- Home

- »

- Next Generation Technologies

- »

-

AI Supercomputing Platforms Market Size Report, 2026-2033GVR Report cover

![AI Supercomputing Platforms Market (2026 - 2033)Report]()

AI Supercomputing Platforms Market (2026 - 2033)

Size, Share & Trends Analysis Report By Offering (Hardware, Software, Services), Application (Generative AI, Computer Vision), Deployment Mode, Component, End Use, By Region, And Segment Forecasts

Market Size, 2025

$3.5BMarket Estimate, 2026

$4.3BMarket Forecast, 2033

$20.1BCAGR, 2026–2033

24.7%AI Supercomputing Platforms Market Summary

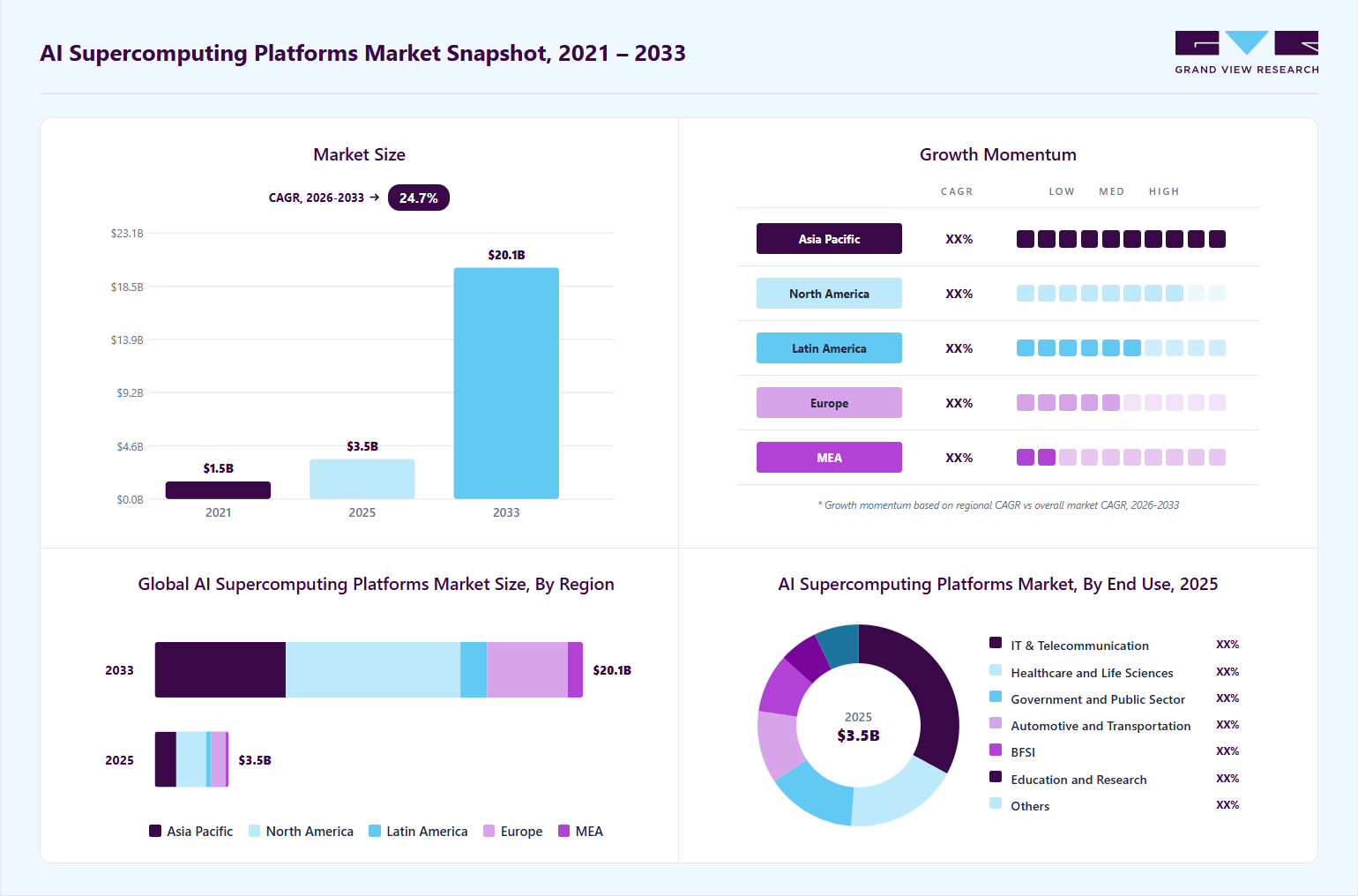

The global AI supercomputing platforms market size was valued at USD 3.5 billion in 2025 and is projected to grow from USD 4.3 billion in 2026 to USD 20.1 billion by 2033, at a CAGR of 24.7% from 2026 to 2033. The market in North America dominated with a revenue share of 40.5% in 2025. The industry is experiencing robust growth, driven by the escalating demand for high-performance computing infrastructure capable of training and deploying large-scale artificial intelligence models.

Key Market Trends & Insights

- By offering: Hardware segment held the largest market share of 71.0% in 2025.

- By application: Large language model (LLM) segment held the largest market share of 30.0% in 2025.

- By deployment mode: On-premises segment held the largest market share of 57.0% in 2025.

- By component: Compute systems segment held the largest market share of 33.0% in 2025.

- By end use: IT & telecommunication segment held the largest market share of 32.0% in 2025.

Regional Highlights

- Largest regional market: North America (40.5% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 3.5 Billion

- Estimated market size in 2026: USD 4.3 Billion

- Projected market size by 2033: USD 20.1 Billion

- CAGR (2026-2033): 24.7%

As enterprises, research institutions, hyperscale cloud providers, and governments increasingly invest in advanced technologies such as generative AI, large language models (LLMs), deep learning, and scientific simulation, AI supercomputing platforms have become essential for delivering the massive computational power, ultra-fast interconnects, high-bandwidth memory, and scalable storage required to process complex workloads efficiently.")

The demand for AI Supercomputing Platforms is increasing as enterprises, hyperscale cloud providers, research institutions, and governments seek to accelerate artificial intelligence development, scientific discovery, and large-scale data processing across advanced computing environments. Many organizations are increasingly adopting technologies such as generative AI, large language models (LLMs), deep learning, machine learning, high-performance computing (HPC), and accelerated computing to enable large-scale model training, real-time inference, and complex simulation workloads. Additionally, the rapid expansion of AI-optimized data centers, cloud computing platforms, sovereign AI initiatives, and exascale computing programs is driving the need for scalable and high-performance supercomputing platforms that can support massive computational requirements across diverse applications. Furthermore, the expansion of industries such as information technology and telecommunications, healthcare and life sciences, automotive, BFSI, government and public sector, education and research, and manufacturing is accelerating the demand for integrated AI supercomputing platforms featuring advanced GPUs, high-speed interconnects, high-bandwidth memory, and liquid-cooled architectures.

Enterprises, hyperscale cloud providers, research institutions, and government organizations are increasingly prioritizing large-scale artificial intelligence development, advanced scientific computing, and accelerated data processing, which is driving the adoption of AI Supercomputing Platforms across global markets. These platforms enable organizations to process massive datasets, train large language models, and execute complex simulations with exceptional speed and scalability.

Market Dynamics

AI supercomputing platforms are purpose-built systems that combine high-performance GPUs, CPUs, high-bandwidth memory, ultra-fast interconnects, and scalable storage to support large-scale artificial intelligence workloads. The accelerating adoption of generative AI, large language models (LLMs), multimodal AI systems, and advanced scientific simulations is significantly increasing demand for these platforms. Training modern foundation models requires enormous computational resources and highly optimized infrastructure capable of processing vast datasets and coordinating thousands of accelerators simultaneously.

As enterprises, hyperscale cloud providers, research institutions, and government organizations intensify investments in next-generation AI capabilities, AI supercomputing platforms are becoming critical to reducing model development timelines, improving training efficiency, and enabling large-scale deployment of advanced AI applications. These platforms provide tightly integrated compute, networking, storage, and cooling architectures that deliver the performance, scalability, and operational efficiency necessary to support increasingly complex workloads.

Despite their performance advantages, AI supercomputing platforms require substantial upfront investments and specialized infrastructure, which can limit adoption among small and medium-sized organizations. The cost of deploying large GPU clusters, high-speed networking, high-capacity storage, and advanced cooling systems can reach tens or hundreds of millions of dollars, depending on scale. In addition, organizations must invest in data center upgrades, power distribution, and skilled personnel to operate and optimize these systems.

Power consumption is another major consideration, as large AI supercomputing clusters require substantial electrical capacity and advanced thermal management to operate efficiently. Supply constraints for advanced GPUs, high-bandwidth memory, and networking components can also delay deployments and raise procurement costs. Furthermore, integrating hardware, software, and orchestration tools across heterogeneous environments adds technical complexity and may extend implementation timelines.

Governments and enterprises worldwide are investing in sovereign AI capabilities to strengthen technological independence, national security, and domestic innovation. These initiatives are creating substantial opportunities for AI supercomputing platform providers, as countries seek to build localized infrastructure for training national language models, supporting defense research, and accelerating scientific discovery.

Furthermore, the growing emphasis on exascale computing, strategic semiconductor development, and regional data sovereignty is encouraging large-scale investments in advanced AI infrastructure. Countries across North America, Europe, Asia-Pacific, and the Middle East are establishing national AI computing centers and partnering with leading vendors such as NVIDIA Corporation, Hewlett Packard Enterprise (HPE), Dell Technologies, and Intel Corporation to deploy high-performance GPU clusters and liquid-cooled supercomputing systems.

Market Concentration & Characteristics

The industry is moderately fragmented, with a mix of established semiconductor companies, high-performance computing system vendors, enterprise infrastructure providers, and specialized server manufacturers competing across cloud, research, government, and enterprise applications. Leading players such as NVIDIA Corporation, Hewlett Packard Enterprise (HPE), Dell Technologies, Advanced Micro Devices (AMD), and Intel Corporation leverage advanced accelerator technologies, integrated hardware and software ecosystems, and strong global service capabilities to maintain their competitive positions.

The industry faces competition from alternative computing approaches such as conventional high-performance computing (HPC) clusters, general-purpose AI servers, and cloud-based GPU instances that can support artificial intelligence workloads without requiring fully integrated supercomputing platforms. In some applications, organizations may also rely on distributed cloud infrastructure or smaller accelerator clusters that reduce the need for deploying large-scale dedicated AI supercomputing systems.

Offering Insights

The hardware segment dominated the industry, accounting for over 71.0% of the global revenue share in 2025, driven by the increasing deployment of high-performance computing infrastructure required for large-scale artificial intelligence training, inference, and scientific simulation workloads. Hardware components such as GPUs, CPUs, high-bandwidth memory, storage systems, high-speed interconnects, and advanced cooling infrastructure form the core foundation of AI supercomputing platforms, enabling organizations to achieve exceptional computational performance, scalability, and energy efficiency.

The software segment is expected to witness significant growth over the forecast period, driven by the increasing demand for advanced tools that enable efficient orchestration, optimization, and management of large-scale AI and high-performance computing workloads. Software components such as AI frameworks, cluster management platforms, resource schedulers, performance monitoring tools, and security solutions are essential for maximizing hardware utilization, streamlining model development, and ensuring reliable operation of complex supercomputing environments.

Application Insights

The Large Language Model (LLM) Training segment dominated the industry, accounting for over 30.0% of the global revenue share in 2025, driven by the rapidly increasing demand for large-scale foundation models capable of powering generative AI, conversational AI, code generation, and advanced reasoning applications. Training these models requires massive computational resources, including thousands of high-performance GPUs, high-bandwidth memory, ultra-fast interconnects, and scalable storage systems, making AI supercomputing platforms essential for delivering the performance and efficiency needed to process trillions of parameters and vast datasets.

The Generative AI segment is expected to witness significant growth over the forecast period, driven by the rapid adoption of AI technologies capable of generating text, images, videos, code, and multimodal content across enterprise and consumer applications. Generative AI workloads require enormous computational resources for model training, fine-tuning, and inference, including high-performance GPUs, high-bandwidth memory, ultra-fast networking, and scalable storage infrastructure, making AI supercomputing platforms essential for supporting these compute-intensive processes.

Component Insights

The compute systems segment dominated the industry, accounting for over 33.0% of the global revenue share in 2025, driven by the increasing demand for high-performance server architectures that form the foundational building blocks of large-scale AI and high-performance computing environments. Compute systems integrate advanced processors, accelerator-ready server nodes, memory subsystems, and system management capabilities to deliver the computational capacity required for large language model training, generative AI, scientific simulations, and data-intensive analytics.

The storage systems segment is expected to witness significant growth over the forecast period, driven by the increasing need to store, manage, and rapidly access massive volumes of structured and unstructured data used for large language model training, generative AI, and scientific computing workloads. AI supercomputing platforms rely on high-performance storage architectures, including parallel file systems, NVMe-based storage arrays, and distributed storage solutions, to deliver the throughput and low latency required for data-intensive applications.

Deployment Mode Insights

The on-premises segment dominated the industry, accounting for over 57.0% of the global revenue share in 2025, driven by the increasing deployment of dedicated high-performance computing infrastructure by enterprises, hyperscale cloud providers, research institutions, and government organizations. On-premises deployment provides organizations with greater control over data security, system configuration, workload optimization, and regulatory compliance, which is critical for training large language models, running sensitive simulations, and supporting sovereign AI initiatives.

The cloud-based segment is expected to witness substantial growth over the forecast period, driven by the increasing availability of on-demand access to high-performance GPU clusters and AI-optimized infrastructure through cloud service providers. Cloud-based deployment offers organizations enhanced scalability, flexibility, and cost efficiency by enabling them to access advanced computing resources without significant upfront capital investments.

End Use Insights

The IT & Telecommunication segment dominated the industry, accounting for over 32.0% of the global revenue share in 2025, driven by the increasing demand for large-scale AI model training, cloud-based AI services, and data-intensive network optimization applications. Technology companies and telecommunications providers are investing heavily in AI supercomputing platforms to support generative AI, large language models, intelligent network management, cybersecurity analytics, and real-time data processing across hyperscale data centers and distributed infrastructure

The BFSI segment is expected to witness significant growth over the forecast period, driven by the increasing adoption of artificial intelligence for fraud detection, algorithmic trading, credit risk modeling, customer analytics, and regulatory compliance. Banks, financial institutions, and insurance companies are leveraging AI supercomputing platforms to process massive volumes of transactional and customer data, train sophisticated machine learning models, and perform real-time analytics with high accuracy and speed.

Regional Insights

North America AI supercomputing platforms market led in 2025, accounting for over 40.0% of the global revenue share. The industry is driven by the strong presence of leading technology companies, advanced semiconductor manufacturers, and hyperscale cloud providers across the region. The market benefits from substantial investments in artificial intelligence, high-performance computing, data center infrastructure, and accelerated computing platforms. Organizations throughout the region are early adopters of generative AI, large language models, and exascale computing systems, which require large-scale AI supercomputing platforms for model training, inference, and scientific research.

U.S. AI Supercomputing Platforms Market Trends

The AI supercomputing platforms market in the U.S. dominates North America due to the strong presence of leading artificial intelligence, semiconductor, and cloud computing companies, along with substantial investments in advanced computing infrastructure and AI research and development. The country has a highly developed data center ecosystem and is home to major hyperscale cloud providers, research institutions, and government laboratories that are actively deploying AI supercomputing platforms to support generative AI, large language models, scientific simulations, and defense applications. Increasing investments in sovereign AI initiatives, exascale computing programs, and next-generation GPU clusters are further accelerating market growth.

Europe AI Supercomputing Platforms Market Trends

The AI supercomputing platforms market in Europe is witnessing significant growth due to increasing investments in artificial intelligence, high-performance computing, and sovereign digital infrastructure across the region. Governments, research institutions, and enterprises are accelerating the deployment of AI supercomputing platforms to support generative AI, large language models, scientific research, and industrial innovation.

Asia Pacific AI Supercomputing Platforms Market Trends

The AI supercomputing platforms market in Asia-Pacific is witnessing significant growth due to the rapid expansion of artificial intelligence initiatives, hyperscale data centers, and high-performance computing infrastructure across emerging and developed economies such as China, Japan, India, and South Korea. Increasing government support for sovereign AI, growing investments in semiconductor manufacturing, and rising demand for generative AI and large language model training are accelerating the deployment of AI supercomputing platforms throughout the region.

Key AI Supercomputing Platforms Companies Insights

The AI supercomputing platforms market features several key players that significantly shape its global landscape through advanced accelerated computing technologies, high-performance computing systems, and integrated AI infrastructure solutions. NVIDIA Corporation is a prominent provider of AI supercomputing platforms, widely recognized for its GPU-accelerated systems such as DGX SuperPOD and advanced networking technologies that enable organizations to train large language models, deploy generative AI applications, and execute complex scientific simulations. The company’s strong presence in accelerated computing, AI software, and high-speed interconnect solutions supports scalable and energy-efficient AI infrastructure across industries such as healthcare, automotive, research, and cloud computing.

-

NVIDIA Corporation is a prominent player delivering integrated AI supercomputing platforms, including DGX systems, DGX SuperPOD, InfiniBand networking, and CUDA software. The company supports enterprises, hyperscale cloud providers, and research institutions by enabling large-scale AI model training, inference, and scientific computing with industry-leading performance, scalability, and energy efficiency.

-

Hewlett Packard Enterprise (HPE) provides advanced AI supercomputing and high-performance computing systems through its Cray EX platform and liquid-cooled infrastructure solutions. The company enables government laboratories, universities, and enterprises to deploy exascale-class computing environments for generative AI, large language models, and complex simulation workloads.

Key AI Supercomputing Platforms Companies:

The following key companies have been profiled for this study on the AI supercomputing platforms market.

- Dell Technologies

- Advanced Micro Devices (AMD)

- Intel Corporation

- International Business Machines (IBM)

- Lenovo Group Limited

- Super Micro Computer, Inc.

- Atos SE (Eviden)

- Fujitsu Limited

Recent Development

-

In April 2026, Dell Technologies secured a major deployment win for its Pangea 5 AI infrastructure platform, highlighting the company’s growing presence in the AI Supercomputing Platforms Market. The contract underscores increasing demand for integrated high-performance computing systems that combine advanced GPU clusters, high-speed networking, scalable storage, and liquid-cooled architectures to support large language model training and generative AI workloads.

-

In May 2026, Intel Corporation highlighted its expanding AI compute ecosystem at Computex 2026, showcasing advancements spanning AI PCs, edge computing, data centers, and cloud infrastructure. The company emphasized its open-platform strategy and ongoing innovation in processors, AI accelerators, and system technologies designed to support large-scale artificial intelligence workloads.

Competitive benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: NVIDIA Corporation; Dell Technologies; Intel Corporation

- Focus on expanding integrated AI supercomputing ecosystems through strategic partnerships spanning semiconductors, networking, software, and cloud infrastructure.

- Invest heavily in research and development to deliver next-generation GPUs, high-speed interconnects, liquid-cooled architectures, and scalable software platforms

- Strong global presence, established customer base, and advanced expertise in accelerated computing support market leadership.

- Ability to deliver secure, high-performance, and end-to-end AI supercomputing platforms for large-scale AI and scientific workloads.

- Dependence on complex product portfolios and established supply chains can slow adaptation to rapidly evolving AI and accelerator technologies.

- Large operational structures may reduce agility and extend product development and deployment timelines compared to emerging competitors.

Emerging Players: Super Micro Computer, Inc., Atos SE

- Develop specialized and cost-effective AI supercomputing solutions tailored to niche applications and specific performance requirements.

- Focus on agility, customization, and rapid innovation to address evolving customer demands

- Faster speed-to-market enables rapid adoption of new accelerator technologies and evolving customer requirements.

- Strong focus on flexible and customer-centric solutions helps differentiate them in specialized AI supercomputing applications

- Limited financial resources and smaller market presence can restrict large-scale expansion and infrastructure investments

- Lower brand recognition and customer trust compared to established global AI and high-performance computing vendors

AI Supercomputing Platforms Market Report Scope

Report Attribute

Details

Market size in 2025

USD 3.5 billion

Estimated market size in 2026

USD 4.3 billion

Projected market size by 2033

USD 20.1 billion

Growth rate

CAGR of 24.7% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Offering, application, component, deployment mode, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; India; Japan; Australia; South Korea; Brazil; UAE; South Africa; KSA

Key companies profiled

Dell Technologies; Advanced Micro Devices (AMD); Intel Corporation; International Business Machines (IBM) Corporation; Lenovo Group Limited; NVIDIA Corporation; HPE; Super Micro Computer, Inc.; Atos SE (Eviden); Fujitsu Limited

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global AI Supercomputing Platforms Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global AI supercomputing platforms market report based on offering, application, component, deployment mode, end use, and region:

-

Offering Outlook (Revenue, USD Million, 2021 - 2033)

-

Hardware

-

Software

-

Services

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Large Language Model (LLM) Training

-

Generative AI

-

Scientific Research and Simulation

-

Computer Vision

-

AI Model Inference

-

Natural Language Processing

-

Autonomous Systems

-

Others

-

-

Deployment Mode Outlook (Revenue, USD Million, 2021 - 2033)

-

On-Premises

-

Cloud

-

Hybrid

-

-

Component Outlook (Revenue, USD Million, 2021 - 2033)

-

Compute Systems

-

Accelerators

-

Networking and Interconnect Solutions

-

Storage Systems

-

Memory Systems

-

Cooling Infrastructure

-

Others

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

IT & Telecommunication

-

Healthcare and Life Sciences

-

Government and Public Sector

-

Automotive and Transportation

-

BFSI

-

Education and Research

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

North America AI Supercomputing Platform Opportunity Assessment for a Data Center Infrastructure Provider

AI supercomputing demand assessment across the U.S. and Canada

Benchmarking of hyperscale, enterprise, and government investments in GPU clusters

Identified high-growth regional opportunities

Supported product and go-to-market strategy for AI infrastructure solutions

Competitive Benchmarking and Product Positioning Strategy for an AI Hardware Manufacturer

Analysis of GPU density, networking technologies, cooling systems, and software stacks

Evaluation of pricing, performance, and deployment models

Identified product/Platform differentiation opportunities

Supported next-generation platform development

Frequently Asked Questions About This Report

North America dominated with a 40.5% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The hardware segment held the highest market share over 71.0% in 2025, while software is growing significantly.

The large language model segment accounted for the largest share over 30.0% in 2025, while generative AI is growing significantly.

The on-premises segment held the highest market share over 57.0% in 2025.

The global AI supercomputing platforms market size was estimated at USD 3.5 billion in 2025 and is expected to reach USD 4.3 billion in 2026.

The global AI supercomputing platforms market is expected to grow at a compound annual growth rate of 24.7% from 2026 to 2033 to reach USD 20.1 billion by 2033.

Key factors include the rapid expansion of generative AI and large language models, increasing investments in hyperscale AI data centers and sovereign AI initiatives, and continuous technological advancements in GPUs, high-speed networking, storage, and liquid-cooling infrastructure worldwide.

Some key players operating in the AI supercomputing platforms market include NVIDIA Corporation, Hewlett Packard Enterprise (HPE), Dell Technologies, Advanced Micro Devices (AMD), Intel Corporation, International Business Machines (IBM) Corporation, Lenovo Group Limited, Super Micro Computer, Inc., Atos SE (Eviden), Fujitsu Limited, Cisco Systems, Inc., and Oracle Corporation

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.