- Home

- »

- Next Generation Technologies

- »

-

Alternative Data Market Size And Growth Report, 2026-2033GVR Report cover

![Alternative Data Market (2026 - 2033)Report]()

Alternative Data Market (2026 - 2033)

Size, Share & Trends Analysis Report By Data Type (Credit & Debit Card Transactions, Email Receipts), By Industry (Automotive, BFSI), By End Use, By Region, And Segment Forecasts

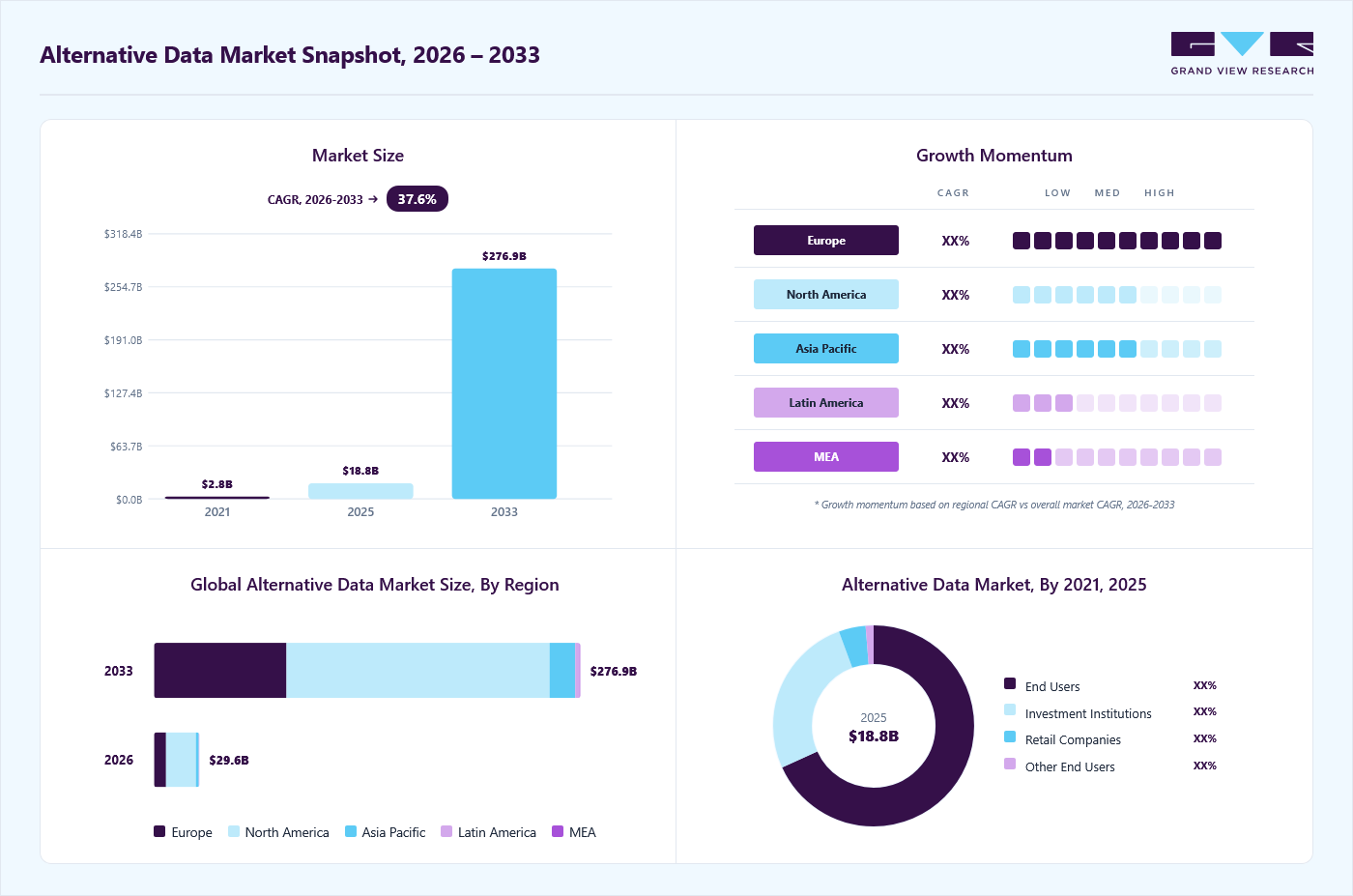

Market Size, 2025

$18.8BMarket Estimate, 2026

$29.6BMarket Forecast, 2033

$276.9BCAGR, 2026–2033

37.6%Alternative Data Market Summary

The global alternative data market size was estimated at USD 18.8 billion in 2025 and is projected to grow from USD 29.6 billion in 2026 to USD 276.9 billion by 2033, growing at a CAGR of 37.6% from 2026 to 2033. The North America market held the largest share of 65.89% of the global market in 2025. The growing use of alternative data in investment and financial services drives market growth.

Key Market Trends & Insights

- By data type: The credit & debit card transactions segment led the market with the largest revenue share of 17.60% in 2025.

- By industry: The BFSI segment led the market with the largest revenue share of 16.72% in 2025.

- By end use: The hedge fund operators segment led the market with the largest revenue share of 67.66% in 2025.

Regional Highlights

- Largest regional market: North America (65.89% revenue share, 2025)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 18.8 Billion

- Estimated market size in 2026: USD 29.6 billion

- Projected market size by 2033: USD 276.9 billion

- CAGR (2026-2033): 37.6%

Hedge funds, asset managers, and institutional investors are using alternative data to gain unique insights that give them an edge in the market. With access to datasets such as foot traffic in retail stores, sentiment analysis from social media, or geolocation data, investors make more accurate predictions about market trends and company performance. This real-time data allows for more agile decision-making in investment strategies, which is critical in the financial sector. According to the 2023 State of Alternative Credit Data Report, 62% of financial institutions utilize alternative data to enhance risk profiling and improve their credit decision-making processes.")

The expansion of artificial intelligence (AI) and machine learning technologies is further fueling the growth of the alternative data market. These technologies enable businesses to analyze large, complex datasets more efficiently and derive actionable insights. Alternative data sources, which are often unstructured and come from various formats, are processed and analyzed with the help of AI to uncover patterns and trends that were previously difficult to detect. As AI and machine learning become more sophisticated, they enhance the value of alternative data by providing deeper insights faster, encouraging more companies to adopt alternative data solutions to stay ahead of their competition.

In addition, the growing volume of data generated from digital transformation and the Internet of Things (IoT) is significantly contributing to the expansion of the alternative data market. With the rapid increase in connected devices, sensors, and online activities, vast amounts of data are generated daily. When analyzed properly, this data provides companies with a deeper understanding of consumer behaviors, market trends, and operational efficiencies. In particular, the proliferation of IoT devices develops new streams of alternative data that businesses use to gain real-time insights. As digital transformation continues to accelerate across industries, the availability of alternative data will grow, further driving demand for tools and platforms to process and analyze these new data sources effectively.

Furthermore, the rise of sustainable and ESG (Environmental, Social, and Governance) investing is also fueling demand for alternative data. Investors and companies are under increasing pressure to demonstrate their commitment to sustainability, and alternative data provides the metrics needed to evaluate ESG factors effectively. For instance, satellite data track deforestation rates, water usage, or pollution levels near manufacturing plants, while social media can provide insight into public sentiment on sustainability practices. As more investors adopt ESG-focused strategies, they rely on alternative data to measure companies' true environmental and social impact, driving further growth in the alternative data market.

Market Dynamics

As organizations prefer non-traditional data sources to improve decision-making, forecasting, and competitive intelligence, the demand for alternative data solutions is rising across industries. The adoption of AI, machine learning, and advanced analytics is enabling businesses to extract actionable insights from diverse datasets. Demand is expanding across financial services, retail, healthcare, and telecommunications sectors. However, stringent data privacy regulations and compliance requirements remain key challenges. Meanwhile, rapid digitalization and growing data availability in emerging markets are creating significant growth opportunities for market participants.

Organizations in various industries are increasingly using alternative data to better understand customer behavior, market trends, supply chains, and competitors. Unlike traditional sources, alternative data such as web traffic, social media sentiment, geolocation, app usage, and transaction data offer real-time, detailed insights that enable more informed decisions. As competition grows, companies are investing in advanced analytics to turn diverse data into actionable intelligence.

The focus on data-driven decision-making is accelerating the use of alternative data among businesses. Companies use these datasets to improve demand forecasting, optimize pricing, enhance marketing, identify new opportunities, and reduce operational risks. As digital transformation expands worldwide, demand for alternative data will continue to grow, making it essential for organizations aiming to increase agility and stay competitive.

Stringent data privacy regulations and compliance requirements pose a significant challenge to the growth of the alternative data market. Alternative data providers often collect and process large volumes of consumer and business information, thus making them subject to strict regulations governing data usage, storage, sharing, and consent. Various regions have implemented stringent data privacy and protection regulations governing the collection, storage, and use of consumer data. For instance, Europe has implemented the General Data Protection Regulation (GDPR), one of the world's most comprehensive data privacy frameworks, while the U.S. has enacted regulations such as the California Consumer Privacy Act (CCPA) to strengthen consumer data rights. Compliance with these regulations requires organizations to obtain user consent, ensure data transparency, and maintain robust data governance practices, thereby increasing operational complexity and compliance costs for alternative data providers and limiting access to certain datasets.

Emerging markets offer significant growth potential for the alternative data sector, driven by the rise of unconventional data sources and rapid digital adoption. Traditional financial and economic data often overlook the complexities of these economies, where diverse consumer behavior, informal activities, cultural factors, and limited reporting create information gaps. Alternative data, such as mobile usage, digital payments, social media, satellite imagery, and supply chain records, enables organizations to better understand market trends and identify investment opportunities.

The expansion of digital economies, increased internet access, and the wider use of advanced analytics and AI are enabling businesses and investors to extract value from alternative datasets. Moreover, financial institutions and policymakers are using alternative data to improve decision-making, assess creditworthiness, identify new opportunities, and improve market forecasting in developing regions. As data ecosystems mature in emerging economies, demand for alternative data solutions is expected to grow significantly.

Analyst Perspective

The alternative data market is evolving from a niche investment research tool into a strategic intelligence resource for a broad range of industries. Market participants are increasingly focusing on enhancing data quality, coverage, and integration capabilities to deliver more actionable insights. The competitive landscape is witnessing growing collaboration between data providers, analytics firms, and technology companies to develop industry-specific solutions. In addition, advancements in data processing technologies are improving the usability of complex and unstructured datasets. As enterprises continue to prioritize real-time intelligence and predictive decision-making, alternative data is expected to become an integral component of modern business and risk management strategies.

Data Type Insights

Based on data type, the market is segmented into credit & debit card transactions, email receipts, geo-location (foot traffic) records, mobile data type usage, satellite & weather data, social & sentiment data, web scraped data, web traffic, and other data types. The credit & debit card transactions segment led the market with the largest revenue share of 17.60% in 2025. The increased use of card transaction data for credit risk assessment drives market growth. Financial institutions and lenders are using credit and debit card data as an additional information layer to assess potential borrowers' creditworthiness.

Traditional credit scoring methods often overlook valuable consumer behavior insights that card transactions can provide, such as spending habits, cash flow patterns, and financial stability. By incorporating card transaction data, lenders develop more accurate credit models, reduce default risks, and extend credit to underbanked or thin-file customers. This shift towards more data-driven credit assessments fuels the demand for transaction-based alternative data in the financial services sector. According to an article published by The Federal Reserve, the rise in credit and debit card usage between 2022 and 2023 led to over 60% of monthly payments being made with credit cards (32%) and debit cards (30%).

The social & sentiment data segment is anticipated to grow significantly with a CAGR of 67.0% over the forecast period. The growth is attributed to the rising demand for smartphone usage from the retail industry. Retail companies utilize it to analyze the user’s e-commerce data type usage patterns. Further, retailers increasingly use sentiment data from social media websites to understand user interests from various groups and regions. Geolocation (foot traffic) from satellite images is also gaining popularity in analyzing customer store visits at a particular time and day, framing the operational strategies for operating the stores. Although these sources have low accuracy compared to transaction data, the companies are finding ways to connect the dots to derive insights.

Industry Insights

Based on industry, the market is segmented into automotive, BFSI, energy, industrial, IT & telecommunications, media & entertainment, real estate & construction, retail, transportation & logistics, and other industries. The BFSI segment led the market with the largest revenue share of 16.72% in 2025. The increasing use of alternative data for fraud detection and prevention drives the segment growth in the alternative data market.

In the BFSI sector, fraudulent activities such as identity theft, money laundering, and unauthorized transactions pose significant threats. To combat these, financial institutions leverage alternative data from various sources, including geolocation data, mobile device usage patterns, and behavioral analytics, to detect real-time anomalies. This ability to track non-traditional data points helps banks and insurance companies identify unusual activities that might go unnoticed by traditional monitoring systems. The need for robust fraud prevention strategies, especially in the age of digital payments, is pushing demand for alternative data solutions within the BFSI sector.

The retail segment is expected to grow significantly from 2025 to 2030. The expansion of e-commerce and omnichannel strategies is also fueling the adoption of alternative data in the retail sector. As more consumers shop online and through multiple channels, retailers seek alternative data to track and analyze customer behavior across various touchpoints. This includes data from mobile apps, online searches, and in-store foot traffic, which helps retailers create a seamless shopping experience across platforms. Integrating alternative data into e-commerce strategies also supports personalized product recommendations, dynamic pricing, and targeted advertising, which are critical for increasing conversion rates in the highly competitive retail landscape. According to a survey conducted by Harvard Business Review in 2023, around 62% of retailers globally had adopted omnichannel strategies, including services such as click-and-collect, online-to-offline (O2O) marketing, and integrated customer service systems.

End Use Insights

Based on end users, the industry is divided into hedge fund operators, investment institutions, retail companies, and other end users. The hedge fund operators segment led the market with the largest revenue share of 67.66% in 2025. The increased integration of natural language processing (NLP) and sentiment analysis in investment decision-making drives market growth. Hedge funds leverage alternative data from news articles, earnings call transcripts, and social media posts to gauge sentiment around companies, sectors, or economic conditions. NLP tools enable funds to analyze these large, unstructured datasets and extract valuable insights into market sentiment, investor confidence, or public perception. By using these insights, hedge funds can adjust their portfolios in response to shifts in sentiment, allowing them to react more swiftly to market-moving events.

The retail segment is expected to emerge as the fastest-growing segment over the forecast period. The growing need for enhanced customer insights and personalized marketing drives market growth. Retailers increasingly recognize that traditional data sources, such as sales figures and demographic information, often fail to provide a comprehensive understanding of customer preferences and behaviors. Retailers gain deeper insights into consumer sentiment and purchasing behavior by leveraging alternative data, such as social media interactions, online reviews, and web traffic analytics. This data enables retailers to tailor their marketing strategies, optimize product end users, and create personalized shopping experiences that resonate with their target audience, ultimately driving sales and customer loyalty.

Regional Insights

North America dominated the alternative data market with the largest revenue share of 65.89% in 2025. The rise of the gig economy and freelance work is influencing the alternative data market in North America. As more individuals engage in gig work or freelance opportunities, businesses are increasingly interested in understanding the dynamics of this labor market. Alternative data can provide insights into gig worker availability, preferences, and income patterns, allowing companies to align their strategies with this evolving workforce better. The need to adapt to these changes fosters a demand for alternative data solutions that can help organizations tap into new opportunities the gig economy presents.

U.S. Alternative Data Market Trends

The alternative data market in the U.S. held the largest share in the North America region in 2025. The Demand for alternative data in the U.S. is experiencing significant growth due to rise of fintech. As financial technology companies innovate and disrupt traditional banking and financial services, they increasingly rely on alternative data to assess creditworthiness and mitigate risk. For instance, fintech firms often use non-traditional data sources such as payment histories, utility bills, and even social media behavior to evaluate borrowers who may lack comprehensive credit histories. This approach expands access to credit for underserved populations and enhances the overall efficiency of lending processes.

Asia Pacific Alternative Data Market Trends

Asia Pacific region alternative data market is expected to achieve the fastest CAGR of 68.2% during the forecast period in the market. The growing trend of collaborative consumption is also impacting the alternative data market. As consumers increasingly adopt sharing economies and collaborative consumption models, businesses leverage alternative data to understand these markets' dynamics better. Companies identify emerging trends and consumer preferences by analyzing data related to shared services, peer-to-peer platforms, and subscription models. This understanding allows businesses to tailor their end users and marketing strategies to align with the evolving landscape of consumer behavior, thus capturing new market opportunities.

Key Alternative Data Company Insights

Some of the key players operating in the market include Dataminr and Preqin, among others.

-

Dataminr is a real-time information discovery and alerts company that analyzes publicly available data to provide actionable insights for various industries. Dataminr’s flagship products include Dataminr for News, Dataminr for Risk, Dataminr for Sports, customizable alerts, and alternative data. Moreover, Dataminr has developed partnerships with major platforms such as Twitter, which allows the company to access and analyze vast amounts of real-time data generated on social media. This collaboration enhances Dataminr’s ability to provide accurate and relevant insights, further solidifying its position in the alternative data market.

UBS Evidence Lab and YipitDataare some of the emerging market participants in the target market.

-

YipitData is an alternative data provider primarily delivering insights and analytics from many non-traditional data sources. YipitData's core end users include data derived from various sources, such as consumer transaction data, web scraping, app usage data, and more. By aggregating this information, the company provides detailed market insights to inform investment strategies across multiple sectors, including e-commerce, technology, and consumer goods. YipitData competes with several other firms, such as Quandl, RavenPack, and Second Measure, all end users varying data analytics and insights.

Key Alternative Data Companies

The following key companies have been profiled for this study on the alternative data market.

-

1010Data

-

Advan

-

Dataminr

-

Earnest Analytics

-

M Science

-

Preqin

-

RavenPack

-

Thinknum Alternative Data

-

UBS Evidence Lab

-

YipitData

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (1010Data, Dataminr, Preqin, UBS Evidence Lab, YipitData)

Expand proprietary data assets and diversify alternative data offerings.

Invest in AI, machine learning, and advanced analytics capabilities.

Strengthen strategic partnerships and expand global customer reach.

Strong brand recognition and established market presence.

Extensive historical datasets and broad data coverage.

Large client base and substantial financial resources.

Higher operational and compliance costs.

Slower adoption of niche and emerging data sources.

Exposure to regulatory and data privacy challenges.

Emerging Players (Advan, Earnest Analytics, M Science, RavenPack, Thinknum Alternative Data)

Focus on niche datasets and specialized industry applications.

Develop innovative analytics solutions and tailored offerings.

Leverage agile business models to rapidly respond to market needs.

Faster innovation and product development cycles.

Specialized datasets addressing specific customer requirements.

Greater flexibility in adapting to evolving market trends.

Limited brand recognition and market penetration.

Smaller customer base and revenue streams.

Recent Developments

-

In October 2024, Earnest Analytics, a data analytics company serving investors, businesses, and consulting firms, launched the Earnest Analytics Spend Index (EASI). This EASI is an alternative data-driven assessment of consumer activity by monitoring spending across 89 merchant category codes (MCC) and including thousands of U.S. merchants. The near real-time data is sourced from millions of de-identified U.S. consumers' credit and debit card transactions.

-

In August 2024, Bipsync, a research and workflow automation software provider, announced a data integration partnership with Preqin, a company specializing in alternative assets data, tools, and insights. This collaboration will enable Bipsync users to access the latest Preqin data on investors, private equity, venture capital, hedge funds, and more. The partnership aims to enhance the experience for clients across all asset classes and strategies, including investors, asset allocators, and fund managers, by providing them with top-tier alternative data to improve decision-making.

Alternative Data Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 18.8 billion

Estimated market size in 2026

USD 29.6 billion

Projected market size by 2033

USD 276.9 billion

Growth rate

CAGR of 37.6% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Data type, industry, end use, region

Regional scope

North America; Europe; Asia Pacific; South America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Japan; India; South Korea; Australia; Brazil; Kingdom of Saudi Arabia (KSA); UAE; South Africa

Key companies profiled

1010Data; Advan; Dataminr; Earnest Research; M Science; Preqin; RavenPack; Thinknum Alternative Data; UBS Evidence Lab; YipitData

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Alternative Data Market Report Segmentation

This report forecasts revenue growths at global, regional, as well as at country levels and offers qualitative and quantitative analysis of the market trends for each of the segments and sub-segments from 2021 to 2033. For the purpose of this study, Grand View Research has segmented the global alternative data market based on data type, industry, end use, and region.

-

Data Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Credit & Debit Card Transactions

-

Email Receipts

-

Geo-location (Foot Traffic) Records

-

Mobile Application Usage

-

Satellite & Weather Data

-

Social & Sentiment Data

-

Web Scraped Data

-

Web Traffic

-

Other Data Types

-

-

Industry Outlook (Revenue, USD Billion, 2021 - 2033)

-

Automotive

-

BFSI

-

Energy

-

Industrial

-

IT & Telecommunications

-

Media & Entertainment

-

Real Estate & Construction

-

Retail

-

Transportation & Logistics

-

Other Industries

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Hedge Fund Operators

-

Investment Institutions

-

Retail Companies

-

Other End Use

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

South America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Data Type

Revenue capture definition

Credit & Debit Card Transactions

This segment includes anonymized consumer payment transaction data collected from credit and debit card usage across merchants and service providers. It is used to analyze consumer spending behavior, sales performance, demand trends, and economic activity.

Email Receipts

This segment consists of anonymized purchase confirmation emails and digital receipt data generated from online consumer transactions. It helps organizations track purchasing patterns, brand performance, customer preferences, and e-commerce trends.

Geo-location (Foot Traffic) Records

This segment includes location-based data captured from mobile devices, GPS signals, and digital applications to monitor physical movement and visitation patterns. It is used to assess consumer mobility, store traffic, location attractiveness, and regional activity trends.

Mobile Application Usage

This segment comprises data generated from user interactions, engagement levels, and behavioral activity within mobile applications. It provides insights into app adoption, user retention, digital consumption behavior, and competitive market positioning.

Satellite & Weather Data

This segment includes earth observation imagery, climate information, and weather-related datasets collected through satellites and meteorological systems. It supports forecasting, operational planning, agricultural monitoring, commodity analysis, and environmental risk assessment.

Social & Sentiment Data

This segment covers data derived from social media platforms, online discussions, reviews, and digital communication channels. It is used to measure public opinion, brand perception, market sentiment, and consumer behavior trends.

Web Scraped Data

This segment includes data automatically extracted from websites, online marketplaces, and digital platforms using web scraping technologies. It enables businesses to monitor pricing, competitor activity, product availability, and market intelligence.

Web Traffic

This segment contains data on website visits, user engagement, browsing behavior, and digital interaction metrics. It is used to evaluate online popularity, consumer interest, competitive performance, and digital market trends.

Other Data Types

This segment includes alternative datasets not categorized as standard data types, such as IoT, sensor, blockchain, and proprietary digital datasets. These data sources provide specialized insights tailored to unique analytical and industry requirements.

Segment - Industry

Revenue capture definition

Automotive

Includes automotive manufacturers, suppliers, dealerships, and mobility service providers utilizing alternative data to analyze consumer demand, vehicle sales, supply chain performance, and market trends.

BFSI

Includes banks, financial institutions, insurance companies, asset managers, hedge funds, and investment firms leveraging alternative data for investment analysis, risk assessment, fraud detection, and customer insights.

Energy

Comprises oil & gas companies, utilities, renewable energy providers, and energy traders using alternative data to monitor production activities, demand patterns, weather impacts, and infrastructure performance. These insights support operational efficiency and investment decisions.

Industrial

Includes manufacturing companies and industrial enterprises utilizing alternative data to optimize production planning, monitor supply chains, assess market demand, and improve operational performance.

IT & Telecommunications

Covers technology companies, software providers, internet platforms, and telecom operators using alternative data to analyze customer behavior, network performance, digital adoption trends, and competitive dynamics. The data support product development and customer engagement strategies.

Media & Entertainment

Includes streaming platforms, publishers, broadcasters, gaming companies, and digital media firms leveraging alternative data to understand audience preferences, content performance, and consumer engagement.

Real Estate & Construction

Comprises real estate developers, property managers, construction firms, and investors using alternative data to assess property demand, site selection, market trends, and construction activity. The data improves investment planning and project evaluation.

Retail

Includes retailers, e-commerce companies, consumer goods manufacturers, and brands utilizing alternative data to track consumer spending, shopping behavior, pricing trends, and market demand.

Transportation & Logistics

Covers logistics providers, freight operators, shipping companies, and transportation firms using alternative data to monitor fleet activity, shipping volumes, route efficiency, and supply chain movements.

Other Industries

Includes healthcare, agriculture, education, hospitality, government, and other sectors utilizing alternative data for market intelligence, operational improvements, and strategic decision-making.

Segment - End Use

Revenue capture definition

Hedge Fund Operators

Includes hedge funds and alternative investment managers that utilize alternative data to identify investment opportunities, generate alpha, and enhance trading strategies. These organizations leverage non-traditional datasets to gain insights beyond conventional financial information.

Investment Institutions

Comprises asset management firms, mutual funds, pension funds, private equity firms, investment banks, and other institutional investors using alternative data for portfolio management, risk assessment, and market analysis.

Retail Companies

Includes brick-and-mortar retailers, e-commerce companies, and consumer brands utilizing alternative data to understand consumer behavior, monitor market trends, optimize pricing strategies, and improve inventory management.

Other End Use

Includes corporations, consulting firms, research organizations, government agencies, and academic institutions leveraging alternative data for business intelligence, operational planning, competitive analysis, and strategic decision-making.

Estimation Model

Name

Key Question

Description

Macroeconomic & Digital Infrastructure Indicators

What macroeconomic and digital trends support alternative data adoption?

Assesses GDP growth, digital transformation spending, internet penetration, cloud adoption, AI investments, and enterprise data consumption trends that drive demand for alternative data solutions.

End-Use Industry Adoption

Which industries are adopting alternative data solutions?

Evaluates adoption across financial services, retail & e-commerce, healthcare, telecommunications, manufacturing, and other enterprise sectors utilizing alternative data for business intelligence and decision-making.

Data Type & Solution Penetration

Which alternative data types and analytics solutions are being utilized?

Measures adoption of transaction data, web and social media data, geolocation data, mobile app data, sensor/IoT data, satellite imagery, and analytics platforms across end users.

Revenue Mapping & Market Validation

How much revenue is generated from alternative data products and services?

Analyzes revenues of alternative data providers, subscription-based data platforms, and analytics vendors, followed by primary interviews and data triangulation to determine the final market.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Assessment of alternative data adoption across key end-use industries

Detailed analysis of adoption trends, use cases, and spending patterns across financial services, retail, healthcare, and telecommunications sectors.

Helped identify high-growth industry segments and revenue opportunities.

Impact analysis of AI and advanced analytics on alternative data adoption

Detailed evaluation of AI-driven data processing, predictive analytics, and automation trends shaping the market.

Enabled informed technology investment and product development decisions.

Analysis of regulatory and compliance landscape

Customized assessment of data privacy regulations, compliance requirements, and their impact on alternative data collection and utilization.

Enabled clients to mitigate regulatory risks and strengthen compliance strategies.

Frequently Asked Questions About This Report

The global alternative data market size was estimated at USD 18.8 billion in 2025 and is expected to reach USD 29.6 billion in 2026.

The global alternative data market is expected to grow at a compound annual growth rate of 37.6% from 2026 to 2033 to reach USD 276.9 billion by 2033.

The credit & debit card transactions segment led with a 17.60% revenue share in 2025, and is the fastest growing data type.

Some key players operating in the alternative data market include 1010Data, Advan, Dataminr, Earnest Research, M Science, Preqin, RavenPack, Thinknum Alternative Data, UBS Evidence Lab, and YipitData.

Asia Pacific is the fastest growing over the forecast period.

The BFSI segment led with a 16.7% revenue share in 2025, and is the fastest growing industry.

North America dominated with a 65.9% revenue share in 2025.

The hedge fund operators segment led with a 67.6% revenue share in 2025, and retail companies is the fastest growing industry.

As organizations prefer non-traditional data sources to improve decision-making, forecasting, and competitive intelligence, the demand for alternative data solutions is rising across industries. The adoption of AI, machine learning, and advanced analytics is enabling businesses to extract actionable insights from diverse datasets.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.