- Home

- »

- Next Generation Technologies

- »

-

AI server Market Size, Growth Report, 2026-2033GVR Report cover

![AI Server Market (2026 - 2033)Report]()

AI Server Market (2026 - 2033)

Size, Share, & Trends Analysis Report By Processor (GPU-based Servers, FPGA-based Servers), By Cooling Technology (Air Cooling, Liquid Cooling), By Form Factor, By End Use (BFSI, Automotive), By Region, And Segment Forecasts

Market Size, 2025

$131.7BMarket Estimate, 2026

$157.0BMarket Forecast, 2033

$598.1BCAGR, 2026–2033

21.2%AI Server Market Summary

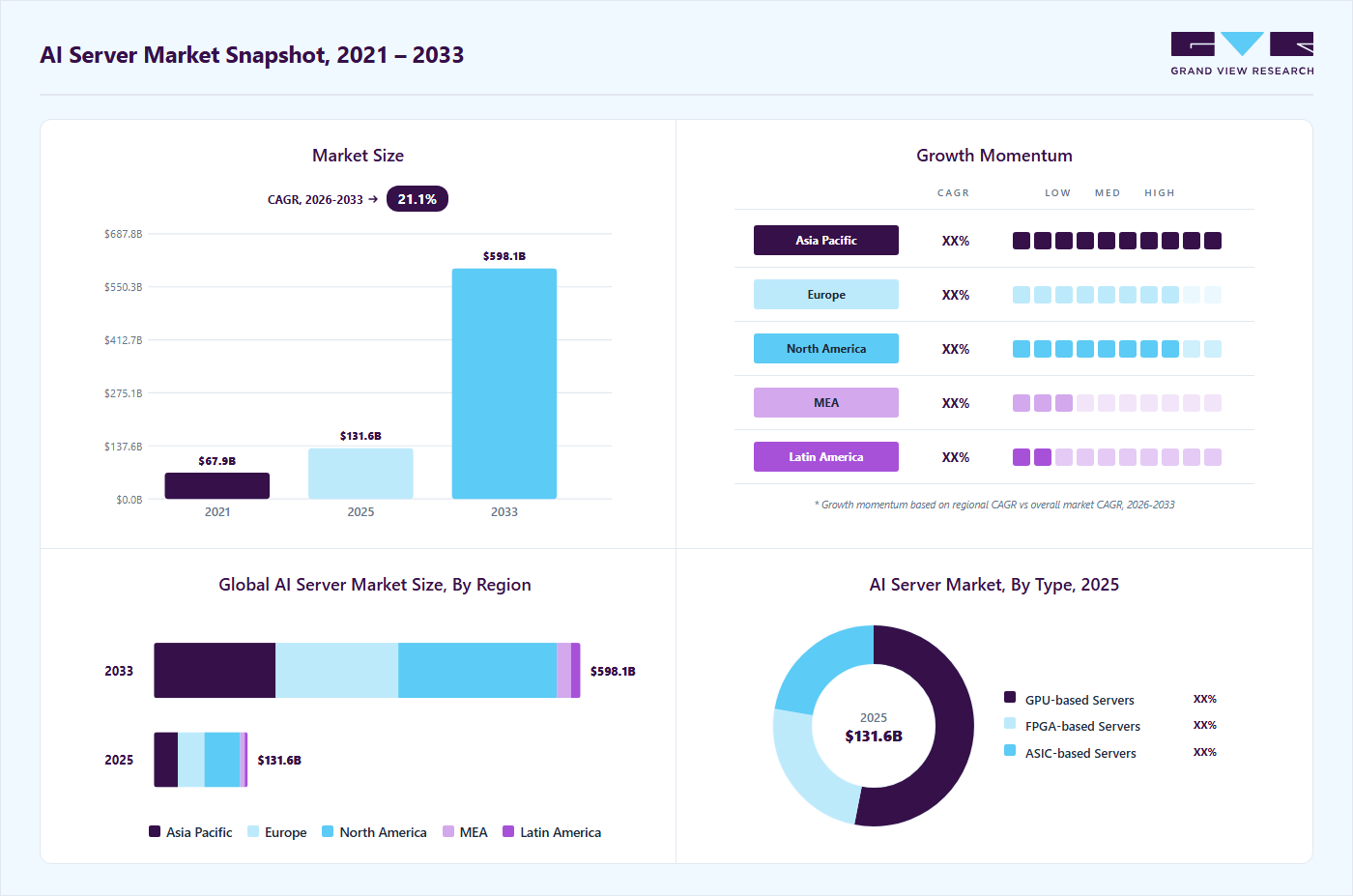

The global AI server market size was valued at USD 131.7 billion in 2025 and is projected to grow from USD 157.0 billion in 2026 to USD 598.1 billion by 2033, at a CAGR of 21.2% from 2026 to 2033. North America dominated the global market, accounting for the largest revenue share of 38.2% in 2025.. Cloud computing and hyperscale data center expansion are driving the market growth.

Key Market Trends & Insights

- By processor: GPU-based servers segment held the largest revenue share of 53.0% in 2025.

- By cooling technology: Air-cooling segment held the largest revenue share in 2025.

Regional Highlights

- Largest regional market: North America (38.2% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. AI server industry is a major contributor to the global market.

Market Size & Forecast

- Market size in 2025: USD 131.7 Billion

- Estimated market size in 2026: USD 157.0 Billion

- Projected market size by 2033: USD 598.1 Billion

- CAGR (2026-2033): 21.2%

Major cloud service providers are investing heavily in AI-optimized server infrastructure to cater to the growing number of enterprises seeking AI-as-a-service solutions. These deployments often involve custom server architectures, which allow for better energy efficiency and computational throughput. Moreover, as organizations shift toward hybrid and multi-cloud strategies, the need for scalable, AI-optimized server systems within data centers becomes even more critical, supporting both centralized training and edge inferencing scenarios.

")

The rapid adoption of generative AI applications across various industries is driving market growth, with leading infrastructure providers such as the Supermicro AI server market ecosystem playing a key role in supplying high-performance, GPU-optimized server systems designed for AI workloads. From content creation and customer service automation to personalized marketing and drug discovery, generative AI is pushing the boundaries of compute-intensive operations. These applications require highly specialized server architectures capable of supporting massive parallelism and fast data throughput. The surge in demand for generative models like GPT and DALL·E is compelling enterprises and cloud providers to invest heavily in AI servers that can manage such computational intensity with speed and reliability.

The rise of hybrid and multi-cloud strategies is also accelerating the deployment of AI servers. Enterprises are opting for flexible infrastructure models that allow seamless integration between on-premises systems and public cloud platforms. Artificial intelligence (AI) servers designed for hybrid deployments must be highly adaptable, scalable, and secure to ensure smooth data mobility and unified AI workloads across diverse environments. This flexibility is crucial for organizations looking to optimize cost efficiency, performance, and regulatory compliance when deploying AI solutions on a scale.

Cybersecurity and data privacy concerns are further fueling the need for on-premises AI servers. As organizations become increasingly reliant on AI for handling sensitive information such as biometric data, financial records, and proprietary business intelligence, there is growing reluctance to process such data in public cloud environments. On-premise AI servers offer the control and security needed to meet strict compliance standards such as GDPR, HIPAA, and PCI-DSS, making them indispensable for industries such as healthcare, finance, and defense.

Moreover, the growth of AI chipsets and system-on-chip (SoC) technologies is transforming the design and capabilities of AI servers. Innovations in AI-specific hardware are leading to more compact, energy-efficient servers that can deliver unprecedented levels of performance. These new designs enable edge computing capabilities without compromising on processing power, and they open up possibilities for AI deployment in environments previously deemed impractical such as mobile units, remote locations, or disaster recovery sites. The continuous advancement of AI hardware is thus a foundational driver pushing the server market forward.

Processor Insights

The GPU-based servers segment accounted for the largest market share of over 53.0% in 2025. The rise of large language models (LLMs) and generative AI systems is driving the segment growth. Models like GPT, BERT, and DALL·E depend on high throughput and low latency during training and deployment, both of which are efficiently addressed by advanced GPU architectures such as NVIDIA’s A100 and H100. As enterprises integrate these models into customer service, content creation, and predictive analytics, demand for GPU-based servers has surged, especially among cloud providers and data-intensive industries.

The ASIC-based servers segment is anticipated to grow at the fastest CAGR during the forecast period. The increasing demand for energy-efficient computing is a major driver for ASIC adoption in the market. As AI workloads scale, so too does the energy requirement to process massive datasets and complex models. ASICs, by design, consume significantly less power than their GPU or CPU counterparts for equivalent workloads. This makes them an ideal solution for data centers and enterprises focused on reducing operational costs and meeting sustainability goals. With hyperscale data centers under pressure to optimize performance per watt, ASIC-based servers are increasingly favored in large AI deployments.

Cooling Technology Insights

The air cooling segment dominated the market and accounted for a revenue share in 2025. The rising number of edge AI applications is also boosting demand for air-cooled systems. Many edge data centers or modular deployments operate in environments where liquid cooling infrastructure is impractical or unavailable. Air cooling solutions, with their simpler installation and operational flexibility, are better suited for such distributed setups. As AI becomes more pervasive across smart cities, autonomous systems, and industrial automation, compact and efficient air-cooled servers are increasingly being deployed at the edge to enable real-time processing and decision-making.

The hybrid cooling segment is expected to register a significant CAGR from 2026 to 2033. The advancement of high-performance AI chips, including GPUs and custom ASICs, is pushing thermal management to new frontiers. These chips generate concentrated heat loads that exceed the limits of conventional cooling systems. Hybrid solutions, which integrate direct-to-chip liquid cooling with ambient air handling, offer a robust response to this challenge. They ensure the stable operation of high-density AI clusters, preventing thermal throttling and maximizing the chips' computational throughput. This is a critical factor for real-time analytics, machine learning training, and complex simulations.

Form Factor Insights

The rack-mounted servers segment dominated the market and accounted for a revenue share in 2025. The growing emphasis on modular and space-efficient data center architectures is a key factor fueling the demand for rack-mounted AI servers. As AI adoption spreads across industries, data centers are being designed or retrofitted to support higher-density computing without expanding physical space. Rack-mounted servers allow for efficient stacking and cable management, which not only simplifies deployment but also optimizes airflow and power consumption. These characteristics make them a preferred choice for enterprises looking to enhance their AI capabilities while maintaining operational efficiency and cost-effectiveness.

The blade servers segment is expected to register the fastest CAGR from 2026 to 2033. The rise in the adoption of converged and hyper-converged infrastructure in support of AI initiatives is promoting the use of blade servers. Their integration into such architectures allows for centralized control and streamlined deployment of resources, which helps in optimizing performance across compute, storage, and networking components. Enterprises looking to implement AI-driven analytics or intelligent automation in a simplified, cohesive environment are increasingly turning to blade server solutions to meet these needs. This is particularly relevant in sectors like manufacturing and telecommunications, where large-scale data processing and analysis are fundamental to operational advancement.

End Use Insights

The IT & telecommunication segment accounted for the largest market share in 2025. The shift towards edge computing is driving the adoption of AI servers in the IT & telecommunications segment. As networks evolve to support IoT devices and real-time services such as augmented reality (AR), virtual reality (VR), and autonomous vehicle communication, telecom companies require AI servers at the edge to ensure immediate data processing and minimal latency. This shift is critical to support next-generation services and reduce the burden on central data centers. AI servers, especially those designed for edge deployments, are becoming essential to telecom providers aiming to deliver seamless, intelligent connectivity to customers and businesses alike.

The retail & e-commerce segment is anticipated to register a substantial CAGR during the forecast period. The need for fraud detection and cybersecurity has prompted e-commerce platforms to deploy AI algorithms capable of identifying and mitigating threats in real-time. These advanced threat detection systems run best on specialized AI servers that can handle rapid data processing and analysis. As cyber threats become more sophisticated, the demand for secure and responsive infrastructure increases accordingly.

Regional Insights

North America AI Server Market Trends

North America AI server industry dominated the market and held the major share of over 38.2% in 2025. The surge in data generation from connected devices, enterprise applications, and digital services is creating an unprecedented need for powerful data processing capabilities. AI servers, especially those equipped with GPUs and other specialized hardware, are being deployed in data centers across North America to manage this growing data deluge. The region’s advanced cloud ecosystem further boosts demand as cloud providers increasingly offer AI as a service, which relies on the deployment of high-capacity AI servers.

U.S. AI Server Market Trends

The U.S. AI server industry is projected to grow during the forecast period. The U.S. market benefits from a robust ecosystem of semiconductor and server hardware providers. Companies such as NVIDIA, AMD, Intel, and emerging AI chip startups such as Cerebras and Groq are introducing innovative processors optimized for AI workloads. The availability of cutting-edge components domestically reduces supply chain friction and encourages wider adoption of AI servers across industries. These advances also allow for greater customization and scalability, which is particularly valuable for enterprises building AI capabilities tailored to niche applications or verticals.

Europe AI Server Market Trends

The AI server industry in Europe is expected to grow at a CAGR from 2026 to 2033. Europe's automotive industry, especially in Germany and France, is a major contributor to the market growth. The development of autonomous driving systems and smart mobility solutions requires immense computational power, typically delivered by high-performance AI servers. As these technologies progress from pilot phases to real-world deployment, the infrastructure to support real-time data processing and AI model training is expanding rapidly, driving investment in both centralized and edge-based AI server installations.

The AI server industry in Germany is growing during the forecast period. Germany’s emphasis on data protection and digital sovereignty further contributes to the growth of the domestic AI server industry. With strict enforcement of the General Data Protection Regulation (GDPR), organizations are prioritizing in-country data processing and storage. This necessitates local deployment of AI infrastructure, including servers capable of handling complex analytics and machine learning workloads while maintaining compliance. As organizations seek to keep sensitive data within national borders, demand for AI servers hosted in German facilities is on the rise.

Asia Pacific AI Server Market Trends

The demand for AI servers in the Asia Pacific is expected to be the fastest growing and is anticipated to register a lucrative CAGR from 2026 to 2033. The region’s fast-growing e-commerce and digital entertainment industries are driving the need for AI-enhanced customer experiences. Online retail platforms in the Asia Pacific markets use AI servers to support recommendation engines, fraud detection systems, inventory management, and demand forecasting. Meanwhile, streaming services rely on AI for content personalization, language translation, and network optimization. As user bases grow and data volumes increase exponentially, these industries are scaling up their AI server capacities to ensure seamless and intelligent services, contributing steadily to market expansion.

The AI server industry in China is projected to grow during the forecast period. China’s expanding digital economy, particularly in sectors such as e-commerce, fintech, and online entertainment, is also fueling AI server adoption. E-commerce platforms such as JD.com and Alibaba utilize AI servers to optimize logistics, manage dynamic pricing, and personalize user experiences. Similarly, fintech firms deploy AI for fraud detection, credit scoring, and intelligent customer support. Video streaming services use AI for content curation and real-time translation, which are computationally intensive and rely on high-throughput AI servers to ensure low latency and high availability.

Key AI Server Company Insights

Some of the key companies operating in the market, such as Dell Inc. and IBM Corporation, among others, are some of the leading participants in the AI server industry.

Key AI Server Companies:

The following key companies have been profiled for this study on the AI server market.

- Dell Inc.

- Cisco Systems, Inc.

- IBM Corporation

- HP Development Company, L.P.

- Huawei Technologies Co., Ltd.

- Nvidia Corporation

- Fujitsu Limited

- ADLINK Technology Inc.

- Lenovo Group Limited

- Super Micro Computer, Inc.

Recent Developments

-

In May 2025, Dell Inc. launched new servers powered by Nvidia's Blackwell Ultra chips to meet growing AI demand. The servers are offered in air- and liquid-cooled versions. They support up to 192 chips by default, with customization up to 256, enabling AI model training up to four times faster than before.

-

In May 2025, NVIDIA Corporation launched the DGX Spark and DGX Station systems. These systems feature ConnectX-8 SuperNIC, which delivers networking speeds of up to 800 Gb/s, enabling high speed connectivity and scalable performance. The DGX Station can function either as a powerful desktop workstation for a single user running complex AI models with local data or as a centralized compute resource accessible on demand by multiple users. It also supports NVIDIA Multi-Instance GPU (MIG) technology, allowing the GPU to be partitioned into up to seven instances, each equipped with dedicated high-bandwidth memory, cache, and compute cores, creating a personal cloud environment ideal for AI development and data science teams.

-

In April 2025, Fujitsu Limited partnered with Supermicro Inc. and Nidec Corporation to enhance data center energy efficiency. They are integrating Fujitsu’s liquid-cooling software, Supermicro’s high-performance GPU servers, and Nidec’s efficient liquid-cooling system to create AI server systems optimized for liquid cooling. This approach eliminates air cooling fans, cuts server power consumption, lowers noise, and reduces operating temperatures, boosting overall data center power usage effectiveness (PUE).

AI Server Market Report Scope

Report Attribute

Details

Market size in 2025

USD 131.7 billion

Market size value in 2026

USD 157.0 billion

Revenue forecast in 2033

USD 598.1 billion

Growth rate

CAGR of 21.2% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Processor, cooling technology, form factor, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Dell Inc.; Cisco Systems, Inc.; IBM Corporation; HP Development Company, L.P.; Huawei Technologies Co., Ltd.; NVIDIA Corporation; Fujitsu Limited; ADLINK Technology Inc.; Lenovo Group Limited; Super Micro Computer, Inc.; and Others

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global AI Server Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the AI server market report based on processor, cooling technology, form factor, end use, and region:

-

Processor Outlook (Revenue, USD Billion, 2021 - 2033)

-

GPU-based Servers

-

FPGA-based Servers

-

ASIC-based Servers

-

-

Cooling Technology Outlook (Revenue, USD Billion, 2021 - 2033)

-

Air Cooling

-

Liquid Cooling

-

Hybrid Cooling

-

-

Form Factor Outlook (Revenue, USD Billion, 2021 - 2033)

-

Rack-mounted Servers

-

Blade Servers

-

Tower Servers

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

IT & Telecommunication

-

BFSI

-

Retail & E-commerce

-

Healthcare & Pharmaceutical

-

Automotive

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

North America dominated with a 38.2% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The rack-mounted servers segment held the largest revenue share in 2025, while blade servers is the fastest-growing factor.

The air cooling segment accounted for the largest revenue share in 2025.

The IT & telecommunication segment held the largest revenue share in 2025.

The global AI server market size was valued at USD 131.7 billion in 2025 and is estimated at USD 157.0 billion for 2026.

The global AI server market is expected to grow at a CAGR of 21.2% from 2026 to 2033, reaching USD 598.1 billion by 2033.

The GPU-based servers segment accounted for the largest market share of over 53.0% in 2025 in the AI server market. The rise of large language models (LLMs) and generative AI systems is driving the segment growth in the AI server market. Models like GPT, BERT, and DALL·E depend on high throughput and low latency during training and deployment, both of which are efficiently addressed by advanced GPU architectures such as NVIDIA’s A100 and H100.

Key players include Dell Inc.; Cisco Systems, Inc.; IBM Corporation; HP Development Company, L.P.; Huawei Technologies Co., Ltd.; NVIDIA Corporation; Fujitsu Limited; ADLINK Technology Inc.; Lenovo Group Limited; Super Micro Computer, Inc.; and Others.

Factors such as growing cloud computing and hyperscale data center expansion, along with increasing investment in AI-optimized server infrastructure to cater to the growing number of enterprises seeking AI-as-a-service solutions, are driving the growth of the AI server market.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.