutions and subscription models has lowered entry barriers, enabling SMEs to integrate advanced AI capabilities into their workflows. AI-assisted development also supports faster product iteration and shorter release cycles, helping SMEs remain competitive in dynamic digital markets. As businesses prioritize efficiency and scalability, AI code assistants are becoming a key enabler of streamlined development processes within the SME segment.

Application Insights

The code generation & autocompletion segment accounted for the largest revenue share in 2025. This segment growth is driven by their ability to reduce manual coding effort and accelerate development cycles. These tools provide real-time suggestions and automate repetitive programming tasks, enabling developers to focus on higher-value problem-solving. Their integration into development environments enhances coding consistency, reduces errors, and supports faster feature delivery. The capability to generate context-aware code across multiple languages strengthens its significance across different software projects.

The test case generation & QA automation segment is projected to grow significantly over the forecast period. These tools automate the creation of test scenarios, reducing manual effort and improving coverage across complex codebases. Integration with continuous integration and delivery pipelines enables real-time validation and early defect detection during development. For instance, in November 2024, Tricentis announced the launch of qTest Copilot, a generative AI-powered assistant integrated into its test management platform to enhance software testing processes.

Regional Insights

North America dominated the AI code assistants market with a revenue share of 32.7% in 2025. The region is driven by early enterprise adoption of AI-driven development tools supported by advanced cloud infrastructure and mature DevOps practices. Strong presence of global technology providers and continuous investment in generative AI research enable rapid integration of coding assistants into software workflows. Organizations focus on productivity optimization and software delivery efficiency to accelerate deployment across engineering teams.

U.S. AI Code Assistants Market Trends

The U.S. AI code-assistant industry is characterized by high levels of enterprise spending on AI technologies and strong integration of coding assistants into software development workflows. Organizations are focusing on improving engineering productivity and accelerating innovation through AI-enabled tools. The presence of leading AI model developers and platform providers supports continuous advancement in capabilities and deployment scale. Widespread adoption across sectors such as technology, finance, and e-commerce is highlighting the role of AI code assistants as a standard development tool.

Europe AI Code Assistants Market Trends

In Europe, the market growth is supported by increasing focus on regulatory compliance, data protection, and ethical AI deployment across industries. Organizations are adopting AI code assistants to improve software quality while maintaining adherence to strict governance standards. The region also benefits from strong industrial digitalization initiatives, particularly in manufacturing, automotive, and financial sectors. Collaborative research programs and government-backed innovation initiatives are contributing to the structured adoption of AI assistants in code development.

Asia Pacific AI Code Assistants Market Trends

The Asia Pacific AI code assistants industry is expected to grow at the fastest CAGR during the forecast period, driven by a rapidly growing developer base and increasing demand for digital transformation across enterprises. Organizations are adopting AI code assistants to enhance productivity, reduce development timelines, and support large-scale application development. The rise of startup ecosystems and technology outsourcing hubs is further contributing to widespread adoption. Cost optimization and efficiency improvements remain key factors influencing the integration of AI code assistants.

Key AI Code Assistants Company Insights

Some key companies in the AI code assistants industry are GitHub, Inc., TRAE (Tabnine),Amazon Web Services, Inc, Cognition AI, Inc (Devin)

-

Amazon Web Services (AWS) provides a broad set of cloud computing services that help organizations build, launch, and manage applications as needed. Its platform includes computing, storage, networking, databases, analytics, and machine learning, all available in flexible cloud environments. AWS also offers APIs, developer tools, and integrated services to simplify automation and deployment. It supports open-source projects and works with many frameworks and technologies for both businesses and developers.

-

GitHub is a software development platform that provides tools for version tracking, issue management, and collaborative workflows, allowing teams to coordinate development activities efficiently. The platform supports continuous integration and deployment processes through automation features, enabling streamlined application delivery across environments. GitHub hosts a large ecosystem of open-source and private repositories, facilitating knowledge sharing and code reuse among developers. It also integrates with a wide range of development tools and cloud platforms, supporting modern software engineering practices.

Key AI Code Assistants Companies:

The following key companies have been profiled for this study on the AI code assistants market.

- Amazon Web Services, Inc

- Anysphere, Inc.(Cursor)

- Augment Code

- CodeAnt AI (Qodo)

- Codeium (Exafunction Inc.)

- Cognition AI, Inc (Devin)

- GitHub, Inc. (Microsoft)

- Google (Gemini)

- OpenAI Codex

- TRAE (Tabnine)

Recent Developments

-

In March 2026, Qodo secured $70 million in Series B funding led by Qumra Capital to build AI agents for code review, testing, and governance, helping verify code generated by tools such as GitHub Copilot. Other investors include Maor Ventures, Phoenix Venture Partners, and people from OpenAI and Meta. Companies like Nvidia, Walmart, and Monday.com use Qodo’s platform to assess how code changes affect their systems and ensure compliance with organizational standards.

-

In December 2025, Accenture and Anthropic announced a multi-year partnership expansion that establishes the Accenture Anthropic Business Group, with training provided to approximately 30,000 Accenture professionals on Anthropic's Claude models. The collaboration equips tens of thousands of Accenture developers with Claude Code for enterprise software development tasks.

-

In February 2025, Google launched Gemini Code Assist for individuals, a free AI coding assistant powered by a fine-tuned Gemini 2.0 model variant optimized for coding tasks. The tool integrates with development environments such as VS Code and JetBrains, supporting code completion, chat interactions, bug fixes, and explanations of codebases across multiple programming languages.

AI Code Assistants Market Report Scope

Report Attribute

Details

Market size in 2025

USD 8.5 billion

Estimated market size in 2026

USD 10.3 billion

Projected market size by 2033

USD 42.8 billion

Growth rate

CAGR of 22.5% from 2026 to 2033

Base year for estimation

2025

Actual data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Component, deployment mode, application, end-user, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

Amazon Web Services, Inc.; Anysphere, Inc.(Cursor); Augment Code; CodeAnt AI (Qodo); Codeium (Exafunction Inc.); Cognition AI, Inc (Devin); GitHub, Inc. (Microsoft); Google (Gemini); OpenAI Codex; TRAE (Tabnine)

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global AI Code Assistants Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global AI code assistants market report based on component, deployment mode, application, end-user, and region:

-

Component Outlook (Revenue, USD Million, 2021 - 2033)

-

Software

-

Service

-

-

Deployment Mode Outlook (Revenue, USD Million, 2021 - 2033)

-

Cloud-Based

-

On-Premises

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Code Generation & Autocompletion

-

Code Debugging

-

Test Case Generation & QA Automation

-

Documentation Generation

-

Others

-

-

End-user Outlook (Revenue, USD Million, 2021 - 2033)

-

Large Enterprises

-

SMEs

-

Individual Developers

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

Some key players operating in the AI code assistants market include Amazon Web Services, Inc; Anysphere, Inc.(Cursor); Augment Code; CodeAnt AI (Qodo); Codeium (Exafunction Inc.); Cognition AI, Inc (Devin); GitHub, Inc. (Microsoft); Google (Gemini); OpenAI Codex; TRAE (Tabnine)

Key factors that are driving the market growth include increasingly replacing traditional coding support tools by delivering contextual, real-time recommendations directly within development environments.

Code generation & autocompletion held the largest revenue share in 2025.

Large enterprises segment held the largest revenue share in 2025.

The software segment led with a 78.7% revenue share in 2025.

Cloud-based held the largest share (over 74.1%) in 2025.

The global AI code assistants market size was estimated at USD 8.5 billion in 2025 and is expected to reach USD 10.3 billion in 2026.

The global AI code assistants market is expected to grow at a compound annual growth rate of 22.5% from 2026 to 2033 to reach USD 42.8 billion by 2033.

North America dominated the AI code assistants market with a share of 32.7% in 2025.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.