- Home

- »

- Next Generation Technologies

- »

-

AI Search Engine Market Size, Share, Industry Report, 2033GVR Report cover

![AI Search Engine Market Size, Share & Trends Report]()

AI Search Engine Market (2025 - 2033) Size, Share & Trends Analysis Report By Organization Size (Large Enterprises, SMEs), By Technology, By Deployment (On-premises, Cloud), By End Use, By Region, And Segment Forecasts

Market Size, 2024

$16.3BMarket Estimate, 2026

$18.3BMarket Forecast, 2033

$50.9BCAGR, 2025–2033

13.6%AI Search Engine Market Summary

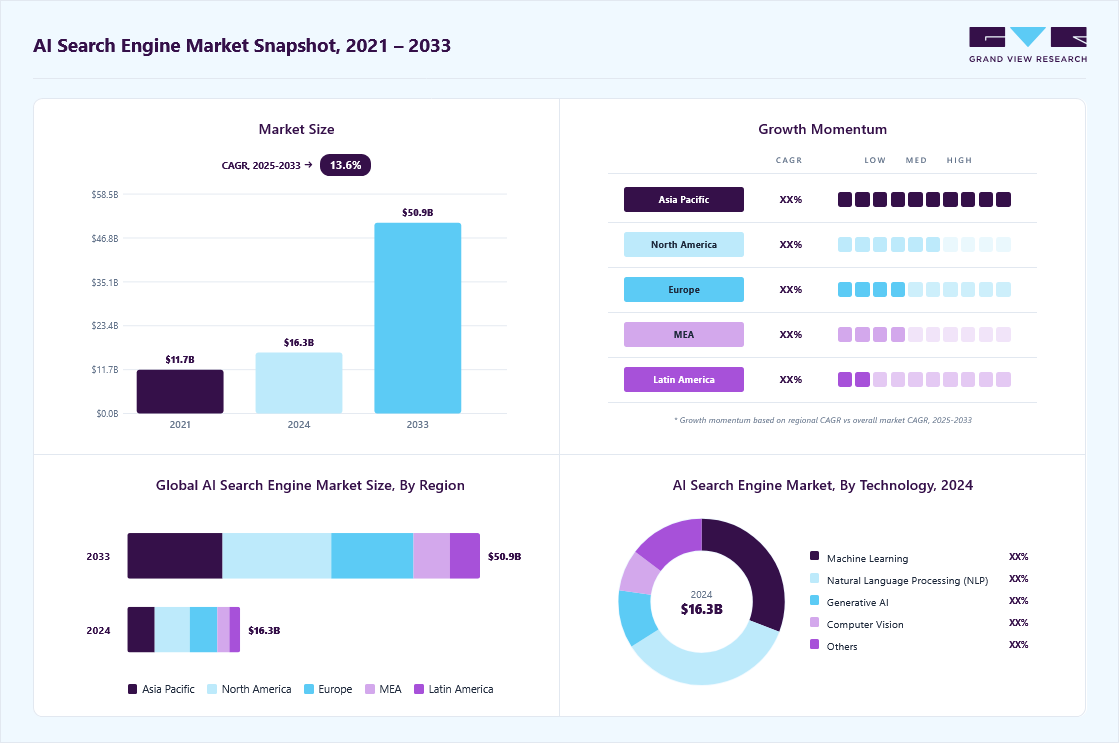

The global AI search engine market size was estimated at USD 16.28 billion in 2024 and is projected to reach USD 50.88 billion by 2033, growing at a CAGR of 13.6% from 2025 to 2033. This growth is driven by rising demand for personalized, context-aware, and generative search experiences that deliver faster, more relevant results, fueled by advancements in natural language processing, machine learning, and growing enterprise adoption for enhanced decision-making.

Key Market Trends & Insights

- North America dominated the global AI search engine market with the largest revenue share of 31.1% in 2024.

- The AI search engine industry in the U.S. led North America in 2024.

- By organization size, the large enterprises segment led with the largest revenue share of 63.1% in 2024.

- By deployment, the cloud segment held the dominant market position in 2024.

- By end use, the retail & e-commerce segment held the dominant market position in 2024.

Market Size & Forecast

- 2024 Market Size: USD 16.28 Billion

- 2033 Projected Market Size: USD 50.88 Billion

- CAGR (2025-2033): 13.6%

- North America: Largest Market in 2024

- Asia Pacific: Fastest Growing Market

The global AI search engine industry’s growth is driven by the explosion in data volume across digital platforms fuels demand for faster, more relevant, and contextually accurate search results. Users and businesses alike seek solutions that move beyond traditional keyword matching to deliver personalized and nuanced responses. Advances in natural language processing and machine learning enable AI search engines to better understand complex user intents and provide more precise results. Furthermore, the widespread adoption of cloud computing offers scalable and cost-effective infrastructure, accelerating market penetration across enterprises of all sizes. The rise of specialized AI search engines tailored for industry-specific needs enhances the market’s diversity, supporting strong current demand.Moreover, continued innovation in natural language processing, including large language models, will deepen the capabilities of AI search engines to handle conversational queries, summarization, and semantic understanding. Integration of AI with other technologies, such as voice assistants and visual search functionalities, expands the market footprint across new applications and user interfaces. Increasing digital transformation across healthcare, finance, and retail sectors drives the need for intelligent search tools capable of managing vast and diverse datasets efficiently. In addition, the growing emphasis on delivering personalized and context-aware experiences encourages the deployment of search algorithms that adapt to individual user behavior and preferences.

")

The AI search engine market also benefits from rising investments in AI research and the increasing adoption of cloud-based AI search solutions that offer flexibility, accessibility, and continuous updates. Expansion into emerging economies within various regions broadens the user base and creates new opportunities for tailored AI search products. At the same time, ongoing focus on addressing ethical considerations, data privacy, and algorithmic fairness shapes development practices, gaining user trust and regulatory compliance. Together, these factors support persistent market expansion and innovation in the AI search engine industry over the coming years.

Organization Size Insights

The large enterprises segment led the AI search engine industry in 2024, with a revenue share of 63.1%. These organizations manage vast and complex databases and multifaceted operational processes that require intelligent automation for data retrieval and knowledge management. Large enterprises benefit from AI search engines that reduce information silos across departments, enable efficient document indexing, and support decision-making through real-time data insights. They often deploy tailored agentic AI solutions integrated with ERP and CRM systems, enhancing workflow automation and regulatory compliance. Furthermore, ongoing investments in digital transformation incentivize enterprises to leverage scalable AI search platforms that adapt to evolving business needs.

The SMEs segment is projected to experience the fastest CAGR in the forecast years as small and medium-sized enterprises increasingly understand the competitive advantages of AI-powered search technologies in streamlining operations and enhancing customer interactions. Affordable cloud-based AI search services allow SMEs to gain access to search capabilities previously limited to large players. These organizations use AI search engines for market research, customer support automation, and knowledge management without heavy IT overhead. In addition, the rise of plug-and-play AI solutions with minimal setup requirements accelerates adoption among SMEs, resulting in improved productivity, better resource utilization, and more agile business models.

Technology Insights

The Natural Language Processing (NLP) segment accounted for the largest revenue share of the AI search engine industry in 2024, driven by enabling AI search engines to interpret user queries with greater contextual understanding and semantic precision. NLP’s ability to handle conversational language, slang, and complex phrase structures improves search relevance across diverse user bases. Industries such as healthcare leverage NLP in clinical data searches, while finance applies it for regulatory document analysis. NLP-driven AI engines also enhance multilingual support, broadening market applicability. The continuous refinement of NLP models through transformer-based architectures and pre-trained language models ensures persistent improvement in understanding nuanced queries and delivering actionable results.

The generative AI segment is expected to grow at the fastest CAGR during the forecast period. It transforms traditional search into interactive experiences by generating original content, summaries, and explanations based on user queries rather than limiting results to existing documents. Generative AI supports dynamic knowledge synthesis, enabling users to obtain concise responses and creative insights through AI assistants and chatbots embedded in search engines. Enterprises utilize generative models for report automation, content creation, and virtual help desks. The versatility of generative AI across both B2B and B2C applications expands functional scope, while continuous advancements in model scaling and fine-tuning drive greater adoption across varied verticals.

Deployment Insights

The cloud segment accounted for the prominent revenue share in 2024, driven by infrastructure supporting rapid scaling, high availability, and seamless integration with existing IT ecosystems. Cloud-hosted AI search platforms facilitate collaborative workflows by enabling multiple users to access and analyze data concurrently from different locations. The pay-as-you-go pricing models make AI search more accessible across industries, supporting dynamic scaling based on demand. Cloud providers increasingly embed AI search capabilities into broader platform services, integrating them with data lakes, analytics tools, and enterprise applications, reinforcing adoption as part of comprehensive digital strategies. Security measures such as encryption and identity management further ensure trust in cloud deployments.

The on-premises segment is anticipated to grow significantly during the forecast period, driven by demand from organizations prioritizing full control over data governance, privacy, and latency-sensitive applications. Sectors including banking and healthcare utilize on-premises AI search infrastructures to comply with strict regulations concerning sensitive information and to shutter external data exposure risks. These deployments allow customization of AI models and integration with legacy systems, supporting unique enterprise needs. On-premises solutions also address connectivity challenges in remote or highly secured environments, ensuring uninterrupted performance. Hybrid architectures combining on-premises control with cloud scalability complement diverse organizational requirements, contributing to segment growth.

End Use Insights

The retail & e-commerce segment accounted for the largest revenue share of the AI search engine market in 2024, due to the sector’s reliance on personalized and efficient product discovery experiences. AI-powered search engines enhance customer engagement by delivering highly relevant, context-aware search results tailored to individual preferences and browsing behaviors. The growth of online shopping and increasing competition push retailers to adopt advanced AI search technologies that improve conversion rates, streamline inventory management, and optimize merchandising strategies. Additionally, integration of AI with voice and visual search capabilities provides shoppers with convenient, intuitive ways to find products, boosting sales and customer satisfaction in the retail and e-commerce landscape.

The media & entertainment segment is anticipated to grow at the fastest CAGR during the forecast period due to increased demand for real-time content adaptation, audience targeting, and interactive search experiences powered by generative AI and NLP. As consumers engage with immersive content across devices, AI search engines enable dynamic subtitle generation, content summarization, and multilingual support. The industry’s pivot toward personalized advertising campaigns and user-generated content growth further stimulates AI-driven search innovation. Integration of AI search with Augmented Reality (AR) and Virtual Reality (VR) enhances interactive entertainment experiences, while platforms continuously refine AI algorithms to deliver seamless, engaging content discovery.

Regional Insights

North America dominated the AI search engine market with a revenue share of 31.1% in 2024, owing to a well-established technology ecosystem, large-scale enterprise adoption, and strong investments in AI research. The region benefits from prominent AI research institutions, tech startups, and established enterprises collaborating to develop cutting-edge AI capabilities. Advanced digital infrastructure supports extensive data collection and processing, enabling AI search applications. Regulatory environments across North America balance innovation with data privacy, encouraging responsible AI deployment.

U.S. AI Search Engine Market Trends

The U.S. AI search engine industry is expected to grow significantly in 2024, driven by a blend of innovation hubs, venture capital investment, and active government initiatives promoting AI adoption across sectors. Its diverse economy drives the adoption of AI search engines in technology, finance, healthcare, and retail, where managing complex data landscapes is paramount. Federal programs emphasize AI development for national competitiveness, cybersecurity, and public services modernization, increasing demand for advanced search platforms.

Europe AI Search Engine Market Trends

The AI search engine industry in Europe is expected to grow significantly over the forecast period, driven by comprehensive regulatory frameworks such as GDPR that require organizations to implement AI systems ensuring data privacy, transparency, and user consent management. European enterprises prioritize AI search platforms that balance innovation with compliance, particularly in sectors such as finance, healthcare, and manufacturing. Cross-border digital services and collaborative innovation projects funded by EU programs accelerate the adoption of advanced AI search tools.

Asia Pacific AI Search Engine Market Trends

The AI search engine industry in the Asia Pacific region is anticipated to grow at the fastest CAGR over the forecast period, driven by rapid digitalization, expanding internet penetration, and increasing enterprise digitization across emerging and developed economies. Governments promote AI-driven innovation and smart city initiatives that include intelligent search applications for public services, healthcare, and finance. The growing e-commerce sector uses AI search to enhance customer experiences and operational efficiency. Asia Pacific’s diverse market includes a vibrant ecosystem of startups and multinational corporations collaborating to develop locally optimized AI search technologies.

Key AI Search Engine Company Insights

Some key companies in the AI search engine industry are SAP SE; Amazon Web Services, Inc.; Salesforce, Inc., and Google LLC.

-

Amazon Web Services, Inc. is a cloud services provider offering a broad portfolio of AI-powered search and machine learning tools that empower enterprises to build intelligent search engines. It incorporates advanced AI technologies, including natural language processing, machine learning, and agentic AI capabilities through services such as Amazon Kendra, which delivers highly accurate, context-aware enterprise search solutions. It continuously innovates with offerings such as Amazon Bedrock AgentCore that enable scalable deployment and secure operation of autonomous AI agents.

-

Google LLC drives innovation in the AI search engine market through its advanced AI platforms and large language models integrated into its core search technologies. Leveraging cutting-edge natural language understanding, generative AI, and machine learning, Google LLC enhances search relevance, personalization, and conversational abilities across web and enterprise contexts. Google LLC’s AI research fuels the development of interactive search features and AI assistants, enabling users to interact naturally and receive precise, synthesized information.

Key AI Search Engine Companies:

The following are the leading companies in the AI search engine market. These companies collectively hold the largest market share and dictate industry trends.

- SAP SE

- Amazon Web Services, Inc.

- Salesforce, Inc.

- Google LLC

- IBM Corporation

- Zeta Global Corp.

- Adobe

- Microsoft

- NVIDIA Corporation

- Oracle

Recent Developments

-

In July 2025, Google LLC launched a new AI-powered search tool called "AI Mode" in the UK, marking a significant transformation of its traditional search engine. Unlike the conventional search results page that displays a list of blue links to websites, AI Mode delivers answers in a conversational style, synthesizing information from multiple sources into a single, coherent response with fewer links to external pages. Built on Google LLC's advanced Gemini 2.5 AI model, this feature supports complex, multi-part queries, allowing users to engage in a more natural and interactive search experience, including follow-up questions that retain contextual understanding.

-

In March 2025, One 97 Communications Limited announced a strategic partnership with Perplexity AI, Inc., an AI-driven answer engine, to integrate advanced AI-powered search capabilities into the Paytm app. This collaboration is designed to enhance digital accessibility and financial literacy by enabling users to ask questions, explore diverse topics in multiple local languages, and make well-informed financial decisions with real-time, trusted insights. Leveraging Perplexity AI, Inc.’s AI technology, One 97 Communications Limited aims to provide millions of users with seamless access to accurate financial information, facilitating smarter and more inclusive digital financial services across India.

-

In October 2024, Meta Platforms Inc. undertook development of an artificial intelligence-based search engine to reduce its reliance on Google LLC and Microsoft's Bing. This initiative involves creating a dedicated web crawler to independently index information for its AI chatbot, Meta AI, which is integrated across platforms such as Facebook, Instagram, WhatsApp, and Messenger. The new search engine is designed to provide users with conversational answers about current events and other topics, enhancing the chatbot’s ability to deliver real-time, accurate information without depending on external search providers.

AI Search Engine Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 18.28 billion

Revenue forecast in 2033

USD 50.88 billion

Growth rate

CAGR of 13.6% from 2025 to 2033

Actual data

2021 - 2023

Forecast period

2025 - 2033

Quantitative units

Revenue in USD billion/million and CAGR from 2025 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Deployment, end use, organization size, technology, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; India; Japan; Australia; South Korea; Brazil; UAE; South Africa; KSA

Key companies profiled

SAP SE; Amazon Web Services, Inc.; Salesforce, Inc.; Google LLC; IBM Corporation; Zeta Global Corp.; Adobe; Microsoft; NVIDIA Corporation; Oracle

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global AI Search Engine Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global AI search engine market report based on organization size, technology, deployment, end use, and region:

-

Organization Size Outlook (Revenue, USD Million, 2021 - 2033)

-

Large Enterprises

-

SMEs

-

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Machine Learning

-

Natural Language Processing (NLP)

-

Generative AI

-

Computer Vision

-

Other

-

-

Deployment Outlook (Revenue, USD Million, 2021 - 2033)

-

On-premises

-

Cloud

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

BFSI

-

Media & Entertainment

-

Healthcare

-

IT & Telecom

-

Retail & E-commerce

-

Travel & Hospitality

-

Manufacturing

-

Education

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

UAE

-

KSA

-

South Africa

-

-

Frequently Asked Questions About This Report

The global AI search engine market size was estimated at USD 16.28 billion in 2024 and is expected to reach USD 18.28 billion in 2025.

The global AI search engine market is expected to grow at a compound annual growth rate of 13.6% from 2025 to 2033 to reach USD 50.88 billion by 2033.

North America dominated the AI search engine market with a share of 31.1% in 2024. This is attributable to the well-established technology ecosystem, large-scale enterprise adoption, and strong investments in AI research. The region benefits from prominent AI research institutions, tech startups, and established enterprises collaborating to develop cutting-edge AI capabilities.

Some key players operating in the AI search engine market include SAP SE; Amazon Web Services, Inc.; Salesforce, Inc.; Google LLC; IBM Corporation; Zeta Global Corp.; Adobe; Microsoft; NVIDIA Corporation; and Oracle.

Key factors that are driving the AI search engine market growth include the rising demand for personalized, context-aware, and generative search experiences that deliver faster, more relevant results, fueled by advancements in natural language processing, machine learning, and growing enterprise adoption for enhanced decision-making.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.